Entero Healthcare Solutions Limited, a prominent pharmaceutical distributor in India, supplies a wide range of healthcare products to hospitals, clinics, and pharmacies. These include medicines (pharmaceuticals), medical equipment and tools, everyday medical supplies like gloves and syringes (consumables), and health supplements (nutraceuticals). Company sources products from over 2,000 manufacturers and offers more than 76,600 stock-keeping units (SKUs). In essence, Entero acts like a comprehensive health supermarket for hospitals and pharmacies, ensuring they have access to everything they need from trusted sources. As of December 2024, Entero earned ₹9 as gross profit for every ₹100 worth of medicine distributed (before other expenses). Over the past year, the company recorded product sales worth ₹4,791 crores and a net profit of ₹97 crores.

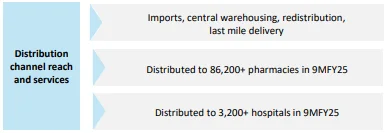

Founded in 2018, Entero Healthcare Solutions Limited has rapidly emerged as one of the largest and fastest-growing players in India’s healthcare distribution space. It operates a technology-driven, integrated supply chain platform that serves over 86,200 retail pharmacies and more than 3,200 hospitals across 20 states and union territories.

What are the business plans to increase sales?

The company’s mission is to consolidate the highly fragmented Indian healthcare distribution market by offering end-to-end commercial and supply chain solutions, supported by advanced digital platforms and a pan-India logistics network.

Business segments

Entero’s operations are organized into the following key business segments:

- Pharmaceutical distribution: This is the largest segment, supplying both prescription and over-the-counter (OTC) medicines to retail pharmacies and hospitals. Entero holds one of the largest hospital customer networks among pharmaceutical distributors in India, serving over 3,200 hospitals and supplying approximately 1 in every 10 pharmacies nationwide.

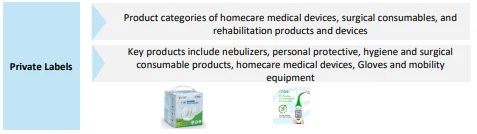

Medical devices and consumables: This includes homecare medical devices (such as nebulizers, blood pressure monitors, and digital thermometers), surgical consumables, personal protective equipment, gloves, and rehabilitation products. This is a growing focus area contributing to margin expansion due to its higher profitability.

Nutraceuticals and vaccines: Distributed to pharmacies and hospitals, these products complement the core pharmaceutical offerings and expand Entero’s product portfolio.

- Private label products: Entero markets and sells products under its brand, including medical devices and consumables, enhancing control over margins and boosting customer loyalty.

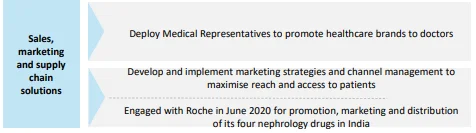

- Commercial and supply chain solutions: These value-added services include sales, marketing, promotion, and demand generation for healthcare product manufacturers. Entero deploys medical representatives and leverages data-driven insights to optimize brand performance and market reach.

Revenue Share by Business Segment

| Segment | Revenue Share (FY24) | Notes |

|---|---|---|

| Pharmaceutical distribution | ~98%+ | Core business; includes all major distribution activities |

| Private label products | ~1% | Limited to non-pharma (mainly medical devices and consumables) |

| Commercial & supply chain solutions | <1% | Value-added services, not a material standalone revenue contributor |

Market share and positioning

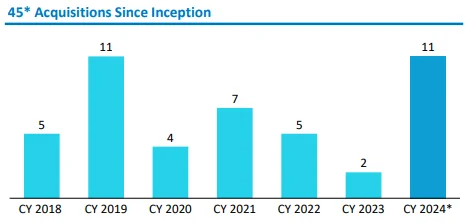

Entero ranks among the top three healthcare product distributors in India and holds a significant share of the hospital distribution segment. It boasts the largest hospital customer network in the country. Among medical supply distribution companies, Entero stands out for its expansive hospital network and acquisition-driven growth model. The strategy of acquiring and integrating smaller distributors has significantly accelerated its market share growth, with 45 acquisitions completed by FY24, enabling rapid geographic and product portfolio expansion.

![]()

From ₹ 293 crores of sales in 2019, it has grown to ₹ 4791 crores in the last twelve months(TTM).

Future outlook and valuation

The company is well-positioned for strong revenue and earnings growth over the next three years. The TTM revenue is ₹4791 crores, which is projected to reach approximately ₹8,900 crores by FY28 at a CAGR of 23%, driven by expansion in medical devices, increasing demand for consumables, and rising traction in private label products. This projection is based on management’s conservative estimates.

EBITDA margins are expected to improve to 4–5% by FY27. Assuming a 4% EBITDA margin, the company would generate an EBITDA of ₹356 crores, supported by scale benefits and growing contributions from high-margin segments.

The stock currently trades at a P/E ratio of 65, based on a market price of ₹1,350. Factoring in other income, interest payments, depreciation ,and tax, PAT is estimated at around ₹200 crores. Assuming unchanged equity capital, EPS is projected at ₹46, resulting in a two-year forward P/E of 29.30. While this valuation appears high, it should be viewed in the context of the company’s long-term earnings potential. As healthcare demand grows and the Indian sector evolves, Entero is strategically positioned for sustainable success.

Key risks

- Negative Operating Cash Flows: These pose risks to liquidity and financial flexibility, although management expects positive operating cash flows in the upcoming quarters.

- Integration Risk: Rapid, acquisition-driven growth necessitates effective integration to realize synergies and prevent disruptions.

- Competitive Market: With ~90% of the Indian distribution market controlled by small, local players, Entero must continuously invest in technology and services to maintain its market share.

- Regulatory Environment: Changes in healthcare policies or distribution regulations could impact operating dynamics.

Scalable play on India’s healthcare growth story

India’s pharmacy market is expected to grow significantly, from $25.4 billion in 2018 to $53.1 billion by 2030, driven by rising chronic illnesses, better access to care, and the shift toward organized retail. Entero Healthcare Solutions, with its presence across hospital and retail distribution, aims to benefit from this trend. Its acquisition-led growth, diversified product portfolio, and tech-driven supply chain support scalability. While challenges like integration and financial leverage exist, the company’s expanding network positions it to participate meaningfully in India’s evolving healthcare ecosystem.