A liquor company exits a cricket franchise at a 36x gain. A conglomerate, a media house, an American sports investor, and a global private equity giant step in. This is not just a sports story.

The Deal

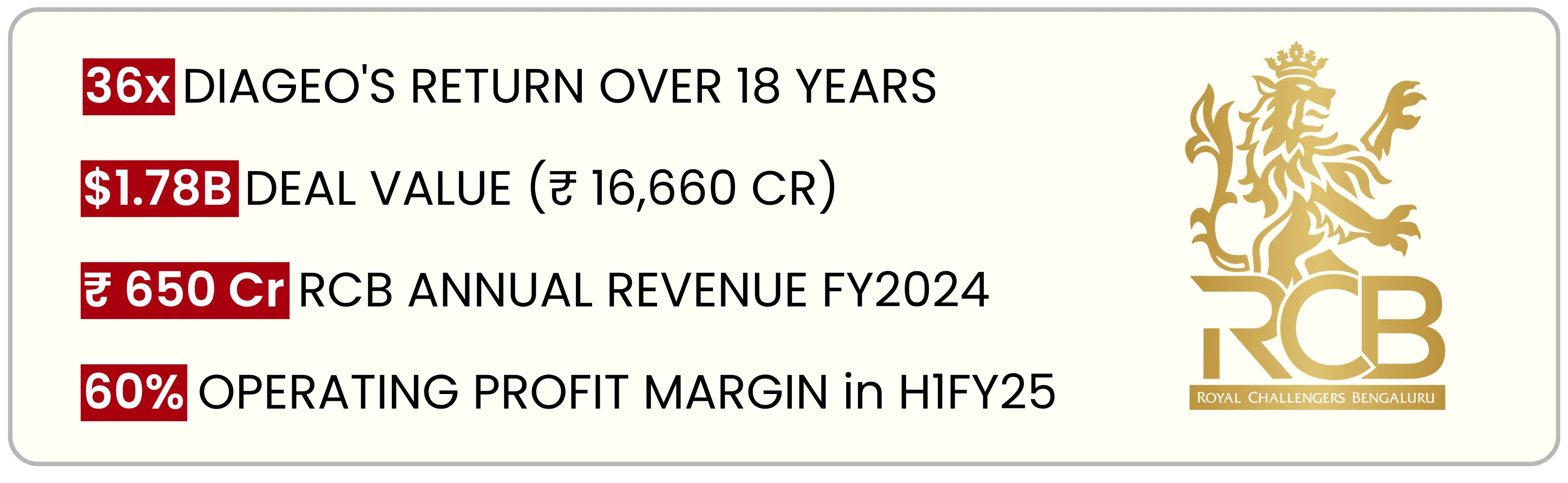

On March 24, 2026, United Spirits Limited (USL) announced the sale of its entire 100% stake in Royal Challengers Sports Private Limited, the legal entity that owns the Royal Challengers Bengaluru franchise in both the Indian Premier League and the Women's Premier League, to a four-party consortium for ₹16,660 crore, or approximately $1.78 billion. The transaction is structured as a complete, all-cash deal.

The buyer group comprises four organisations: Aditya Birla Group, which is leading the consortium; The Times of India Group, represented by Times Internet Chairman Satyan Gajwani; Bolt Ventures, the sports investment firm of American investor David Blitzer; and BXPE, the perpetual private equity arm of global asset manager Blackstone. Aryaman Vikram Birla, son of Kumar Mangalam Birla and a former Ranji Trophy cricketer who played for Madhya Pradesh, will serve as Chairman. Satyan Gajwani will serve as Vice-Chairman.

To put the scale of this number in context: when Vijay Mallya's United Breweries Group first acquired this franchise in 2008, the price paid was $111.6 million, which at 2008 exchange rates (₹43.5 per USD) translates to roughly ₹454 crore. The 2026 sale price is approximately 36.69 times that original investment in nominal terms.

The Business Model

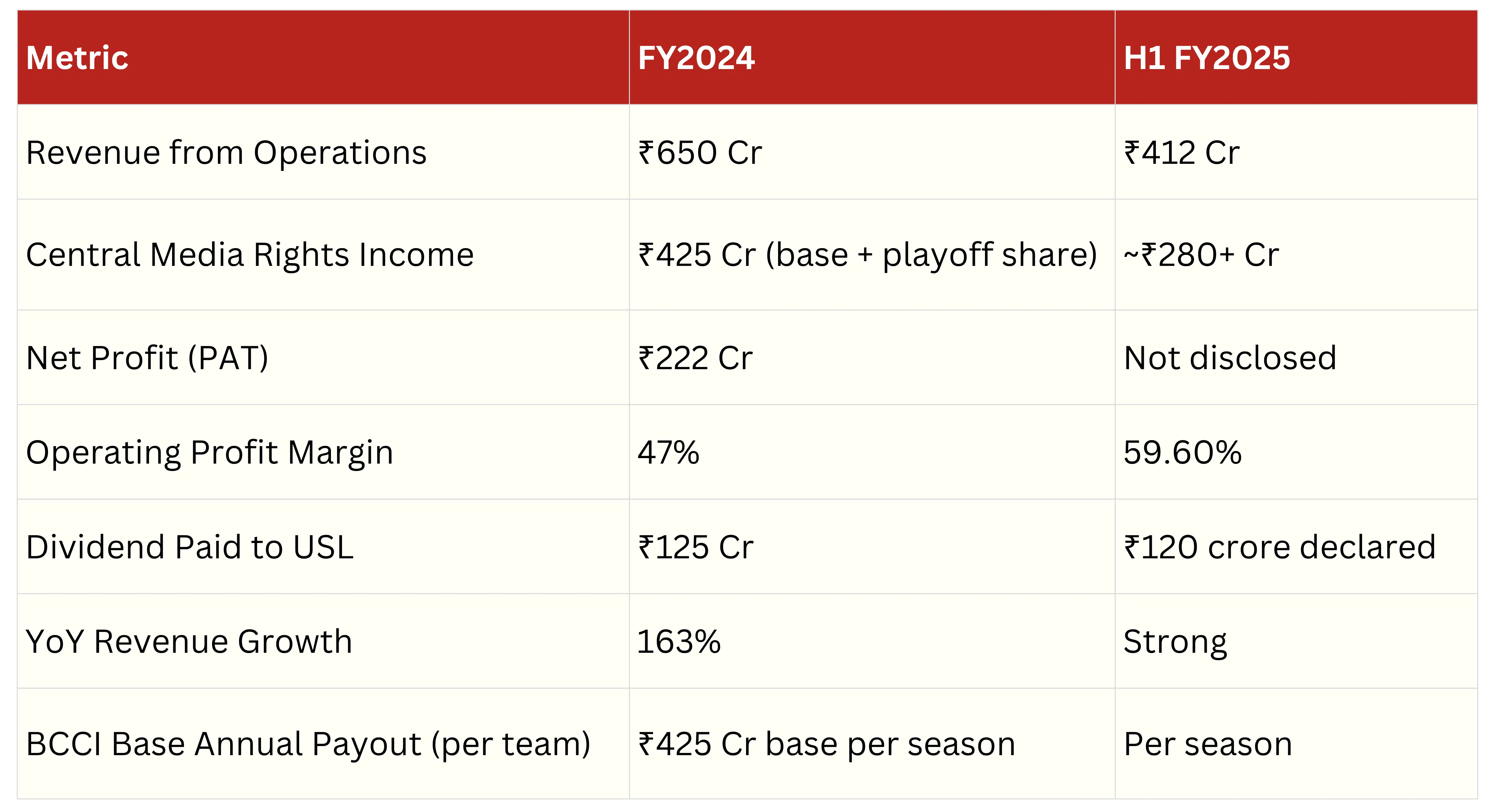

Royal Challengers Sports Private Limited is not a traditional business in the way a factory or a software firm is. It does not manufacture anything, and its core product, cricket, is played only in the summer months. Yet in FY2024, the company recorded ₹650 crore in revenue and a net profit of ₹222 crore, with an operating profit margin that touches 47% for the full year and an extraordinary 60% in the first half of FY2025. To understand how this is possible, one needs to understand where the money comes from.

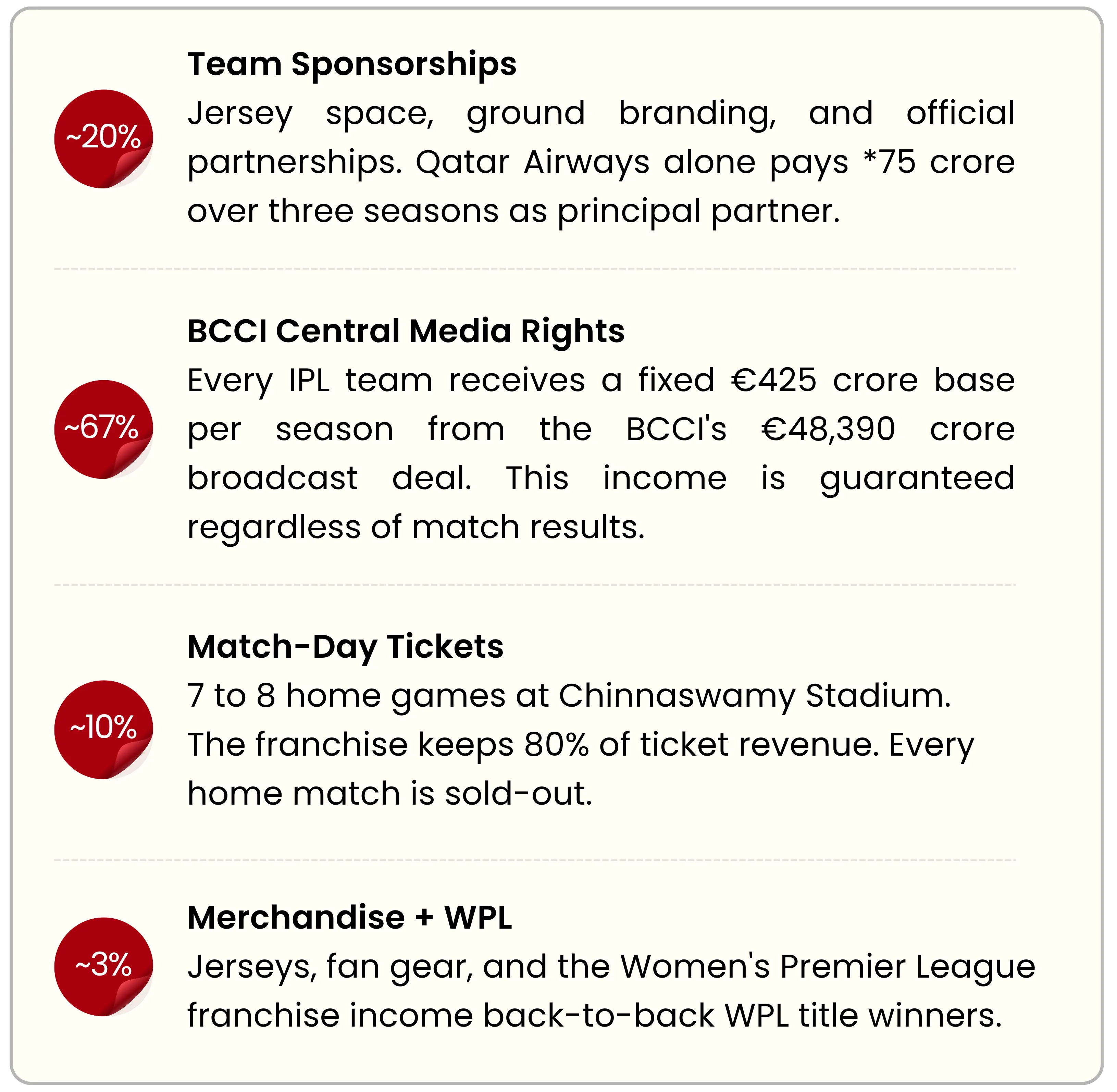

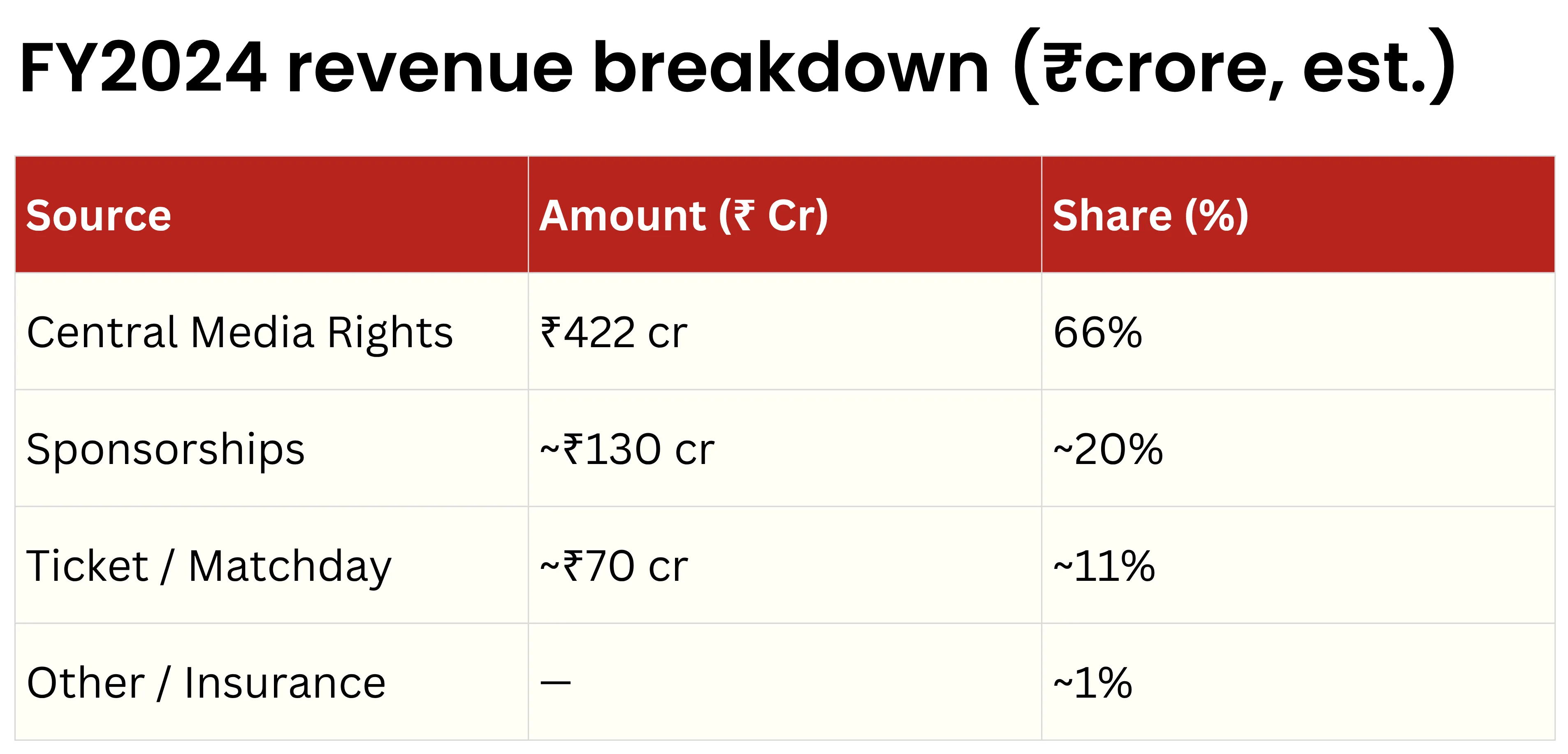

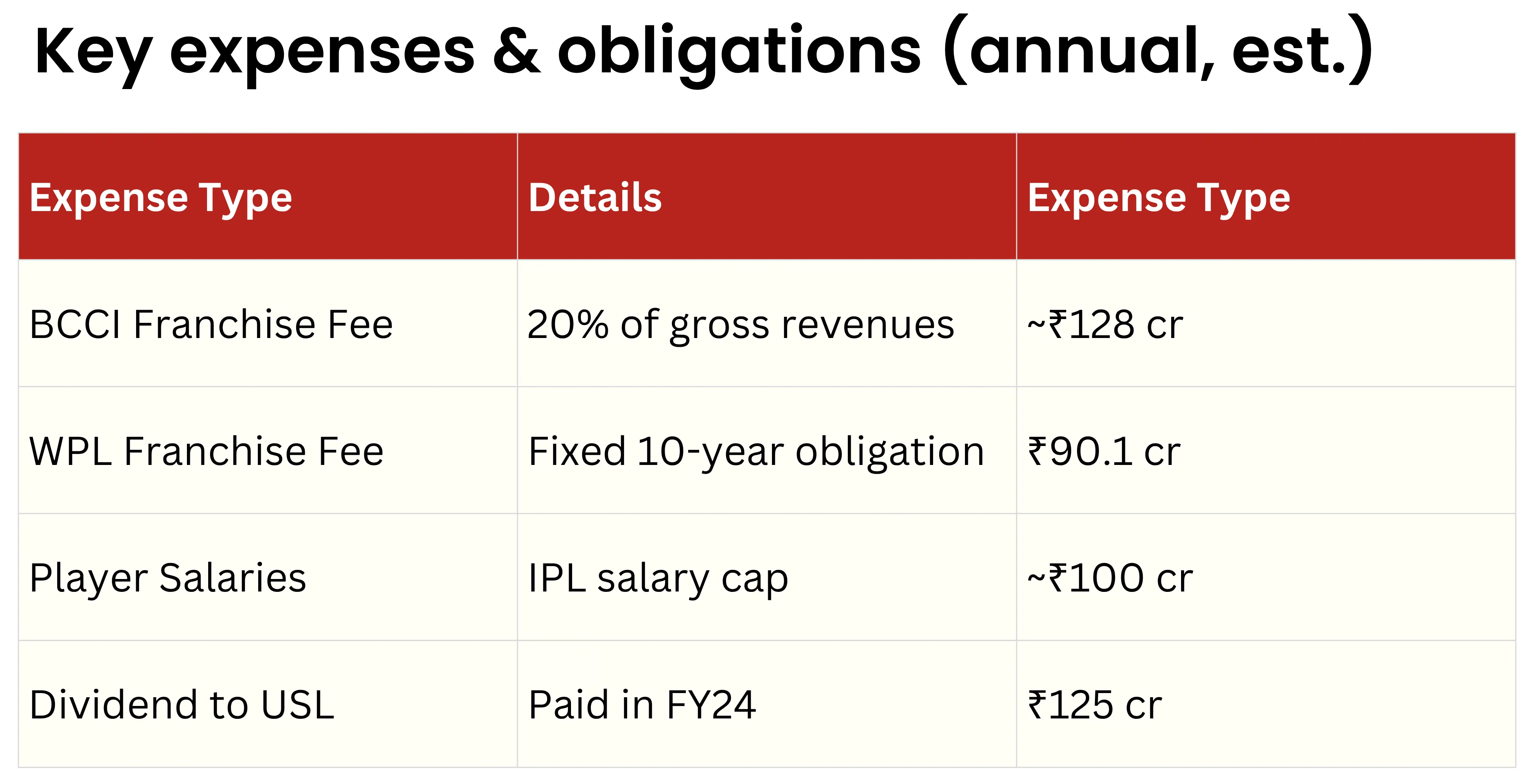

The most important of these, by a significant margin, is the central media rights distribution from the BCCI. When the BCCI sold the broadcasting and streaming rights to IPL in 2022, it fetched ₹48,390 crore for the five-year period from 2023 to 2027. That is approximately ₹9,678 crore per season, shared between the BCCI itself and all ten franchises. Every team receives a base fixed income of around ₹422 to ₹425 crore per season, regardless of performance, as their share of this pool. There is an additional variable component tied to how many matches a team plays in the playoffs. The more RCB advances, the higher the payout.

This structure is fundamentally different from most businesses. For instance, a car company's revenue depends entirely on how many cars it sells. RCB's revenue, to a large degree, is pre-contracted and guaranteed by the BCCI, regardless of whether the team wins or loses. In FY2024, when RCB played 17 matches instead of the usual 12 due to a deeper playoff run, revenues jumped by 163% year-on-year, directly because of that performance premium.

The BCCI, in exchange for these rights, charges each franchise a 20% franchisee fee on gross revenues. This is the cost of being in the league, and it is non-negotiable. What remains after paying this fee, the playing budget, and operational costs is the profit, and the margins, as the numbers above show, are remarkably high for any business.

How Was ₹16,660 Crore Arrived At

The single most important question any investor asks before writing a large cheque is this: given what this business earns today, is the price being paid reasonable? At ₹650 crore in revenue and ₹222 crore in net profit, a valuation of ₹16,660 crore implies that the buyer is paying approximately 26 times annual revenue and 75 times annual profit. In a traditional industry, those multiples would be considered very expensive. But franchise businesses in global sports leagues are not valued like traditional industries, and there are specific reasons why.

The current BCCI media rights cycle, worth ₹48,390 crore, ends in 2027. The next auction, which will cover 2028 onwards, is widely expected to fetch significantly more. When the 2023 cycle was sold, it was a 300% increase over the previous cycle, which had been worth ₹16,347 crore. If even a fraction of that growth rate repeats in 2028, every franchise's guaranteed annual income roughly doubles overnight. The new buyers of RCB are pricing in that expectation. They are not buying a ₹650 crore annual revenue business; they are buying a business that could credibly earn ₹900 crore to ₹1,200 crore per season by FY2030.

The second factor is competitive bidding. Nine parties submitted bids for RCB. Among them were EQT, a Swedish private equity firm, and a consortium led by Ranjan Pai of Manipal Group, which also had KKR and Temasek as backers. Diageo had originally targeted a valuation close to $2 billion. The presence of multiple credible, well-capitalised buyers effectively ran an auction, and the price settled at $1.78 billion, which was broadly where the market cleared.

The third factor is timing. RCB entered this sale process as the reigning IPL champion (2025) and as a two-time WPL title winner. A championship season inflates both brand value and commercial interest. The brand valuation firm Houlihan Lokey had already identified RCB as the foremost brand in the IPL ecosystem in 2025, while Brand Finance ranked it second after Mumbai Indians. These rankings directly affect sponsorship pricing, which in turn affects revenue projections, which in turn affect what the franchise is worth.

What Each Party Gets From This Deal

United Spirits Limited and Diageo

Diageo, the British drinks giant that owns United Spirits Limited, bought RCB for $111.6 million in 2008. The original purchase was made partly as a marketing vehicle for Royal Challenge whisky, an early form of surrogate advertising through cricket sponsorship. As advertising regulations tightened and Diageo's global portfolio strategy evolved, cricket no longer fit the company's core business definition. The exit is strategically clean and financially exceptional.

Aditya Birla Group

For Aditya Birla Group, this is not a financial investment in the conventional sense. Kumar Mangalam Birla explicitly described it as "institution-building," a phrase that signals a multi-decade, legacy-oriented commitment. The group's consumer-facing businesses, including Aditya Birla Capital, Aditya Birla Fashion and Retail, Ultratech Cement, and Birla Sun Life, gain direct exposure to approximately 800 million IPL viewers every season, across television and digital platforms, without buying a single advertisement. That organic brand visibility, priced into the investment rather than billed as an ad spend, is the core commercial logic. Aryaman Birla's appointment as Chairman also reflects a deliberate choice to use RCB as a high-profile, consumer-facing leadership platform for the next generation of Birla Group management.

Times of India Group

The Times Group, through Satyan Gajwani of Times Internet, is buying direct strategic access to one of the largest and most engaged sports fan communities in the world. RCB has over 100 million followers across social media platforms. For a media company building its digital and OTT presence, ownership of a franchise gives preferential content access, exclusive behind-the-scenes rights, and data on hundreds of millions of cricket fans. The Vice-Chairman role also means Times Internet is structurally embedded in how the franchise is managed, not just a passive investor.

Blackstone (BXPE)

Blackstone's entry through BXPE is particularly telling. BXPE is Blackstone's perpetual capital vehicle, which means it does not operate like a traditional private equity fund with a 10-year exit window. Perpetual capital is designed to hold assets indefinitely, collecting steady cash flows while waiting for the right moment to exit at maximum value. RCB's guaranteed BCCI distributions, high margins, and upcoming media rights re-auction make it exactly the kind of asset perpetual capital is designed for: predictable income today, large capital appreciation event in the future. An eventual IPO of the franchise, or a secondary sale to a strategic buyer, could deliver multiples that a traditional PE fund would never wait around to collect.

Bolt Ventures (David Blitzer)

David Blitzer holds stakes in Crystal Palace in the English Premier League, the Philadelphia 76ers and New Jersey Devils in the NBA and NHL respectively, the Washington Commanders in the NFL, the Cleveland Guardians in MLB, and Real Salt Lake in MLS. Adding RCB gives him the most valuable cricket franchise in the most commercially dynamic cricket league in the world. For Blitzer, the IPL is the only major global sports league in which he did not previously have a stake. This is a portfolio completion trade, anchoring him in the one large market, India, that no other global sports ecosystem currently matches for growth trajectory.

The Bigger Picture

The RCB deal did not happen in isolation. On the same day, the Rajasthan Royals franchise was also sold for $1.63 billion. Two IPL franchises changed hands on a single day for a combined value of over $3.4 billion. The overall IPL business is now estimated at approximately $18.5 billion, placing it firmly among the top five sports leagues in the world by enterprise value, alongside the NFL, NBA, Premier League, and the Champions League.

The broader signal from these transactions is that Indian cricket franchises have crossed a threshold. They are no longer marketing tools for conglomerates or vanity purchases by wealthy businessmen. They are now institutionally owned financial assets with predictable revenue, contracted income streams, global brand value, and multiple paths to liquidity. The entry of Blackstone, one of the largest and most disciplined institutional investors in the world, confirms this shift more clearly than any valuation number could.

For investors and market observers watching this from the outside, the most useful takeaway is simple. A business that earns ₹650 crore a year with 47% operating margins, whose revenue is pre-contracted by India's most powerful sports body, and whose media rights income is likely to roughly double in the next auction cycle, is not just a cricket team. It is a high-quality financial asset that happens to play cricket. And a consortium that includes Aditya Birla Group, Blackstone, and The Times of India just paid $1.78 billion to own it.

That price may look high today. History, at least in the IPL, suggests it probably is not.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.