Brainbees Solutions Limited, operating as FirstCry, is India’s largest multi-channel retailer for mothers’, babies’, and kids’ products. It operates within India’s childcare market, a sector poised for significant expansion with a projected 13-14% CAGR over the next four to five years according to a report by Redseer. The industry’s most compelling feature is its structure; an estimated 84-85% remains unorganized, presenting a massive, long-term consolidation opportunity. This structure shift from unorganized to organized retail is expected to accelerate, driven by rising consumer incomes and evolving preferences. As the largest and most visible organized player, FirstCry is strategically positioned to be the primary beneficiary of this market formalization.

Business model overview

FirstCry has built its business on a sophisticated omnichannel model that integrates its digital platform with a vast network of physical stores. While the business is digitally led, these stores serve as crucial brand-building hubs and customer acquisition points. The model encourages customers to move seamlessly between online and offline channels, a behavior seen frequently among its user case. This physical presence builds trust and drives traffic to the more extensive online platform, enhancing customer loyalty and creating a business model that is difficult for competitors to replicate.

Financial performance overview

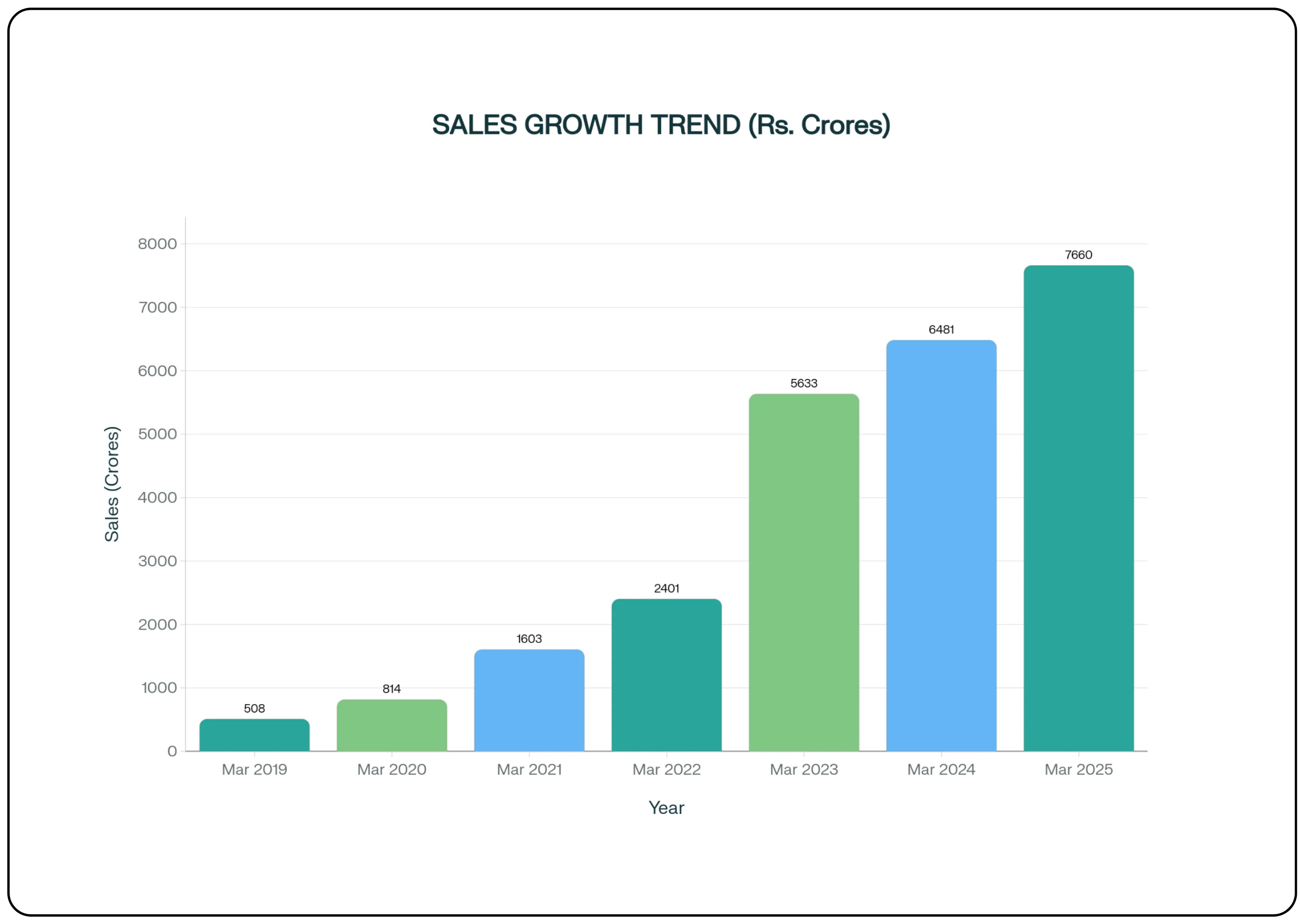

FirstCry is hitting a growth spurt. In FY25, the company’s total sales jumped by an impressive 18%, touching INR 7,660 crores. Even better, it’s not just selling more, it is also making more from each sale. Its profit margins have also increased noticeably, with the gross margin rising to 37.5%. In simple terms, FirstCry is earning more from the revenue it is generating

A pivotal milestone was achieved in FY25 as the core India Multi-channel business turned both Profit After Tax (PAT) and Free Cash Flow (FCF) positive, signaling a transition from a cash-burning growth phase to a more sustainable operational model. While the consolidated entity remains loss-making, the trajectory of operational profitability is a key positive indicator.

Business segments breakdown

FirstCry operates across four distinct business segments, each contributing uniquely to its growth story.

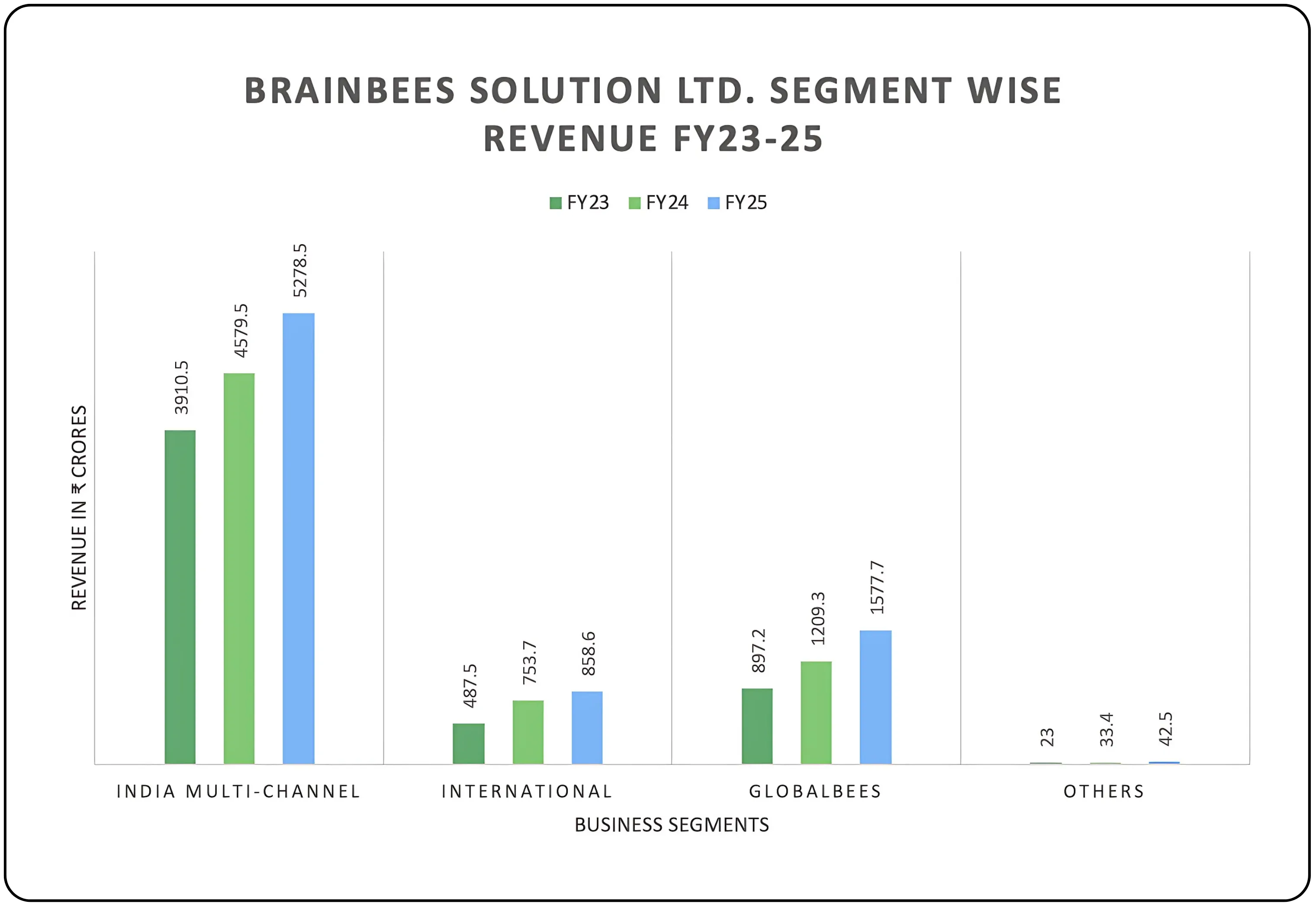

The India Multi-channel business remains the bedrock, demonstrating the underlying viability of the core model. As discussed earlier it integrates online platforms with over 1,000 offline modern stores, including company-owned (COCO) and franchisee stores, and has a distribution network for home brands (in house brands of products) to general trade retail. Home brands like BabyHug contribute over 55% of GMV. This multi-channel approach is improving unit economics and helping customer acquisition.

International Business: This segment is aiming to replicate the India playbook in the Middle East (UAE and KSA), operating primarily as an online-only platform. It plans to establish approximately 12 offline stores in KSA over the next 24-30 months, starting gradually. Their main focus is to tap into the opportunity posited by the significantly higher average order value, around 4.1 times that of the India business. The strategy aims to leverage favorable demographics and market opportunities.

GlobalBees: It is a Direct-to-Consumer (D2C) venture that aggregates and invests in e-commerce brands to help them scale and transform their digital presence. It operates across categories like Home Improvement, Home Appliances, Active Lifestyle & Accessories, and Home & Personal Care. It has strategically been focusing on organic growth and reducing the proportion of less profitable brands in its portfolio. These steps have allowed this segment to achieve a remarkable 9.6x growth in its Adjusted EBITDA margin YoY.

- Others (Preschool Business): This segment comprises the company’s asset-light preschool business, operating on an asset-light franchisee model. It caters to children aged 2.5 to around 6 years. As of FY25, it had 363 operational preschools with 18,470 enrolled students across 160+ cities across India. This segment addresses the largely unorganized and unbranded preschool market in India.

| Segment Name | FY25 Revenue Growth | FY25 Adj. EBITDA Margin |

|---|---|---|

| India Multi-channel | 15% | 9.5% |

| International | 14% | (16%) |

| Globalbees | 30% | 1.4% |

| Others (Preschool) | 27% | 24% |

Source: Q4 FY25 filings

Strategic moats & differentiators

FirstCry’s competitive advantage is built on a deeply integrated ecosystem that collaborates commerce, content, and community. This defense insulates it from both horizontal e-commerce giants and traditional retailers

- The Integrated Omnichannel Network : FirstCry’s masterstroke is its seamless fusion of digital and physical retail. The online platform, generating 78% of GMV, is reinforced by over 1,000 physical stores. These stores are more than sales points;they are trust-building hubs that drive brand visibility and customer acquisition. The proof is in the numbers: 38% of GMV in the top 20 cities comes from “cross-channel” customers who shop both online and offline, validating the symbiotic relationship between the two.

- The “Home Brands” Fortress: A cornerstone of FirstCry’s margin and differentiation strategy is its exclusive portfolio of proprietary brands, including BabyHug and Pinekids. Termed “Home Brands” to reflect a commitment to quality and brand equity, this portfolio has grown to contribute over 55% of the India business GMV, up from 37% in FY20. These brands, which are unavailable on competing platforms, grow 1.5 times faster than the overall India business, creating a powerful, high-margin draw for customers.

- A low-cost customer Acquisition Engine: FirstCry has engineered a uniquely effective customer acquisition flywheel. It begins with the Hospital Gift Box Program, a high ROI channel that distributes over 2.5 million gift boxes annually to new parents, capturing them at the “perfect point of market entry” and covering approximately 10% of all births in India. This is also complimented by the FirstCry Parenting App, India’s largest digital parenting community, which builds long-term relationships through content and support, embedding the brand into the parenting journey itself.

Growth drivers & expansion plans

FirstCry’s future growth is pinned on a clear strategy focused on deepening its domestic presence, replicating its model internationally, and relentlessly driving margin expansion.

Deepening the Domestic Footprint and Fueling Margin Expansion: The company plans to strategically expand its physical network by adding approximately 350 new company-owned stores over the next 2 to 2.5 years. This expansion is not growth for growth’s sake. Signaling a shift towards optimization, FirstCry recently closed 38 underperforming stores for the first time, using data on footfall and wallet share to refine its retail footprint and enhance efficient use of capital. It is also a primary objective to grow the adjusted EBITDA margin of the core business to 17-19% which will be achieved through a combination of operating leverage as the business scales, and crucially, by increasing the sales mix of its higher-margin SKUs in its Home Brands segment

Replicating the Indian Playbook internationally: The next major growth vector is the international market, particularly the Middle East. The strategy is to export the proven Indian playbook, starting with an offline foray into the Kingdom of Saudi Arabia with plans to establish approximately 12 stores over the next 24-30 months. Management is confident that the losses arising from expansion into this region have peaked, and the plan is to steer this business towards EBITDA neutrality within a few years.

Risks & industry headwinds

Despite its strong strategic positioning, Brainbees Solutions faces several material risks.

Macroeconomic Slowdown: The business is exposed to the risk of a sustained slowdown in consumer discretionary spending, which could impact sales of non-essential items like fashion and premium gear.

Competitive Pressure: The primary competitive threat lies in international markets, where new, well-capitalized players are engaging in aggressive promotional activity. Matching the same level of promotions could hamper profitability.

Operational Challenges: The business is exposed to supply chain disruptions and one-off incidents, such as warehouse fires and systematic stress on the working capital cycle.

Valuation & market view

Valuing a multi-faceted, high -growth company like Brainbees Solutions requires a nuanced approach. A simple look at consolidated metrics can be misleading, as the company trades at a high EV/EBITDA multiple of 38.6, while traditional P/E ratios are not meaningful given its consolidated losses.

When compared to a profitable, niche player like Purple United Sales Ltd., the valuations troy becomes clearer. Brainbees trades at a Price-to-Sales ratio of 2.4x, which is lower than Purple United's 3.17x. However, the difference lies in the EV/EBITDA multiple. Brianbees’ multiple of 38.6 is substantially higher than Purple United’s 17.7.

This premium valuation for Brainbees suggests that the market is pricing in significant future growth and margin expansion, driven by its dominant market leadership and the proven profitability of its core India business. In contrast, the market assigns a lower multiple to Purple United for its proven, high profitability (20.1% EBITDA margin) but on a smaller scale.

To better contextualize this valuation, it is also useful to compare it with foreign multi-channel retailers in the childcare segment, such as Carter’s from the US, Mothercare from the UK, and Chicco from Italy. While these companies differ in scale and geographic spread they share a common focus on selling products for mothers, babies, and children. Carter’s, a profitable and established player, typically trades at EV/EBitdA multiples in the lower to mid-20s, reflecting its mature market presence and stable cash flows. Mothercare, operating internationally but facing more modest growth prospects and profitability challenges, generally trades at a lower EV/EBITDA multiples in the 10-20x range. Meanwhile, Chicco, part of the Artsana Group, records steady profits with EBITDA margins often above 15% and trades at valuation multiples that reflect a stable, sustainable growth trajectory.

This deep dive provides a crucial lens: while FirstCRy’s overall valuation seems demanding, the market is likely factoring in the turnaround potential of significant assets like its subsidiary Globalbees and their pre-school business. A successful implementation of its India strategy to the international markets will also unlock value for the company.

Bottom line

Brainbees Solutions is more than just a retailer; it's a complex ecosystem with a mature, profitable core business nurturing high-growth, turnaround ventures. The company has reached a pivotal inflection point, with its main India business now generating positive profit and free cash flow. The investment case, however, rests not just on expanding margins in the core business, but on the successful execution of its strategic segments.

Brainbees Solutions Limited is gearing up for significant growth in India’s childcare market. Don’t miss out on opportunities ahead. Start your trading journey with CubePlus today and stay in control of your investments. Sign up now and invest smarter

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.