Capacit’e Infraprojects Limited (CIL) is a leading Indian Engineering, Procurement, and Construction (EPC) company, specializing in turnkey solutions for high-rise and super high-rise buildings, mass housing, specialty buildings, and urban infrastructure. The company caters to marquee real estate developers and government bodies, offering end-to-end construction services across residential, commercial, and institutional sectors. CIL is recognized for its execution excellence, technical capabilities, and focus on high-value, complex projects.

Business segments and capabilities

A. Construction capabilities

Residential: High-rise, super high-rise, townships, mass housing

Commercial: Office complexes, IT parks

Institutional: Hospitals, educational buildings, MLCPs (Multi-Level Car Parks), hospitality, healthcare, industrial

Specialized Services: MEP (Mechanical, Electrical & Plumbing), finishing, and interiors

B. Project portfolio

The company boasts a strong track record with over 60 completed projects and more than 64 million square feet of constructed area. Its geographical presence spans major urban centers including the Mumbai Metropolitan Region (MMR), Pune Metropolitan Region (PMR), National Capital Region (NCR), Varanasi, Bengaluru, Chennai, and Hyderabad. Notable landmark projects include The Park by Lodha, Piramal Mahalaxmi, and Oberoi Enigma, among others. The company has also earned prestigious recognitions, such as a mention in the Limca Book of Records for the fastest hospital construction, and is distinguished as one of the few organized players specializing exclusively in building construction.

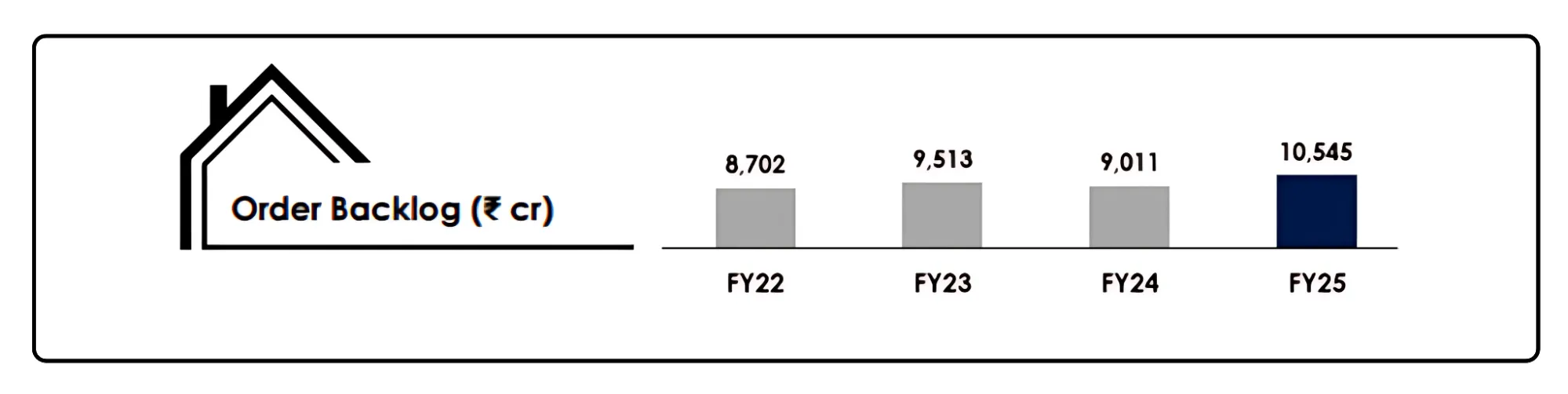

Order book and client mix

Order book

Total order book (Dec 2024): ₹10,545 crore (up from ₹8,702 crore in FY22)

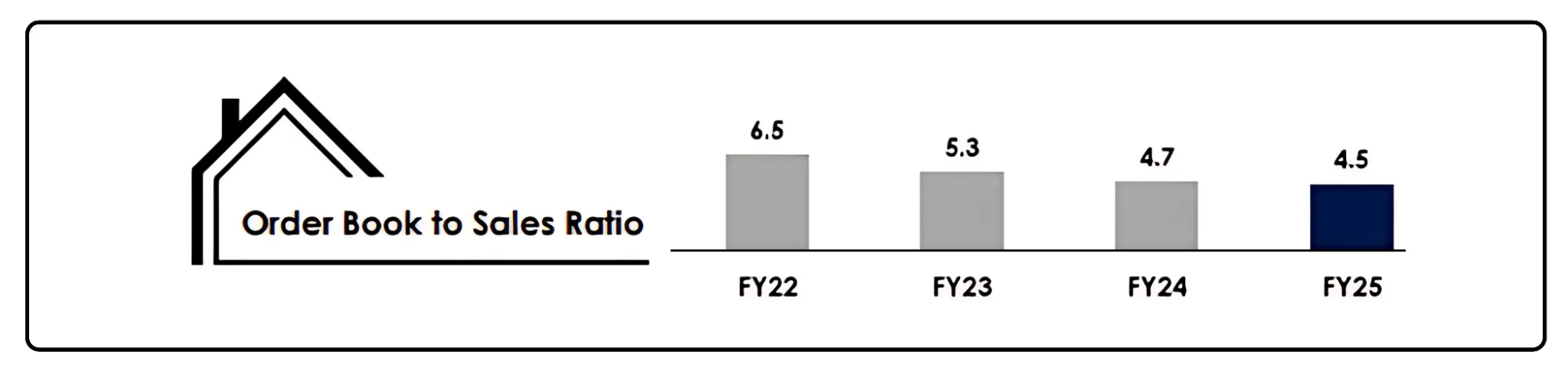

Order Book to Sales Ratio: ~4.5x FY25 revenue, providing multi-year growth visibility.

Order book mix

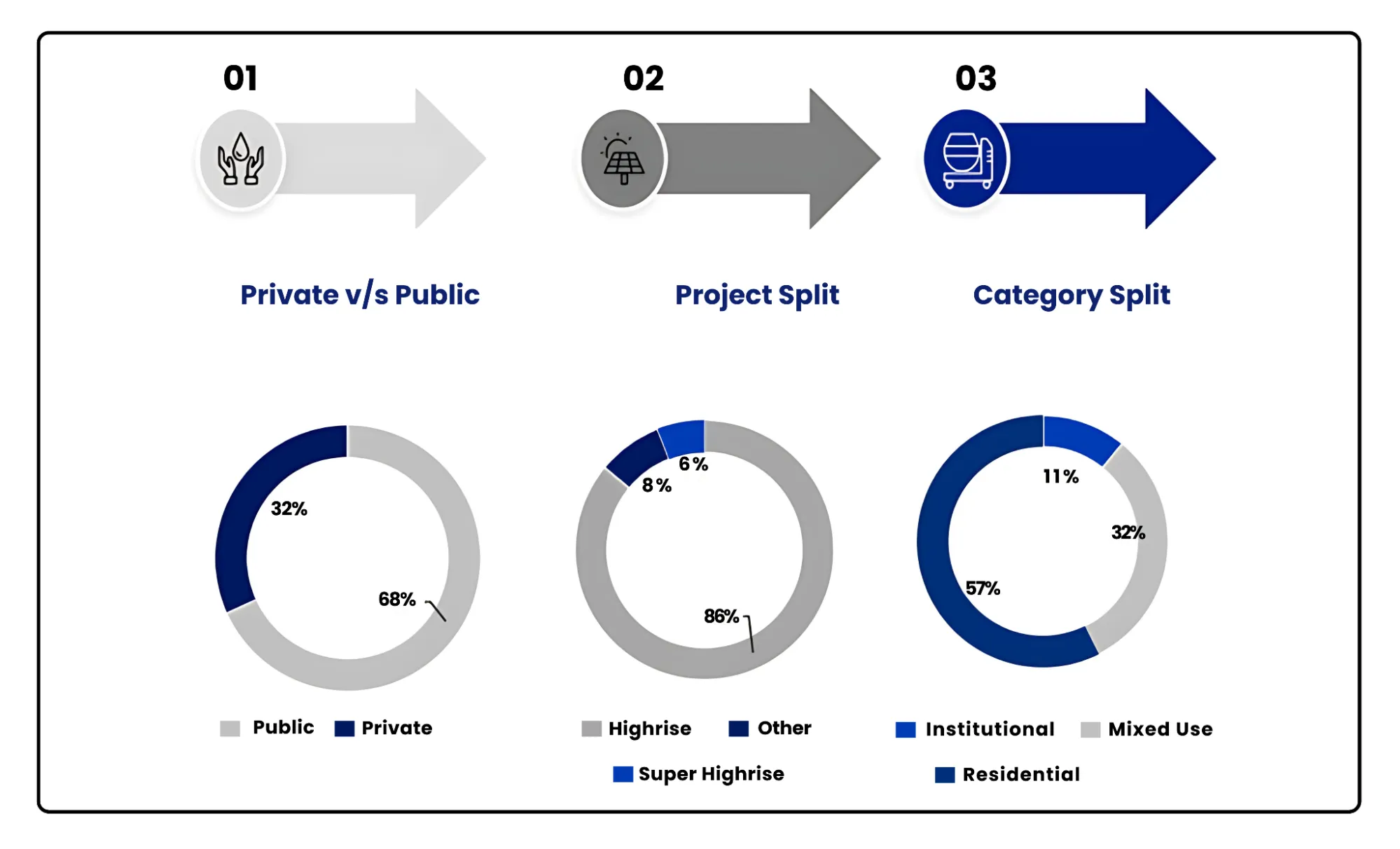

By category (FY25):

Residential: 57% (vs. 30% in FY22)

Mixed Use: 32% (vs. 56%)

Institutional: 11% (vs. 15%)

By client:

Public Sector: 68% (CIDCO, MHADA, Indian Oil, BSNL, etc.)

Private Sector: 32% (Raymond, Piramal Realty, Prestige, Lodha, DLF, etc.)

By project split:

Highrise: 86%

Super highrise: 6%

other: 8%

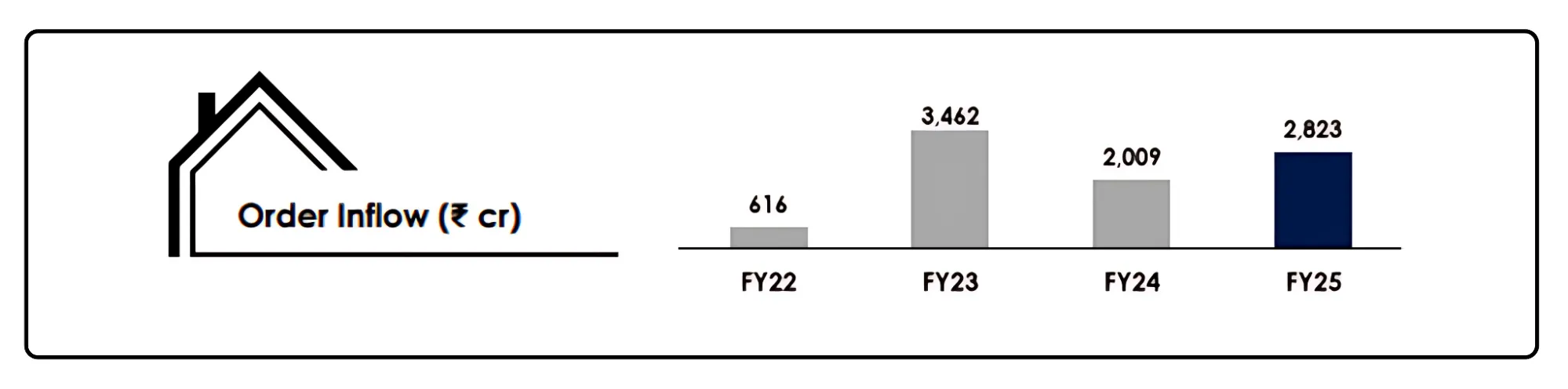

Recent wins: Feb 2025: ₹1,320 crore EPC contract from NBCC for a residential project in Greater Noida.

Marquee Clients

| Public Sector Clients | Private Sector Clients |

|---|---|

| MHADA (Maharashtra Housing and Area Development Authority) CIDCO (City and Industrial Development Corporation) Public Works Department, Government of Maharashtra Municipal Corporation of Greater Mumbai BSNL (Bharat Sanchar Nigam Limited) Gujarat International Finance Tec-City (GIFT City) Indian Oil Corporation Saifee Burhani Upliftment Trust |

Oberoi Realty GIC Piramal Realty K Raheja Corp Raymond Realty Brookfield Godrej Properties Prestige Group Brigade Group Lodha Group Tata Trusts The Phoenix Mills Limited Signature Global M3M DLF |

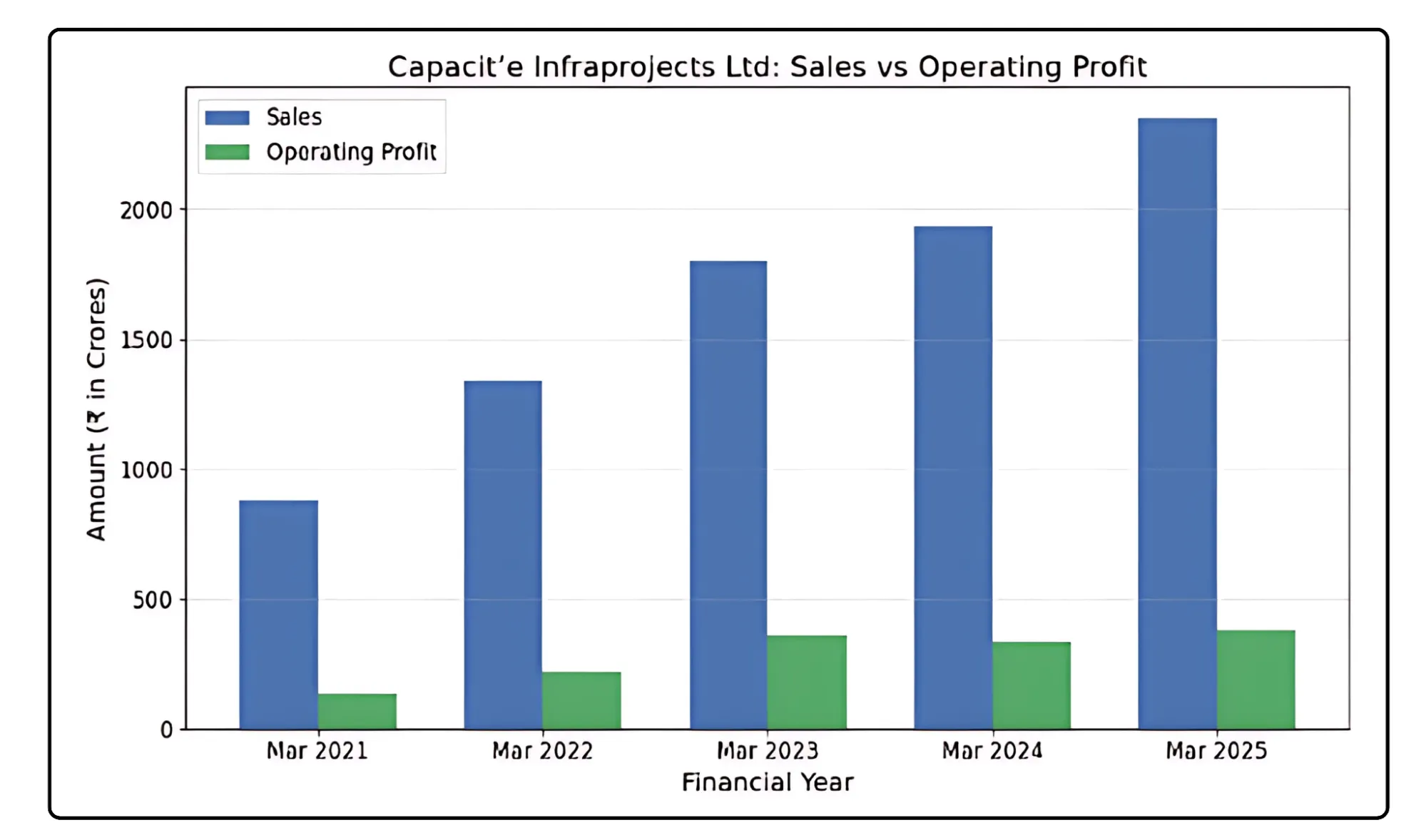

Financial performance

| Metric | FY24 | FY25 | FY26E (TTM) | Growth YoY |

|---|---|---|---|---|

| Revenue (₹ Cr) | 1,932 | 2,350 | 2,900 | +22% |

| EBITDA (₹ Cr) | 334 | 379 | - | +13.5% |

| EBITDA Margin (%) | 17 | 16 | 17 | -100bps |

| PAT (₹ Cr) | 120 | 204 | 255 | +70% |

| PAT Margin (%) | 6.2 | 8.7 | - | +250 bps |

| Order Book (₹ Cr) | 9,011 | 10,545 | - | +17% |

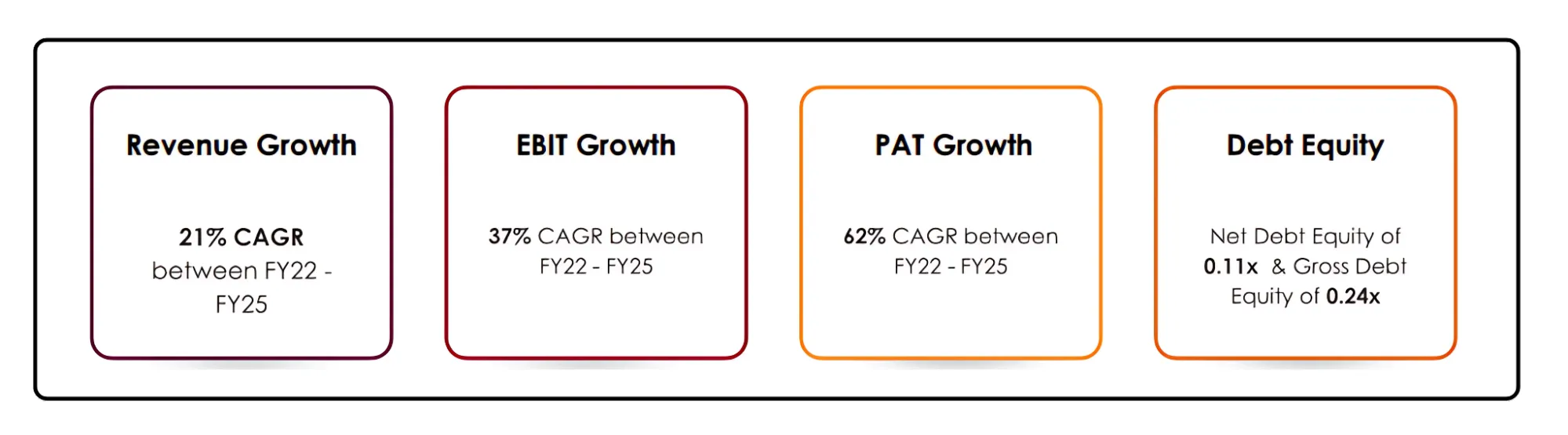

Other notable highlights include a capital expenditure of ₹45 crore in FY24, primarily directed towards equipment and technology upgrades. In January 2024, the company raised ₹200 crore through a Qualified Institutional Placement (QIP), further strengthening its balance sheet. The cost structure remains stable, with construction costs—comprising materials, labor, and subcontractors—consistently accounting for 65–66% of revenue

Strategic focus and growth drivers

A. Sectoral strengths

The company is a preferred contractor for complex high-rise and super high-rise structures, with a strong execution track record and an active pipeline that includes a joint venture with Tata Projects for constructing 300-meter-tall towers. In the data center segment, it has successfully delivered 11 facilities for BSNL and continues to pursue new bids, leveraging its design partnerships and EPC (Engineering, Procurement, and Construction) expertise. Broader industry tailwinds such as government-led housing initiatives, urban infrastructure development, and the expanding digital economy—particularly in data centers—are expected to drive sustained growth.

B. Execution excellence

The company maintains an optimized project portfolio, emphasizing fewer but larger projects that generate higher revenue per project and enhance overall management efficiency. Its order book reflects a well-balanced mix of public and private sector clients, with a strategic focus on high-value, margin-accretive projects that support profitability and long-term growth.

Future growth outlook

A. Revenue and order book execution

At the current revenue run rate of approximately ₹2,350 crore per year, the company’s ₹10,545 crore order book offers a revenue visibility of around 4.4 years. However, with anticipated revenue growth, this execution timeline could shorten to 3.5–4 years.

B. Earnings growth

The company reported an exceptional 70% year-on-year growth in PAT during FY25. Looking ahead, a more sustainable forward PAT CAGR of 20–25% is estimated over the next 2–3 years, supported by strong project execution, consistent new order wins, and ongoing margin expansion.

C. Margin expansion

The EBITDA margin contracted to 16% in FY25. Management anticipates margin enhancement to around 18% driven by operational efficiencies and a strategic focus on selecting high-margin projects.

D. Sector tailwinds

Urbanization, rising housing demand, and the expansion of digital infrastructure are fueling strong momentum in residential, mixed-use, and data center projects. Additionally, continued public sector investments in housing, healthcare, and urban infrastructure under various government initiatives are expected to further support industry growth and project pipeline expansion.

Valuation analysis

A. Current valuation metrics

| Metric | Value |

|---|---|

| Market Cap | ₹2,834 Cr |

| Current Price | ₹335 |

| Current P/E | 14.0 |

| P/S | 1.21 |

| Order Book | ₹10,545 Cr |

B. PEG ratio

The current PEG ratio, based on a forward PAT CAGR of 22%, stands at 0.63. This suggests that the stock is undervalued relative to its future growth potential, indicating there is room for a P/E re-rating as growth is expected to sustain.

C. Peer comparison

The sector P/E for mid-cap Infra/EPC companies ranges between 15–22x. Capacit’e trades at the lower end of this range, despite demonstrating higher growth and margin potential, highlighting an undervaluation relative to its peers.

D. Upside triggers

Key growth drivers for the company include sustained order inflows and strong project execution, ongoing margin expansion, and effective cost control measures. Additionally, the reversal of one-off expenses, such as the GST provision, is expected to further boost profitability. The sectoral growth in high-rise and data center construction also provides significant tailwinds for continued success.

Risks and mitigants

Execution Delays: Mitigated by management’s track record and focus on project selection

Working Capital Cycles: Improved by prudent financial management and recent fundraise

Regulatory/Client Risks: Diversified client base and strong legal standing on GST reimbursement

Strategic growth drivers

Capacit’e Infraprojects Limited is entering a high-growth, high-margin phase, underpinned by a record order book, strong execution capabilities, and sectoral tailwinds. The company’s financial performance in FY25 has set new benchmarks, with significant improvements in revenue, margins, and profitability. With strong order inflows, a healthy balance sheet, and a forward PEG ratio well below 1, Capacit’e is attractively valued relative to its growth prospects.

Capacit’e offers a compelling opportunity for long-term investors seeking exposure to India’s infrastructure and urbanization boom. The company’s focus on high-value, complex projects, coupled with prudent financial management and sectoral growth drivers, positions it for sustained outperformance and potential valuation re-rating.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.