Ever wondered how much your option premium might move if the stock shifts by ₹1? Delta in options trading does exactly that, it measures how much an option’s price will change for every rupee move in the underlying. Simple, yet powerful.

In options trading, Delta offers a snapshot of direction, a hint of probability, and a practical way to estimate P&L all in one concise Greek.

Whether you’re trading calls or puts, understanding Delta is the first step to making sense of price movements.

Understanding Option Delta

| Concept | Details |

|---|---|

| Delta Range (Call Options) | 0 to +1 |

| Delta Range (Put Options) | 0 to –1 |

| Example – Call Option | If Δ = 0.60, a ₹1 rise in stock adds ₹0.60 to the premium |

| Example – Put Option | If Δ = –0.60, a ₹1 rise in stock reduces ₹0.60 from the premium |

| Other Uses of Delta | - Estimates probability of finishing in-the-money - Represents equivalent stock exposure - Indicates direction bias in a portfolio |

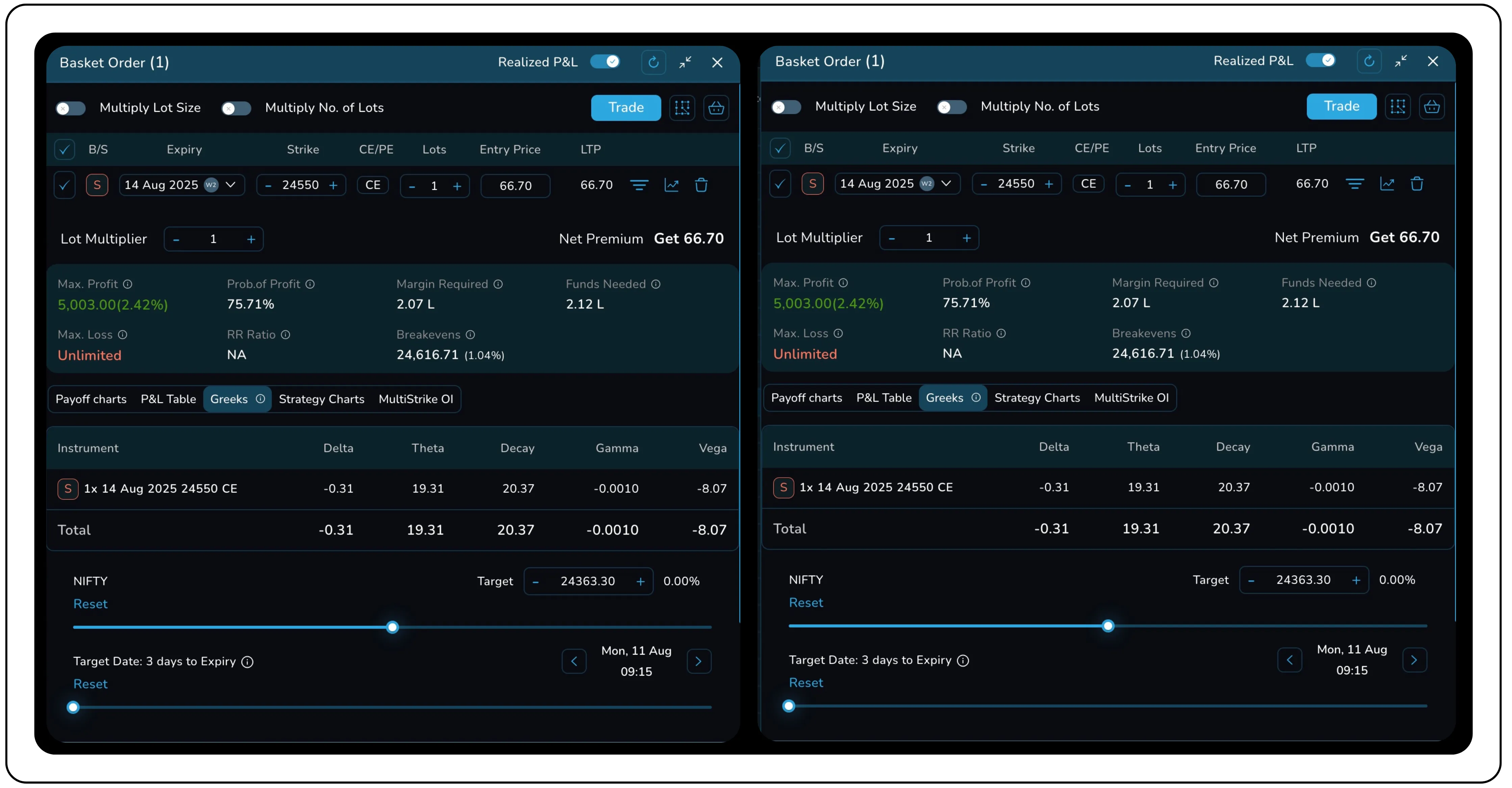

Example setup:

You sell 1 lot of Nifty 24550CE expiring on 14th Aug 2025 (weekly expiry)

Spot Price: 24,363

Strike Price: 24,550 CE

Premium Collected: ₹66.70

Delta: -0.31 (here Delta is negative because we have taken a short position with call option)

Now, if NIFTY moves up by ₹10, here is how Delta plays out:

Change in Premium = Δ × Price Move = -0.31 × ₹10 = - ₹3.10

So the new theoretical premium becomes:

₹66.70 - ₹3.10 = ₹63.60

Profit Realized: ₹3.10 × 75 = ₹232.5 (Nifty lot size = 75)

This Delta also tells us the trade has a 31% chance (as per the Delta approximation) of expiring in-the-money or roughly 69% chance of profitability since the option is slightly OTM.

NOTE: Here, an out-of-the-money (OTM) call option has been sold, meaning the position will be profitable if the option remains OTM at expiry. Since the delta indicates approximately a 31% probability of the strike expiring in-the-money (ITM), it implies a 69% chance that it will remain OTM and thus result in a profit.

What affects Delta?

Delta is not a static figure. It is a derived measure calculated in real time based on several variables affecting the option’s theoretical value. Since Delta reflects how sensitively an option’s price premium reacts to changes in the underlying asset, understanding what drives its fluctuations is crucial to making informed, risk-calibrated decisions in options trading.

The most important determinants of Delta are -

1. Moneyness of the Option

It refers to whether an option is in the money (ITM), at the money (ATM), or out of the money (OTM).

It is the foremost factor influencing Delta because it determines the probability of the option expiring in the money.

- Call Deltas increase as options move deeper into the money (approaching 1.00).

- Put Deltas become more negative as the strike moves into the money (approaching -1.00).

- ATM options exhibit Delta values close to ±0.50, indicating uncertain expiration outcomes.

The same logic applies to the NIFTY 24,550 CE, which sits in the delicate zone between ATM and slightly ITM, hence its Delta is balanced but still responsive.

2. Time to Expiry

Time remaining until expiry has a pronounced impact on Delta. Options with a long time horizon tend to have Delta values closer to ±0.50, regardless of their moneyness.

This is because the greater the time available, the higher the uncertainty about whether the options will end up in the money.

- Shorter-dated options show sharper Delta Transitions.

- Long-dated options have flatter Delta curves, giving traders more leeway and time for directional accuracy.

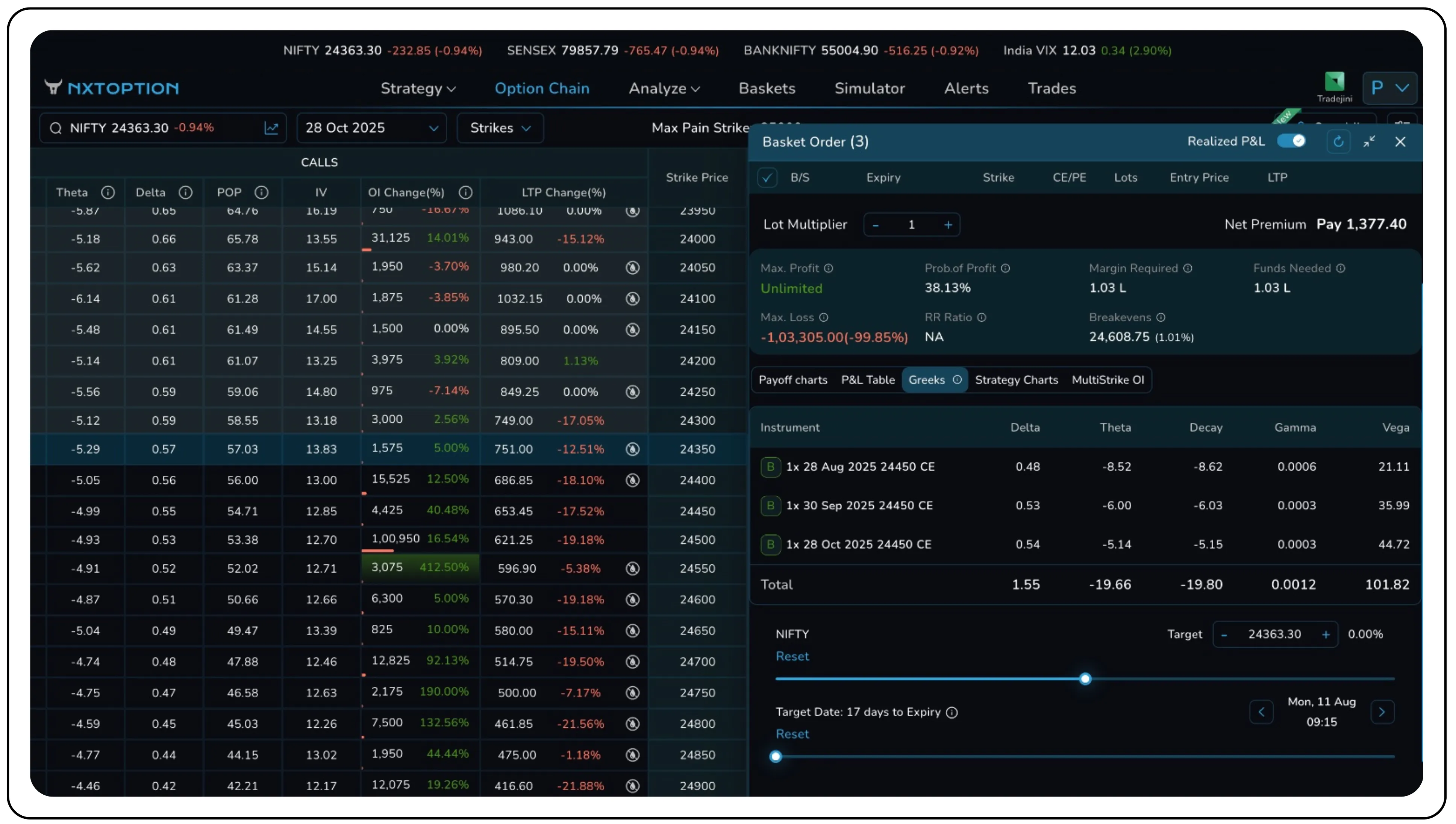

In our NIFTY 24,550 CE sell trade, the expiry is due on 7 August 2025, and the position is evaluated on the morning of expiry day.

As expiry approaches:

- ITM Calls approach Delta = 1.00

- OTM Calls drift toward Delta = 0

- ATM Calls polarise rapidly, often moving from 0.50 to near 1.00 or 0.00

NOTE: This binary-like behaviour makes near-expiry Delta highly sensitive, which is desirable for trades executing expiry trades focused on Theta decay.

In the example above, the 28 Aug 2025 CE expiring at the end of the month of August, has a Delta of 0.48, while the longer-dated 30 Sep and 28 Oct 2025 CEs hold Deltas closer to 0.54. As time to expiry increases, Delta flattens, reflecting more uncertainty and allowing directional trades more time to play out.

3. Implied Volatility

It reshapes the Delta curve by altering the probability landscape.

When IV rises:

- OTM options gain Delta

- ITM options lose some Delta marginally

- The Delta curve becomes flatter

Higher IV stretches the probability distribution, making it more likely that OTM options could expire ITM, increasing their Delta.

For instance, a 24550 CE with a Delta of 0.60 in a low IV environment might shift toward 0.70 if volatility spikes.

When IV falls:

- OTM options lose Delta

- ITM options gain Delta slightly

- Delta curve steepens

Lower IV signals a narrower range of expected outcomes. Far OTM options see their Delta fall toward zero, while ITM options move toward full Delta (±1.00), especially near ATM strikes.

The Call-Put Delta Relationship

The sum of absolute Deltas for corresponding call and put options (same strike and expiry):

The absolute value of Call Delta + The absolute value of Put Delta ≈ 1.00

This relationship holds especially for European-style options, such as those on NIFTY.

For example, if our 24,550 CE has a Delta of 0.60, then 24,550 PE will have a Delta roughly near -0.40.

When to use Delta effectively

Delta becomes particularly significant when expiry is near and the underlying asset is trading close to a key technical level, such as a support or resistance zone.

At this stage, even small price movements can lead to disproportionately large impacts on an option's price due to the combined effects of Delta and Theta.

When Delta hovers around 0.50 to 0.60, the strike is effectively at-the-money or slightly out-of-the-money. This zone represents a point of balance between risk and reward.

Such Delta values are ideal for trades where the outlook is mildly directional but not overly aggressive.

Strategies involving options with mid-range Deltas are often deployed when:

- The market is expected to remain within a well-defined range

- Price action is consolidating near a critical inflection point

- Traders wish to express a view while benefiting from Theta decay

Whether through selling options for income or buying them for a directional move, Delta in this range helps manage exposure, it gives the trader enough "skin in the game" to benefit from movement, while allowing Theta to contribute meaningfully if the market stagnates.

Risk, reward and probability

- Risk - Reward Ratio: Not defined (unlimited risk since naked call)

- Max Profit: ₹5,003

- Margin Required: ₹2.07 Lakh

- Break-even: 24,616.71 (Spot + Premium Received)

- Probability of Profit: 75.71%

For delta hedging and better risk control, view Delta not just as a number but as the cornerstone of informed trading decisions.

As seen in the NIFTY call sell setup, understanding Delta’s -0.60 helped anticipate a fall in premium when the index rose, a perfect expiry play. Pair it with Theta and keep an eye on spot levels, and you will begin trading with clarity, not guesswork.

Track Delta values in real-time and make smarter, more informed trades using Nxtoption.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.