Indian mothers have always been natural financial planners. Whether it's bargaining at the market, saving that extra ₹10 from the household budget, or transforming old sarees into cushion covers, their ability to stretch every rupee is unparalleled. But what if those everyday savings could be transformed into long-term wealth?

Financial independence is no longer just about earning an income. For many Indian mothers, whether homemakers, working professionals, or women restarting their careers, it’s about building a secure and confident future for themselves and their families. It means ensuring that your child’s education is funded, your health needs are covered, and your retirement is on track, all without relying on anyone else.

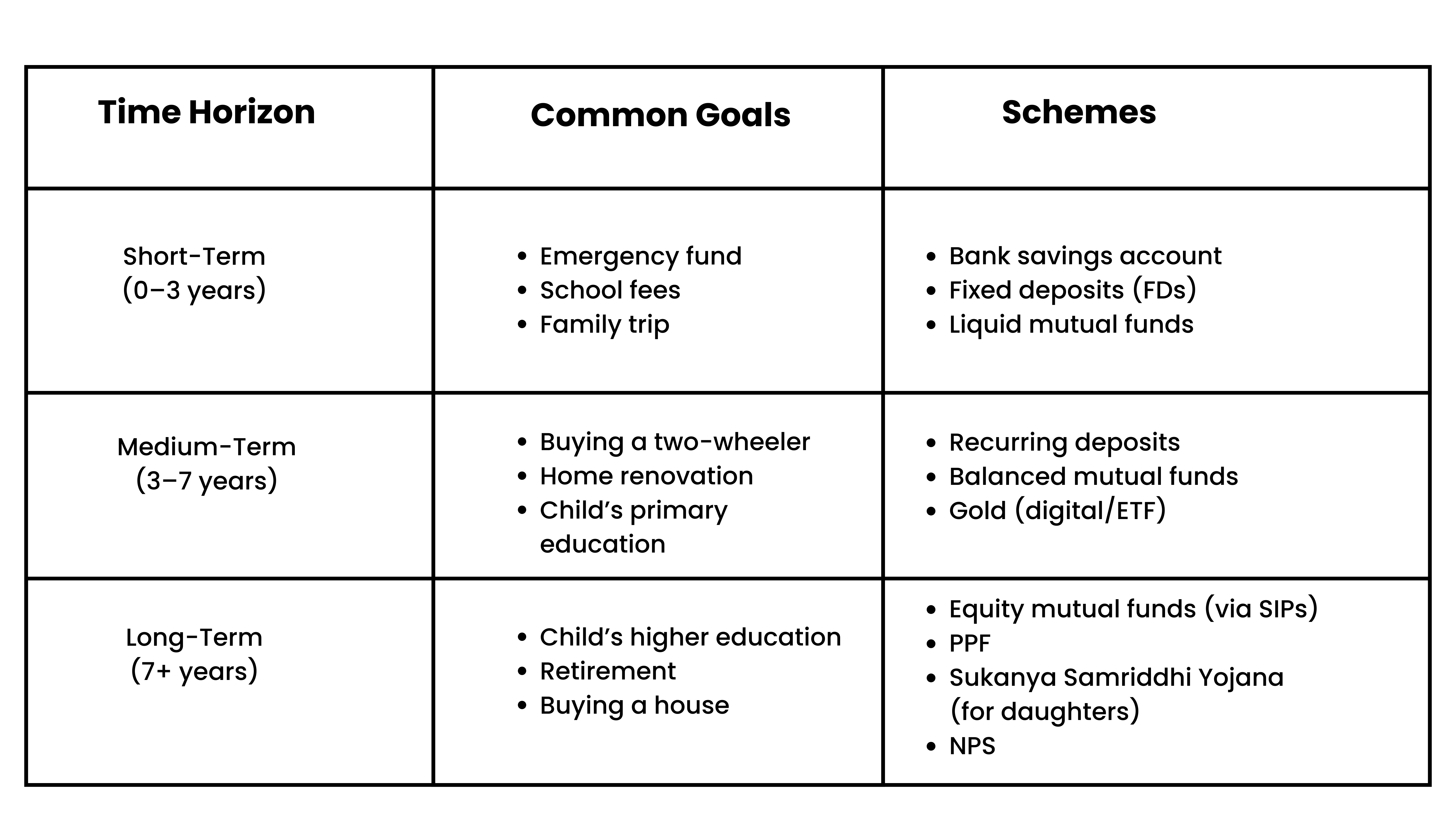

Set financial goals

Match your investment with your goal timeline and stay consistent, no matter how small the amount.

Should you still invest in gold?

Gold has long been a preferred asset for women in India, but modern investment options surpass physical gold in many ways. Gold ETFs, for example, eliminate the risks associated with storage and purity while providing greater liquidity and often lower costs.

Gold is often seen as an emotional investment, particularly when it comes to securing your children’s future. While buying jewellery for milestone events may be tempting, financial gold like ETFs offers greater flexibility. They can be bought and sold easily, track gold prices closely, and provide transparent pricing and value. Over the past decade, gold has delivered a return of 178%, making it a valuable addition to any investment portfolio.

Instead of accumulating jewellery, which often comes with high wastage and making charges, this approach secures your wealth more efficiently

Laying a strong foundation for your child’s future

With education costs rising rapidly, planning ahead is essential. A well-structured Child Education Plan or early investment in a Public Provident Fund (PPF) can make a significant difference. The PPF currently offers an interest rate of 7.1% (as of 2025), is tax-exempt under Section 80C, and has a 15-year lock-in period—making it an ideal option for long-term goals such as your child’s higher education or wedding.

If you have a girl child, the Sukanya Samriddhi Yojana is a viable option, currently offering returns of around 8.2%. Fixed deposits are another safe investment, typically providing returns between 7% and 8%. Ultimately, the right choice depends on your financial goals and needs.

Strong foundation for your child’s future

With education costs rising rapidly, planning ahead is essential. A well-structured Child Education Plan or early investment in a Public Provident Fund (PPF) can make a significant difference. The PPF currently offers an interest rate of 7.1% (as of 2025), is tax-exempt under Section 80C, and has a 15-year lock-in period, making it an ideal option for long-term goals such as your child’s higher education or wedding.

If you have a girl child, the Sukanya Samriddhi Yojana is a viable option, currently offering returns of around 8.2%. Fixed deposits are another safe investment, typically providing returns between 7% and 8%. Ultimately, the right choice depends on your financial goals and needs.

One basket won’t take you far

Financial independence looks different for every mother, but one principle remains universal: diversification. Allocate investments across SIPs and mutual funds for steady growth, include Gold ETFs for security and legacy, and consider PPF or child education plans to secure your child’s future. Avoid relying on a single asset class—instead, align your investments with your financial goals and risk tolerance for a balanced and resilient portfolio

| Mrs Reddy | PPF | Gold | Mutual fund | Total |

|---|---|---|---|---|

| Invested amount for 15 years | 3,60,000 | 3,60,000 | 3,60,000 | 10,80,000 |

| Amount generated after 15 years | 6,00,000 | 11,00,000 | 12,00,000 | 29,00,000 |

Mrs. Reddy’s journey illustrates that no single investment is a magic formula. Her PPF provided stability, gold offered safety and traditional value, while mutual funds delivered higher growth. Combined, these investments transformed ₹10.8 lakhs into approximately ₹29 lakhs over 15 years. Diversifying across asset classes not only reduces risk but also balances returns and better aligns with long-term goals such as children's education and financial independence

Start small, but start now

Whether you are new to investing or looking to build on existing assets, the key is to start early and stay consistent. Financial freedom is not just about earning more, it is about gaining control over your money, setting clear goals, and investing with intention.

This Mother’s Day, let us celebrate the women who have always looked out for us, not just with love, but with wisdom. When mothers make smart financial choices, they are not only investing in themselves, they are building a legacy of security and strength for the entire family.