When you file your income tax return and claim a refund, you’re essentially lending money to the government interest-free until they process your claim. However, if the Income Tax Department delays your refund beyond statutory timelines, they must compensate you with interest. Understanding the ITR refund interest rate and how it works can help you maximize your refund benefits and ensure you receive fair compensation for any processing delays.

The income tax refund interest system operates under Section 244A of the Income Tax Act, providing taxpayers with automatic compensation when refunds are delayed. This interest serves as the time value of money and encourages the tax authorities to process refunds efficiently.

In this comprehensive guide, we’ll explore the current ITR refund interest rate for 2024-25, eligibility criteria, calculation methods, and practical tips to optimize your refund processing experience.

Current ITR Refund Interest on Income tax 2024-25

The Income Tax Department pays interest at 6% per annum (equivalent to 0.5% per month) on income tax refunds under Section 244A of the Income Tax Act. This rate has remained consistent and applies from April 1, 2024, for Assessment Year 2024-25.

Here are the key features of the current ITR refund interest rate:

Interest Rate: 6% per annum or 0.5% per month

Calculation Method: Simple interest, not compound interest

Minimum Threshold: Interest paid only if refund exceeds 10% of total tax liability

Absolute Minimum: Refund must be at least Rs. 100 to qualify for interest payment

The government pays interest on delayed refunds to compensate taxpayers for the delayed use of their excess tax payments. This ensures fairness in the tax system and provides incentive for timely refund processing by the tax department.

The applicable interest rate remains uniform across all categories of taxpayers, whether individuals, Hindu Undivided Families (HUFs), companies, or other entities. The rate is designed to balance taxpayer compensation with fiscal considerations for the exchequer.

Eligibility Criteria for income tax return Refund Interest

Not all income tax refunds qualify for interest payments. The Income Tax Department has established specific eligibility criteria to determine when interest on refunds becomes payable:

Primary Eligibility Requirements

Refund Amount Threshold: The refund amount must be at least 10% of your total tax paid during the financial year. For example, if your total tax liability was Rs. 50,000, your refund must exceed Rs. 5,000 to qualify for interest.

Minimum Refund Value: The absolute minimum refund threshold is Rs. 100. Any refund below this amount doesn’t qualify for interest payment, regardless of the percentage of total tax liability.

Source of Excess Tax: Interest applies only to excess tax paid through legitimate channels such as:

- Tax deducted at source (TDS)

- Advance tax payments

- Self-assessment tax

- Tax collected at source (TCS)

Filing and Documentation Requirements

Timely Filing: Your income tax return must be filed within prescribed due dates or extended deadlines announced by the Central Board of Direct Taxes (CBDT). Late filing affects the interest calculation period but doesn’t disqualify you from receiving interest.

Complete Documentation: Interest is not applicable if delays are caused by taxpayer errors, incomplete documentation, or failure to respond to Income Tax Department queries promptly.

Bank Account Validation: You must have a pre-validated bank account in the income tax portal to receive refunds and associated interest payments.

Many taxpayers overlook these eligibility criteria and wonder why their small refunds don’t include interest payments. Understanding these thresholds helps set proper expectations and ensures you focus on cases where interest is genuinely due.

How ITR Refund Interest is Calculated

The calculation of ITR refund interest follows a straightforward methodology based on simple interest principles. The Income Tax Department uses a standardized approach to ensure consistency across all refund cases.

Basic Calculation Formula

The interest calculation uses this simple formula: Interest Amount = Refund Amount × 0.5% × Number of months delayed

Let’s examine a practical example:

- Refund amount: Rs. 50,000

- Processing delay: 8 months

- Interest calculation: Rs. 50,000 × 0.5% × 8 = Rs. 2,000

The total amount credited to your bank account would be Rs. 52,000 (Rs. 50,000 refund + Rs. 2,000 interest).

Monthly Calculation Rules

The Income Tax Department follows specific rules for monthly calculations:

- Any fraction of a month counts as a full month

- Interest accrues for each month or part thereof until refund credit

- Calculation continues until the refund reaches your taxpayer’s bank account

- Processing delays by the tax department are covered under interest payment

For instance, if your refund is delayed by 3 months and 15 days, the interest calculation treats this as 4 full months.

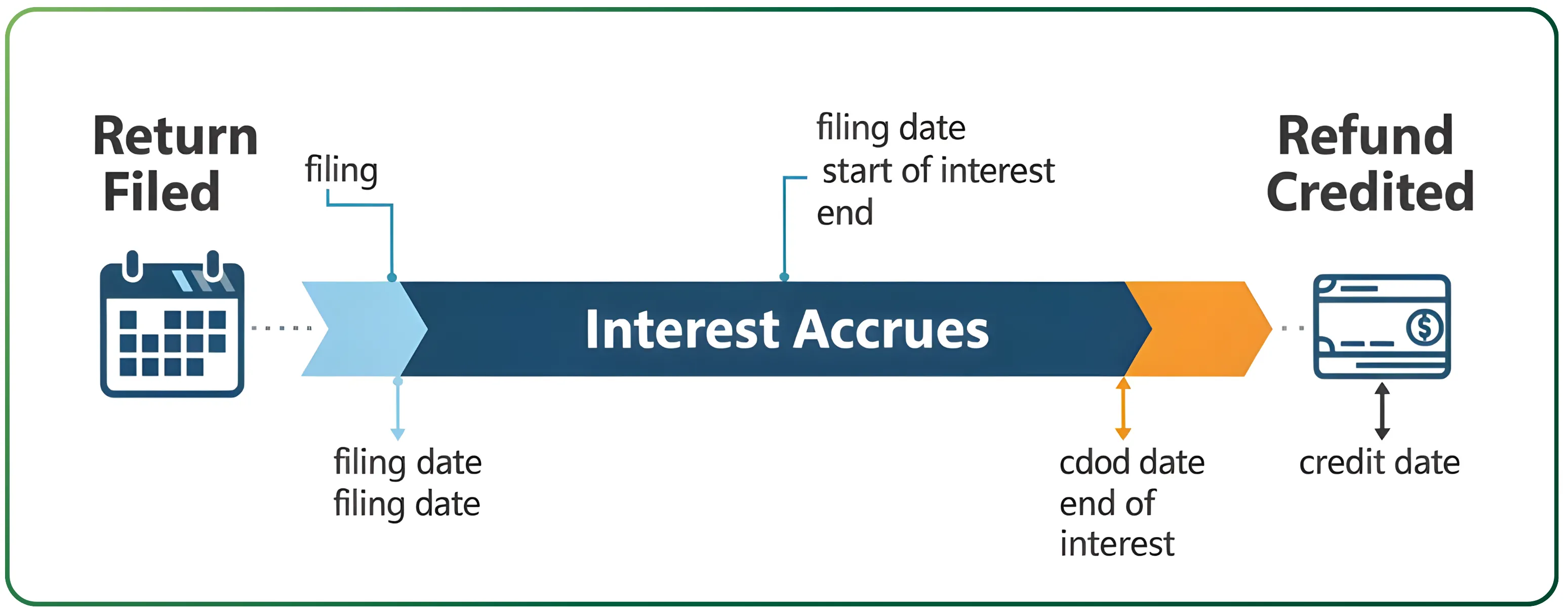

Interest Calculation Period

The interest period determination depends on your filing timeline:

For ITR Filed by Due Date: Interest calculation begins from April 1st of the assessment year and continues until the refund date. For Assessment Year 2024-25, if you file by September 15, 2024, interest starts accruing from April 1, 2024.

For Late-Filed Returns: Interest calculation begins from your actual filing date rather than April 1st, potentially reducing your total interest compensation.

The interest continues accumulating until the refund with interest is credited to your pre-validated bank account provided in the income tax portal.

Section 244A of Income Tax Act - Legal Framework

Section 244A serves as the primary legal foundation for income tax refund interest in India. This provision was introduced to create a unified, automatic mechanism for compensating taxpayers when the Income Tax Department delays refund processing.

Historical Context and Legislative Intent

Section 244A replaced earlier fragmented provisions that separately dealt with different types of excess tax payments. Before this unified approach, taxpayers often had to separately claim interest or approach courts for compensation, creating administrative burden and delays.

The legislative intent behind Section 244A includes:

- Creating automatic statutory entitlement to interest on delayed refunds

- Providing uniform interest rates across different refund categories

- Reducing litigation by making interest calculation objective and mechanical

- Ensuring fair compensation for taxpayers facing government-caused delays

Legal Provisions and Taxpayer Rights

Under Section 244A, interest on income tax refunds is a taxpayer’s legal right, not a discretionary benefit from the tax department. The provision mandates that:

- Interest must be calculated automatically when refunds are processed

- The rate and calculation method are statutory, leaving no room for arbitrary decisions

- Interest payments cannot be denied for eligible refunds meeting threshold criteria

- The provision applies to all categories of taxpayers and assessment years

This legal framework ensures that taxpayers receive fair compensation when the government uses their excess tax payments beyond reasonable processing periods.

Historical Changes in Interest Rates

The ITR refund interest rate has evolved over time to balance taxpayer compensation with fiscal considerations:

Pre-1999 Era: Interest was paid at 4% per annum (0.33% per month) on delayed income tax refunds, which many considered inadequate compensation for inflation and opportunity costs.

1999-2016 Period: The rate was enhanced to 6% per annum (0.5% per month), establishing the current rate structure that better reflects market realities.

Recent Considerations: While the base rate remains 6% annually, some policy discussions have explored linking refund interest to market rates or government borrowing costs for better economic alignment.

The consistent 6% rate provides predictability for both taxpayers and the exchequer, though it may be relatively attractive during low-interest environments and less compensatory when market rates are higher.

Taxability of ITR Refund Interest

Understanding the tax implications of refund interest is crucial for proper compliance and accurate income tax return filing. The tax treatment differs between the principal refund amount and the interest component.

Tax Treatment Framework

Principal Refund Amount: The actual income tax refund is not taxable since it represents a return of your own overpaid taxes. This amount simply corrects the excess payment made during the financial year.

Interest Component: Interest received on income tax refund is fully taxable under “Income from Other Sources” in your income tax return. This interest represents additional income earned on your temporarily deposited funds with the government.

Reporting Requirements

When you receive refund interest, you must:

- Report the interest amount in the “Income from Other Sources” schedule of your ITR

- Include this interest in the financial year when it’s actually received or credited

- Cross-verify the interest amount with your refund order and bank statement

- Maintain supporting documents like the refund intimation from the Centralised Processing Centre

Year of Taxability

The interest becomes taxable in the financial year when it’s received, regardless of which assessment year’s refund it relates to. For example:

- Refund for FY 2022-23 (AY 2023-24) processed in November 2024

- Interest of Rs. 1,500 credited with the refund

- This Rs. 1,500 is taxable in FY 2024-25 (AY 2025-26)

TDS and Tax Planning

The Income Tax Department may deduct TDS on interest payments in certain cases, particularly for higher interest amounts. Any TDS deducted can be claimed against your total tax liability for that assessment year.

Since interest income is taxed at normal slab rates, taxpayers in higher tax brackets should factor this additional income into their tax planning and advance tax calculations.

When Interest is Not Payable on ITR Refunds

Several circumstances can disqualify taxpayers from receiving interest on their income tax refunds. Understanding these exclusions helps manage expectations and avoid disappointment when refunds are processed.

Threshold-Based Exclusions

10% Rule: No interest is payable if the refund amount is less than 10% of your total tax liability for the assessment year. This rule prevents interest payments on proportionally small refunds that may not justify administrative costs.

Minimum Amount Rule: Refunds below Rs. 100 don’t qualify for interest, regardless of the percentage of tax liability they represent. This absolute threshold filters out trivial amounts that could create processing overhead.

Taxpayer-Caused Delays

Interest is not payable when delays result from taxpayer actions or omissions:

Documentation Issues: Missing or incorrect documents, invalid bank account details, or failure to respond to Income Tax Department queries can disqualify interest payments.

Late Payment Consequences: If you paid advance tax or self-assessment tax late, you may not be eligible for interest on any refund arising from those delayed payments.

Processing Delays Within Normal Timeframe: When the tax department processes refunds within normal timeframes (typically 4-6 weeks after e-verification), no additional interest is due since there’s no actual delay.

System and Administrative Factors

Scrutiny Assessment Impact: While scrutiny proceedings generally don’t stop interest accrual, certain taxpayer non-cooperation during scrutiny can affect interest eligibility for the delay period attributable to the taxpayer.

Technical Errors: Errors in ITR filing, mismatched TDS details with Form 26AS, or incorrect income reporting can lead to refund delays that don’t qualify for interest compensation.

Understanding these exclusions helps taxpayers take proactive steps to avoid situations that could jeopardize their interest entitlement on legitimate refund claims.

How to Report Interest in ITR Filing

Proper reporting of refund interest in your income tax return ensures compliance and avoids potential notices from the tax authorities. The interest must be accurately disclosed in the appropriate sections of your ITR form.

Disclosure Requirements

Schedule OS (Other Sources): Declare the interest amount received on income tax refund in the “Income from Other Sources” schedule of your ITR form. This interest is treated like any other interest income you might receive.

Supporting Documentation: Maintain comprehensive records including:

- Refund order showing separate interest component

- Bank account statement confirming interest credit

- Form 26AS reflecting any TDS on interest payments

- CPC intimation details separating principal refund from interest

Step-by-Step Reporting Process

Identify the Interest Component: Check your refund intimation to separate the principal refund from interest amount

Determine the Correct Financial Year: Report interest in the year when it was actually received or credited

Fill Schedule OS: Enter the interest amount in the appropriate field for “Interest on Income Tax Refund”

Cross-verify with Form 26AS: Ensure consistency between your reported interest and any TDS certificates

Claim TDS Credits: If TDS was deducted on interest, claim it in the TDS section of your ITR

Common Compliance Mistakes

Many taxpayers inadvertently omit refund interest from their returns, viewing it as part of the refund rather than separate taxable income. This oversight can trigger mismatch notices from the tax department.

Another common error involves reporting interest in the wrong financial year, particularly when refunds span across multiple years. Always report interest in the year when it was actually credited to your bank account.

Professional tax advisors recommend maintaining a separate record of all refund-related transactions to ensure accurate reporting and seamless compliance with tax obligations.

Tips to Expedite ITR Refund Processing

Efficient refund processing minimizes delays and maximizes your interest earnings when delays do occur. Following best practices can significantly reduce processing time and ensure smooth refund experiences.

Pre-Filing Optimization

Timely Submission: File your income tax return before the due date to start interest calculation from April 1st rather than your actual filing date.

Bank Account Pre-validation: Complete bank account pre-validation in the income tax e-filing portal well before filing your return. This prevents processing delays due to banking formalities.

Document Verification: Ensure all TDS details in your return exactly match Form 26AS to avoid mismatches that could delay processing.

Filing Best Practices

Complete E-verification: Complete e-verification within 30 days of ITR submission using available methods like Aadhaar OTP, bank account validation, or demat account verification.

Accurate Information: Double-check all personal details, bank account information, and income figures to prevent queries that could delay refund processing.

Monitor Refund Status: Regularly check refund status through the income tax portal or CPC portal to identify and resolve any issues promptly.

Post-Filing Monitoring

Prompt Response to Notices: If the tax department raises any queries or requests additional information, respond immediately with required documents to avoid extended delays.

Regular Status Checks: Monitor your refund status and contact the tax department if processing extends beyond normal timeframes without apparent reason.

Professional Assistance: Consider engaging a chartered accountant for complex cases involving multiple income sources, business income, or significant refund amounts to ensure accuracy and faster processing.

Technology Utilization

Digital Documentation: Maintain digital copies of all supporting documents for quick submission if requested by tax authorities.

Mobile App Usage: Use the official Income Tax Department mobile app to track refund status and receive timely updates on processing milestones.

Automated Reconciliation: Use tax software that automatically reconciles TDS details with Form 26AS to minimize errors that could trigger manual verification processes.

These optimization strategies not only expedite refund processing but also demonstrate proactive compliance, reducing the likelihood of scrutiny or additional queries that could further delay your refunds.

The ITR refund interest rate system provides important protection for taxpayers while incentivizing efficient government processing. Understanding the 6% annual interest rate, eligibility criteria, calculation methods, and compliance requirements empowers you to maximize refund benefits and ensure proper tax compliance.

Whether you’re a salaried individual expecting TDS refunds or a business owner with advance tax overpayments, knowing how refund interest works helps you plan your cash flows and tax strategies more effectively. The key is timely filing, accurate documentation, and proactive monitoring of your refund status.

By following the guidelines outlined in this comprehensive guide, you can optimize your refund processing experience while ensuring full compliance with income tax obligations. Remember that refund interest, while beneficial, is taxable income that must be properly reported in your subsequent tax returns.

Stay informed about any changes to interest rates or calculation methods by monitoring official notifications from the Central Board of Direct Taxes, and consider consulting tax professionals for complex situations involving significant refund amounts or business-related excess payments.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.