_6_11zon.webp%3Falt%3Dmedia%26token%3D34373b7e-ea08-4a4f-a82e-289291c970b9&w=3840&q=85)

JSW Cement was incorporated in March 2006 as a public limited company and has since emerged as a formidable force in India's rapidly evolving cement industry. As part of the prestigious JSW Group, one of India’s most diversified and respected business conglomerates, the company began with a clear mission: to offer sustainable alternatives in cement manufacturing by adopting environmentally responsible practices right from the outset.

Over the past 19 years, JSW Cement has carved a niche for itself by focusing on green cementitious solutions, positioning sustainability not as a mere compliance requirement, but as a competitive advantage and core business value. At a time when the global cement industry is grappling with the environmental implications of high carbon emissions, JSW Cement has championed the use of industrial by-products such as Ground Granulated Blast Furnace Slag (GGBS) and fly ash, thereby reducing clinker usage and significantly cutting down its carbon footprint.

Today, it is not just a cement producer—it is a technology- and ESG-led construction material company, serving critical needs in infrastructure, housing, and industrial development. Its manufacturing footprint spans key regions of the country, and its capacity expansion plans signal the company’s ambition to become a pan-India leader in the green cement category.

With a blend of sustainable innovation, operational scale, and JSW Group synergies, JSW Cement is ideally positioned to contribute meaningfully to India’s infrastructure transformation while leading the industry toward a cleaner, greener future.

| Parameter | Details |

|---|---|

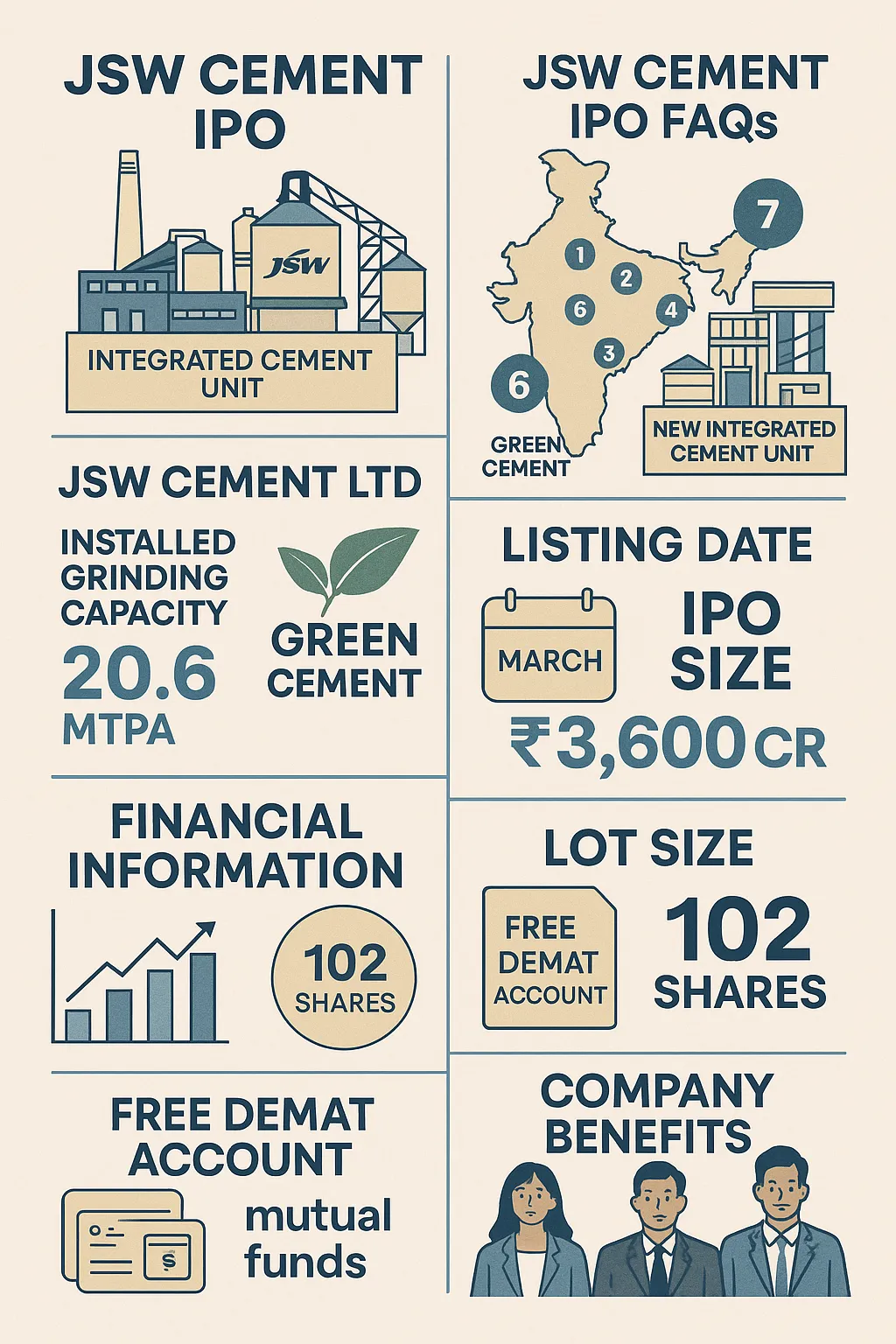

| Installed Grinding Capacity | 20.60 Million Tonnes Per Annum (MTPA) |

| Clinker Capacity | 6.44 Million Tonnes Per Annum (MTPA) |

| Number of Plants | 7 |

| Locations | Andhra Pradesh, Karnataka, Maharashtra, Odisha, and West Bengal |

Plant capacity overview (As of March 31, 2025)

The geographic spread enables JSW Cement to serve markets across Southern, Eastern, and Western India, offering freight advantages, better logistics management, and region-specific product tailoring.

Growth drivers

India's infrastructure development is entering a golden phase, supported by strong government push through programs like PM Gati Shakti, Smart Cities Mission, Housing for All, and Make in India. These initiatives demand not just scale, but also sustainable construction materials. Amidst this backdrop, JSW Cement Ltd., a part of the $23 billion JSW Group, is stepping forward with a bold, green agenda to reshape the Indian cement industry.

Unlike conventional cement manufacturers, JSW Cement is one of the few players operating on a low-carbon, circular economy model. The company leverages industrial waste like blast furnace slag and fly ash to manufacture blended cements, thus reducing clinker dependency and cutting CO₂ emissions. Now, with its ₹3,600 crore Initial Public Offering (IPO), JSW Cement aims to fund capacity expansion and deleverage its balance sheet—cementing its place as a pan-India green cement powerhouse.

Product portfolio

| Category | Product | Description / Feature | Primary Applications |

|---|---|---|---|

| Blended Cement | PSC (Portland Slag Cement) | Contains GGBS; enhances durability, reduces CO₂ emissions |

Bridges, foundations, coastal structures |

| PCC (Portland Composite Cement) | Highly durable; ideal for mass concreting |

Dams, tunnels, heavy infrastructure | |

| PPC (Portland Pozzolana Cement) | Fly ash-based; cost-effective, improves long-term strength |

General construction, low-rise housing | |

| Other Cement | OPC (Ordinary Portland Cement) | High early strength but higher carbon footprint |

Roads, high-load structures, precast units |

| Clinker | Intermediate product; partially sold to external grinding units |

Used in cement production | |

| GGBS (Granulated Blast Furnace Slag) | By-product from steel; improves performance and sustainability |

RMC, blended cement, high-performance concrete | |

| Allied Products | Ready-Mix Concrete (RMC) | Delivered in mixed form; consistent quality |

Mega infrastructure, real estate |

| Construction Chemicals | Admixtures, bonding agents, performance enhancers |

Commercial and industrial construction | |

| Waterproofing Compounds | Prevents leakage; improves durability of concrete |

Basements, rooftops, tanks | |

| Screened Slag | Processed industrial waste for reuse in cement/concrete |

Road construction, cement blending |

Sustainability at the core

JSW Cement’s operational philosophy is deeply rooted in environmental responsibility and sustainable manufacturing. The company follows a robust circular economy model, wherein industrial by-products like blast furnace slag and fly ash are efficiently converted into high-quality cementitious products, significantly reducing the environmental burden of waste disposal. In line with its green energy commitment, JSW Cement met 21.5% of its power requirements in FY25 through renewable sources such as solar energy and waste heat recovery systems (WHRS), lowering its carbon footprint. The company also maintains an industry-leading low clinker-to-cement ratio, which not only conserves natural resources but also minimizes CO₂ emissions during production. Moreover, certain manufacturing units have achieved water positivity, meaning they replenish more water than they consume, thereby contributing to ecological balance. Through these initiatives, JSW Cement has built a business model that is strongly aligned with Environmental, Social, and Governance (ESG) principles, aiming to create long-term value for the environment, its stakeholders, and the broader community.

Growth strategy: capacity expansion & market diversification

To transition into a pan-India cement major, JSW Cement is investing in greenfield and brownfield expansions to achieve:

Grinding Capacity: 41.85 MTPA

Clinker Capacity: 13.04 MTPA

Target Timeline: By FY2030

Key Projects:

Nagaur, Rajasthan (Greenfield)

Clinker: 3.30 MTPA | Grinding: 2.50 MTPA

₹800 Cr from IPO proceeds allocated

Land: 373 acres; Limestone Reserves: >600 million tonnes

Expected Commissioning: FY27

Hatta, Madhya Pradesh (Brownfield)

Talwandi Sabo, Punjab (Greenfield)

Eastern UP, Odisha (Mixed models)

JSW Cement is also exploring inorganic growth through M&As, especially distressed assets via the IBC route.

(The IBC route refers to acquiring distressed assets through the Insolvency and Bankruptcy Code. For JSW Cement, it offers a fast-track way to expand capacity by bidding for insolvent cement companies at attractive valuations. This approach enables quicker market entry, access to existing plants and raw material linkages, and lower capital costs compared to greenfield setups. Backed by JSW Group’s experience, the company is well-positioned to use the IBC route as a smart tool for inorganic growth.)

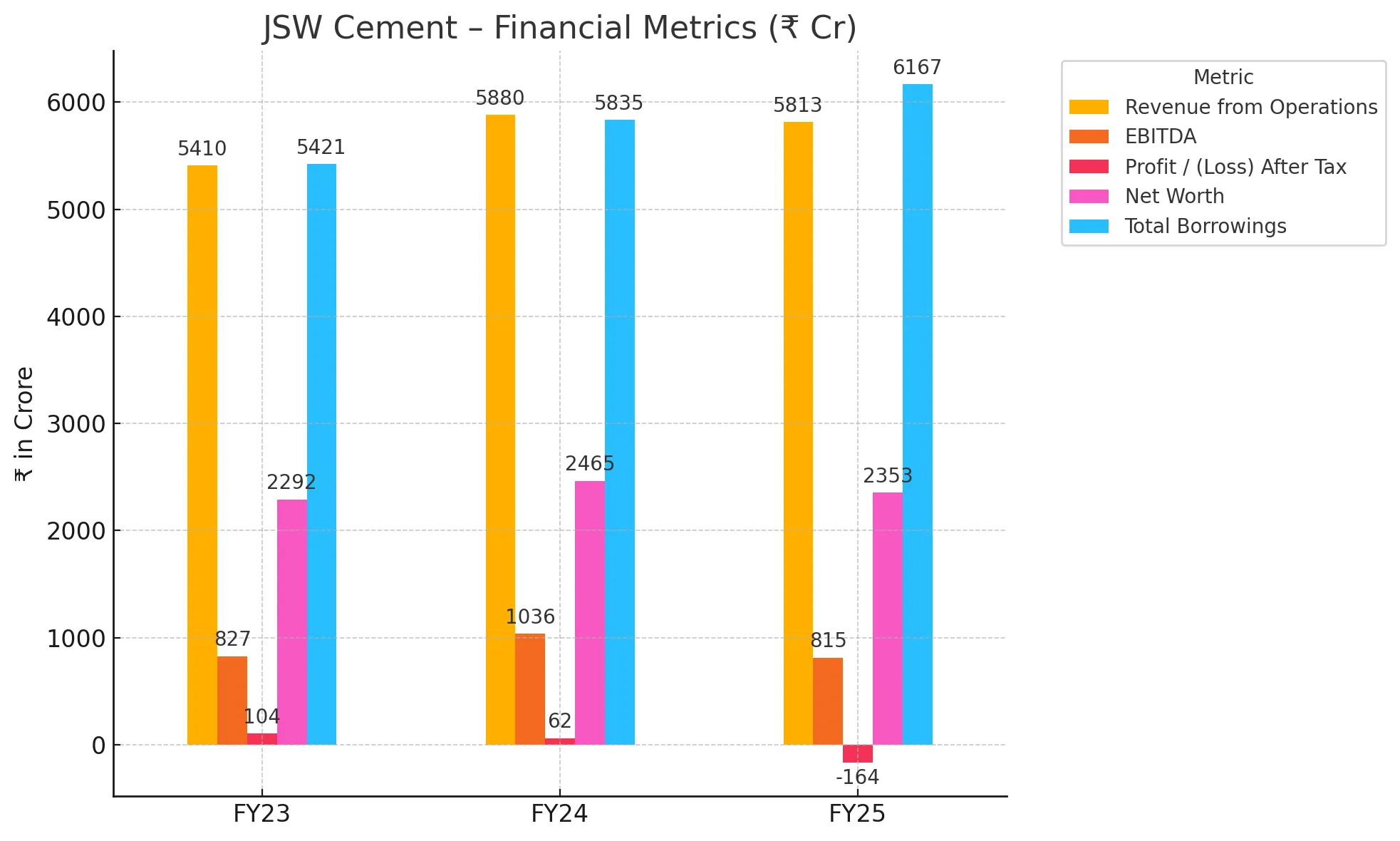

Financial overview (consolidated)

| Metric | FY25 | FY24 | FY23 |

|---|---|---|---|

| Revenue from Operations | ₹5,813 Cr | ₹5,880 Cr | ₹5,410 Cr |

| EBITDA | ₹815 Cr | ₹1,036 Cr | ₹827 Cr |

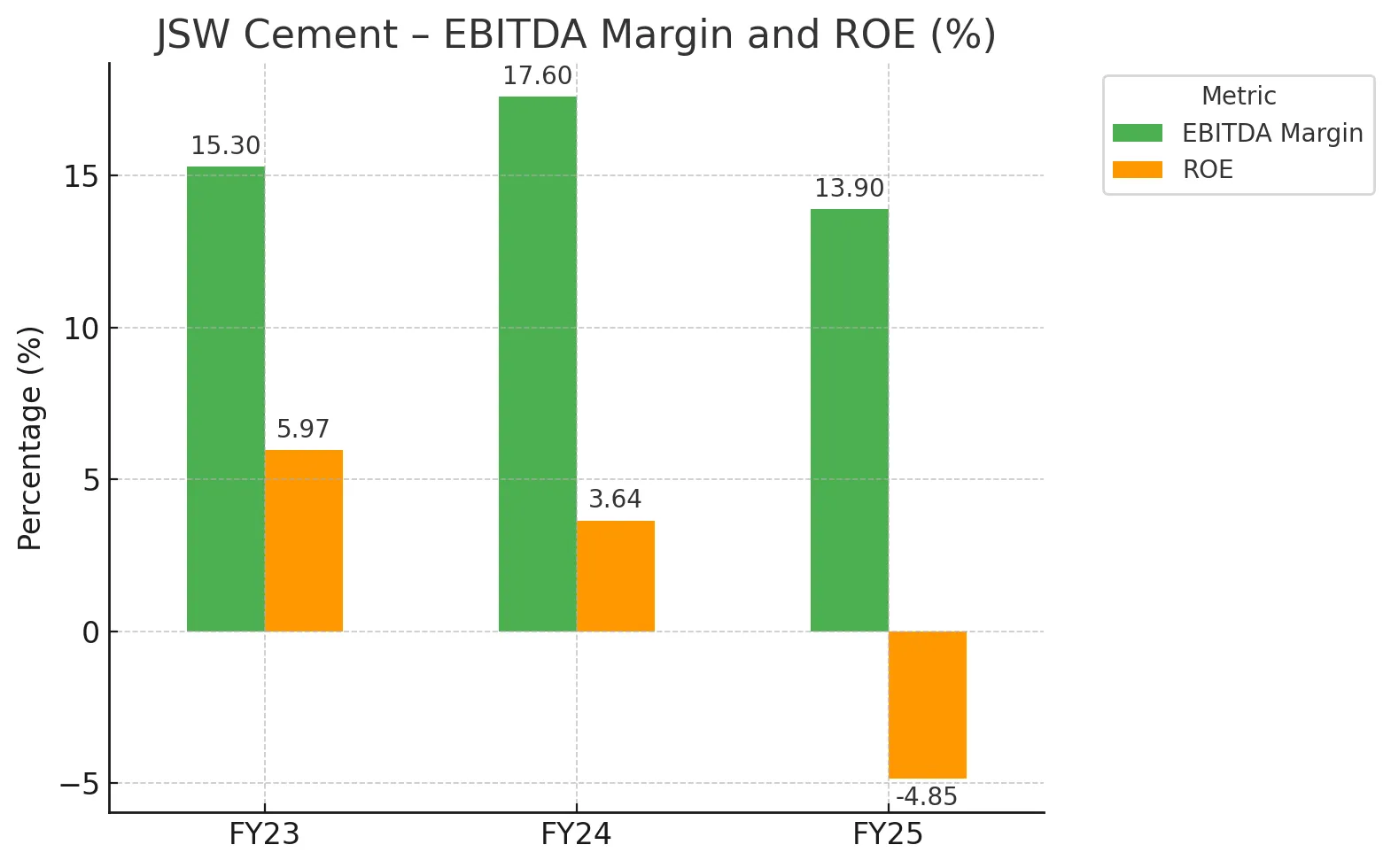

| EBITDA Margin | 13.9% | 17.6% | 15.3% |

| Profit / (Loss) After Tax | ₹(164) Cr | ₹62 Cr | ₹104 Cr |

| Net Worth | ₹2,353 Cr | ₹2,465 Cr | ₹2,292 Cr |

| Total Borrowings | ₹6,167 Cr | ₹5,835 Cr | ₹5,421 Cr |

| ROE | -4.85% | 3.64% | 5.97% |

FY25’s net loss is primarily due to:

Decline in cement realization per tonne (down 7.98%)

Increase in energy and raw material costs

Losses from joint ventures like JSW Cement FZC

IPO Details

| Attribute | Value |

|---|---|

| Total Issue Size | ₹3,600 crore |

| Fresh Issue | ₹1,600 crore |

| Offer for Sale (OFS) | ₹2,000 crore |

| Price Band | ₹139 to ₹147 per share |

| Face Value | ₹10 per share |

| Lot Size | 102 shares |

| Minimum Investment | ₹14,994 (at ₹147 per share) |

| Issue Opens | August 7, 2025 |

| Issue Closes | August 11, 2025 |

| Anchor Investor Bidding | August 6, 2025 |

| Listing Exchanges | NSE (Designated), BSE |

Selling Shareholders (OFS)

| Shareholder | Amount (₹ Cr) |

|---|---|

| AP Asia Opportunistic Holdings | ₹931.8 Cr |

| Synergy Metals Investments | ₹938.5 Cr |

| State Bank of India | ₹129.7 Cr |

Use of Fresh Issue Proceeds (₹1,600 Cr)

| Purpose | Amount (₹ Cr) |

|---|---|

| Setting up Nagaur Integrated Cement Plant | ₹800 |

| Repayment of Certain Borrowings | ₹520 |

| General Corporate Purposes | ₹280 (estimated) |

This allocation strengthens JSW Cement's capacity expansion, balance sheet health, and financial flexibility.

Promoters and Leadership

Promoters

| Name | Role |

|---|---|

| Sajjan Jindal | Chairman, JSW Group |

| Parth Jindal | Managing Director, JSW Cement |

| Sangita Jindal | Promoter |

| Adarsh Advisory Services | Promoter Group Entity |

| Sajjan Jindal Family Trust | Promoter Group Entity |

Key Management Personnel

| Name | Designation |

|---|---|

| Nilesh Narwekar | CEO & Whole-time Director |

| Narinder Singh Kahlon | Chief Financial Officer |

| Sneha Bindra | Company Secretary |

Strengths

Strong Parentage: Part of the well-diversified and financially sound JSW Group.

Sustainability Leadership: Among India’s top green cement manufacturers; 84% market share in GGBS.

Raw Material Security: Backward integrated via group synergies with JSW Steel.

Geographic Diversification: Presence across high-demand zones with expansion into north India.

Product Diversification: Wide portfolio beyond cement — includes RMC, construction chemicals.

Strong Distribution Network: Over 4,600 dealers, 8,800+ sub-dealers, and 150+ warehouses.

Efficient Logistics: Proximity to ports, railway sidings, and captive transport facilities.

Risks

High Group Dependency: 93% of blast furnace slag comes from JSW Steel; lack of supply diversification.

Execution Risk: Large greenfield projects like Nagaur could face regulatory, land, or cost delays.

Margin Pressure: Vulnerability to volatile fuel, freight, and raw material costs.

Debt Load: Though partly repaid via IPO, borrowings remain significant.

Geographical Gaps: Currently underrepresented in Northern India (though being addressed).

Regulatory Exposure: Mining and environmental clearances can be time-intensive.

Recent Profitability Dip: FY25 reported a loss due to cost escalations and JV losses.

Conclusion: A sustainable cement giant in the making

JSW Cement is more than just a cement producer—it is a strategic enabler of India’s green infrastructure revolution. With a firm commitment to environmental, social, and governance (ESG) principles, the company has positioned itself as a pioneer in sustainable manufacturing, supported by a robust product portfolio, an expanding pan-India footprint, and the financial and strategic backing of the esteemed JSW Group. Its upcoming IPO presents a rare and timely opportunity for investors to align themselves with India’s green construction boom, support a sustainability-first industrial player, and invest in a business with a well-defined roadmap to double its production capacity and accelerate profitability. While short-term challenges such as fluctuating raw material prices and execution risks on new projects may persist, the company’s long-term growth trajectory remains compelling—making it an attractive proposition for both institutional and retail investors looking to gain exposure to India's infrastructure growth story and ESG-aligned enterprises.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)