For over three decades, investors enjoyed a strong bull market driven largely by falling interest rates and supportive central bank policies. But the tide is turning. Inflation, rising interest rates, and changing trade dynamics are indicating the beginning of a new investing era. Strategies that worked in the past may not be as effective going forward.

Three-decade bull run driven by easy money

Since the early 1990s, global equities have seen sustained gains, helped by ultra-low interest rates that made stocks more attractive than fixed-income assets. But those conditions are no longer in place. Rates are rising, liquidity is tightening, and valuations are being re-examined.

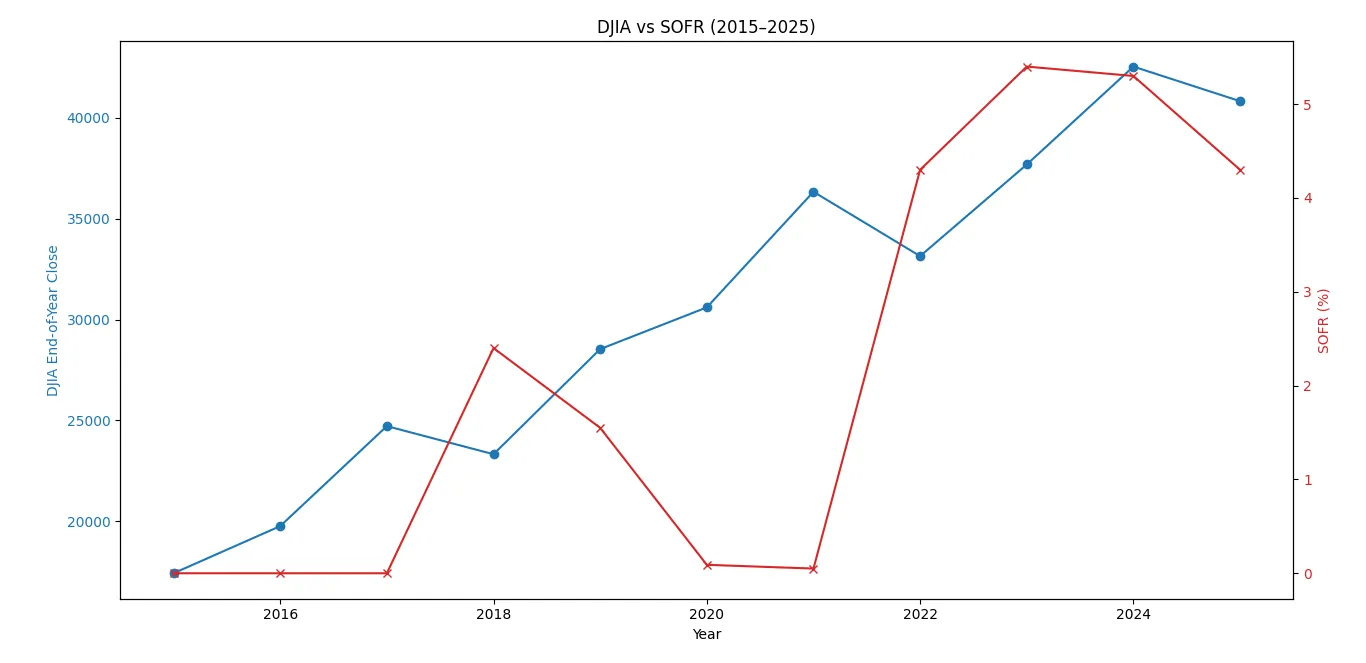

Market trends: DJIA vs SOFR (2015–2025)

Between 2015 and 2025, the Dow Jones Industrial Average (DJIA) rose steadily from around 17,425 to over 41,200 (as of May 2025). This happened despite major events like the COVID-19 pandemic and aggressive rate hikes. In contrast, the Secured Overnight Financing Rate (SOFR) near zero until 2022 spiked above 5% by 2023 as the US Federal Reserve fought inflation.

(Ultra-low rates are no longer the norm. Higher rates mean lower equity valuations and a shift in investor behaviour.)

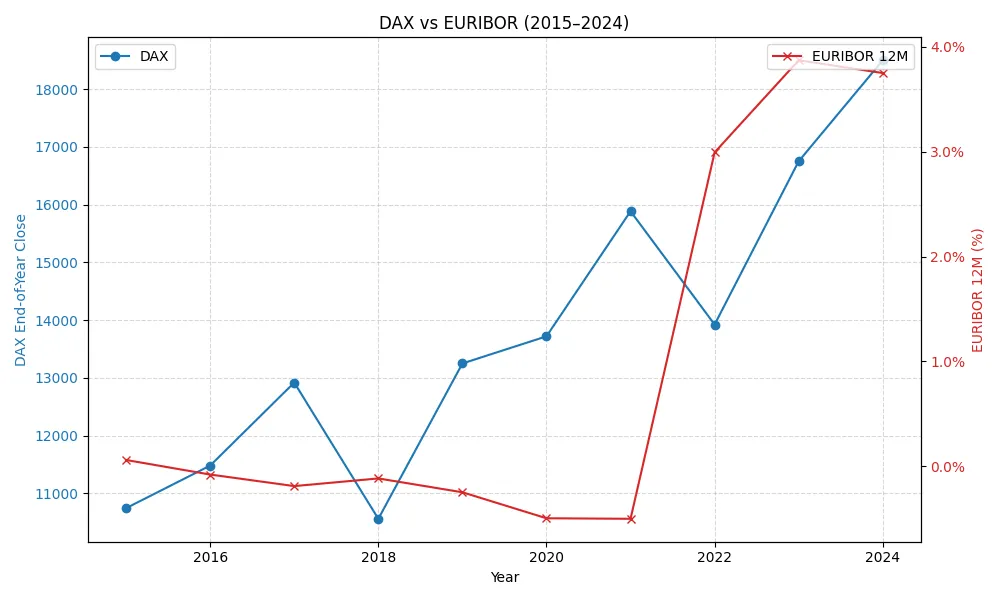

Europe followed a similar pattern. The DAX continued to climb over the decade, while the 12-month EURIBOR stayed negative until 2022, then jumped close to 3.75% by 2024.

Implications for India: Global capital flows are influenced by relative returns. Rising rates in the West can draw money away from emerging markets like India.

World in transition

After World War II, the U.S. helped set up a global economic system that shaped many of the market cycles we’ve seen since. In the 1970s, the world moved away from the gold standard, and the U.S. dollar became the dominant global currency. Each decade brought its own market trend, from the boom in U.S. stocks in the ’70s to the rise of emerging markets in the 2000s and the recent tech stock surge in the U.S.

After the pandemic in 2020, central banks pumped money into the system, which kept U.S. stocks rising. But now, the gains are mostly focused on a few very large companies. At the same time, the U.S. government’s growing debt and trade deficit are warning signs of possible instability ahead.

Global trade and tariff pressures

Adding to the uncertainty is the rise of protectionism. As of May 2025, Europe is imposing tariffs on Chinese EVs and solar components, while China is shifting its focus to Belt and Road markets. These moves could fragment global supply chains and change how companies invest and trade.

India stands to gain if global firms diversify their manufacturing base. But this opportunity will only materialize if we address local hurdles like infrastructure gaps, regulatory delays, and policy inconsistency.

At the same time, the UK–India Free Trade Agreement, reportedly in its final stages, offers a timely counterpoint. It could unlock high-value export opportunities for India in pharma, fintech, and textiles and mark a broader shift towards strategic bilateral trade ties.

Lessons from currency and market history

Currency policy has long shaped global economic dynamics. Take China: its yuan was pegged to the U.S. dollar in 1997, then shifted to a managed float in 2005. Allowing only a ±2% move from a reference rate kept exports competitive. This helped China grow its forex reserves from $615 billion in 2004 to nearly $3.9 trillion in 2014 and lifted per capita GDP by over 2,500% between 1994 and 2022.

However, this export-led growth also created structural imbalances and growing dependence on external demand. For India, the challenge lies not solely in currency fluctuations but in enhancing product quality and competitiveness to truly capitalize on global trade opportunities.

At the same time, market history offers another crucial lesson: growth is rarely linear. Retail investors often assume markets will keep rising steadily, but the Nikkei 225 tells a different story. After peaking in 1989, the index took more than three decades to regain those levels, finally crossing its all-time high in 2024, only to experience a sharp correction shortly after. For Indian retail investors, it’s a cautionary tale against assuming perpetual growth in indices like the Nifty or Sensex.

Lessons in non-linear market behaviour

India’s potential and the need for reform

The ‘China plus one’ strategy hasn’t yet translated into significant gains for India. Countries like Vietnam and Bangladesh have moved faster in attracting manufacturing investment. Why? India still grapples with slow bureaucracy, labour law complexity, and inconsistent implementation.

Despite these challenges, Indian entrepreneurs and corporates continue to build and grow. But to unlock real scale and global relevance, structural reforms, especially in logistics, education, and digital infrastructure, are essential.

Rethinking Risk and Valuation

The prolonged bull market may have inadvertently skewed perceptions of risk. As the tide potentially turns, a more fundamental approach to valuation becomes paramount. Returns are ultimately tethered to the underlying profitability of businesses. Paying exorbitant multiples for growth stocks, without a clear path to commensurate earnings, carries significant risk. Historical examples underscore that even market-leading companies require time to deliver substantial returns, and overpaying can severely diminish long-term outcomes.

Don’t chase yesterday’s playbook

Market narratives can often become detached from underlying fundamentals, leading to periods of irrational exuberance. Cultivating a disciplined and rational approach, grounded in principles of value investing, is essential to manage such environments. Remaining level-headed and recognizing the cyclical nature of markets can help investors avoid impulsive decisions driven by fear or greed. Identifying undervalued assets in unloved sectors, as demonstrated in previous market cycles, can yield significant long-term rewards.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)