The Securities and Exchange Board of India (SEBI), the market regulator, has proposed a major overhaul of the mutual fund fee structure, aiming to improve transparency, reduce costs, and simplify rules for the mutual fund industry. This initiative is part of SEBI’s continuous effort to bring regulatory clarity and ensure investor protection. The reform primarily targets a more transparent and efficient total expense ratio (TER) framework, directly benefiting mutual fund investors and ensuring fair cost allocation across mutual fund schemes.

Reduction in Total Expense Ratio (TER)

A central feature of SEBI’s proposal is the reduction in the base Total Expense Ratio (TER) for open-ended equity and non-equity mutual fund schemes by approximately 15 to 20 basis points. This reduction allows investors to retain a larger portion of their returns, as TER is deducted from the Net Asset Value (NAV) of a mutual fund scheme.

To balance the change, SEBI has proposed a 5 basis points increase in the first two expense ratio slabs for open-ended active schemes managed by asset management companies (AMCs). Additionally, SEBI plans to remove the earlier permitted 5 bps additional expense that fund houses could levy across schemes.

These changes are part of SEBI’s broader mutual fund rules under the SEBI Mutual Funds Regulations, 1996, ensuring regulatory fees and statutory levies are handled transparently. The proposal aims to make mutual fund investments more efficient while reducing hidden costs within the expense ratio limits.

Exclusion of Statutory Levies from TER

One of the most impactful changes SEBI has proposed is the exclusion of statutory levies from TER. Taxes such as the Securities Transaction Tax (STT), Goods and Services Tax (GST) excluding GST on management fees, Commodity Transaction Tax (CTT), and stamp duty will now be billed separately to investors.

This means statutory levies, statutory charges, and regulatory fees will no longer inflate TER values. This reform enhances transparency, ensures greater clarity, and prevents investors from unknowingly paying for changes in government levies.

By excluding statutory levies, SEBI simplifies compliance for asset management companies, making it easier to identify all the expenditures charged to mutual fund investors. It also eliminates bundled service arrangements, keeping mutual fund fee structure clean and fair.

Tightening of Brokerage and Transaction Costs

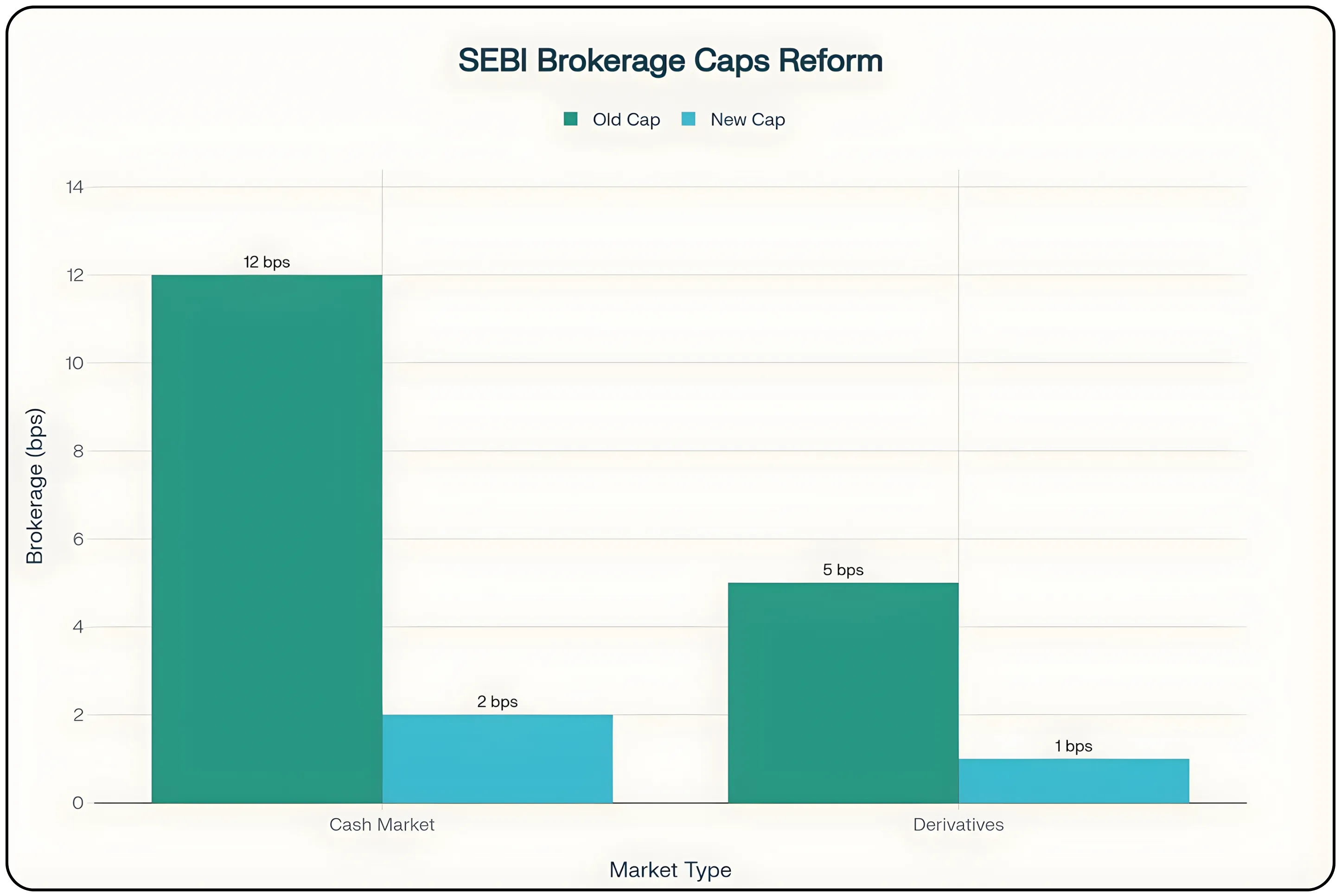

Another major proposal from SEBI targets brokerage and transaction costs. Brokerage charges for cash market transactions will now be capped at 2 basis points (bps), down from 12 bps, while derivatives transactions will see a reduction from 5 bps to 1 bps.

This sharp cut helps avoid double charging of investors and ensures brokerage and transaction charges are fully disclosed rather than embedded in the total expense ratio. The move will result in lower brokerage costs and more efficient cost structures for investors in mutual fund units and arbitrage funds.

While this may reduce income from brokerage paid for fund houses and brokers, it ultimately benefits mutual fund investors by improving greater transparency and reducing transaction costs incurred across all mutual fund schemes. The brokerage limits revision also aligns with SEBI’s intent to simplify rules and make expense ratio calculations more investor-friendly.

Performance Linked TER (Optional Framework)

SEBI has also proposed an optional performance-linked TER model for open-ended active schemes. Under this system, asset management companies (AMCs) may charge a variable fee based on how well the scheme performs relative to its benchmark.

If the mutual fund scheme outperforms its benchmark, AMCs may charge slightly higher fees; if it underperforms, the expense ratio must decrease. This model directly ties advisory fees and management fees to fund performance, ensuring fund houses charge investors fairly and creating strong alignment between fund managers and investors.

This framework promotes accountability, encourages active value creation, and links investor communication with measurable results strengthening trust within the mutual fund industry.

Enhanced Disclosures and Simplified Compliance

The proposed draft regulations also focus on enhanced disclosure and reduced compliance burden. SEBI has mandated that all expenditures including brokerage and transaction costs, transaction fees, audit fees, custodian fees, and regulatory expenses must be distinctly disclosed, separate from the TER.

Furthermore, SEBI plans to streamline redundant compliance obligations such as reducing the number of mandatory trustee meetings and encouraging electronic disclosures in place of print advertisements. This not only cuts down expenditures pertaining to administration but also supports SEBI’s digital transformation agenda.

These steps will simplify rules, bring regulatory clarity, and enhance transparency for investors while ensuring fund houses and AMCs maintain accountability in cost reporting.

Implications for Investors and the Mutual Fund Industry

For mutual fund investors, these new TER rules represent lower investor costs, greater transparency, and a clearer understanding of what they are paying for. By removing statutory levies and reducing brokerage and transaction costs, SEBI ensures that the mutual fund fee structure is directly linked to fund performance rather than hidden operational charges.

While fund houses and asset management companies (AMCs) may face tighter expense ratio margins, these changes are expected to enhance investor protection and foster long-term trust in the mutual fund industry. The inclusion of a performance-linked TER also encourages mutual fund schemes to prioritize consistent returns over high fees.

Also read: Understanding the Cost Structure of Mutual Funds

Conclusion

SEBI’s major proposal under its draft mutual fund regulations is a bold step to modernize mutual fund rules, simplify compliance, and promote greater transparency. The exchange board of India aims to make mutual funds a more efficient and trustworthy component of the personal finance landscape, reinforcing its commitment to investor communication, cost efficiency, and regulatory fairness.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.