Back in my college days, even though I came from a comfortable, affluent family, managing money on my own was a different challenge. It became one of the biggest personal finance lessons for students. Designer clothes, fine dining, weekend getaways, and the latest gadgets always caught my eye. I often craved those little luxuries that seemed just beyond my monthly allowance. Around that time, banks were aggressively offering “free” student credit cards, and it felt like the perfect gateway to upgrade my lifestyle without waiting. Like many exploring a student credit card in India, I wondered, should I get my first credit card?. I applied for one, and soon enough, that sleek piece of plastic was in my wallet.

To me, it wasn’t just a card, it was freedom, my first credit card experience. No more holding back on dinners at upscale places, no more postponing that new watch or branded shoes. It felt like one of those first-time credit card user tips that said: enjoy now, worry later. For a while, it felt like life had shifted gears. Until the first bill arrived. I expected something around ₹5,000. What landed instead was ₹12,000 plus interest and fees. My heart sank, it was my first real credit card bill shock. Every indulgent swipe had piled up quietly, and now the reality was staring at me in bold print. That’s when I realised the danger of first credit card mistakes.

The Lesson Behind the Bill

I couldn’t help but compare it to the stock market. A credit card swipe felt like chasing a hot stock tip thrilling at the start, but painful when the reality set in. My ₹12,000 bill was like buying high and regretting later. It was the classic case of credit card vs investment. To make it worse, I calculated what could have happened if I had invested that money instead. At a modest 12% CAGR over five years, it could have grown into nearly ₹21,000. That’s how I learned how to build wealth instead of debt. That number hurt more than the debt itself.

From that day, I made two rules:

Always pay the bill in full—never just the minimum.

Before every swipe, ask—“Is this money better spent or better invested?”

Slowly, I shifted. The thrill of “buy now, pay later” was replaced by the quiet satisfaction of funneling money into SIPs and ETFs. The card stopped being a trap and became what it was meant to be a backup, not a lifestyle.

Full Circle

Today, working at Tradejini, I see this story from the other side. Banks and financial institutions frequently approach me with new credit cards that offer lifetime free, extra rewards, lounge access. They sound tempting, just like they did in my college days. But this time, I know better. It’s one of the best pieces of credit card advice for college students I could give.

The difference is awareness. Back then, I saw a credit card as free money. Now, I see it as borrowed money, useful when disciplined, dangerous when misused. The irony? Many of my friends who once laughed at my bill shock are still juggling EMIs and rolling balances today. Many are stuck in the credit card debt trap. For me, that one painful lesson set the foundation.

The Bigger Truth

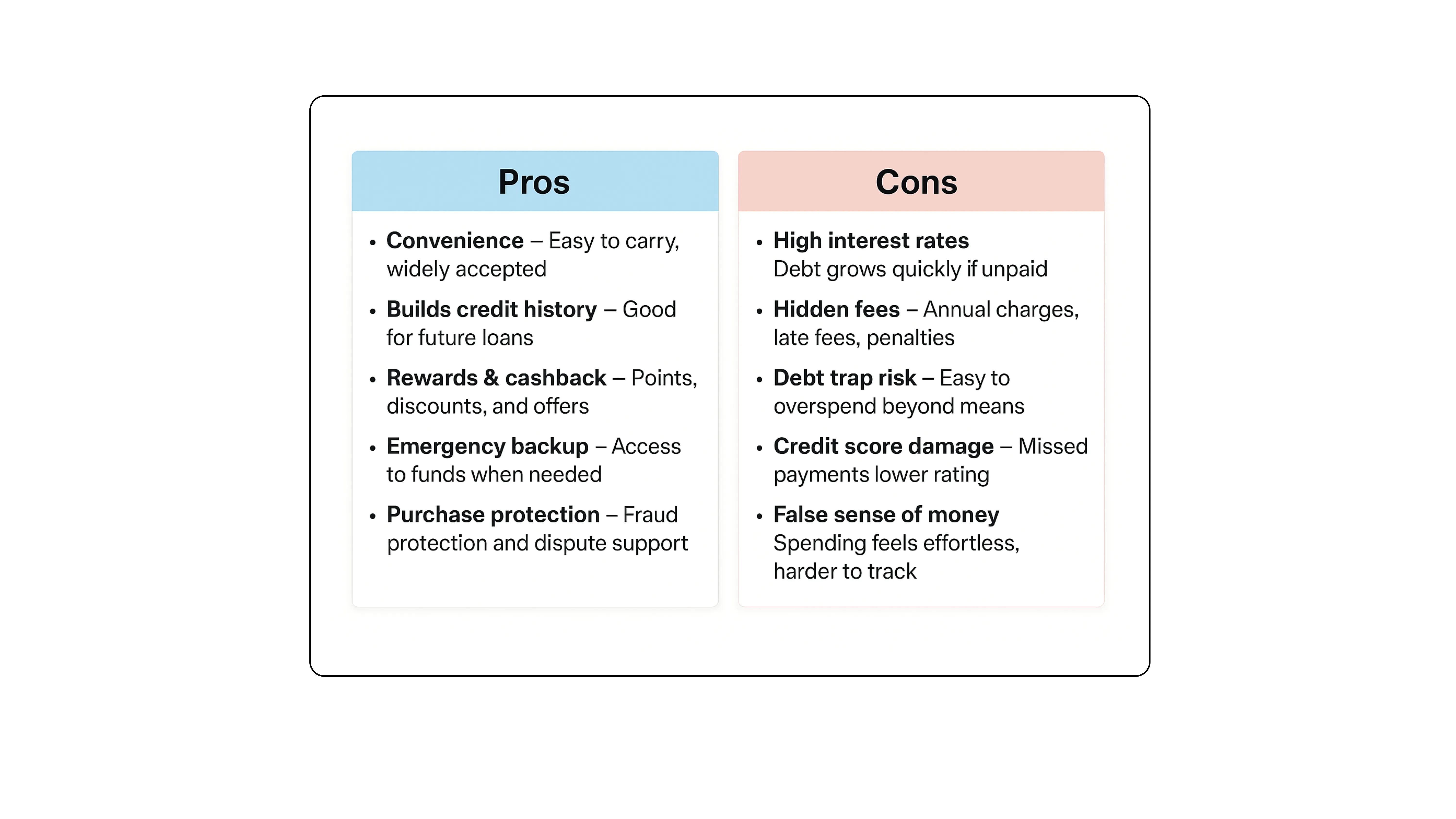

Credit cards and investments are both double-edged swords. Impulse cuts deep, discipline builds wealth. That sums up credit card pros and cons for beginners. One missed payment can stick on your credit history for years, just as one rash trade can wipe out months of gains. Both demand patience, responsibility, and the willingness to think long-term.

My Takeaway

That first bill wasn’t just a financial mistake, it was my introduction to financial literacy. It taught me that money has two paths: it either disappears into consumption or compounds into growth. And every rupee I earn today stands at that same crossroads. That’s the essence of financial literacy for young professionals.

So the next time you’re tempted to swipe or to jump into a stock, pause for a moment and ask: Am I building debt, or am I building wealth?

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.