HDB Financial Services Ltd, a wholly-owned subsidiary of HDFC Bank, is a prominent non-banking financial company (NBFC) in India, established in 2007. Classified as an upper-layer NBFC (NBFC-UL) by the Reserve Bank of India (RBI), it has become a key player in the financial services sector, focusing on retail lending and underserved markets. As of March 31, 2025, HDB Financial Services boasts a rapidly growing customer base of 19.2 million, catering primarily to individuals and small businesses in semi-urban and rural areas. The company operates an extensive network of 1,771 branches across 1,170 towns and cities in 31 states and union territories, with over 80% of its branches located outside India’s top 20 cities.

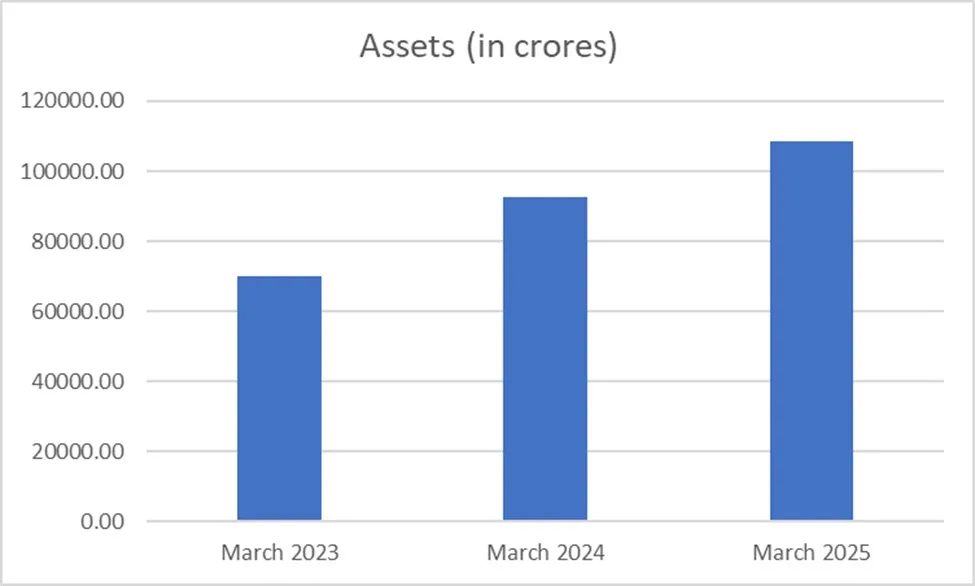

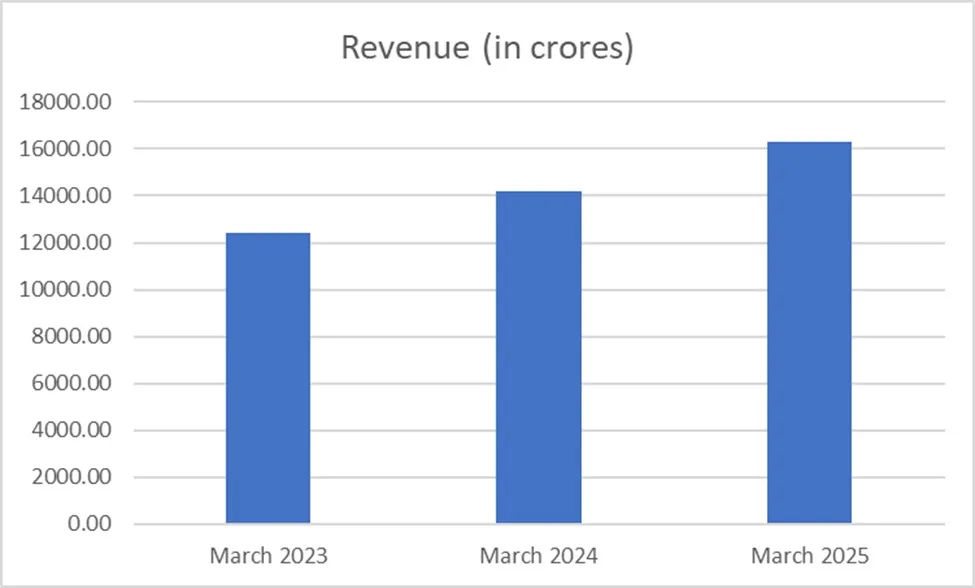

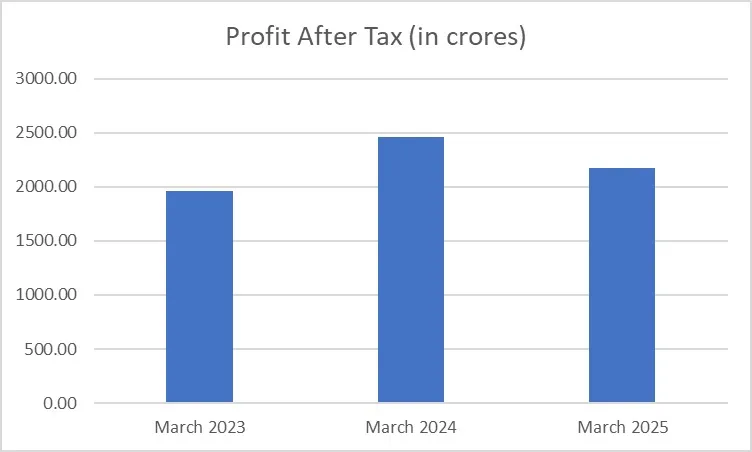

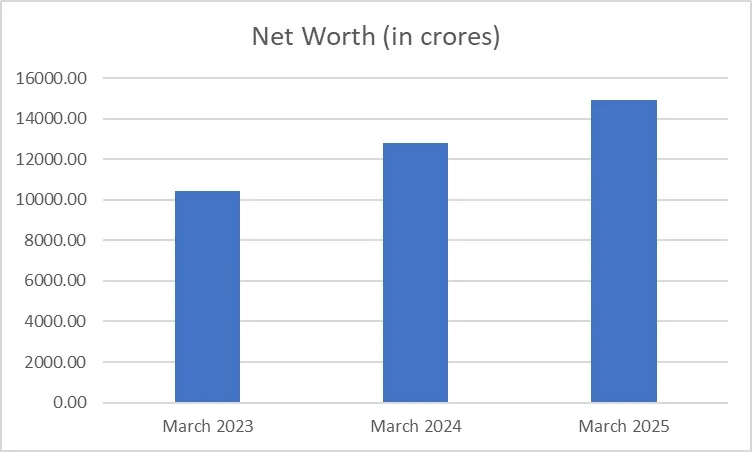

HDB Financial Services is India’s seventh-largest diversified retail-centric NBFC, with a total gross loan book of ₹1,068.8 billion as of March 31, 2025, reflecting a compound annual growth rate (CAGR) of 23.54% from fiscal 2023 to 2025. Its assets under management (AUM) stood at ₹1,072.6 billion, with a CAGR of 23.71% over the same period. The company reported a net profit of ₹21.8 billion in fiscal 2025, achieving a CAGR of 5.38%. These strong financial metrics highlight HDB Financial Services’ resilience through economic challenges, including the 2008 financial crisis, the 2018 NBFC liquidity crunch, and the COVID-19 pandemic.

The company’s diversified product portfolio is structured around three key segments: enterprise lending, asset finance, and consumer finance. Enterprise lending, accounting for 39.85% of the portfolio, offers secured and unsecured loans to micro, small, and medium enterprises (MSMEs) and salaried employees for working capital and business growth. Asset finance, comprising 37.36% of the portfolio, provides secured loans for income-generating assets like commercial vehicles, construction equipment, and tractors. Consumer finance focuses on secured and unsecured loans for personal and household needs, serving a broad range of retail customers, including self-employed individuals. Additionally, HDB Financial Services provides business process outsourcing services, such as back-office and sales support, and distributes insurance products, further diversifying its revenue streams.

HDB Financial Services IPO: Key Details

The HDB Financial Services IPO, launched in June 2025, is the largest NBFC IPO in India, aiming to raise ₹12,500 crore. The IPO comprises a fresh issue of 3.38 crore equity shares worth ₹2,500 crore and an offer for sale (OFS) of 13.51 crore shares valued at ₹10,000 crore by promoter HDFC Bank, which holds a 94.3% stake pre-IPO. The price band was set at ₹700 to ₹740 per share, with a lot size of 20 shares. Retail investors needed a minimum investment of ₹14,800 at the upper price band, while small high-net-worth individuals (sNII) required 14 lots (280 shares) worth ₹2,07,200, and big high-net-worth individuals (bNII) needed 68 lots (1,360 shares) totaling ₹10,06,400.

The IPO opened for subscription on June 25, 2025, and closed on June 27, 2025, with the allotment finalized on June 30, 2025. Shares were credited to demat accounts, and refunds were initiated on July 1, 2025. The IPO was listed on both the BSE and NSE on July 2, 2025, marking a significant event for HDB Financial Services and the Indian stock exchanges. The HDB Financial Services IPO attracted significant interest, reflecting strong investor appetite.

Financial Services IPO: Subscription and Investor Response

It was subscribed 16.69 times, receiving applications for over 217.67 crore equity shares against the 13.04 crore shares offered, as per NSE data. Qualified institutional buyers (QIBs) showed exceptional enthusiasm, subscribing 55.47 times their reserved portion, underscoring massive institutional interest from mutual funds and foreign investors. Non-institutional investors (NIIs) subscribed 9.99 times, while retail investors booked their portion 5.72 times. The employee reserved portion was subscribed 5.70 times, and the shareholder quota saw a subscription of 4.25 times.

The robust response from institutional investors highlights confidence in HDB Financial Services’ strong fundamentals, robust credit underwriting, and its association with HDFC Bank. The IPO raised ₹3,369 crore from anchor investors, reinforcing its appeal to high-quality institutional investors. The subscription figures position this IPO as the second most subscribed IPO among offerings exceeding ₹10,000 crore, surpassed only by the Tata Technologies IPO.

Financial Services IPO Listing: A Strong Debut

On July 2, 2025, HDB Financial Services shares debuted strongly on the Indian stock exchanges, listing at ₹835 per share on both the BSE and NSE, a 12.84% premium over the issue price of ₹740. This performance aligned with early indicators pointing to a healthy listing gain of 8–10%, as predicted by market analysts. The strong debut reflects investor confidence in the company’s growth potential and its position as a leading NBFC with a granular loan book and diversified operations.

Emkay initiated coverage with a “buy” rating and a target price of ₹900 per share, suggesting a 22% upside from the IPO price. The brokerage highlighted the company’s projected AUM growth at a 20% CAGR over the next three years, driven by its focus on retail lending and underserved markets. However, analysts noted a potential risk from a draft RBI circular in October 2024, which proposes that banks and their subsidiaries avoid business overlap, potentially affecting HDB Financial Services’ operations.

Allotment Status: How to Check

Investors could check their HDB Financial Services IPO allotment status through the BSE, NSE, or the registrar’s website, MUFG Intime India Private Limited (Link Intime). The allotment was finalized on June 30, 2025, and the process was user-friendly:

On BSE: Visit the BSE application status page, select “equity” as the issue type, choose “HDB Financial Services,” enter the application number or PAN, verify the captcha, and click “Search.”

On NSE: Access the NSE IPO application tracking page, select “HDB Financial Services IPO,” enter the application number and PAN, and click “Submit.”

On MUFG Intime Portal: Visit the registrar’s website, select “HDB Financial Services IPO,” choose a search method (PAN, Application Number, DP ID/Client ID, or Bank Account Number), enter the details, complete the captcha, and click “Search.”

Shares were credited to demat accounts on July 1, 2025, with refunds for unsuccessful bidders initiated the same day, ensuring a seamless post-allotment process.

Financial Services IPO Allotment: Valuation Insights

The IPO was attractively valued compared to peers, with a price-to-book (P/B) ratio of 3.2x to 3.4x at the upper price band, based on FY25 financials. This is lower than peers like Bajaj Finance (4.4x P/B) and Cholamandalam Investment (4.4x P/B) but higher than Shriram Finance (2x P/B). HDB Financial Services reported a return on assets (ROA) of 2.2% and a return on equity (ROE) of 14.7% for FY25, competitive though slightly lower than larger peers due to its focus on higher-risk underserved segments.

Brokerages such as SBI Securities, Sharekhan, and KR Choksey Securities recommended “subscribe,” citing the company’s strong parentage, robust credit underwriting, and access to low-cost funding due to its AAA-rated credit profile. The valuation, combined with India’s growing credit market (projected to reach ₹297 lakh crore by FY28 at a CAGR of 13–15%), positions HDB Financial Services as an appealing long-term investment.

_2_11zon.webp?alt=media&token=aecee85e-77a1-4763-9170-3ad6a856e290)

Diversified Product Portfolio: A Competitive Edge

HDB Financial Services’ diversified product portfolio is a cornerstone of its success, enabling it to serve diverse customer needs while maintaining a granular loan book with low concentration risk. The top 20 customers account for less than 0.36% of total loans, reflecting a de-risked lending profile. The company’s three key segments—enterprise lending, asset finance, and consumer finance—are supported by independent operations and dedicated management teams, ensuring scalability and efficiency.

Enterprise Lending: Launched in 2008, this segment provides secured and unsecured MSME loans for working capital and business expansion, targeting micro, small, and medium enterprises and salaried employees.

Asset Finance: This segment offers secured loans for commercial vehicles, construction equipment, and tractors, catering to customers in transportation and heavy machinery sectors, enhancing asset quality by reducing default risks.

Consumer Finance: Focusing on personal and household needs, this segment provides secured and unsecured loans, including personal loans and financing for two-wheelers and automobiles, serving a rapidly growing customer base in underbanked regions.

The company’s omni-channel “phygital” distribution model integrates 1,771 branches with digital platforms, including its mobile application and fintech partnerships. It also leverages an extensive external network of over 140,000 retailers and dealer touchpoints and partnerships with 80+ brands and original equipment manufacturers (OEMs). This hybrid approach enhances accessibility and supports HDB’s commitment to financial inclusion.

_1_11zon.webp?alt=media&token=7b3e23c4-3f34-4c41-9892-f97ec8f5eef2)

Financial Services IPO Allotment: Strategic Objectives

The net proceeds from the ₹2,500 crore fresh issue will bolster HDB Financial Services’ Tier-I capital base, enabling it to meet future requirements for onward lending across its business segments. The company plans to expand its presence in tier 2 and tier 3 cities, where credit demand is surging. The funds will also ensure compliance with the RBI’s capital adequacy norms, supporting long-term growth.

The ₹10,000 crore OFS by HDFC Bank will not contribute to the company’s capital but will reduce the promoter’s stake, enhancing the public float and stock liquidity. The IPO’s structure balances raising capital for growth with providing an exit opportunity for the promoter, aligning with market expectations for large NBFC offerings.

HDB Financial: Future Growth Prospects

HDB Financial Services is well-positioned to capitalize on India’s expanding credit demand, particularly in underserved segments. Its focus on retail lending, robust credit underwriting, and diversified product portfolio provides a strong foundation for growth. The “phygital” distribution model, combining physical branches with digital channels, enhances its reach and scalability. The company’s in-house underwriting team of 4,500 professionals and a collections workforce of over 12,000 further strengthen its operational capabilities.

India’s NBFC sector is projected to grow significantly, with systemic credit expected to reach ₹297 lakh crore by FY28. HDB Financial Services’ smaller size compared to peers like Bajaj Finance offers a long runway for growth, supported by favorable macroeconomic conditions and its strong parentage. However, challenges such as regulatory changes, including the RBI’s draft circular on business overlap, and potential volatility in net interest margins could impact future performance.

The company’s asset quality remains robust, with a gross non-performing asset (NPA) ratio of 2.1% and a net NPA ratio of 0.6% as of March 31, 2025. Its focus on secured loans (70% of the portfolio) and a granular loan book mitigates credit risk, while its AAA credit rating ensures access to cost-effective funding. HDB Financial Services’ strategic partnerships with HSBC Securities and other book-running lead managers further enhance its market credibility.

Comparison with Bajaj Housing Finance IPO

The HDB Financial Services IPO draws parallels with the Bajaj Housing Finance IPO, which was also a blockbuster offering in 2024. Both IPOs attracted strong institutional and retail interest, driven by their parentage (HDFC Bank and Bajaj Finance, respectively) and focus on retail lending. However, HDB Financial Services’ larger loan book and broader product portfolio, including business process outsourcing services, provide a competitive edge. While Bajaj Housing Finance focuses primarily on housing loans, HDB’s diversified offerings across enterprise lending, asset finance, and consumer finance cater to a wider market, positioning it for sustained growth.

Conclusion

The HDB Financial Services IPO marked a pivotal moment in India’s financial services landscape, offering investors a chance to invest in a leading NBFC with strong fundamentals and a diversified product portfolio. The IPO’s robust subscription, driven by qualified institutional buyers and non-institutional investors, and its 13% listing premium on July 2, 2025, underscore significant investor confidence. The company’s focus on enterprise lending, asset finance, and consumer finance, combined with its granular loan book and robust credit underwriting, makes it an attractive investment for those with a 3–5-year horizon.

With plans to strengthen its Tier-I capital base and expand in Tier 2 and Tier 3 cities, HDB Financial Services is well-positioned to meet future capital needs and capitalize on India’s growing credit market. Its association with HDFC Bank, extensive branch network, and “phygital” distribution model enhances its growth potential. Investors should monitor post-listing performance and broader market trends while leveraging the company’s strong fundamentals for long-term value creation.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)