When it comes to mutual funds, there’s no single formula that works for everyone. Your ideal mutual fund depends largely on your risk appetite, investment horizon, and financial goals. Whether you are looking for long-term wealth creation, regular income, or portfolio stability, choosing the right fund type, such as Equity, Debt, or Hybrid, is crucial. Mutual fund schemes are classified by SEBI into categories such as equity, debt, hybrid, and solution-oriented funds to help investors choose based on their goals.

Equity mutual funds: For growth-oriented investors

Equity mutual funds primarily invest in shares of listed companies and are designed for long-term wealth creation. Since they are directly linked to the stock market, they are subject to short-term volatility. However, this volatility often evens out over longer periods, offering higher return potential compared to other fund types.

These funds are best suited for investors who have a higher risk appetite and can stay invested through market ups and downs. Typically, equity funds perform well in growing economies or bullish market cycles, but may see temporary dips during market corrections or global uncertainties

Individuals in their early earning years, or those aiming to build a strong corpus for long-term goals. Over time, rupee cost averaging through SIPs and the power of compounding can help cushion volatility and boost returns if investors stay disciplined.

Below are different types of schemes in Equity mutual fund

Multi Cap Fund: Invests at least 75% in equities, spread equally across large, mid, and small cap stocks (25% each). Suitable for diversified long-term exposure.

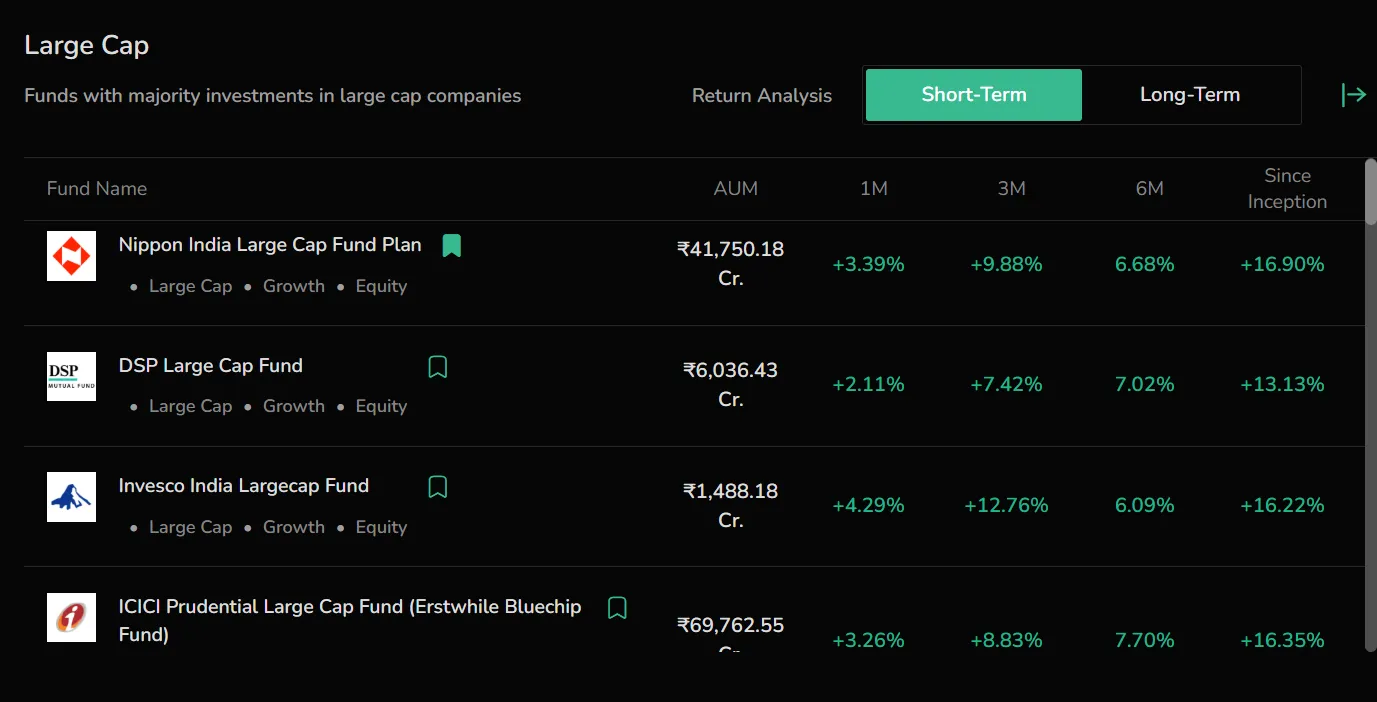

Large Cap Fund: Focuses at least 80% on India’s top 100 companies by market cap. Offers stability with moderate returns. Large-cap equity funds invest in well-established, large companies.

Large and Mid-Cap Fund: Allocates at least 35% each to large and mid-cap stocks. Balances safety and growth.

Mid Cap Fund: Requires 65% investment in mid-cap companies (101st-250th by market cap). Potential for higher returns, with increased risk. Mid-cap funds focus on medium-sized companies, balancing growth potential and risk.

Small Cap Fund: Minimum 65% in small-cap stocks (251st onward). High return potential but with significant volatility. Small-cap funds invest in smaller companies with high growth potential and higher risk.

Dividend Yield Fund: At least 65% in dividend-yielding equities. Good for investors seeking income and moderate growth. These funds focus on dividend-yielding stocks to provide regular income.

Value or Contra Fund: Invests a minimum 65% in undervalued or out-of-favour stocks. Suitable for seasoned investors who understand cyclical investing. Value funds follow a value investment strategy, seeking undervalued stocks for long-term gains.

Focused Fund: Invests in a maximum of 30 stocks, with at least 65% in equities. Can be multi-cap or focused on a specific cap category.

Sectoral/Thematic Fund: Minimum 80% investment in a specific sector or theme. High risk, high reward. Best for informed investors. Emerging market funds focus on developing economies and come with higher risk.

ELSS (Equity Linked Savings Scheme): 80% in equities, with a 3-year lock-in. Offers tax benefits under Section 80C under the old regime.

Flexi-cap Fund: At least 65% in equities, with no cap restrictions. Provides flexibility to switch across market caps as per opportunities. Index funds follow a passive investment strategy, tracking specific market indices like the Sensex or Nifty 50.

Growth funds and aggressive growth funds are types of equity funds that focus on capital appreciation and accept higher risk, making them suitable for long-term, risk-seeking investors.

Debt mutual funds: For conservative or income-focused investors

Debt funds invest in fixed-income instruments and are ideal for those who want steady returns with lower risk. These funds are ideal for individuals with short- to medium-term financial goals such as saving for a child’s education within five years, building an emergency fund, or parking surplus funds temporarily. Retired individuals or those nearing retirement also consider debt funds to preserve capital while earning regular returns.

Debt mutual funds invest in debt market securities such as government bonds, PSU bonds, and non-convertible debentures, providing a range of options for different risk profiles.

For example, a Short Duration Fund can be suitable for someone planning a big purchase in 2 to 3 years and wants better returns than a fixed deposit with manageable risk.

Debt funds come with different risk profiles based on duration and credit quality, so selecting the right type based on your investment horizon and risk appetite is essential

Below are different types of schemes in Debt mutual fund

Overnight Fund: Invests in 1-day maturity securities. Lowest risk, ideal for parking surplus funds.

Liquid Fund: Maturity up to 91 days. Suitable for emergency corpus. These funds invest in short-term debt instruments and money market securities to ensure high liquidity and minimal risk.

Ultra-Short/Low/Short Duration Funds: Varying maturities from 3 months to 3 years. Balances liquidity and returns.

Money Market Fund: Instruments with up to 1-year maturity. Slightly higher return potential. Money market funds invest in money market instruments like treasury bills, commercial papers, and certificates of deposit.

Medium to Long Duration Funds: Invest in instruments with 3 to 7+ years maturity. Suitable for medium-term goals, but sensitive to interest rate changes.

Dynamic Bond Fund: Actively managed across durations. Suitable in uncertain interest rate scenarios. Dynamic bond funds adjust portfolio duration based on interest rate trends.

Corporate Bond Fund: Minimum 80% in AA+ or above rated corporate bonds. Stable and predictable. Corporate bond funds focus on high-rated corporate bonds for steady income.

Credit Risk Fund: Invests 65% in lower-rated corporate bonds (AA and below). Higher returns but also higher credit risk. Fixed income securities in these funds provide stable returns for conservative investors.

Banking and PSU Fund: 80% in debt from banks and PSUs. Relatively safer among debt funds. Bond funds are a key segment of mutual funds that invest in bonds for stability and diversification.

Gilt Fund / Gilt 10-year: Minimum 80% in government securities. Zero credit risk, but rate sensitive. These funds primarily invest in government bonds, offering low credit risk.

Floater Fund: Minimum 65% in floating rate instruments. Useful during rising interest rate cycles. Fixed maturity funds have a set maturity period and offer predictable returns.

Money market funds are considered very low-risk funds suitable for capital preservation.

Also Read: ELSS Mutual Funds: Best Tax Saving Options in 2025

Hybrid mutual funds: For balanced risk and return

Hybrid mutual funds invest in a mix of equity and debt instruments, offering a balanced approach to investing. They are ideal for investors with a medium risk appetite who want to benefit from the growth potential of equities while cushioning volatility through debt exposure. Hybrid funds combine equity and debt investments to balance risk and reward.

There are different types, like aggressive hybrid funds (more equity) and conservative hybrid funds (more debt), allowing investors to pick based on their comfort with risk. For example, an Aggressive Hybrid Fund might be suitable for someone in their 30s aiming for long-term capital growth but with slightly lower volatility than pure equity funds.

Below are different types of schemes in a Hybrid mutual fund

Conservative Hybrid Fund: Allocates 75–90% to debt and 10–25% to equity. Best suited for conservative investors seeking regular income with limited market exposure. These are debt-oriented hybrid funds with a higher allocation to debt.

Balanced Hybrid Fund: Invests 40–60% each in equity and debt. Designed to maintain an even split without using arbitrage. While rare, it offers a true 50-50 blend for moderate investors. These are balanced funds maintaining a specific allocation between equity and debt.

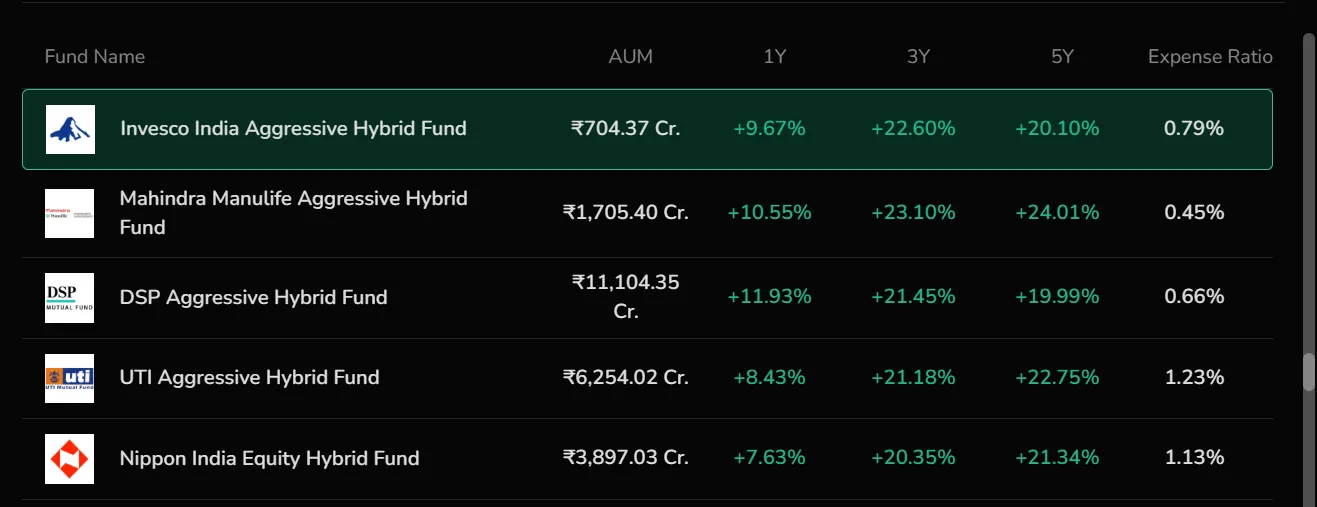

Aggressive Hybrid Fund: Holds 65–80% in equity and 20–35% in debt. Ideal for those with a medium risk appetite who want equity-style growth but with a debt cushion during market corrections.

Dynamic Asset Allocation / Balanced Advantage Fund: Actively shifts allocation between equity and debt based on market conditions. Suitable for investors who prefer fund managers to decide the ideal mix.

Multi Asset Allocation Fund: Invests in at least three asset classes, with a minimum of 10% in each. This diversification reduces reliance on any one market segment. Mutual funds are categorized by the asset class they invest in, such as equities, debt, or real estate.

Arbitrage Fund: Maintains a minimum of 65% in equity via arbitrage strategies. Offers low-risk returns similar to liquid funds, ideal for short-term parking with tax efficiency.

Equity Savings Fund: Combines minimum 65% equity and 10% debt, with the portfolio disclosing hedged and unhedged equity exposure. Suitable for cautious investors wanting tax-efficient growth with limited risk.

Specialised mutual funds offer a tailored approach for specific financial goals, providing unique investment solutions.

Also Read: What Is a Mutual Fund?

Which mutual fund should you choose?

Ask yourself these three questions:

What is your investment horizon? (Short-term = Debt; Long-term = Equity)

How much risk can you tolerate? (Low = Debt; Medium = Hybrid; High = Equity)

Do you need regular income or wealth growth? (Income = Debt/Hybrid; Growth = Equity)

Solution-oriented funds and solution-oriented mutual funds are designed for specific life goals like retirement or children's education, often with a lock-in period until retirement age. Target-date funds align with specific investment horizons and automatically adjust asset allocation as the target date approaches. Retirement funds are long-term investment vehicles with typical lock-in periods until retirement age, focusing on building a corpus for post-retirement income.

For example:

A 25-year-old saving for retirement 30 years away can consider Flexi-cap or Multi-Cap Funds.

A 45-year-old planning for their child’s college education in 5 years might lean towards Aggressive Hybrid or Short Duration Funds.

A retiree looking for low-risk income can opt for Banking and PSU or Gilt Funds.

How Tradejini Mutual Fund helps you pick the right scheme

Tradejini mutual funds simplifies the process of selecting a mutual fund by matching your investment preferences. With just a click, you can filter schemes based on your risk appetite and time horizon. For instance, if you are looking for equity large-cap funds, the platform presents a curated list of schemes from various AMCs. You can easily compare them based on past performance, making it more convenient to choose the one that aligns with your financial goals.

The image below displays the list of funds that appear when the Aggressive Hybrid category is selected.

Asset management companies and professional fund managers oversee mutual fund schemes, ensuring compliance with regulations and providing expert management of your investments. Mutual fund units are bought and sold at the prevailing net asset value (NAV), which determines the price for transactions. Switching between schemes within the same fund house is convenient and allows for easy portfolio adjustments. Other mutual funds, such as Funds of Funds, invest in other mutual funds to provide diversification across asset classes and strategies.

Choosing the right fund is about matching goals, time, and risk

Selecting the right mutual fund category is like choosing the ideal vehicle for your financial journey. Your goal is the destination, your time horizon is the route, and your risk appetite is the terrain. Together, these factors help you decide between equity, debt, or hybrid funds. Different funds manage accept market risks in various ways. While aggressive growth funds accept higher risks for greater returns. Most mutual funds do not have lock-in periods and offer high liquidity, making them accessible and flexible for investors. Mutual funds in India play a significant role in household investment strategies and are regulated by the Securities and Exchange Board to ensure transparency and investor protection. Mutual funds invest in a variety of financial assets such as stocks, bonds, and money market instruments to achieve diversification and meet different investment objectives. Open-ended funds provide liquidity and flexibility, allowing investors to enter and exit at any time. The maturity period is important in closed-ended and fixed maturity funds, defining the investment horizon and exit options. Global funds may include both domestic and foreign investments for broader diversification, and foreign funds invest outside the investor's home country to tap into international opportunities. Debt investments and debt securities provide stability and income, making them essential for conservative portfolios. Mutual fund investors should understand the different fund types and strategies to make informed decisions. Your investment strategy shapes fund selection and asset allocation, ensuring your portfolio aligns with your financial goals.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.