Anlon Healthcare Limited (Anlon Healthcare Ltd) is a Rajkot-based chemical manufacturing company incorporated in 2013. It specializes in producing high-purity pharmaceutical intermediates and active pharmaceutical ingredients (APIs) that are used in making formulations such as tablets, capsules, syrups, nutraceutical APIs, personal care and veterinary products, and animal health products.

The company’s products meet international pharmacopoeia standards like IP, BP, EP, JP, and USP, ensuring consistent quality and compliance with industry standards. Anlon operates a single manufacturing facility in Gujarat, which is WHO-GMP certified and ISO 9001:2015 accredited. The company’s focus is on maintaining quality, safety, and strong product portfolio across more than 65 chemical compounds including pharmaceutical intermediates and active APIs.

Its client base includes both domestic and international markets (including South Korea), though 96% of revenue comes from India. The company plans to expand through custom manufacturing services (CMS) and custom manufacturing of intermediates, offering flexible minimum order quantity options for pharma clients.

Promoters include Punitkumar R. Rasadia, Meet Atulkumar Vachhani, and Mamata Rasadia. With IPO proceeds, Anlon Healthcare Ltd aims to fund capital expenditure requirements, repay its term loan, and meet working capital needs.

Core Business

Anlon Healthcare is engaged in the manufacturing of high-purity pharmaceutical intermediates and Active Pharmaceutical Ingredients (APIs). These are essential raw materials used by pharmaceutical companies to produce finished dosage forms such as tablets, capsules, syrups, ointments, personal care products, nutraceuticals, and veterinary medicines.

Business Verticals

Pharmaceutical Intermediates – High-purity intermediates that act as key starting materials.

Active Pharmaceutical Ingredients (APIs) – Bulk drug substances for various formulations.

Nutraceutical – Dietary supplement ingredients.

Personal Care Ingredients – Specialty APIs such as loxoprofen sodium dihydrate and piroctone olamine.

Veterinary – Ingredients for animal healthcare products.

Anlon Healthcare IPO Details

| Particulars | Details |

|---|---|

| Issue Type | 100% Book Built Healthcare IPO |

| Issue Size | 1,33,00,000 Equity Shares (Fresh Issue only) |

| Face Value | ₹10 per share |

| Offer for Sale (OFS) | Nil |

| Price Band | To be announced (2 days before opening) |

| Minimum Bid Lot | To be announced |

| IPO Opens | August 26, 2025 |

| IPO Closes | August 29, 2025 |

| Anchor Investor Bidding | August 25, 2025 |

| Listing Date | On NSE (Designated SE) and BSE |

| Lead Manager (BRLM) | Interactive Financial Services Ltd. |

| Registrar | KFin Technologies Ltd |

| Pre-Issue Promoter Holding | 70.26% |

| Post-Issue Holding | Will reduce due to dilution |

| Use of Net Proceeds | Expansion (capital expenditure), term loan repayment, working capital, general corporate purposes |

Allocation Structure:

Qualified Institutional Buyers (QIBs): Not less than 75% of net issue

Non-Institutional Investors (NII): Not more than 15%

Retail Investors (RII): Not more than 10%

Financial Overview

| Particulars | FY2023 | FY2024 | FY2025 |

|---|---|---|---|

| Total Income | ₹113.12 Cr | ₹66.69 Cr | ₹120.46 Cr |

| Profit After Tax (PAT) | ₹5.82 Cr | ₹9.66 Cr | ₹20.52 Cr |

| Net Worth | ₹7.37 Cr | ₹21.03 Cr | ₹80.42 Cr |

| Equity Share Capital | ₹12.00 Cr | ₹16.00 Cr | ₹39.85 Cr |

| Borrowings (Total Debt) | ₹66.39 Cr | ₹74.56 Cr | ₹58.35 Cr |

| Earnings Per Share (EPS) | ₹4.85 | ₹6.68 | ₹6.38 |

| Net Asset Value (NAV) | ₹6.15 | ₹13.14 | ₹20.18 |

| Debt-Equity Ratio | 9.00x | 3.55x | 0.73x |

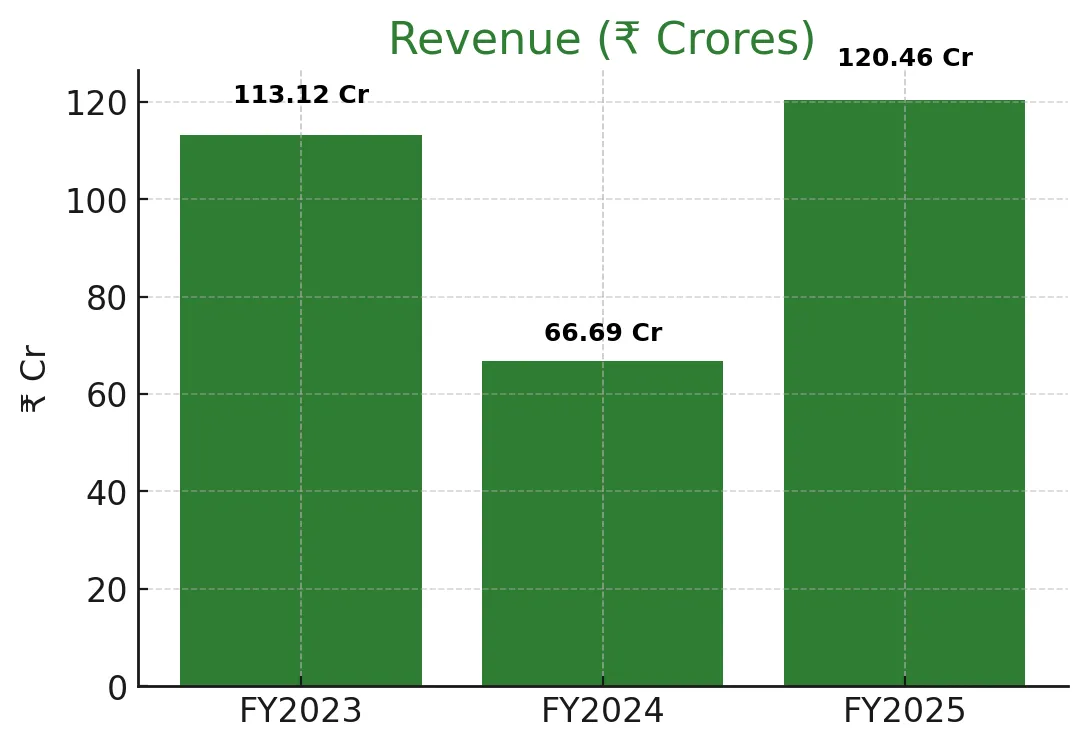

Revenue:

Anlon Healthcare reported revenues of ₹113.12 Cr in FY23, which dropped to ₹66.69 Cr in FY24 due to a regulatory shutdown. The company rebounded strongly in FY25, crossing ₹120 Cr in revenue.

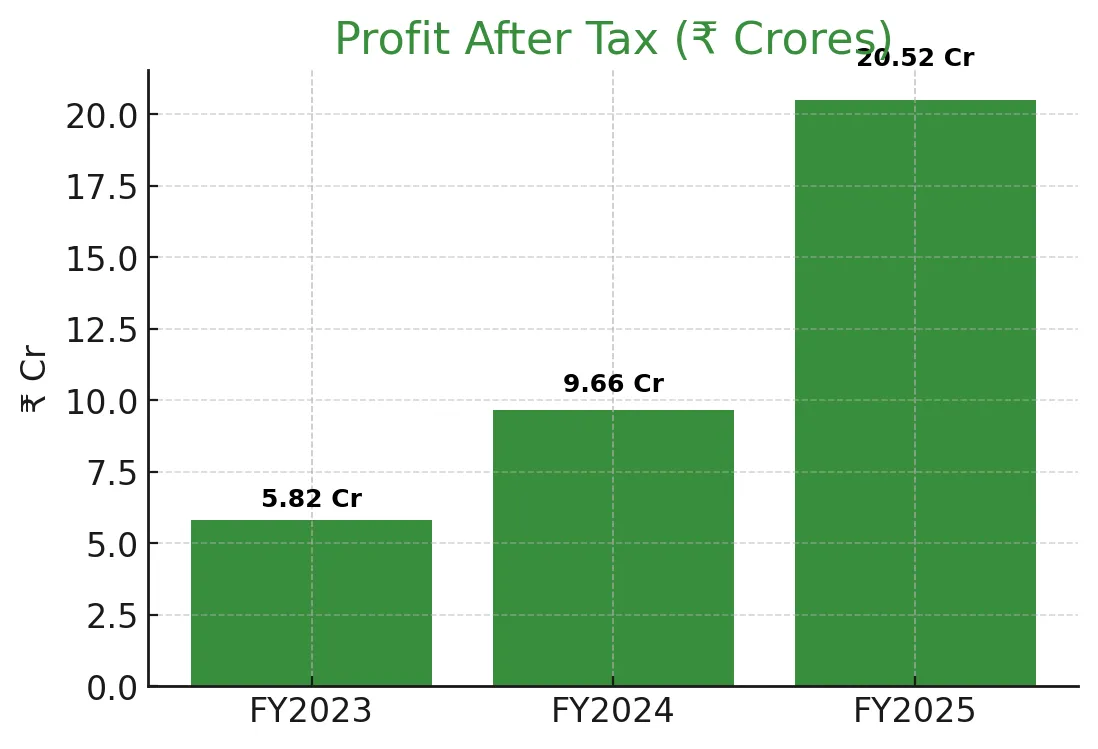

Profit After Tax (PAT):

PAT grew from ₹5.82 Cr in FY23 to ₹9.66 Cr in FY24, showing resilience despite lower revenues. By FY25, PAT more than doubled to ₹20.52 Cr, reflecting improved margins and recovery.

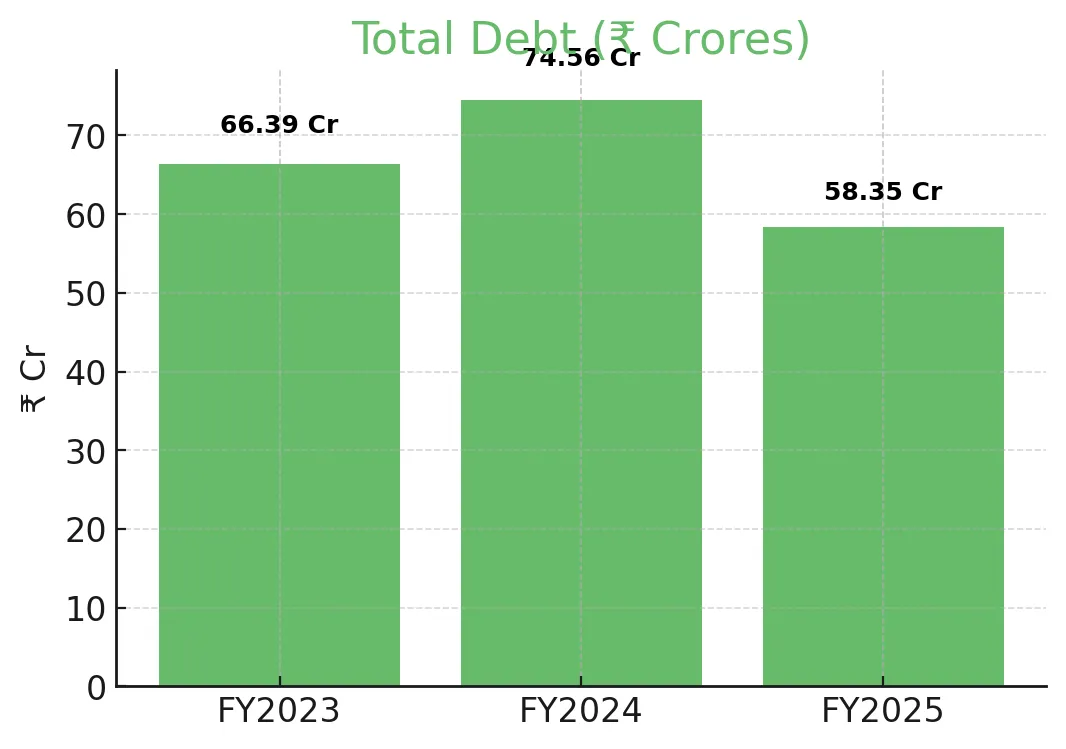

Borrowings (Total Debt):

Debt levels increased from ₹66.39 Cr in FY23 to ₹74.56 Cr in FY24, as the company faced working capital requirements. In FY25, borrowings reduced to ₹58.35 Cr, improving leverage.

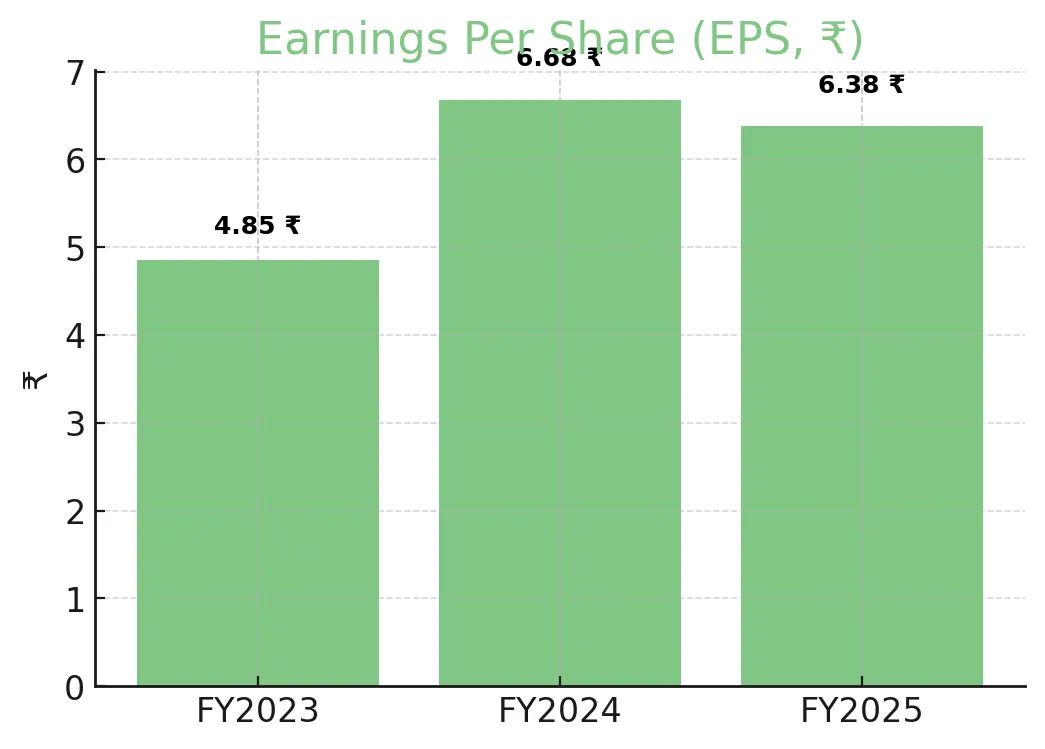

Earnings Per Share (EPS):

EPS improved from ₹4.85 in FY23 to ₹6.68 in FY24, aided by higher profitability. It slightly declined to ₹6.38 in FY25 due to equity dilution, despite higher absolute profits.

Risks

Regulatory Risks: Facility shutdown risks due to DMF approvals and audits.

Customer Concentration: Around ~75% of revenue comes from the top 10 clients.

Supplier Concentration: High dependence on a few suppliers for raw materials.

Geographic Dependence: 96% of sales are generated from India, indicating low export diversification.

Working Capital Stress: Negative operating cash flow (OCF) of ₹-22.55 Cr in FY25.

Competition & Imports: India imports 70–75% of APIs from China, increasing competitive and supply chain risks.

No Long-Term Contracts: Business operations are largely based on purchase orders (PO) without long-term agreements.

Legal Liabilities: Pending GST disputes amounting to approximately ₹1.15 Cr.

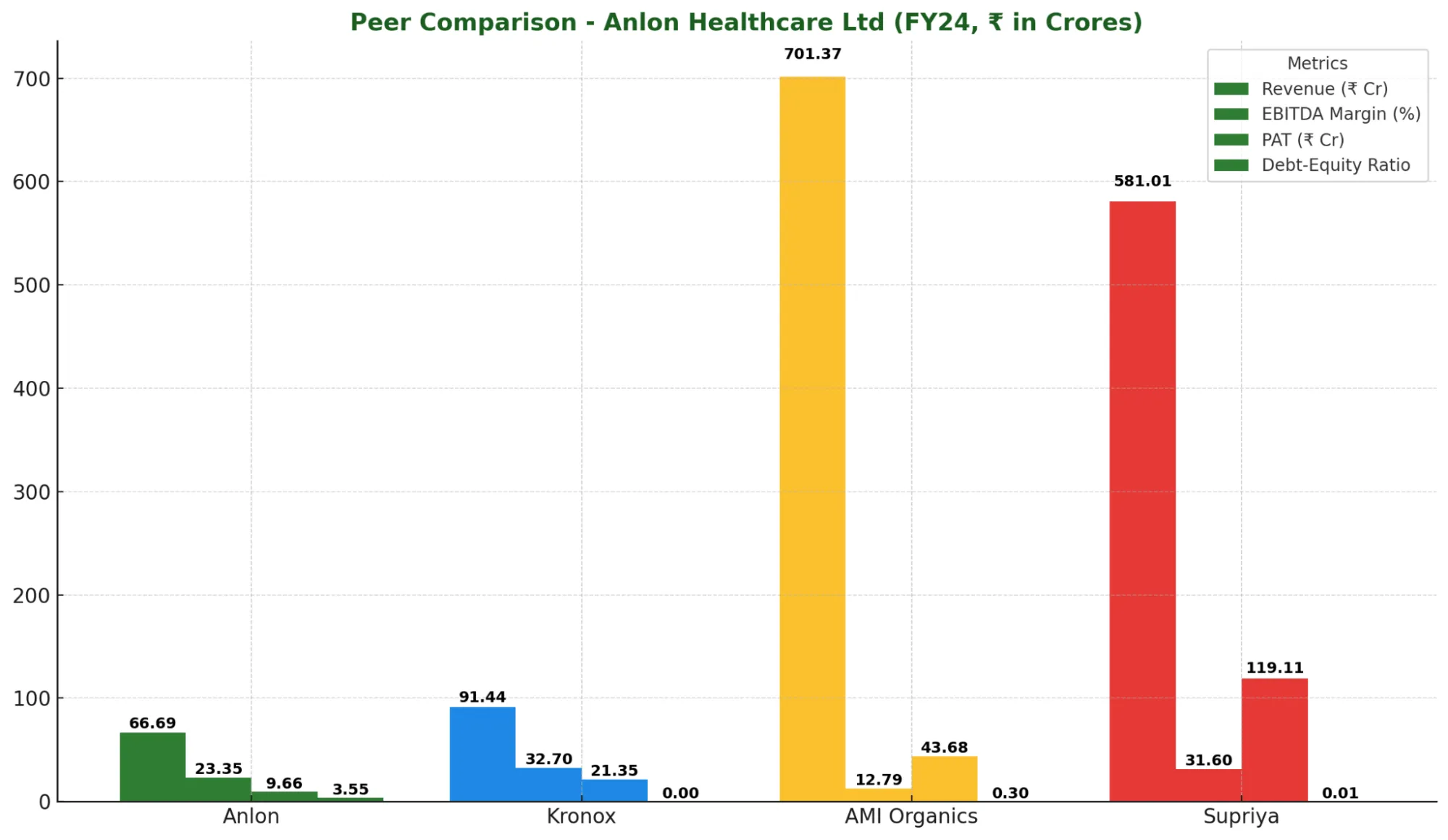

Peer comparison :

| Particulars | Anlon Healthcare Ltd | Kronox Lab Sciences Ltd | AMI Organics Ltd | Supriya Lifesciences Ltd |

|---|---|---|---|---|

| Revenue (Total Income) | ₹66.69 Cr | ₹91.44 Cr | ₹701.37 Cr | ₹581.01 Cr |

| EBITDA Margin (%) | 23.35% | 32.70% | 12.79% | 31.60% |

| PAT (Profit After Tax) | ₹9.66 Cr | ₹21.35 Cr | ₹43.68 Cr | ₹119.11 Cr |

| Net Profit Margin (%) | 14.50% | 0.24% | 6.34% | 20.50% |

| Return on Equity (RoE) | 67.99% | 0.65% | 0.07% | 15.00% |

| Debt-Equity Ratio | 3.55x | 0.00x | 0.30x | 0.01x |

| Current Ratio | 2.01 | 6.07 | 1.76 | 5.17 |

Strengths

- Strong product portfolio of 65+ items across pharma intermediates, APIs, nutraceuticals, veterinary, and personal care.

- Certified manufacturing facility ensuring consistent quality and quality control.

- Growing financial performance despite challenges.

- Experienced promoters with domain knowledge.

- Proposed expansion to enhance market position.

- Beneficiary of government schemes supporting API production.

Conclusion

Anlon Healthcare Ltd IPO offers exposure to a few manufacturers in India focusing on pharmaceutical intermediates and active APIs with custom manufacturing services. The company’s financial information shows strong recovery in FY25, improved net worth, and better leverage. IPO proceeds will strengthen the balance sheet via capital expenditure and working capital infusion.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)