If you have ever sold a long-term asset, such as land or property, you have likely encountered the term Cost Inflation Index (CII). It's a crucial concept that helps reduce your tax liability by adjusting the purchase price of assets for inflation. But with recent changes coming into effect in July 2024, it's more important than ever to understand how this works.

What is the Cost Inflation Index (CII)?

The cost of goods and services increases over time due to inflation, reducing the value of money. For example, ₹10 lakh today won’t have the same value 20 years later. To account for this while calculating capital gains, the government uses the Cost Inflation Index, notified annually by the Central Board of Direct Taxes (CBDT). The base year is 2001–02, with a CII value of 100. Each year, a new value is notified. For the current financial year 2025–26, the CBDT has set the CII at 376.

Why is CII Used?

CII allows taxpayers to claim indexation benefits on long-term capital assets, mainly real estate. Indexation adjusts the purchase price of an asset to reflect inflation, thus reducing the capital gains and the tax payable on them.

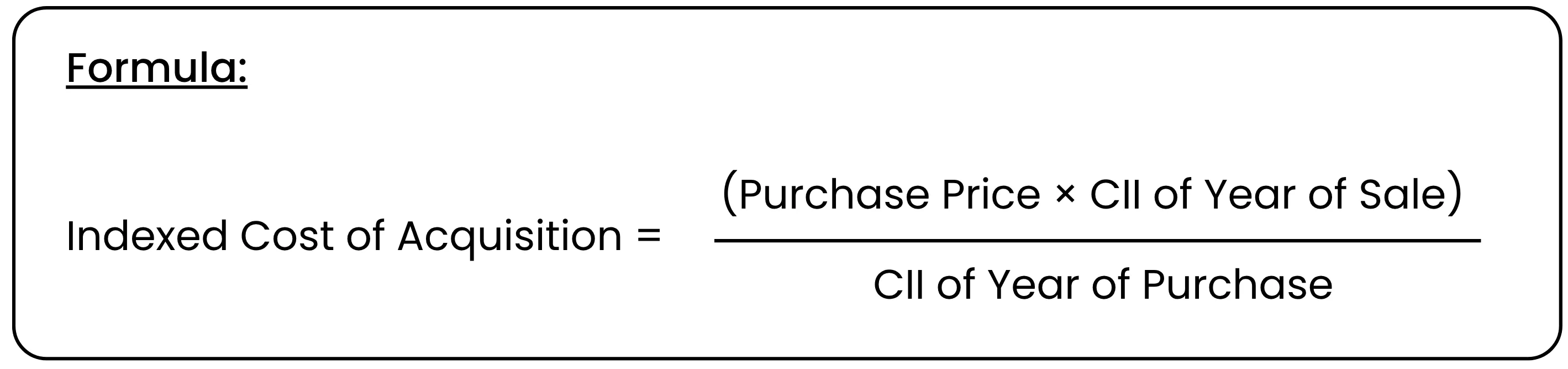

Example Calculation:

Let’s say you bought a property in 2003 for ₹5 lakh and sold it in 2022 for ₹20 lakh.

Without Indexation

LTCG = ₹20 lakh – ₹5 lakh = ₹15 lakh

With Indexation

₹5 lakh × (CII in 2022: 331 / CII in 2003: 109) = ₹15,18,348

LTCG = ₹20 lakh – ₹15,18,348 = ₹4.81 lakh

Using indexation significantly lowers your tax burden. Accurate computation of the indexed cost of acquisition using the CII value for the year of sale ensures that investors can minimize their taxable capital gains when selling long-term real estate assets.

What Changed from 23 July 2024?

As per the Finance Act, 2024, changes were introduced to the long-term capital gains framework. The availability of indexation now depends on the type of capital asset and applicable provisions under the Income-tax Act.

What this means:

For property purchased before 23 July 2024, you can choose between:

12.5% LTCG tax without indexation, or

20% LTCG tax with indexation

For transfers taking place on or after 23 July 2024, the applicable LTCG rate and availability of indexation depend on the nature of the asset and specific provisions of the amended law.

Latest CII Values (as per CBDT up to FY 2025–26)

| Financial Year | CII Value |

|---|---|

| 2021–22 | 317 |

| 2022–23 | 331 |

| 2023–24 | 348 |

| 2024–25 | 364 |

| 2025–26 | 376 |

What should investors do?

Check purchase dates carefully. If you bought land or a house before 23 July 2024, you can still take advantage of indexation.

When selling property purchased before 23 July 2024, a thorough assessment of your tax options is crucial to determine whether the 12.5% LTCG tax without indexation or the 20% tax with indexation results in a lower tax liability.

Understand the real gain. Use the CII to calculate the indexed cost before deciding how to declare capital gains.

Always compare 12.5% without indexation vs. 20% with indexation if you’re eligible. In some cases, the 20% option could still mean lower tax outgo

While indexation can significantly reduce your tax burden, investors should also explore any available exemption options, such as reinvesting capital gains into specified bonds or residential property, to optimize their tax savings further.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.