ITC Limited is one of India's foremost private sector companies, recognised for a diverse range of businesses spanning fast moving consumer goods, agri business, paperboards, packaging, hospitality, and information technology, with strong synergies across every vertical ITC Limited employs approximately 36,500 people across more than 60 locations in India, making it one of the country's largest private sector employers.

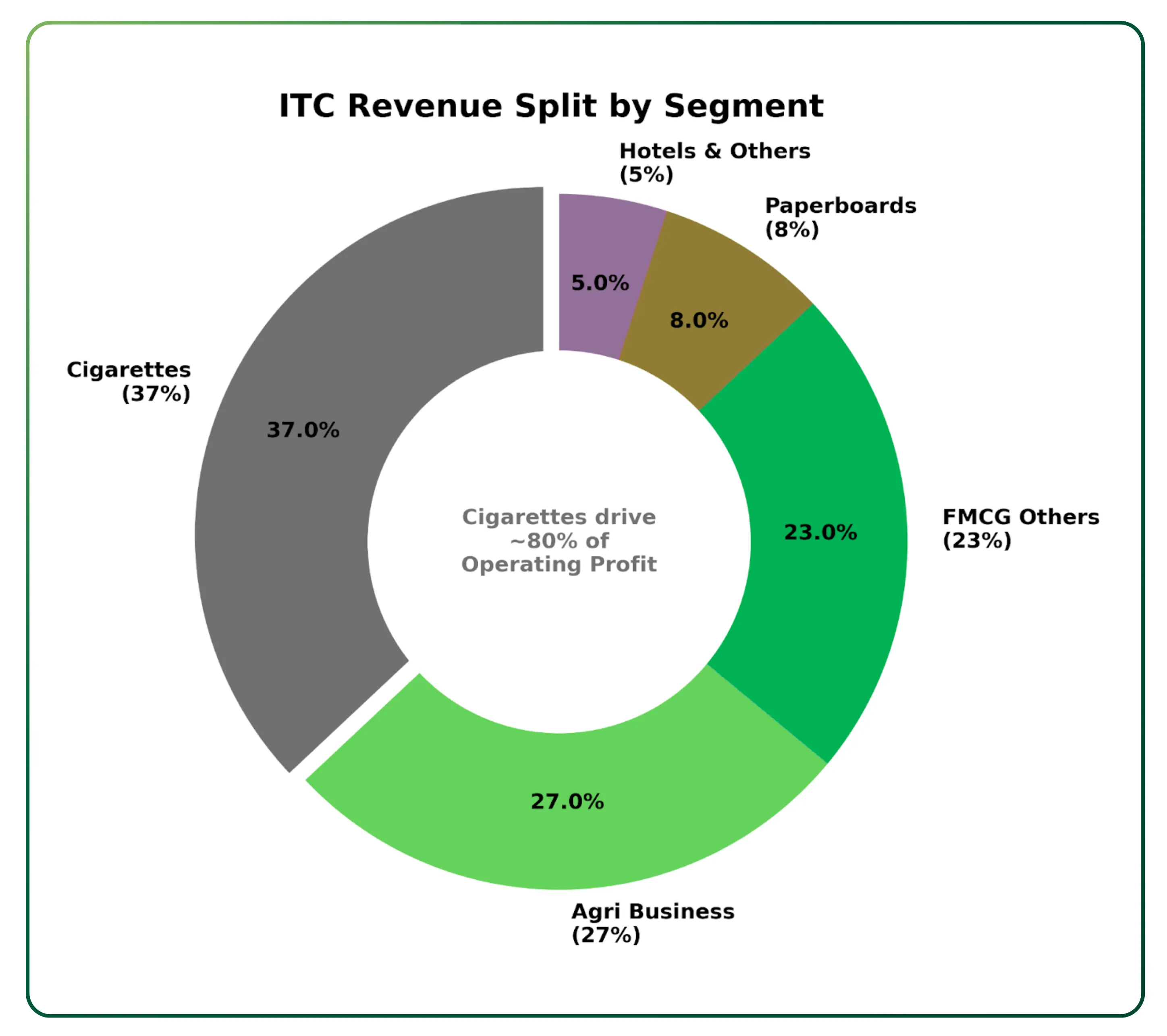

The FMCG Others segment has scaled impressively to contribute 23% of total revenues, driven by household staples, premium personal care, dairy, and a high-growth digital-first organic portfolio. The Agri Business contributes 27% leveraging a strong farm-to-factory model handling millions of tonnes of commodities to drive both domestic value added products like spices and coffee as well as leaf tobacco exports. The paperboards and packaging division accounts for 8% of revenues, operating through a vertically integrated business model with strong backward linkages and sustainable forestry, though currently battling soft domestic realizations and wood shortages.

ITC Limited revenue split by segment, with cigarettes driving approximately 80% of consolidated operating profits across its diverse range of businesses.

ITC Hotels Limited: Demerger and Strategic Realignment

The recent demerger of the hospitality vertical into ITC Hotels Limited, with ITC retaining an approximate 40% stake, has streamlined the balance sheet by removing a capital-intensive segment. ITC Hotels now operates independently, managing a portfolio of premium hotels across India, while continuing to benefit from ITC's brand equity and institutional strengths.

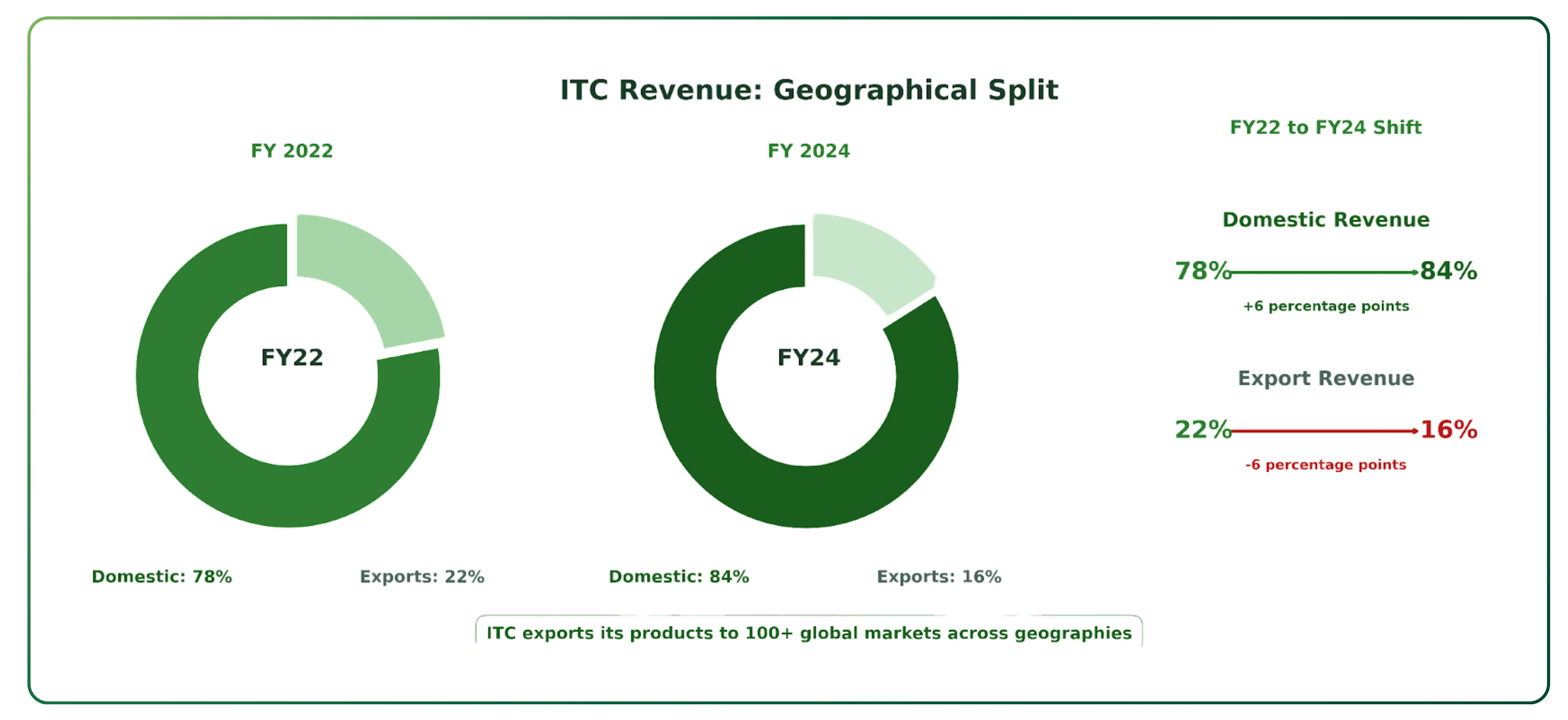

ITC Limited geographical revenue split showing domestic revenues growing from 78% in FY22 to 84% in FY24, driven by rapid scaling of fast moving consumer goods brands across India.

Domestic revenues accounted for 84% of total sales in FY24, up from 78% in FY22, reflecting the rapid scaling of FMCG brands and strong domestic demand across categories. Exports contributed 16% in FY24 versus 22% in FY22, driven primarily by the Agri Business segment which exports leaf tobacco, spices, and marine products to over 100 global markets.

Operating Performance and Growth

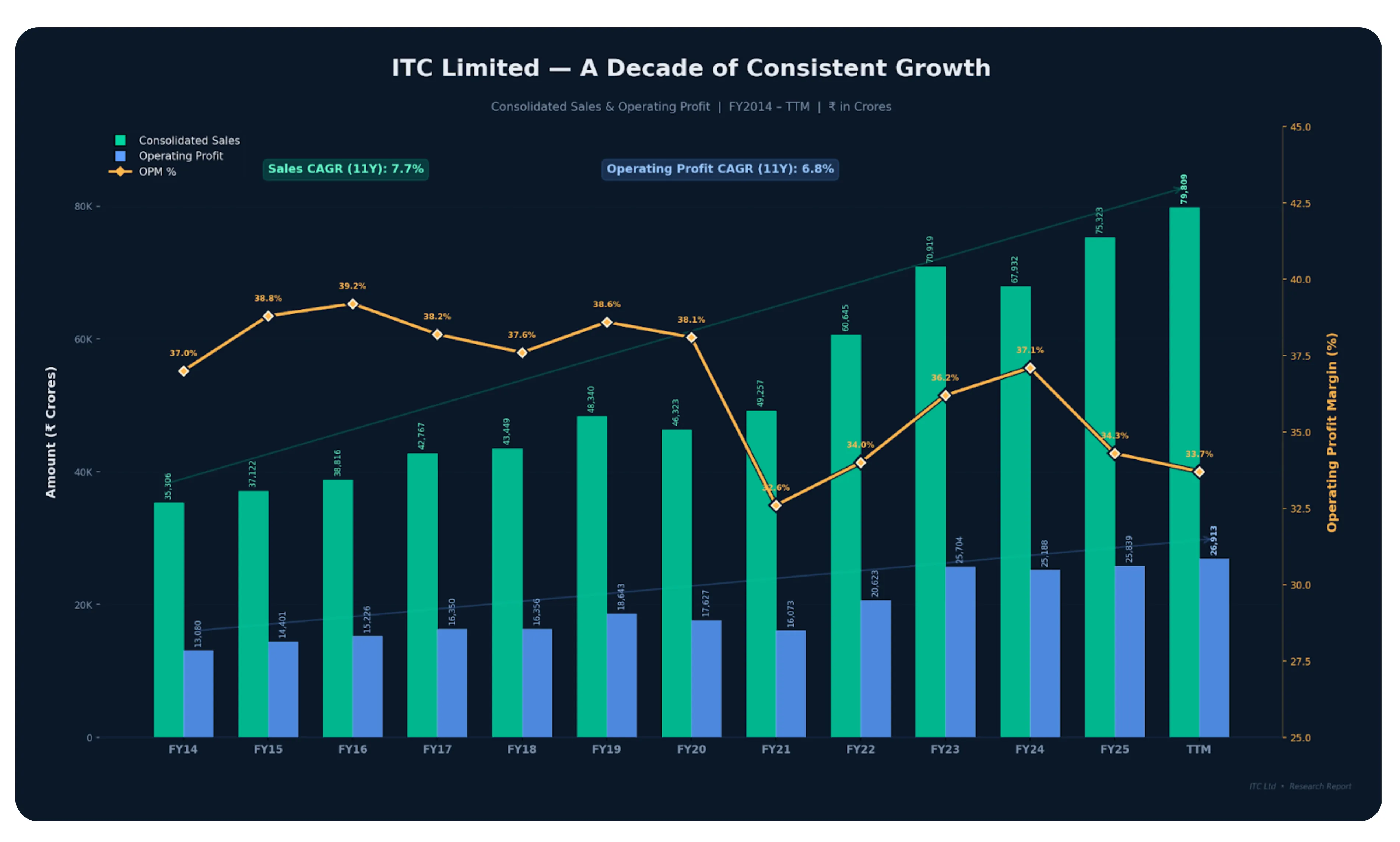

The company has demonstrated consistent growth over the past decade. Consolidated sales increased from Rs 35,306 crores in March 2014 to Rs 79,809 crores on a trailing twelve month basis. During the same period, operating profit grew from Rs 13,080 crores to Rs 26,913 crores. Operating profit margins have remained remarkably stable between 34 and 39% throughout the decade.

ITC Limited consolidated sales and operating profit growth over a decade, reflecting a sales CAGR of 7.7% and operating profit CAGR of 6.8% driven by its diverse range of businesses.

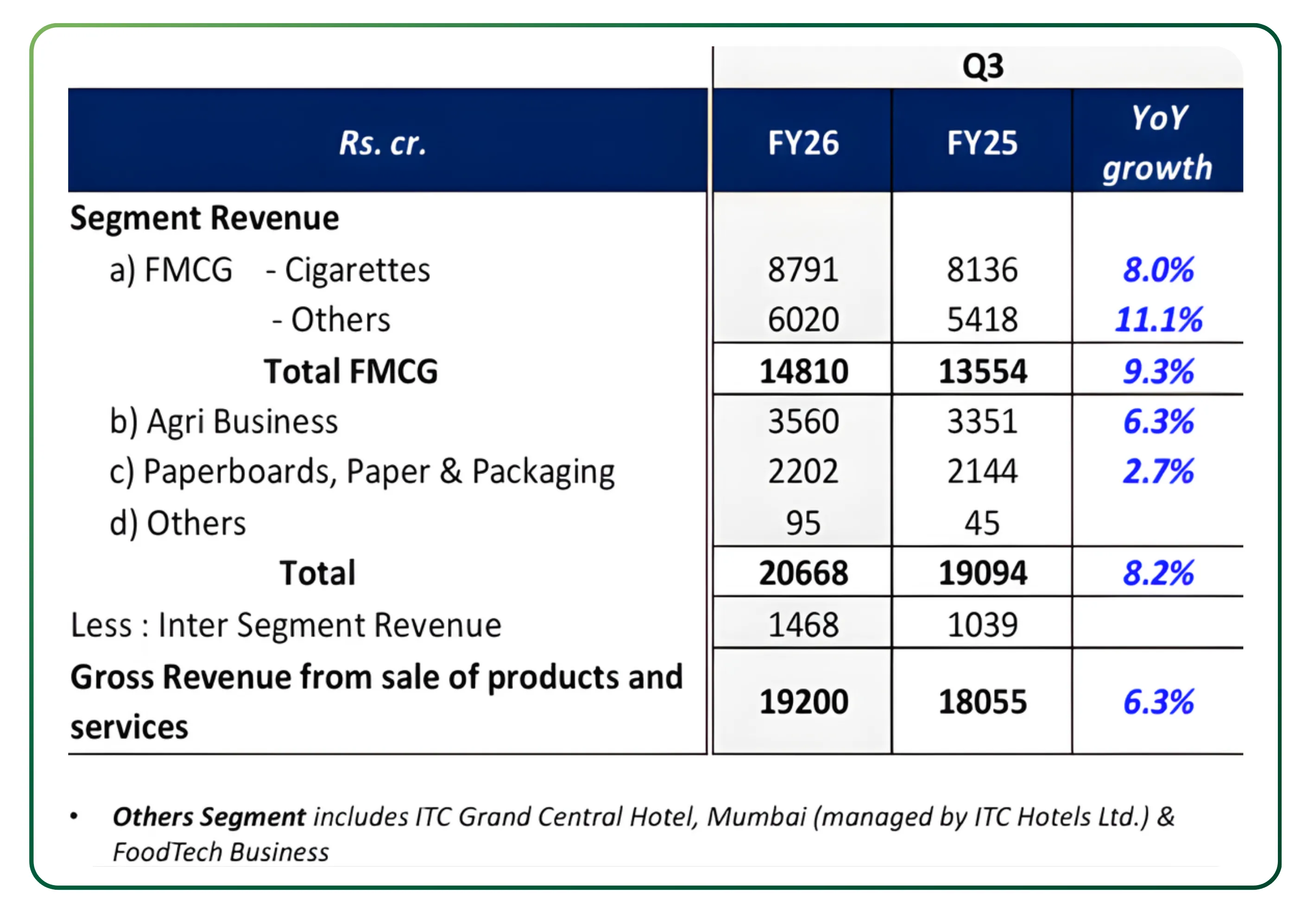

In the most recent quarter, the FMCG Others segment delivered robust performance with an 11% increase in revenue and an EBITDA margin expansion of 145 basis points. The Agri Business also saw a 6.3% revenue growth, driven by value added agricultural products and leaf tobacco exports.

Financial Performance

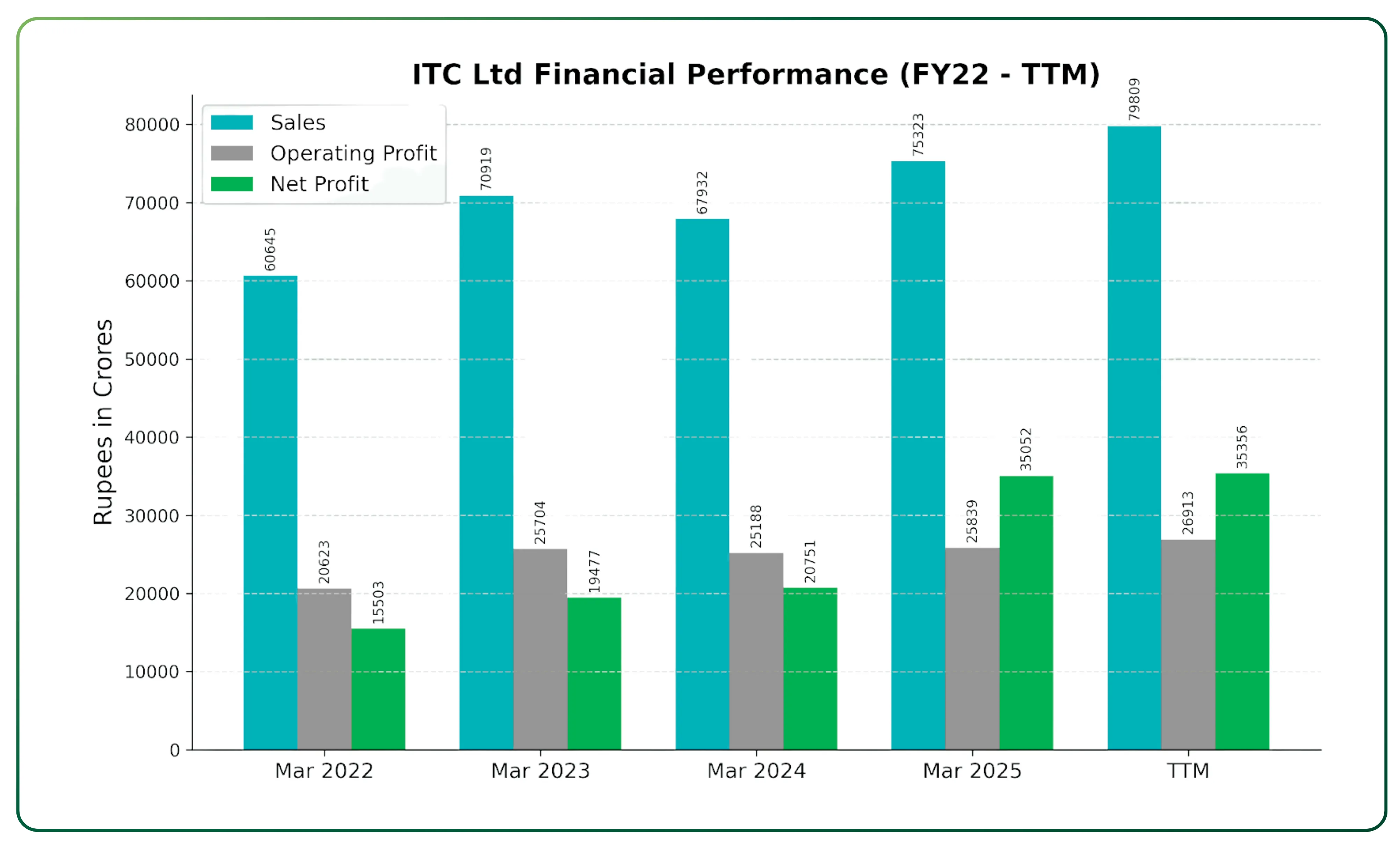

The consolidated financials reflect a resilient business capable of consistent compounding, capable of sustaining high margins and expanding the asset base without leveraging the balance sheet. The net profit figure for March 2025 incorporates the effects of exceptional items related to the hotel business demerger effective January 1, 2025, though this did not materially alter the financial risk profile.

Profit and Loss Consolidated in Rupees Crores

| Metric | Mar 2022 | Mar 2023 | Mar 2024 | Mar 2025 | TTM |

|---|---|---|---|---|---|

| Sales | 60,645 | 70,919 | 67,932 | 75,323 | 79,809 |

| Operating Profit | 20,623 | 25,704 | 25,188 | 25,839 | 26,913 |

| OPM % | 34% | 36% | 37% | 34% | 34% |

| Net Profit | 15,503 | 19,477 | 20,751 | 35,052 | 35,356 |

ITC Limited financial performance from FY22 to TTM showing consistent growth in sales, operating profit, and net profit across its diverse range of businesses.

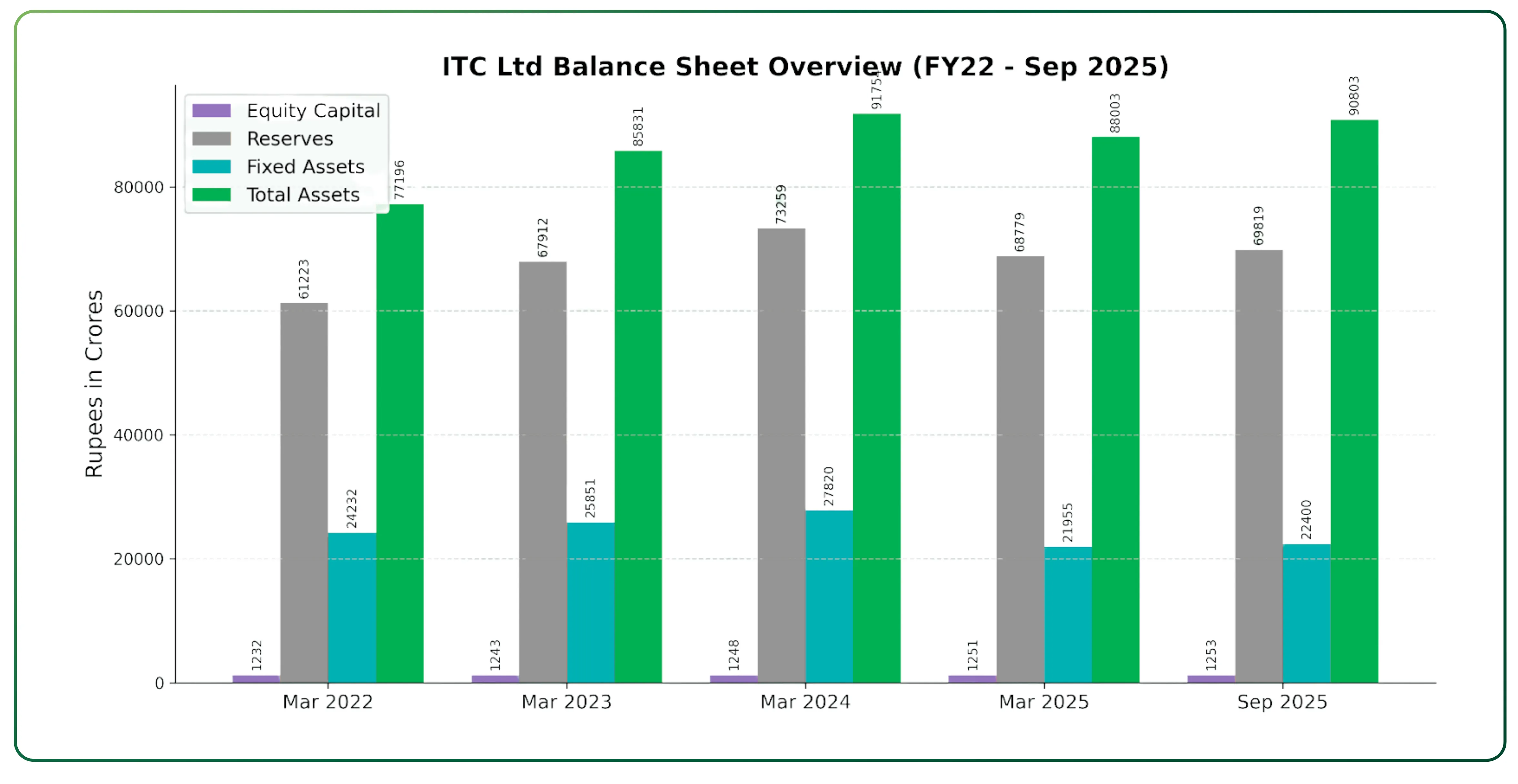

Balance Sheet Consolidated in Rupees Crores

| Metric | Mar 2022 | Mar 2023 | Mar 2024 | Mar 2025 | Sep 2025 |

|---|---|---|---|---|---|

| Equity Capital | 1,232 | 1,243 | 1,248 | 1,251 | 1,253 |

| Reserves | 61,223 | 67,912 | 73,259 | 68,779 | 69,819 |

| Borrowings | 249 | 306 | 303 | 285 | 363 |

| Fixed Assets | 24,232 | 25,851 | 27,820 | 21,955 | 22,400 |

| Total Assets | 77,196 | 85,831 | 91,754 | 88,003 | 90,803 |

ITC Limited balance sheet overview from FY22 to September 2025 reflecting a pristine zero debt capital structure with steadily growing reserves and total assets, supporting a sustainable future for the enterprise.

The financial trajectory captures the steady growth in sales and operating profit over the last decade. The balance sheet demonstrates a negligible reliance on external borrowings, peaking briefly but remaining practically insignificant relative to the total equity and reserves of over Rs 70,000 crores.

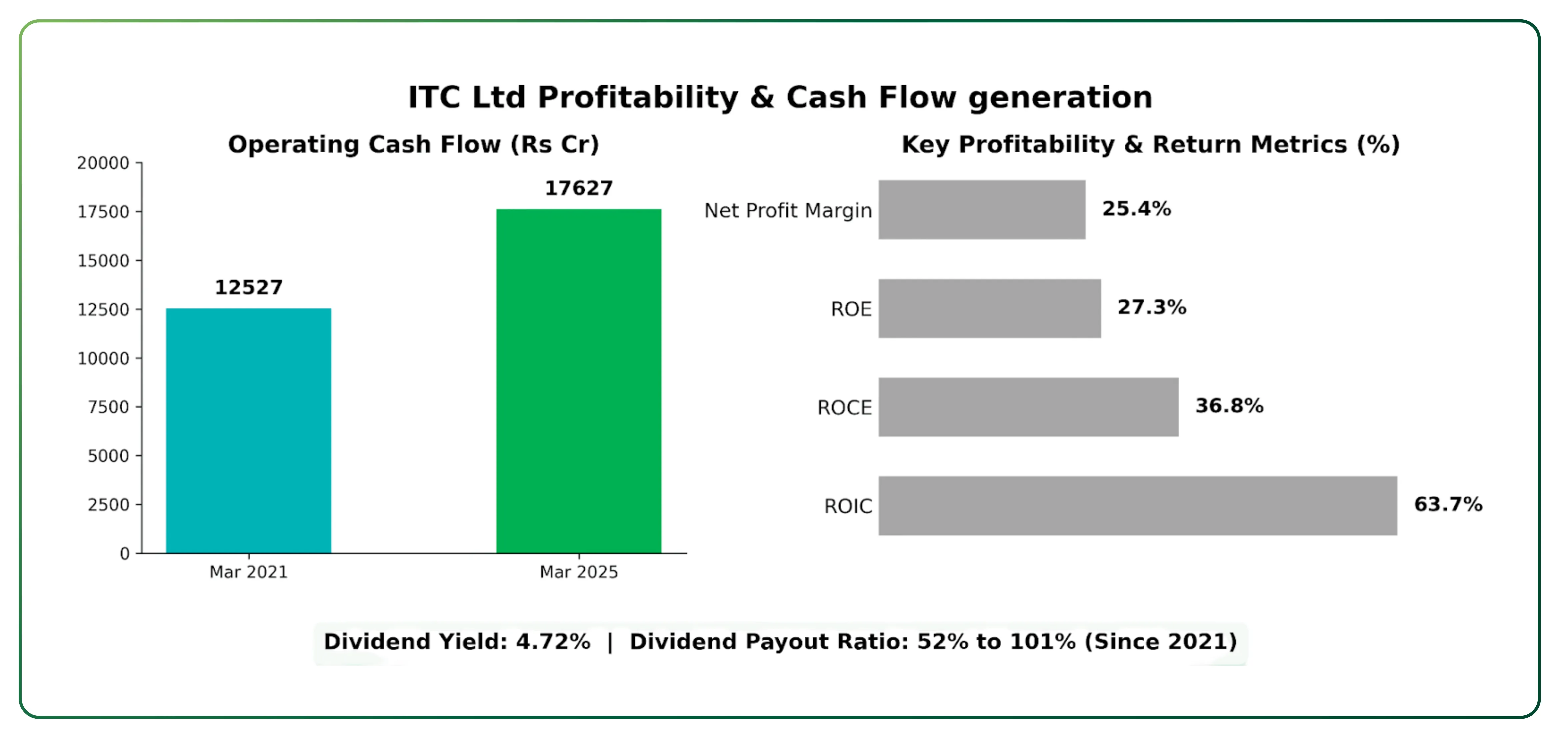

Profitability and Cash Flow Generation

ITC operates as a tremendous cash generating entity. Cash from operating activities reached Rs 17,627 crores in March 2025, up from Rs 12,527 crores in March 2021. This substantial cash flow generation enables the company to maintain a superior liquidity position with over Rs 20,000 crores in free cash and liquid investments. The business maintains a strong dividend payout ratio that has consistently ranged between 52% and 101% since 2021, currently offering a dividend yield of 4.72%. The net profit margin stood at 25.4% in the first half of fiscal 2026. Operating with high capital efficiency, Return on Equity is solid at 27.3% , Return on Capital Employed is 36.8% and Return on Invested Capital stands at an impressive 63.7%

ITC Limited profitability and cash flow generation showing operating cash flow growing to Rs 17,627 crores by March 2025, with a dividend yield of 4.72% and ROIC of 63.7%, reflecting the strength of its diverse range of businesses.

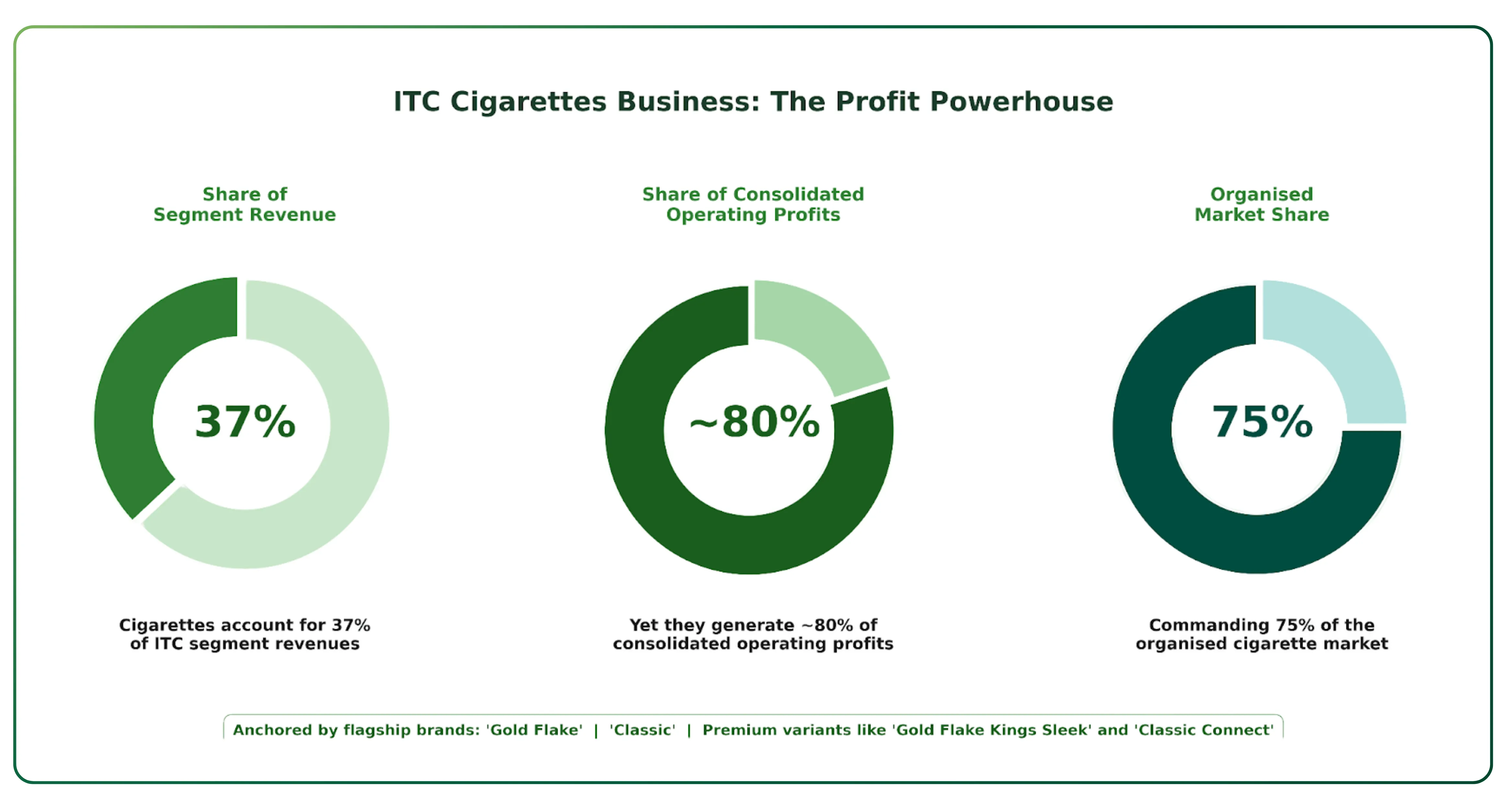

Cigarettes Business

ITC Limited cigarette manufacturing facility, home to the core business segment that commands a 75% organised market share and generates approximately 80% of consolidated operating profits.

As ITC's primary cash cow, the core domestic cigarettes segment accounts for 37% of segment revenues but generates approximately 80% of the company's consolidated operating profits. It commands an unparalleled 75% organised market share. This exceptionally lucrative operating profile is sustained by a robust pricing strategy, product mix enrichment, and deep supply chain efficiencies despite elevated leaf tobacco consumption costs.

ITC Limited cigarettes business contributing 37% of segment revenues while generating approximately 80% of consolidated operating profits, anchored by flagship brands Gold Flake and Classic with a 75% organised market share.

The portfolio is anchored by powerful and highly profitable trademarks, with 'Gold Flake' and 'Classic' serving as the biggest earning mother brands. These are continuously supported by innovative premium variants such as 'Gold Flake Kings Sleek' and 'Classic Connect' to cater to evolving consumer preferences and combat illicit trade.

FMCG Others: Scaling India's Largest Homegrown Brand Portfolio

ITC is widely recognised as the second largest fast moving consumer goods company in India by market capitalisation, reflecting the remarkable scale of its homegrown brand portfolio.

The FMCG Others segment has scaled significantly and now contributes 23% of total revenue, representing one of India's most remarkable organic brand-building stories. ITC's fast moving consumer goods portfolio has evolved well beyond everyday staples, steadily expanding into holistic wellness categories that address health, hygiene, nutrition, and personal wellbeing for millions of Indian households. ITC has built a vibrant portfolio of over 25 homegrown mother brands, including Aashirvaad, Sunfeast, Bingo, Yippee, Classmate, Fiama, Engage, Savlon, and Mangaldeep, that together represent an annual consumer spend exceeding Rs 34,000 crores and reach over 260 million households across the country. In the most recent quarter, this segment delivered an 11% revenue increase with EBITDA margin expansion of 145 basis points, signalling strong operating leverage as the businesses scale.

ITC Limited's fast moving consumer goods portfolio featuring over 25 homegrown mother brands including Aashirvaad, Sunfeast, Bingo, Fiama, and Classmate, spanning food, personal care, and holistic wellness categories across 260 million Indian households.

The Branded Packaged Foods businesses continue to drive growth anchored on vectors of health and nutrition, hygiene, indulgence, and convenience. Products are developed through ITC's state-of-the-art Life Sciences and Technology Centre (LSTC) in Bengaluru, which has filed over 800 patent applications and houses over 400 scientists. The Personal Care portfolio, led by Fiama, Engage, Savlon, and Dermafique, is anchored on premiumisation and science-led formulations across bath and body, fragrances, and skin health, forming a core pillar of ITC's holistic wellness vision for Indian consumers. During the year, over 100 new products were launched across the FMCG businesses, and several value-accretive acquisitions were announced to strengthen presence in high-growth and future-facing categories. The segment has transformed from a loss-making venture a decade ago into a meaningful and rapidly scaling profit contributor.

The Aashirvaad brand, ITC's flagship premium atta offering, crossed the $1 billion revenue mark as of early 2026, cementing its position as one of India's most successful homegrown food brands.

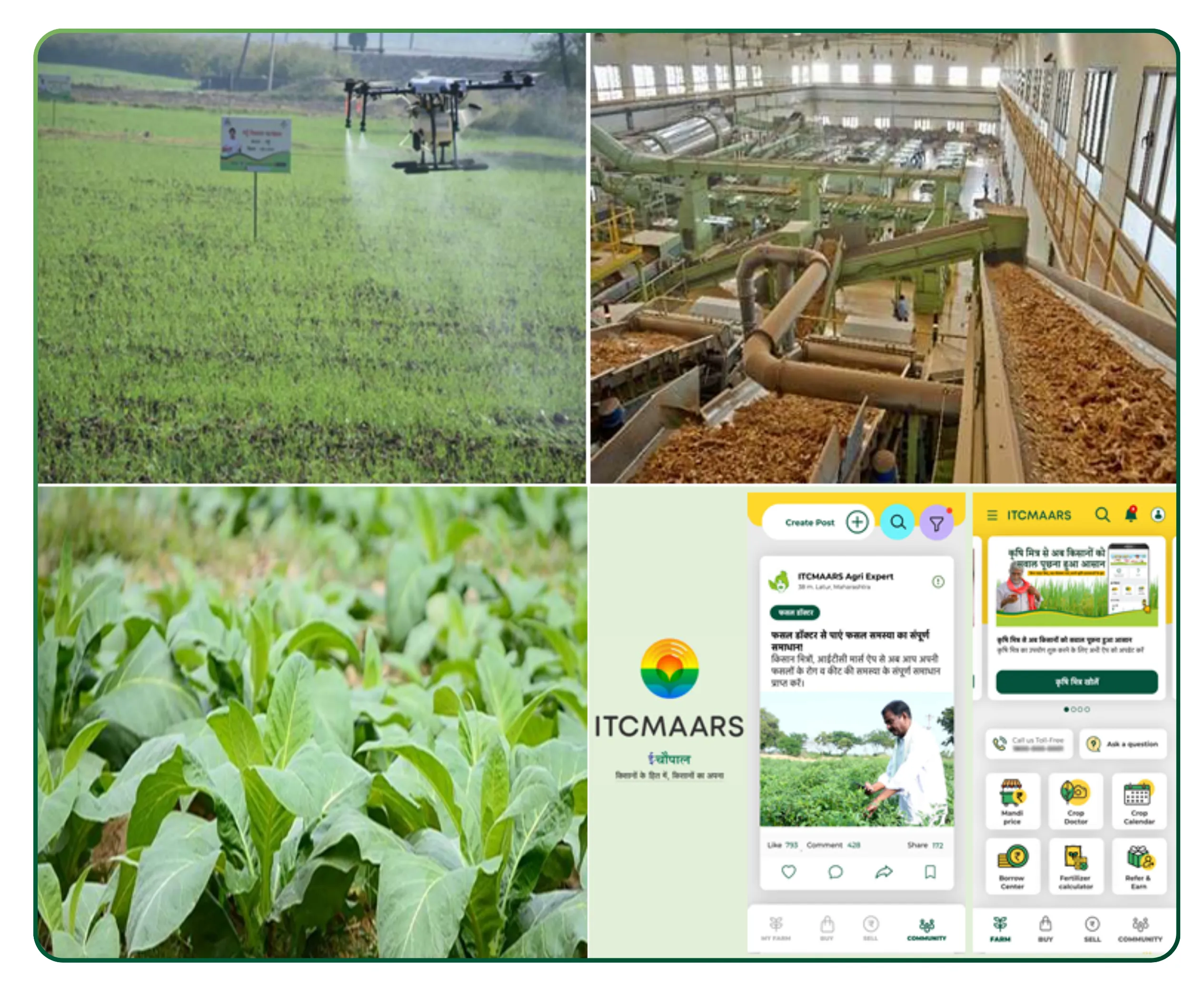

Agri Business

ITC's partnership with the farming community dates back to 1911, giving it over a century of deep rooted expertise in sourcing and developing leaf tobacco and agricultural commodities across India.

The Agri Business segment, contributing 27% of total revenues, leverages ITC's deep backward linkages with the agricultural community. This segment operates a robust farm-to-factory model that handles millions of tonnes of commodities across multiple value chains. Revenue grew 6.3% in the recent quarter, driven by strong performance in Value-Added Agri Products (VAAP) and leaf tobacco exports.

ITC Limited agri business showcasing its farm to factory model, leaf tobacco processing, and the ITCMAARS digital platform delivering personalised agricultural advisory to farmers, building a sustainable future for India's farming community.

The strategic focus of this business has pivoted decisively towards scaling up the VAAP portfolio, which straddles spices, coffee, frozen marine products, and processed fruits. ITC's crop development expertise, superior product quality, and long-standing customer relationships continue to drive robust growth in leaf tobacco exports, making it a world-class leaf tobacco organisation. The ITCMAARS digital platform, a pioneering 'phygital' innovation, delivers hyperlocal and personalised agricultural advisory to farmers at scale through predictive models powered by IoT and data analytics. This platform is laying the foundation for 'Trust Systems at Scale', enabling the farming community to meet evolving traceability and sustainability standards such as the EU Deforestation Regulation (EUDR). The Agri Business also provides crucial strategic sourcing support to ITC's Branded Packaged Foods and Cigarettes businesses, creating deep synergies across the enterprise.

Paperboards, Paper and Packaging

ITC Paperboards and ITC PSPD: Leadership in Value Added Segments

ITC Paperboards, operating under the ITC PSPD (Paperboards and Specialty Papers Division), accounts for 8% of total revenues and holds a leadership position in the Indian paperboards industry, particularly in value-added paperboard and graphic boards used across premium packaging applications. The business operates through a vertically integrated model with backward integration into pulpwood plantations and in-house pulp production at its Bhadrachalam facility.

ITC Paperboards and Specialty Papers Division facility at Bhadrachalam, a vertically integrated plant producing value added paperboards and graphic boards while progressively reducing coal consumption for a sustainable future.

Currently, this segment faces near-term headwinds from soft domestic realizations, low-priced imports, and elevated wood prices caused by severe cyclones during the harvesting season. However, the medium-term outlook is anchored by two significant growth drivers. First, the ongoing acquisition of Century Pulp and Paper at an estimated outlay of Rs 3,500 crores will materially expand capacity at a new location, given that existing facilities are already saturated.

Specialty Papers Division

The Specialty Papers Division within ITC PSPD produces a wide range of specialty papers catering to industrial, educational, and packaging end uses, supported by the backward integrated pulpwood plantations and captive pulp production at the Bhadrachalam facility.

ITC is rapidly scaling up sustainable packaging solutions to replace single-use plastics through its wholly-owned subsidiary, ITC Fibre Innovations Limited (IFIL), which has commissioned a state-of-the-art moulded fibre products facility in Madhya Pradesh. Additionally, the recently commissioned future-ready High Pressure Recovery Boiler at the Bhadrachalam mill is progressively enhancing energy efficiency and significantly lowering coal consumption, reinforcing the business's sustainability credentials.

ITC Limited Q3 FY26 segment revenue breakdown showing total FMCG growing 9.3%, agri business up 6.3%, and ITC paperboards and packaging growing 2.7%, with ITC Hotels Limited managed properties included under the others segment

ITC Hotels Business

ITC Hotels offers authentic indigenous luxury experiences designed to be in harmony with the environment and society. Its portfolio spans multiple brands including the EPIQ Collection, which blends culinary innovation, service excellence, and design sophistication, as well as Welcomhotel, a premium collection designed for curated travel experiences. Fortune Hotels, also part of the ITC Hotels portfolio, is India's leading chain of full service business and leisure hotels.

Regulatory and Industry Risks

The cigarettes division faces significant regulatory headwinds, navigating a highly punitive and discriminatory tax regime. Taxes on cigarettes in India are among the highest globally, standing at 71% as a percentage of Per Capita GDP according to WHO data. The recent Union Budget introduced an unprecedented and steep increase in GST and Excise Duty rates effective February 1, 2026. This aggressive taxation creates a significant near term headwind by expanding the tax arbitrage for smuggled and illicit cigarettes, posing a severe threat to legal industry volumes. Additionally, the paperboards segment is contending with low priced imports and elevated wood prices caused by severe cyclones during the harvesting season.

Beyond taxation and import pressures, the broader operating environment is increasingly shaped by the risks of climate change, which affect raw material availability, supply chain resilience, and evolving regulatory frameworks across the agri and paperboards businesses.

Capital Allocation and Strategic Investments

The balance sheet remains highly conservative. The debt to equity ratio is 0.01, with total borrowings at just Rs 363 crores against total assets of Rs 90,803 crores in September 2025. ITC is deploying its internal accruals toward expanding its manufacturing capacities and value chains. The company plans to invest Rs 20,000 crores over the medium term across its businesses. A notable step in this expansion is the ongoing acquisition of Century Pulp and Paper at an estimated capital outlay of Rs 3,500 crores. These investments are fully funded by internal cash flows without stressing the capital structure.

Future Strategy: The 'ITC Next' Horizon

To scale the next horizon of competitiveness, the company is executing its comprehensive 'ITC Next' strategy. This future-facing roadmap is anchored on driving purpose-led innovation, accelerating digital adoption, and embedding sustainability across its operations:

Digital and Tech-Led Growth ('Mission DigiArc')

ITC is aggressively transforming into a 'Future-Tech' enterprise. This involves leveraging advanced digital technologies, artificial intelligence, and a 'digital-first' architecture to drive superior consumer insights, agile innovation, and deep supply chain efficiencies.

ITC Infotech: Powering the Digital Transformation

ITC Infotech, a wholly owned subsidiary specialising in IT services and digital solutions, plays a pivotal role in enabling this transformation by providing technology platforms, data analytics capabilities, and enterprise solutions that power ITC's operations across its diverse range of businesses globally.

Sustainability 2.0

Reimagining enterprise growth under the pressing challenges of climate change, the strategy focuses on extensive decarbonisation, circular economy practices, and developing eco-friendly product alternatives.

Solid Waste Recycling Positive: A Core Sustainability Commitment

A defining pillar of Sustainability 2.0 is ITC's commitment to becoming solid waste recycling positive, ensuring the company recycles more solid waste than it generates across its manufacturing operations. This commitment is supported by the rapid scale-up of solid waste recycling infrastructure and the replacement of single-use plastics through ITC Fibre Innovations Limited, directly addressing the growing challenges of climate change. Beyond environmental sustainability, ITC has facilitated the formation of more than 10,000 self help groups bringing together over 120,000 women members across more than 10 states, while also ensuring women's representation on the boards of more than 2,100 farmer producer organisations. These initiatives collectively cover 6 million women across India, reflecting ITC's commitment to inclusive and sustainable growth.

Value-Added Adjacencies and FoodTech

While fortifying its core 25+ mother brands, the FMCG division is expanding into premium value-added adjacencies in health, hygiene, and naturals. Additionally, ITC is actively nurturing a new, dynamic FoodTech business vector that synergises its institutional strengths in food science, FMCG brands, hospitality, and digital capabilities, having rapidly scaled up a network of cloud kitchens.

ITC's Master Chef Creations, the food technology business, offers a range of quality food products available for home delivery through platforms like Swiggy and Zomato, rapidly scaling its reach across urban India.

Agri Business Evolution

The strategic focus of the Agri division has resolutely pivoted towards rapidly scaling up its Value-Added Agri Products (VAAP) portfolio (encompassing spices, coffee, and frozen marine products) to accelerate both revenue growth and margin expansion, moving beyond traditional commodity trading.

ITC is the only company in the world, of comparable size and diversity, to be carbon positive for over 20 years, water positive for over 23 years, and solid waste recycling positive for over 18 years, a distinction that underscores its unmatched commitment to building a sustainable future while combating climate change.

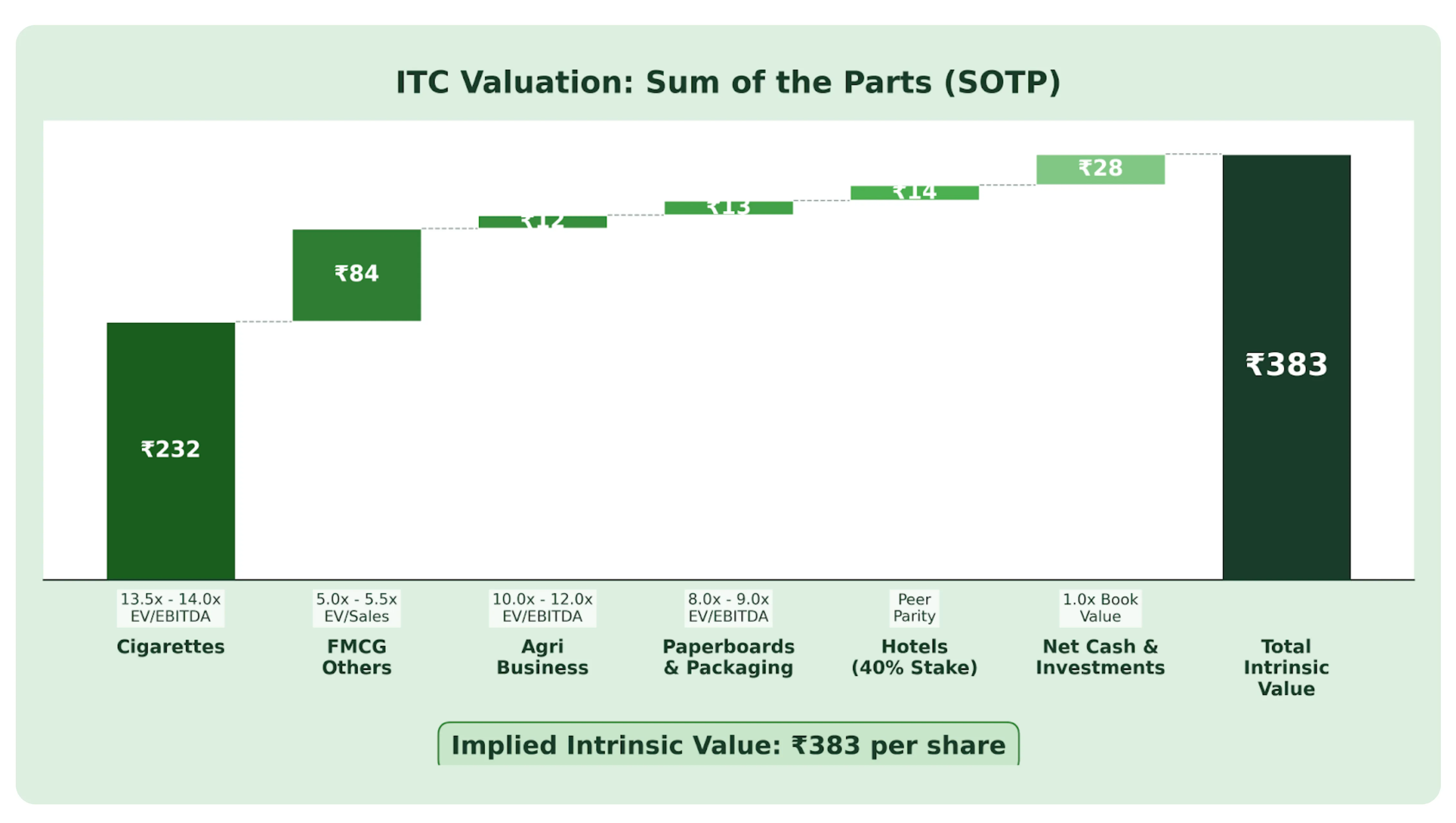

Valuation Approach: Sum of the Parts (SOTP)

Valuing a diversified conglomerate like ITC requires a Sum of the Parts (SOTP) methodology to individually price the distinct growth and risk profiles of its operating businesses.

SOTP Valuation Breakdown

| Business Segment | Valuation Metric | Target Multiple | Implied Segment Value (₹ Cr) | Value per Share (₹) | % of Total Value |

|---|---|---|---|---|---|

| Cigarettes | EV / EBITDA | 13.5x – 14.0x | 290,000 | 232 | 59% |

| FMCG Others | EV / Sales | 5.0x – 5.5x | 105,000 | 84 | 21% |

| Agri Business | EV / EBITDA | 10.0x – 12.0x | 15,000 | 12 | 3% |

| Paperboards & Packaging | EV / EBITDA | 8.0x – 9.0x | 16,000 | 13 | 3% |

| Hotels (40% Stake) | Peer Parity | – | 18,000 | 14 | 4% |

| Net Cash & Investments | Book Value | 1.0x | 35,000 | 28 | 10% |

| Total Intrinsic Value | ~479,000 | ~383 | 100% |

ITC Limited sum of the parts valuation assigning segment values to cigarettes, fast moving consumer goods, agri business, ITC paperboards and packaging, and ITC Hotels Limited stake, implying a total intrinsic value of Rs 383 per share.

Valuation Rationale:

Cigarettes: Assigned a 13.5x-14.0x EV/EBITDA multiple, reflecting its status as a mature cash cow. The multiple embeds a discount to global consumer peers due to the severe taxation environment in India, yet accounts for ITC's immense pricing power and 75% market share.

FMCG Others: Valued at 5.0x-5.5x EV/Sales. While EBITDA multiples are typically used, valuing this rapidly scaling segment on a sales basis better captures its growth trajectory and peer parity (where pure-play Indian FMCG companies trade at 6x-10x EV/Sales).

Other Segments: Agri and Paperboards are assigned conservative multiples (10x-12x and 8x-9x respectively) reflecting cyclicality and near-term headwinds. The 40% retained stake in ITC Hote

The consolidated EV/EBITDA currently stands at 12.7 times, which remains at a noticeable discount to its five-year historical median of 17.2 times. The SOTP implies an intrinsic value.

The Structural Growth Paradigm

ITC Limited presents a compelling combination of deep value and structural growth. While near-term taxation realities in the Cigarettes division and cyclical headwinds in Paperboards have temporarily compressed valuation multiples, the underlying business fundamentals remain extraordinarily resilient. The company's strategic pivot under the 'ITC Next' roadmap particularly the aggressive scaling and margin expansion of its massive FMCG portfolio and the shift towards value-added agriculture is creating a more balanced and higher-quality earnings stream. Supported by a pristine, zero-debt balance sheet, robust free cash flow generation exceeding Rs 17,000 crores, and a highly attractive dividend yield, ITC offers a formidable margin of safety. As the non-cigarette businesses continue to scale and of Rs 383. The valuation remains deeply anchored by the fortress balance sheet, a >4.5% dividend yield, and aggressive margin scaling within the FMCG portfolio.ls Limited is valued based on comparable hospitality peers.

Command higher market multiples, long-term investors are well-positioned to benefit from both capital appreciation and consistent dividend returns.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.