Mergers and acquisitions (M&A) often make headlines for their size and ambition. Companies announce them as bold strategic moves to gain market share, enter new sectors, or unlock synergies. But once the excitement fades, the real picture emerges.

Globally, studies show that nearly 70 to 90% of acquisitions fail to create long-term value. Several high-profile deals have struggled due to over-optimistic assumptions, cultural mismatches, or difficulties in integrating operations.

So, why do companies keep repeating the same mistakes? One major reason lies in the yardstick used to evaluate M&A deals, earnings per share (EPS).

The Problem with EPS Accretion

EPS accretion or dilution is the most widely quoted metric after an acquisition is announced. If the deal is said to be ‘EPS-accretive,’ it means the combined entity’s post-merger earnings per share are expected to rise. On paper, this appears positive; however, in reality, it can be misleading.

EPS is an accounting number, not an economic measure of value. A company with a high price-to-earnings (P/E) ratio can acquire another target company with a lower P/E, and even if the total net income doesn’t improve much, the merged entity may still show higher EPS.

This happens because EPS ignores the cost of capital, risk, and reinvestment needs. A deal can improve EPS in the short term yet destroy shareholder value if it fails to earn returns above the acquirer’s weighted average cost of capital (WACC).

Curious about financial ratios? Learn what they really reveal about a company: Understanding Stock Valuation Through Key Financial Ratios

In short, a rising EPS doesn’t always mean rising value. It often reflects deal structure and accounting adjustments, not real economic gains. Generally speaking, investors need to focus on financial synergies and cash flows rather than just accounting numbers.

A Better Way to Judge M&A Deals

To understand whether a merger truly creates value, you can look at cash flow-based measures rather than earnings-based ones.

Authors Michael Mauboussin and Alfred Rappaport, in their book Expectations Investing, suggest a simple but powerful formula for assessing acquisitions:

Value created = Present value of synergies − Acquisition premium

Here’s how it works:

- Acquisition premium is what the acquirer pays above the target’s fair value (usually estimated through a DCF or market price).

- Synergies are the extra cash flows expected from combining the two businesses through operations improvements, cost savings, higher revenues, or better use of assets.

If the discounted value of these synergies exceeds the purchase premium paid, the deal adds value. If not, shareholders lose.

This formula reframes the premium as a bet on future performance. The higher the premium, the greater the expectations, and the greater the risk if those synergies don’t show up.

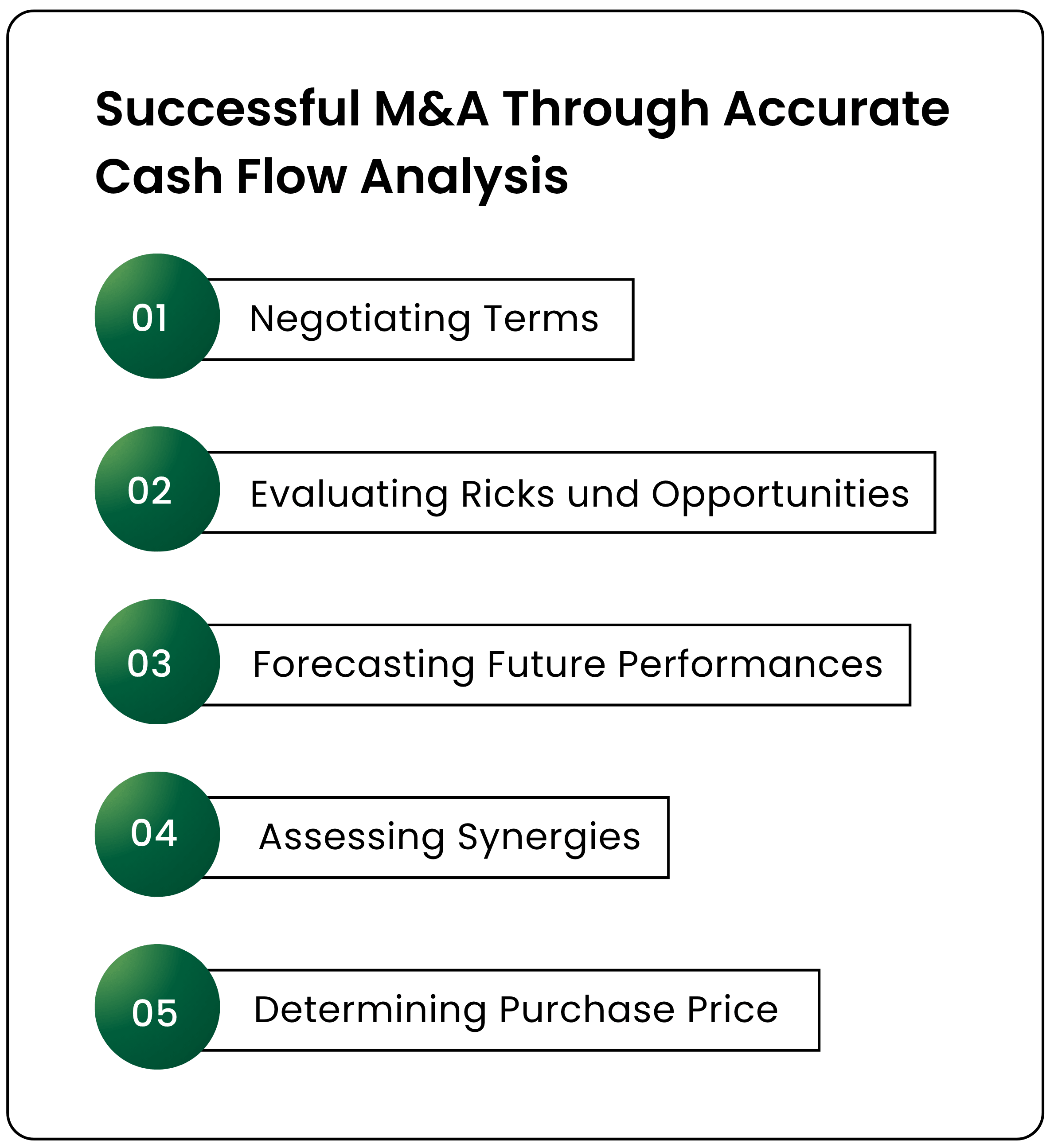

The Four-Step Framework to Evaluate M&As

Using the principles of Expectations Investing, investors can approach M&A analysis in four logical steps.

1. Decode the market’s expectations

Start with the target company’s share price before the proposed merger. A discounted cash flow (DCF) model can reveal what level of growth, margins, and reinvestment the market has already priced in.

Do the same for the acquiring company. This helps identify whether the market is already expecting high growth or if there’s room for value creation.

This helps identify whether the company's ability to generate returns is sufficient or if there’s room for long-term value creation.

2. Quantify the synergies

Not all synergies are equal. They can come from four broad areas:

- Operational efficiency: Streamlining operations or procurement.

- Growth acceleration: Cross-selling, distribution expansion, or higher revenues from new markets.

- Cost savings: Removing duplication or consolidating operations.

- Financial benefits: Better debt management or tax advantages.

Each synergy should be converted into incremental free cash flow and discounted at the acquirer’s WACC. Vague promises like “we will cross-sell more” should be treated with caution unless backed by numbers and proper analysis.

3. Assess the risks

Even when projected synergies look strong, execution risk can erode value. Integration challenges, cultural gaps, or regulatory scrutiny (for instance, by the Competition Commission of India) often reduce the expected benefits. Stress-testing different scenarios helps check how sensitive the deal’s success is to these assumptions.

4. Re-evaluate after announcement

Once a deal is announced, the market quickly revises its expectations. Analysts and investors should reassess the price-implied expectations (PIE) for the combined entity.

If the stock rallies sharply, it might indicate that the market is assuming perfect execution, leaving little margin for error. If sentiment remains cautious, upside potential may exist if management delivers better-than-expected results.

Extra Tools: SVAR and Premium at Risk

Two supplementary measures can help investors gauge how much is at stake:

Shareholder Value at Risk (SVAR): The portion of the acquirer’s market value effectively bet on the deal.

Example: If a ₹40,000 crore company pays a ₹10,000 crore premium, 25% of its value is at risk.Premium at Risk: The proportion of the premium that depends on achieving the projected synergies, especially relevant in stock-swap mergers.

Both metrics help investors understand how much pressure the deal puts on the company’s future performance.

What It Means for Indian Investors

India’s M&A activity is accelerating across financial services, technology, infrastructure, and consumer sectors. Announcements often highlight higher EPS and strategic fit, but these are not reliable indicators of success.

The real questions investors should ask are:

- Are the financial synergies large and credible enough to justify the purchase premium?

- How much of the company’s value is being risked?

- What could go wrong, and how has the market priced that risk?

Ultimately, cash flows, cost of capital, long-term growth, and realistic expectations determine whether a merger and acquisition truly creates value.

For investors, that means looking beyond the headline EPS numbers and focusing on the underlying economics. The market may cheer a deal on day one, but only disciplined capital allocation and real cash flow gains will sustain value in the long run.

Want to know about a company? Check its financials step by step on CubePlus

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.