Sector backdrop

The Indian capital goods sector outlook remains highly favorable, supported by a robust, multi-year capital expenditure cycle India that is gaining strong momentum. Key industrial sectors, including power, steel, cement, and chemicals, are exhibiting strong and sustained enquiry inflows, indicating a broad-based revival in investment sentiment. This positive momentum is supported by favorable macroeconomic indicators, such as a strong Manufacturing Purchasing Manager’s Index (PMI), which signals economic expansion and boosts investor confidence.

Beyond the cyclical upturn, a structural transformation is also underway. With increasing emphasis on sustainability and energy transition, government policies are prioritizing decarbonization, renewable energy, and environmental compliance. This shift is creating substantial opportunities in areas like waste-to-energy, green hydrogen, and emission control. Furthermore, the Atmanirbhar Bharat initiative continues to prioritize domestic manufacturing and technology development, particularly benefiting prospects for sustainable energy solutions India. Together, these drivers open a dual growth path: addressing traditional industrial capex needs while enabling advanced, future-ready sustainable solutions.

This favorable Indian capital goods sector outlook makes companies like Thermax compelling candidates for engineering sector India investment, particularly those positioned in sustainable energy solutions India.

Business snapshot and evolution

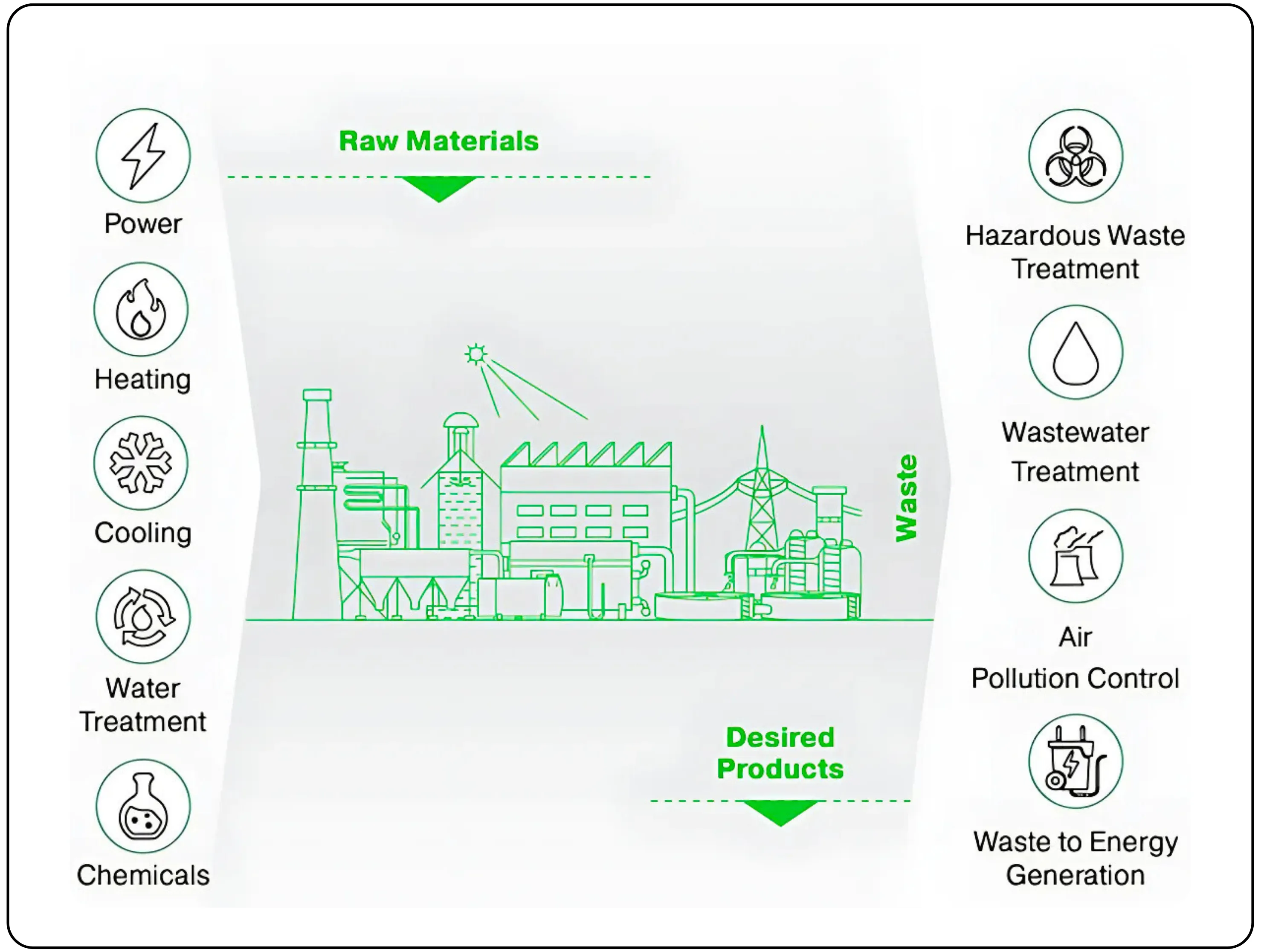

Founded as a global organization, Thermax Limited has established itself as a premier provider of sustainable solutions in the energy and environment sectors in India. With installations in over 90 countries and 16 manufacturing facilities, the company has a significant global footprint, though the domestic market remains its primary revenue contributor.

| Segment Name | Description and Focus | Image |

|---|---|---|

| Industrial Products | Serves as the stable foundation of the business, providing a wide range of standardized equipment, including heating, cooling, and water treatment solutions. |

|

| Industrial Infrastructure | Undertakes large, turnkey projects on an Engineering, Procurement, and Construction (EPC) basis, such as captive power plants, large boiler projects, and environmental solutions. |

|

| Green Solutions | Focuses on renewable and eco-friendly solutions, including biomass energy, solar and wind power generation, and Bio-CNG plants. |

|

| Chemicals | Manufactures and sells specialty chemicals like resins and water treatment chemicals, and is positioned as a key future growth driver. |

|

This breakdown of Thermax's business segments reveals a diversified portfolio where each division addresses different aspects of India’s industrial and energy transition needs.

Historically, the company has operated as a broad-based EPC and product player. However, it is now undergoing a significant strategic evolution. After facing severe profitability challenges in large, high-risk government projects, the company is deliberately pivoting its strategy. It is moving away from projects with extensive civil and construction scope to focus on equipment-centric, technologically complex projects where it has a clear execution advantage. This strategy involves a conscious de-risking of the Industrial Infra business while aggressively investing in the high-growth Chemicals and Green Solutions verticals.

Financial performance overview

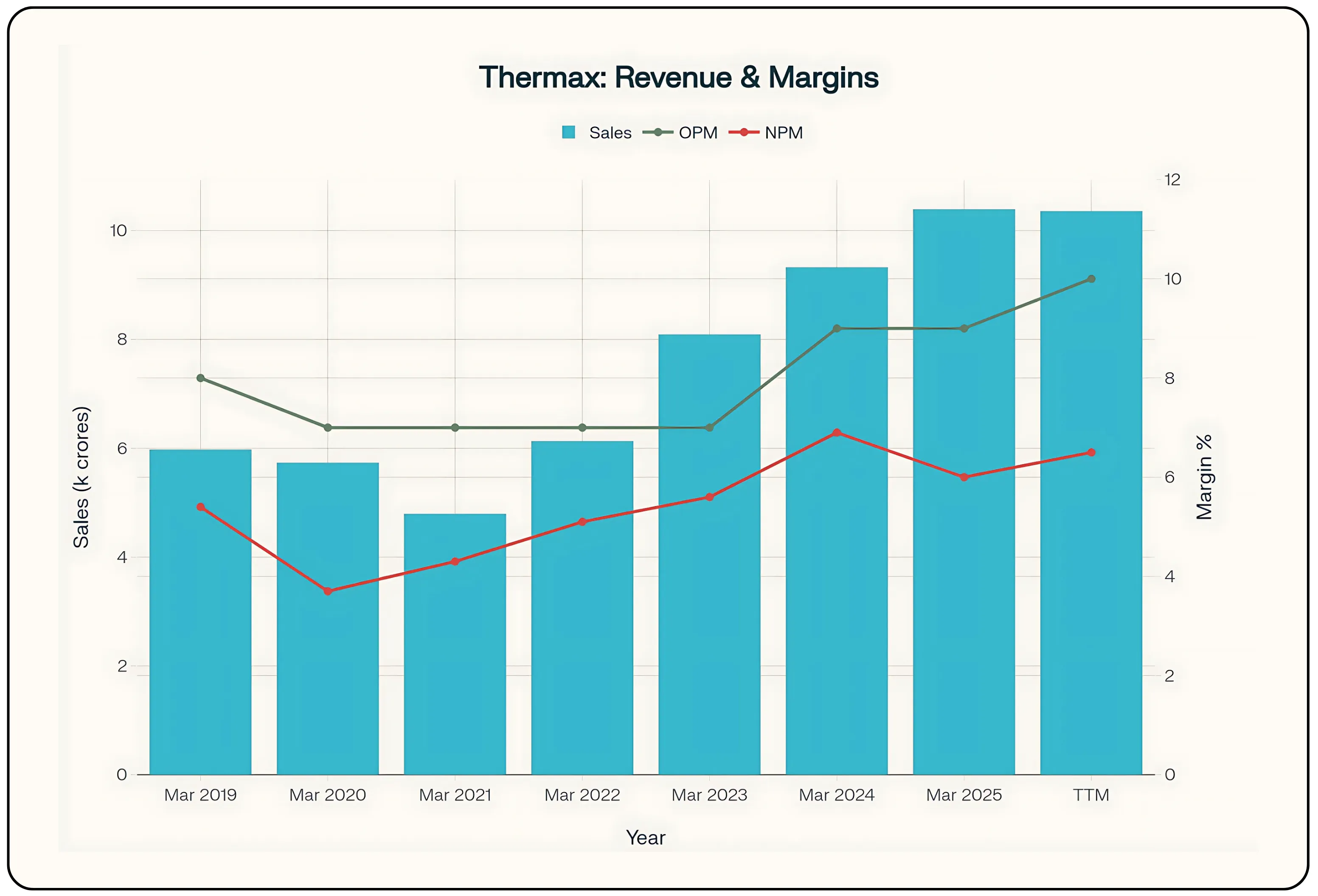

Thermax’s recent financial performance reflects a company in the midst of transformation, characterized by steady revenue growth in its core operations, overshadowed by significant profitability challenges in specific large projects. For the fiscal year ending March 2025 (FY25), the company reported a consolidated revenue of INR 10,389 crore, marking an 11% year-over-year increase. However, this top-line growth did not translate to the bottom line, with Profit After Tax (PAT) declining by 4% to INR 627 crore.

The divergence between revenue growth and profitability was primarily driven by severe cost overruns in the Industrial Infra segment. Specifically, the company incurred financial hits exceeding INR 100 crore throughout the year on technologically complex.

Bio-CNG project risks and legacy FGD contract pressures demonstrate the project execution risk capital goods sector commonly encounters. This impact was particularly stark in Q4 FY25, where a single INR66 crore hit of technology intervention costs on Bio-CNG projects suppressed profitability despite strong revenue delivery.

The first quarter of FY26 signaled a potential turnaround in profitability. While revenue saw a slight 2% decline year-over-year to INR 2,150 crore, PAT surged by 38% to INR 151 crore. This improvement was substantially driven by two key factors-

- A one-off government incentive of INR 56 crore.

- The absence of the major project-related losses that had plagued the same quarter in the previous year.

This quarterly improvement provides an encouraging picture for the investment case. However, sustained revenue and profit growth require the successful execution of the strategic pivot.

This performance underscores the management’s strategic focus on stabilizing the project's business to allow the underlying profitability of the core segments to shine through. Management has guided for a return to double-digit EBITDA margins in FY26, contingent on the non-repetition of the large one-off hits from FY25.

Industrial products

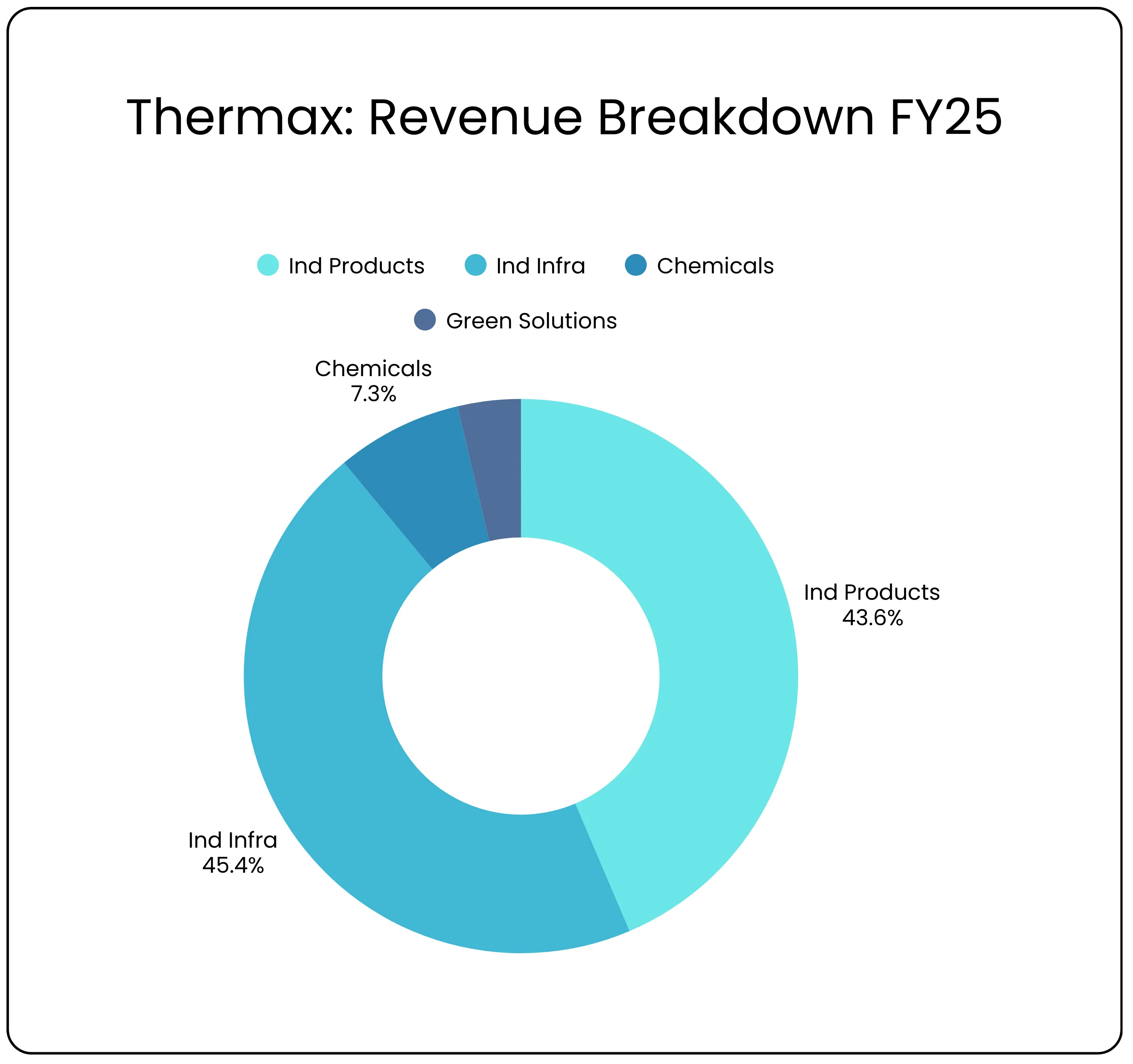

This segment is the company’s stable and profitable core, acting as its “bedrock” and contributing INR 4,529 crore to FY25 sales. It provides a diverse range of engineered equipment, with heating solutions being its most profitable sub-segment. This segment demonstrates classic operating leverage, with margins expanding significantly on higher volumes. The order backlog at the end of FY25 was nearly 20% higher than the previous year, providing strong visibility for FY26. While facing short-term headwinds from a slowdown in the ethanol and sugar sectors, its broad industry exposure and growing international pipeline position it for continued steady, profitable growth.

Industrial infrastructure

This segment, which generated INR 4,715 crore in FY25 sales, has been the primary source of the company’s recent financial volatility. It focuses on large EPC projects and has been severely impacted by losses on government FGD contracts and technologically challenging Bio-CNG projects. These legacy issues have led to a major strategic pivot. The Board has formally decided that Thermax will not bid for large supercritical thermal power projects in their current form, given the high risks associated with extensive civil and construction work. Instead, the company's focus is now on clearing the low-margin legacy backlog and selectively pursuing profitable, equipment-centric projects. The goal is to lift the segment’s profitability from a 1-2% level in FY25 to over 5% in FY26.

Green solutions

This segment is central to Thermax’s long-term vision of providing sustainable solutions. It includes a build-own-operate business for green utilities (TOESL) and a renewable energy generation arm (FEPL). The segment’s performance has been a mixed bag. The Bio-CNG business, housed here, incurred over INR 200 crores in losses over two years, which management has framed as a painful but necessary capability-building exercise. After a year-long pause, the company is selectively re-engaging in this space with more realistic, de-risked performance guarantees. Meanwhile, the renewable energy arm (FEPL) has also been loss-making, but these losses are expected to reduce significantly in FY26 as new projects become operational.

Chemicals

As Thermax’s fastest-growing segment, the chemicals business generated INR 763 crore in FY25 sales. Management is pursuing an aggressive growth strategy through both organic and inorganic routes. This includes commissioning new manufacturing plants in Jhagadia (India) and Indonesia, acquiring companies like Buildtech Products to enter the construction chemicals space, and forming partnerships with international players like Vebro and OCQ to introduce high-performance products. While these heavy investments are currently pressuring near-term margins, the long-term goal is to scale the business and return to a high-teens profitability profile.

Strategic moats

Thermax has cultivated several durable competitive advantages that differentiate it from its peers and support its long-term strategy.

| Theme | What It Means | Why It Matters |

|---|---|---|

| Technology & Innovation Leadership | Thermax is not just making boilers and equipment anymore - it is investing in future tech like Green Hydrogen (clean fuel of tomorrow) and Carbon Capture (removing CO₂ from emissions). It has tied up with IIT Delhi and Ceres to build new technologies. | This makes Thermax a technology pioneer in clean energy, not just a machinery supplier. It is preparing for the energy transition that big industries and governments are moving towards. |

| Integrated Solutions Model | Thermax can provide end-to-end solutions - from generating energy to cleaning emissions and treating water, even supplying specialty chemicals. Through its arm TOESL, it offers “green utilities as a service” (like green steam and water) where Thermax invests and operates the plant, and customers simply pay for usage - no upfront cost for the client. | This gives Thermax a unique edge: customers can decarbonize easily without spending large amounts upfront. It creates recurring revenues for Thermax and long-term partnerships. |

| Evolving Risk Management | Earlier, Thermax sometimes took up very large, risky government projects (EPC with heavy construction work), which often led to problems. Now, it avoids such contracts and focuses only on profitable, less risky projects (called “good calories”). | This makes Thermax’s business more stable and predictable, avoiding cash flow stress and margin losses. It improves the profitability and sustainability of its order book. |

The Atmanirbhar Bharat initiative creates a supportive policy framework for Thermax’s domestic-focused strategy. As India prioritizes energy security and environmental compliance, companies offering sustainable energy solutions gain strategic advantages.

Growth drivers and expansion plans

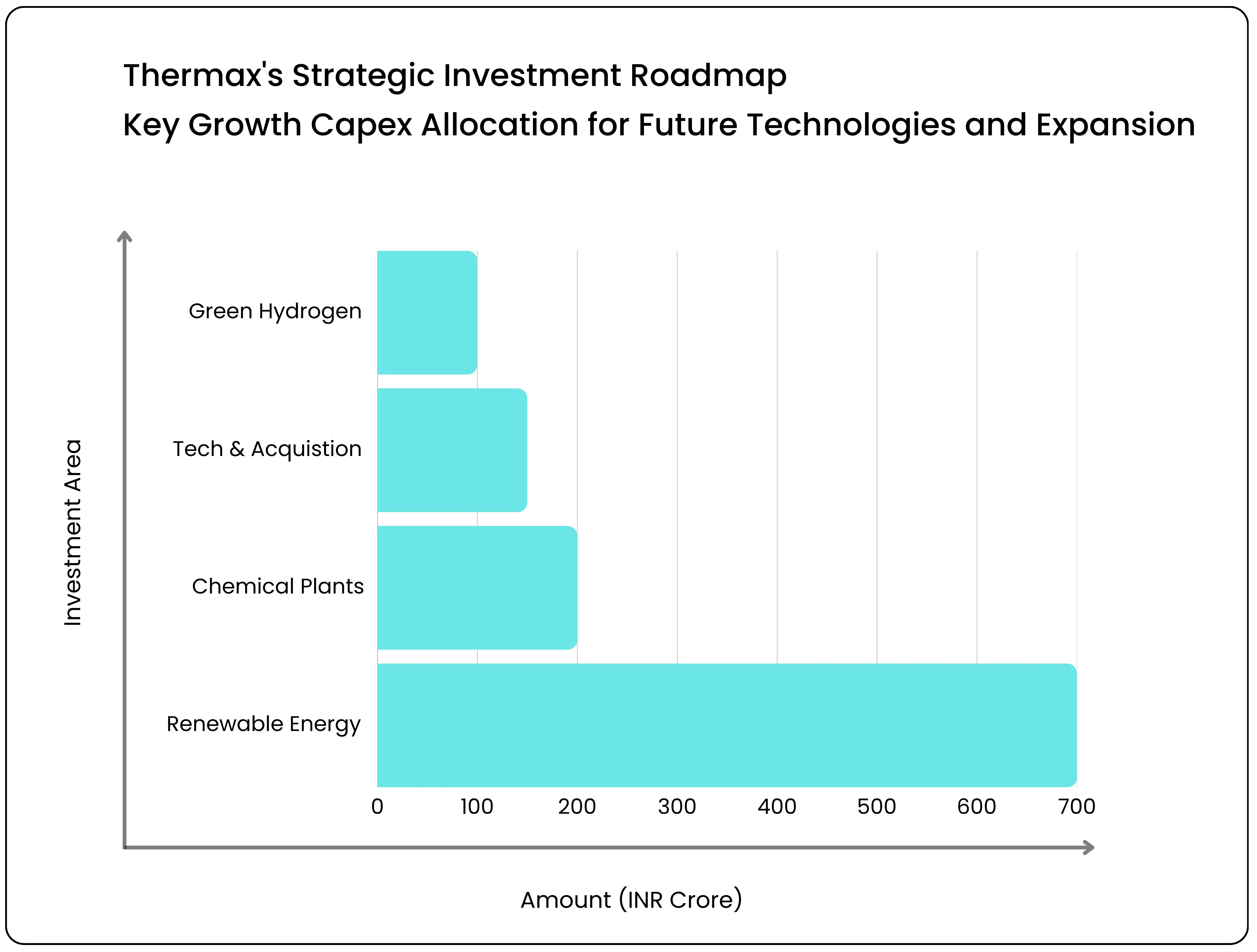

Thermax is in a heavy investment phase, allocating significant capital to build capabilities for future growth.

| Drivers | What It Means | Why It Matters |

|---|---|---|

| Strategic Capex in Future Technologies | Thermax is putting serious money into future tech. It will spend about ₹100 crore in the next 18 months to develop its Green Hydrogen (SOEC) product. Through its arm FEPL, it also plans to set up 1 gigawatt of renewable energy capacity, supported by ₹700 crore equity investment. | These moves make Thermax part of India’s clean energy and Atmanirbhar Bharat story. It shows Thermax is not only chasing today’s business but also investing early in future energy markets. |

| Expansion into Chemicals | Thermax is expanding its chemicals business with new factories in Jhagadia (Gujarat) and Cilegaon (Indonesia). It is also entering new product areas like construction chemicals and high-performance resins via acquisitions and partnerships. | Chemicals offer high margins and recurring demand. This diversification reduces dependence on project business and adds a stable earnings stream. |

| Robust Order Pipeline & International Push | Thermax’s order book is the strongest in 3+ years, with big demand from power, steel, and refining sectors. It also wants to grow faster abroad, focusing on the Middle East, Southeast Asia, and Africa. | A strong pipeline means revenue visibility for the next few years. The international push helps Thermax reduce dependence on the Indian market and tap into fast-growing global demand. |

Risks and industry headwinds

Despite a positive outlook, Thermax faces several material risks inherent to its business model and industry.

Project execution risk: This remains the most significant headwind. The financial drain from legacy projects, particularly the FGD and Bio-CNG contracts, has been substantial. While the company is actively de-risking this segment, any further delays or unforeseen costs in completing these projects could continue to impact profitability.

Lumpy order inflows and sectoral slowdowns: The company’s performance is tied to the industrial capex cycle, which can be lumpy. The lack of large project orders for several quarters in FY25 put pressure on fixed cost absorption. Furthermore, the business is vulnerable to slowdowns in specific sectors, as seen with the ethanol and sugar industries. This has been a recurring headwind for the core industrial Products segments.

Regulatory and policy dependence: the commercial viability of key growth areas like Bio-CNG is highly dependent on a supportive government policy framework, which management notes is still evolving. Additionally, the structure of government tenders for the massive thermal power opportunity remains a risk: if projects are not broken into more manageable packages, Thermax’s self-imposed exclusion could limit a major growth avenue.

Valuation and market view

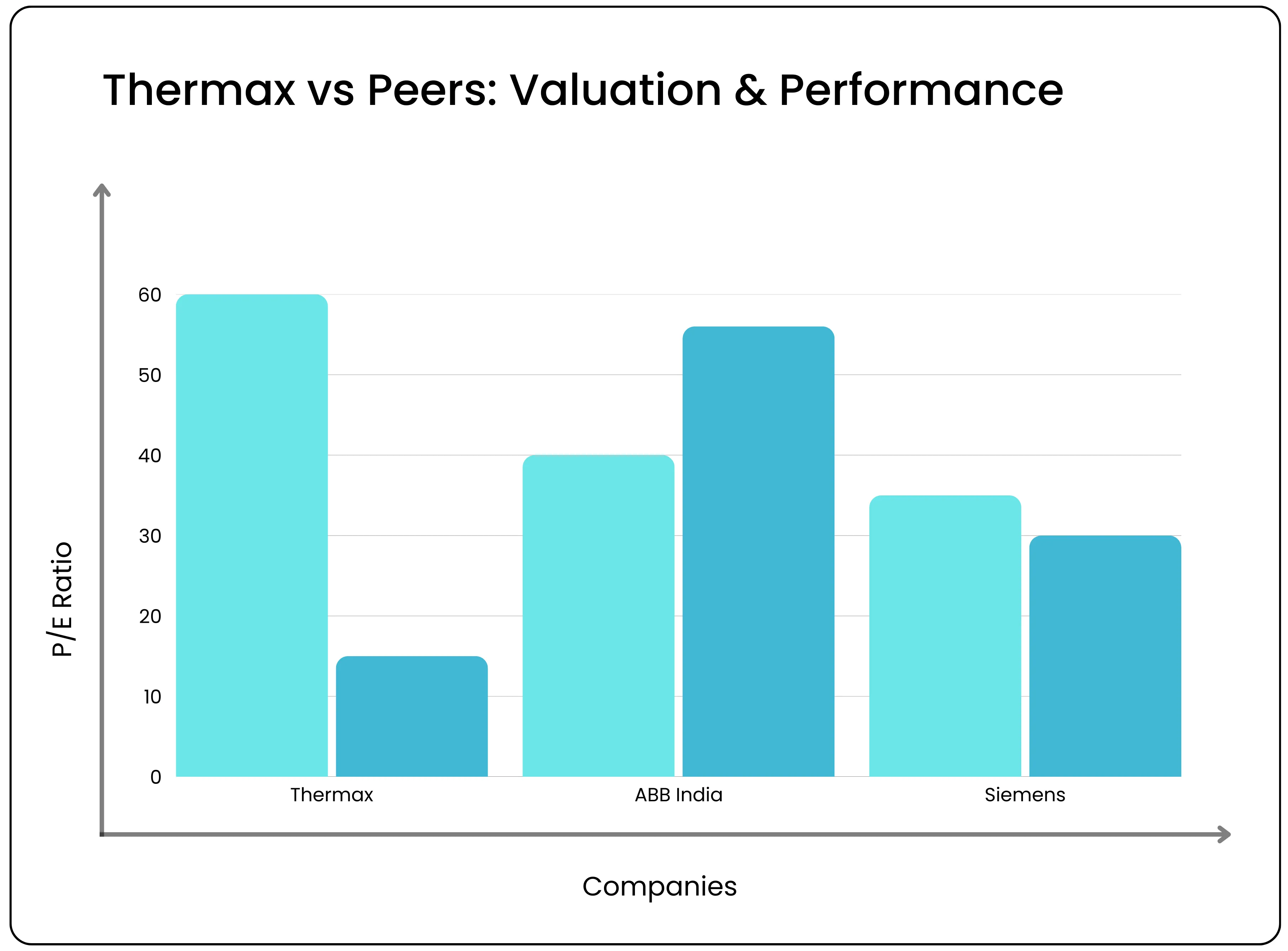

Thermax trades at a Price-to-Earnings (P/E) multiple of approximately 59.3x and an Enterprise Value to EBITDA (EV/EBITDA) of 41.5x. The valuation gap reflects the market’s nuanced view of a company in the midst of a significant median, the discount relative to top-tier players. The valuation gap reflects the market’s nuanced view of a company undergoing a strategic transition. While Thermax’s P/E and EV/EBITDA multiples are slightly above the industry median, the discount relative to top-tier players can be attributed to the recent drag on profitability and return ratios caused by challenges in the industrial Infra segment. Thermax’s Return on Capital Employed (ROCE) of 16.2% is considerably lower than that of ABB (38.7%) and Siemens (23.6%), which reflects the market’s caution surrounding the company.

The market is currently weighing the consistent, high-margin performance of its “bedrock” Industrial products business against the well-documented execution risks and historical losses in large-scale projects. The current valuation suggests a “wait-and-see” approach, with investors looking for sustained evidence that the company’s strategic pivot toward lower-risk, higher-margin projects is successful and that overall return ratios are improving. The potential for a re-rating is significant; if management successfully executes its turnaround of the project business and the high-growth Chemicals and Green Solutions ventures contribute meaningfully to the bottom line, there is a strong case for the valuation gap with its premier peers to narrow substantially.

Bottom line

Thermax represents a compelling strategic pivot and turnaround story. The company stands at an inflection point, transitioning from a period of severe execution challenges in its projects business to a more disciplined, risk-averse operation poised for profitable growth. The core investment thesis rests on management’s successful execution of this shift, which involves leveraging its stable, cash-generative Industrial Products business to fund long-term, high-potential investments in sustainability and chemicals.

While the overhang from legacy projects remains a key risk, the formal decision to avoid high-risk EPC contracts is a crucial and positive change. For investors, this is a play on a high-quality engineering company that is actively cleaning its portfolio to unlock its true earnings potential. The path forward requires flawless execution, but the combination of a robust domestic capex cycle, a de-risked business model, and leadership in future-facing sustainable technologies creates a favorable long-term risk-reward profile.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.