Banking in India is no longer confined to branches and paperwork. It is happening on screens, swipes, and apps. At the forefront of this shift are neobanks, digital-first platforms that are redefining how users interact with their money. Unlike traditional banks, they operate entirely online, offering services through sleek, app-based interfaces.

While legacy banks still hold the lion’s share of the market, neobanks are steadily gaining ground, especially among younger, tech-savvy users who expect fast, seamless, and intuitive financial experiences. With a strong focus on innovation and accessibility, these platforms are making banking more user-centric than ever before.

What is a Neo Bank?

A neobank is a digital-only financial service provider. It doesn’t have any physical branches but offers banking services entirely through apps or web platforms. Most neo banks operate without a banking license of their own instead, they partner with licensed banks to offer services like savings accounts, UPI payments, and small-ticket loans.

In India, the RBI doesn’t currently permit fully digital banks to operate independently, which means neobanks function more as fintech enablers than full-fledged banks.

How Do Neo Banks Operate?

Neobanks typically partner with regulated banks to offer banking services while they manage the front-end experience. Here’s how the model works:

Banking Partner: Holds customer deposits, complies with RBI regulations, and offers the underlying infrastructure.

Neo Bank: Builds the app, acquires customers, handles onboarding, and enhances user experience using data and technology.

Because they don’t maintain branches or deal with heavy infrastructure costs, neobanks are lean, cost-efficient, and agile in launching innovative features.

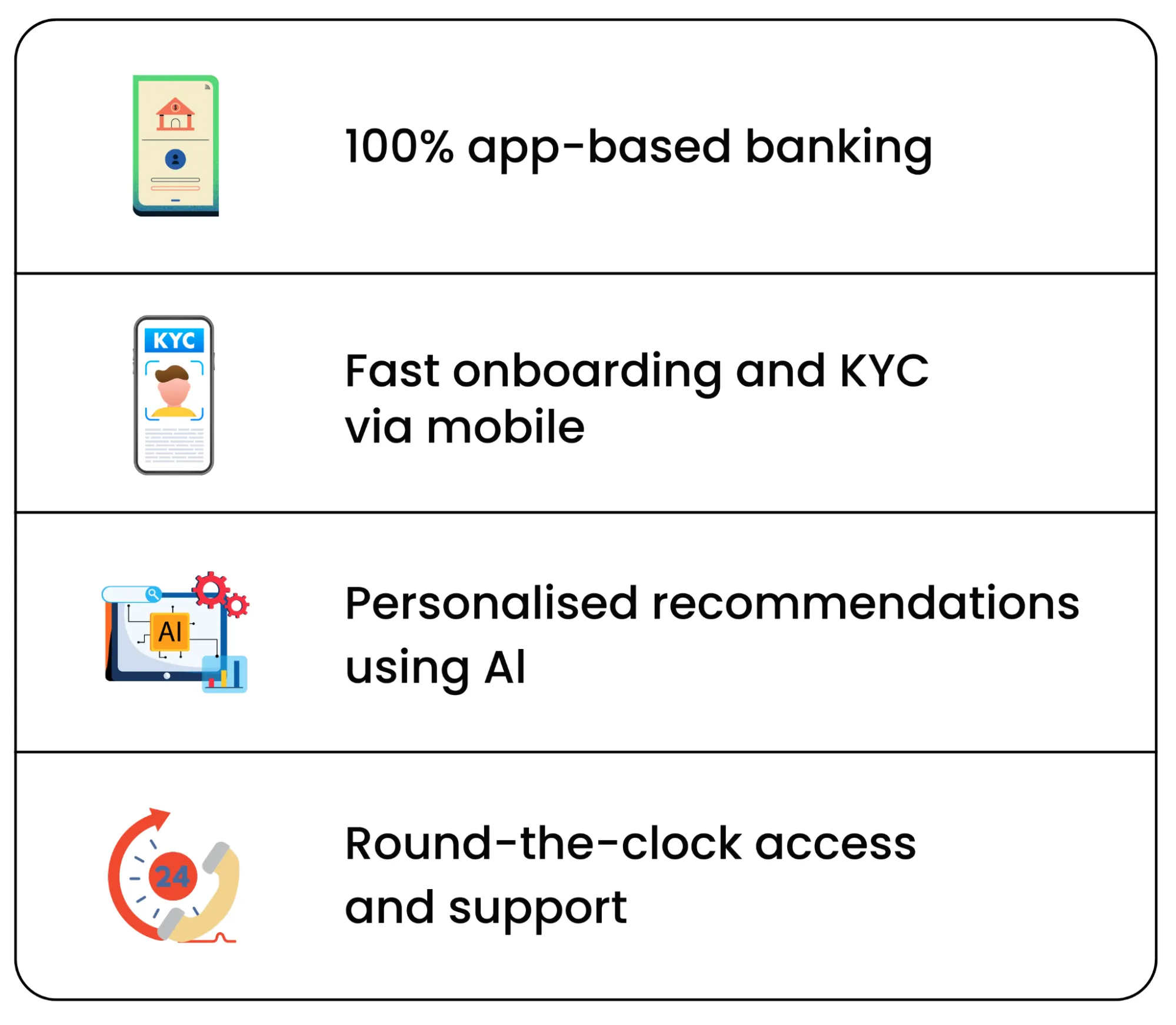

Key Features of Neo Bank

Neo Banks vs Digital Banks vs Payments Banks

Digital Banks: These are often digital arms of existing banks, with licenses and regulatory oversight. They may still maintain limited branches.

Payments Banks: Licensed by the RBI, they can accept deposits up to ₹2 lakh and offer basic banking, but cannot issue credit products.

Neo Banks: No banking license, but act as tech layers on top of regulated banks to improve customer experience and offer features like lending and credit cards.

Neobanks in India

| Neo Bank | Banking Partner(s) | Key Features |

|---|---|---|

| Fi Money | Federal Bank | Smart savings, rewards, expense insights, and UPI |

| Jupiter | Federal Bank | Salary account, zero-balance, spend analytics, and debit card |

| Niyo | Equitas, DCB Bank, SBM Bank | NiyoX savings, Niyo Global forex card, UPI, zero forex markup |

| RazorpayX | RBI-regulated partners (via Razorpay) | Current accounts, payroll, vendor payouts, and APIs |

| Open | ICICI, Axis Bank, SBM Bank | Business accounts, invoicing, tax tools, and expense cards |

| Zolve | US and Indian banks | US bank account, international credit card, and cross-border payments |

| InstantPay | Yes Bank, ICICI Bank | Salary accounts, payouts, API banking, and low-cost onboarding |

| Akudo | RBI partner banks (varied) | Prepaid card, parental control, and gamified savings |

Why Are Neo Banks Gaining Popularity?

Neobanks appeal to digital natives who value speed, simplicity, and minimal friction in their financial interactions. Their advantages include

Seamless user experience on mobile

Low to no fees for basic services

Faster services, from onboarding to fund transfers

Data-driven personalization based on spending patterns

Points to Consider Before Using a Neo Bank

The RBI does not directly regulate neobanks. Your money is held by a partner bank, not the neobank itself. Most neobanks offer limited services compared to traditional banks. In case of a dispute, redressal could be more complex due to layered partnerships.

Challenges and Limitations

No physical branches: Limited personal touch or in-person assistance.

Fewer products: Some services like large loans, fixed deposits, or investment options may not be available.

Security concerns: Operating entirely online makes them vulnerable to data breaches and cyber threats, despite strong encryption.

So, is it better?

Neo banks are not here to replace traditional banks but to complement them. As India’s regulatory environment evolves and user behaviour becomes increasingly mobile-first, neobanks are likely to play a growing role in reshaping how banking is delivered. If you are someone who prefers speed, simplicity, and zero paperwork, a neobank could be the right choice as long as you understand the trade-offs.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.