Wakefit Innovations Limited, incorporated in 2016, has established itself as a prominent player in India’s organized home and sleep solutions market. Initially launching as a digital-first mattress brand, the company has since diversified its portfolio to include furniture and home décor, effectively transitioning from a single-category specialist to a comprehensive home solutions provider.

Operating primarily through a Direct-to-Consumer (D2C) model backed by backward-integrated manufacturing, Wakefit controls its value chain from production to last-mile delivery. This structure allows it to compete directly with legacy incumbents in the consumer durables space by optimizing costs and inventory turnover. With a current market capitalization of approximately ₹5,997 Crores and trailing twelve-month revenues surpassing ₹1,274 crore, the company has moved beyond its startup phase to become a scalable entity focused on balancing volume growth with improving return ratios.

Business Model

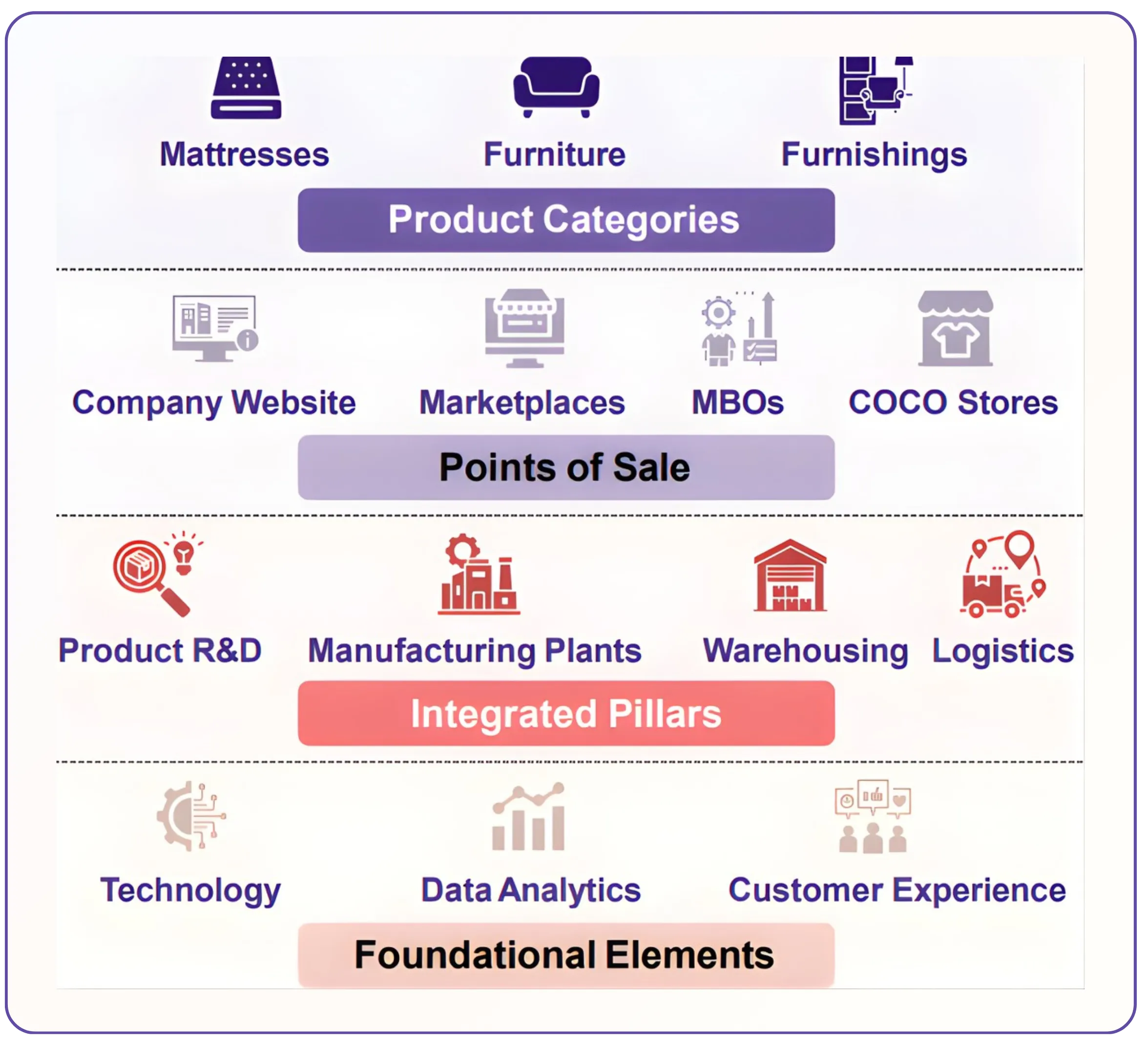

Wakefit’s core business is anchored in the "Home and Sleep Solutions" vertical. Unlike traditional players that rely heavily on third-party distribution, Wakefit operates primarily through a D2C model. This allows the company to control the entire value chain, ensuring quality control and better margins.

The company’s revenue streams are broadly categorized into:

- Sleep Solutions: This remains the key revenue driver, comprising orthopedic memory foam mattresses, pillows, and sleep accessories.

- Furniture & Home Décor: A rapidly growing vertical that includes beds, sofas, wardrobes, and other furnishing items, allowing the company to capture a larger share of the customer's wallet.

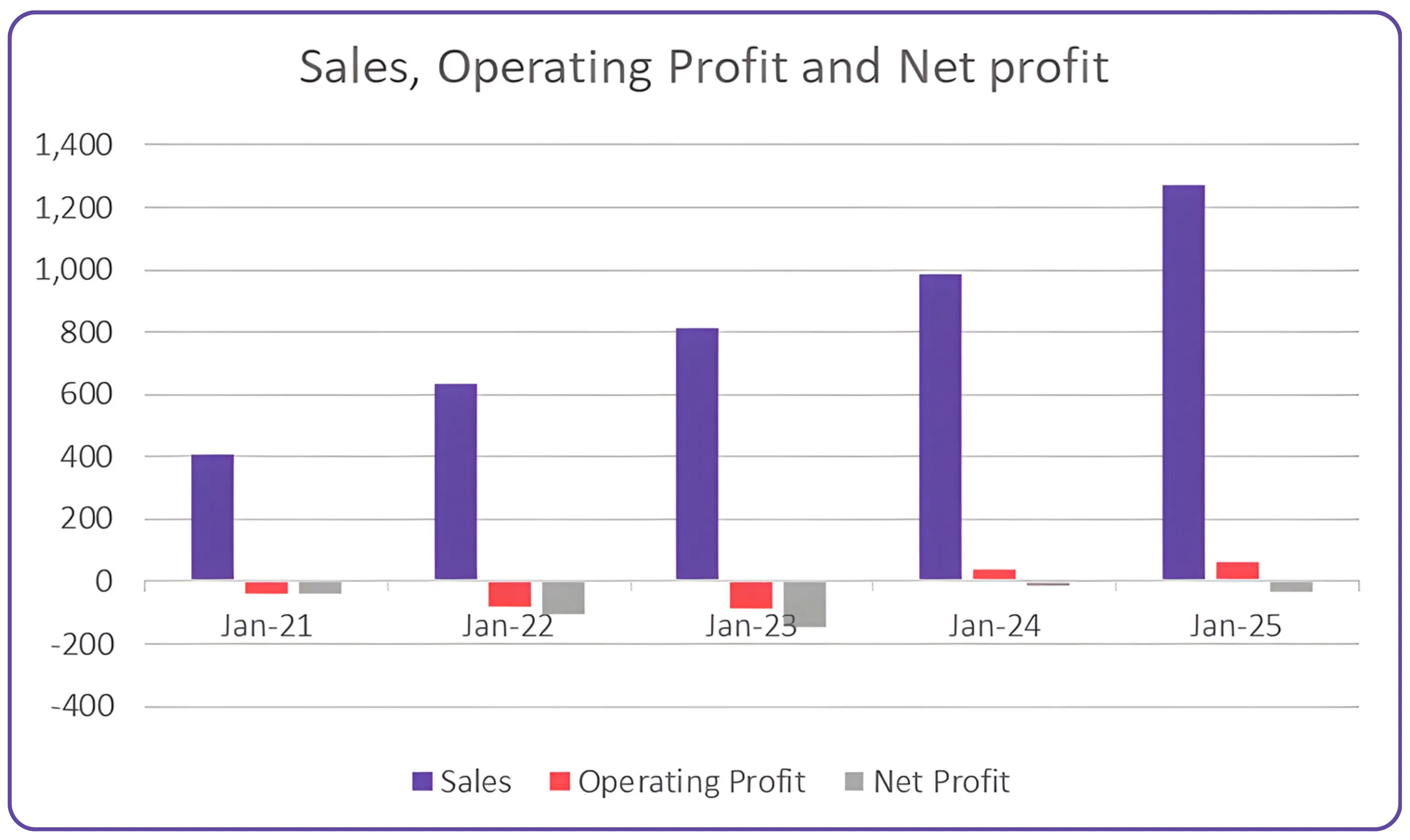

This integrated model has enabled Wakefit to scale its revenue aggressively, growing from just ₹409 Crores in FY21 to over ₹1,274 Crores in FY25.

Financial Performance Snapshot

The following data highlights the company's financial journey over the last five fiscal years.

| Year | Sales | Operating Profit | Net Profit |

|---|---|---|---|

| Mar-25 | 1,274 | 60 | -35 |

| Mar-24 | 986 | 36 | -15 |

| Mar-23 | 813 | -85 | -146 |

| Mar-22 | 633 | -79 | -107 |

| Mar-21 | 409 | -40 | -37 |

(Values in ₹ crores)

FY26 Interim Highlights: A Turnaround Story

The quarterly results for December 2025 mark a definitive inflection point for Wakefit Innovations. After years of prioritizing growth over immediate profits, the company has demonstrated a sharp turnaround in its bottom line.

- Revenue: The company clocked ₹421 Crores in sales for the quarter ending December 2025. This single-quarter run rate suggests a strong and accelerating trajectory compared to its full-year sales of ₹1,274 Crores in FY25.

- Profitability: In a significant shift from historical losses, Wakefit reported a Net Profit of ₹32 Crores for the December 2025 quarter. This is a stark contrast to both the net loss of ₹2 Crores from the same quarter last year (Dec 2024) and the net loss of ₹35 Crores reported for the full year of FY25.

- Operating Efficiency: Operating margin expanded sharply to 14% in the December 2025 quarter, compared to approximately 5% in FY25.

- Asset Utilization: The company has been sweating its assets effectively, with cash flow from operations turned positive at ₹3 crore in FY25, successfully recovering from a negative cash flow position of -₹58 Crores in the previous year (FY24).

Growth Drivers

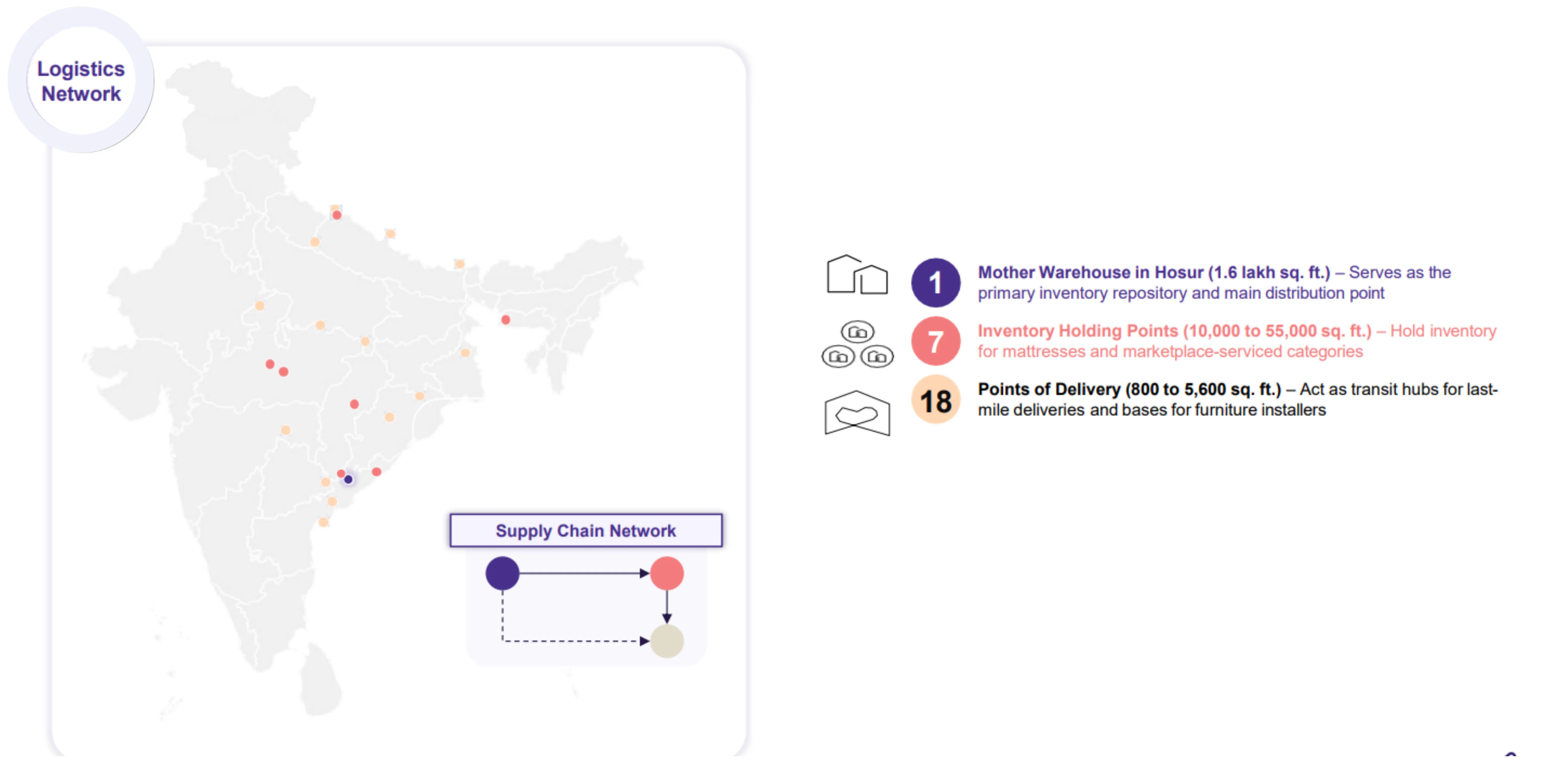

Aggressive Capacity Expansion

Wakefit has consistently invested in building its own manufacturing capabilities rather than relying solely on outsourcing. Net Fixed Assets have grown exponentially from ₹49 Crores in March 2021 to ₹415 Crores in March 2025. As of September 2025, the fixed asset base stands at ₹407 Crores, indicating that the heavy capex cycle is maturing and ready to generate returns.

Revenue Momentum

The company has delivered a robust 3-year Sales CAGR of 26% and a Trailing Twelve Months (TTM) growth of 29%. This outpaces many traditional peers in the consumer durables sector, validating the scalability of its D2C approach.

Institutional Confidence

The shareholding pattern reflects strong institutional backing. As of December 2025, Foreign Institutional Investors (FIIs) hold 19.54% of the company, while Domestic Institutional Investors (DIIs) hold 22.44%. This combined institutional holding of over 40% suggests high confidence in the company's long-term governance and growth prospects.

Risks and Challenges

Return Ratios

Despite the recent turnaround, the company’s historical return ratios remain weak due to past accumulated losses. The Return on Equity (ROE) over the last year was -8.20%, and the Return on Capital Employed (ROCE) was -1.53%. Investors will be watching closely to see if the September 2025 profitability can sustainably boost these metrics into positive territory.

Promoter Holding

Data indicates that promoter holding has decreased over the last quarter and currently stands at 37.39%. While this often happens as companies dilute equity to raise growth capital, a significant reduction can sometimes be a point of caution for minority shareholders.

Interest Coverage

The company has a modest coverage ratio. Interest costs have risen to ₹30 Crores in FY25, and borrowings have increased to ₹277 Crores in September 2025 from negligible levels in FY21. Managing debt serviceability while funding expansion will be critical.

When viewed alongside its peers:

| Company Name | Market Cap | Sales Growth (YoY) | OPM Growth (YoY) |

|---|---|---|---|

| Wakefit Innovations | ₹5,997 Cr | 29.00% | 25.00% |

| Sheela Foam | ₹6,522 Cr | 15.00% | -30.00% |

| Responsive Industries | ₹5,172 Cr | 30.00% | -4.55% |

Wakefit trades at a similar market capitalization to Sheela Foam, despite having a different profitability history. The market seems to be pricing in the high growth rate and the successful pivot to profitability demonstrated in the recent half-yearly results.

Crossing the Inflection Point

Wakefit Innovations is currently in a "sweet spot" of its corporate lifecycle. The company has successfully navigated the cash-burn phase typical of D2C startups (FY21-FY23) and achieved operating breakeven in FY24. The clear Net Profit in the first half of FY26 signals that the business model has matured.

If Wakefit can sustain the 12% operating margins and revenue run rate shown in the September quarter, it is well on its way to becoming a cornerstone player in the organized home solutions market. For investors, the key monitorable will be whether this profitability is structural and if the company can improve its return ratios in the coming quarters.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.