CNC (Computer Numerical Control) machines are the backbone of modern manufacturing. Instead of relying on manual operation, these machines follow pre-programmed instructions to cut, shape, and finish materials with incredible accuracy. From aircraft components to surgical implants, CNC technology powers the production of parts that demand precision, consistency, and efficiency on an industrial scale.

CNC (Computer Numerical Control) machines are automated manufacturing tools that operate using programmed instructions. They are a cornerstone of modern industrial production, delivering both precision and efficiency.

Precision machining: CNC technology enables the production of complex, highly accurate parts that meet the tight tolerances demanded by industries such as aerospace—think turbine blades, engine components, and landing gear, all designed to endure extreme conditions. In healthcare, CNC machining enables the creation of surgical instruments, implants, bone plates, and screws, where flawless finishes, precise measurements, and biocompatibility are crucial for patient safety.

Repeatability: Once programmed, CNC machines can produce identical components in large volumes with minimal variation, making them essential for consistent, high-quality mass production.

About the company

Jyoti CNC Automation Ltd is a vertically integrated global CNC machine maker with a strong experience of selling (installing) 135,000 machines and manufacturing footprints in India and France (Strasbourg via Huron).

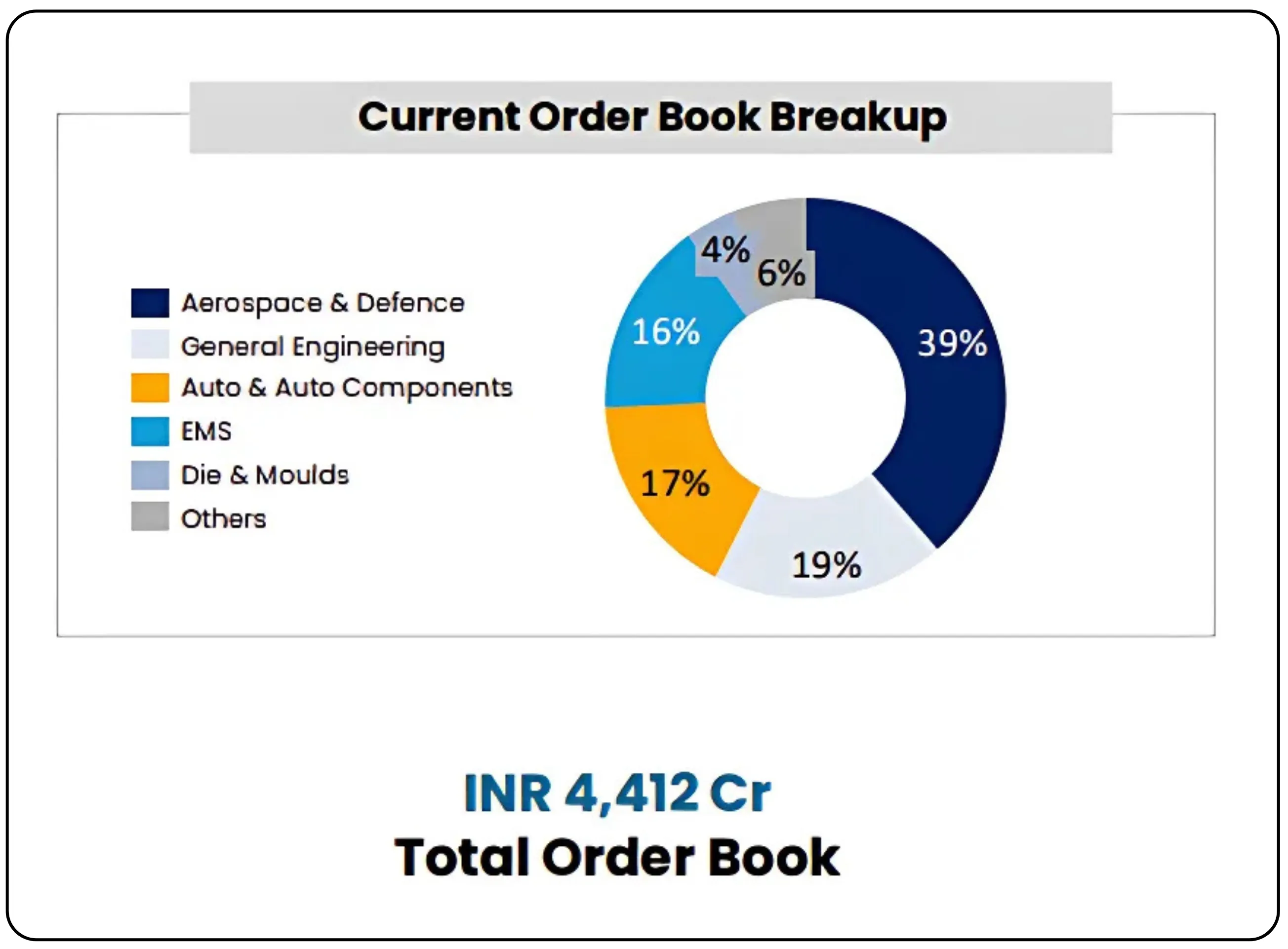

Jyoti CNC Automation currently has an installed manufacturing capacity of 6,000 machines per year in India. The company is undertaking a significant capacity expansion that will add another 10,000 machines annually by September 2026. Its order book stands at approximately ₹4,412 crore, with a well-diversified mix across aerospace, automotive, electronics manufacturing services (EMS), and general engineering sectors.

Jyoti offers more than 200 product variants and employs around 140 dedicated R&D professionals. Recently, the company acquired about 20 acres of land in Tumakuru, Karnataka, to establish customer support and technology hubs. The planned capital expenditure for these initiatives will be funded through a combination of internal accruals and debt, in line with management guidance.

Why it matters

Jyoti CNC Automation combines scale, vertical integration, and a wide product range (from entry-level models to high-ticket 5-axis machines) with a diversified, high-margin order book. This gives the company both stable cash generation and significant growth potential. The growth opportunity could accelerate further through its European subsidiary, Huron, a France-based CNC machine manufacturer that adds premium technology and a strong foothold in European markets. If capacity expansion and Huron’s integration into Jyoti’s global sales network progress as planned, order conversion could see a meaningful boost.

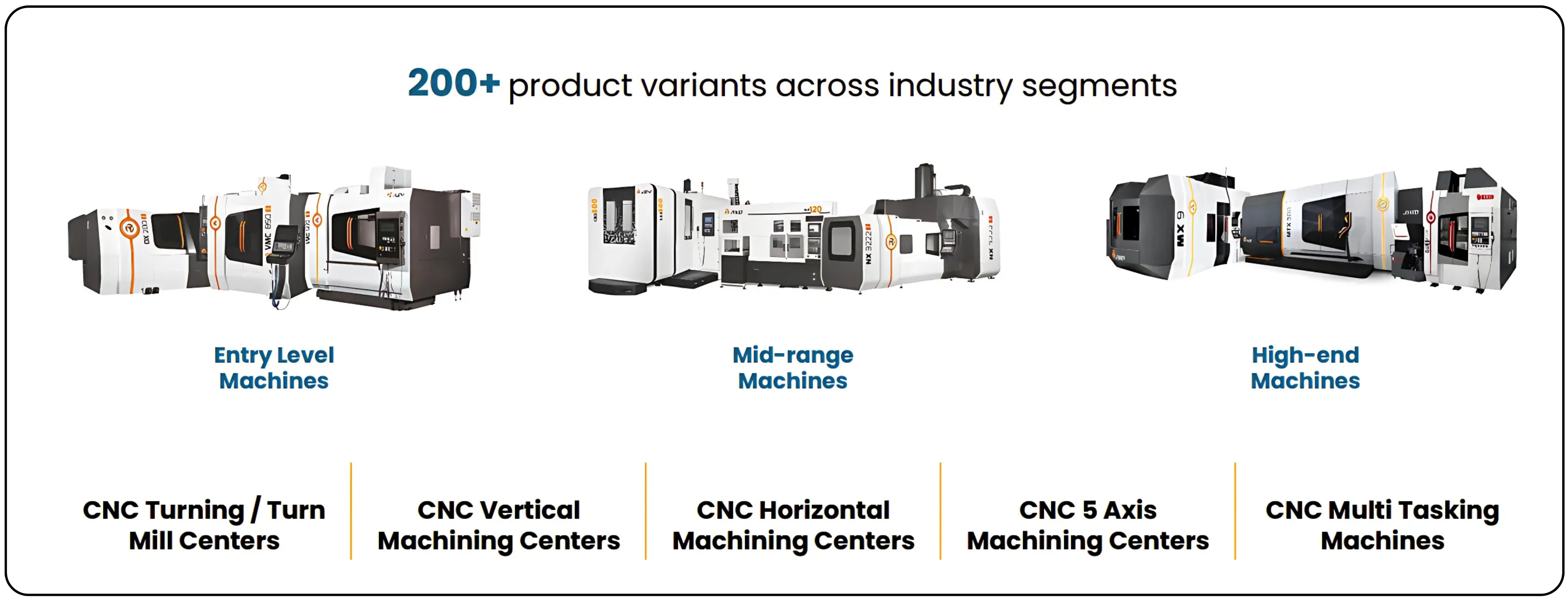

Product portfolio (how they make money)

Picture source: Jyoti CNC investor presentation, Q1FY26

Jyoti CNC’s product portfolio spans three main categories. Entry-level machines focus on high-volume, lower-ticket sales, while mid-range machines offer higher average selling prices. For customers, factors such as precision, reliability, and the Jyoti CNC machine price play an important role in selection across models. At the top end, the company produces large-format, 5-axis, and multi-tasking machines that cater to complex, high-value applications. Beyond machines, Jyoti also develops automated systems such as gantries, twin spindle setups, and automated loading solutions, as well as proprietary software like 7th Sense and HUMA UI. Aftermarket services, including spares and maintenance, further add to recurring revenue. The company also provides detailed information like the Jyoti CNC machine price list to help customers compare features and costs. High-end machines deliver the strongest gross margins, exceeding 55% according to management, while entry- and mid-range models maintain healthy margins in the 35–47% range. In turning machines, buyers often evaluate using the Jyoti CNC turning machine price list to match requirements with budget.

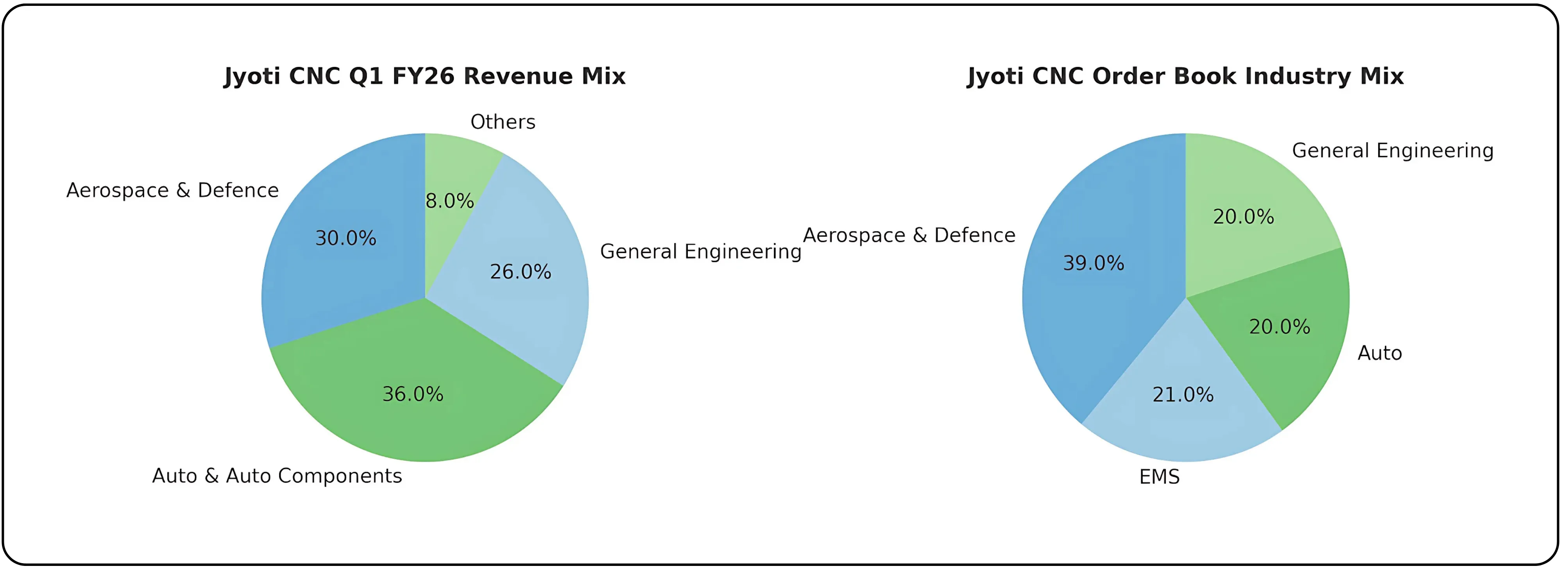

End-market split and strategic focus

Picture source: Jyoti CNC investor presentation, Q1FY26

Q1 FY26 revenue mix: aerospace & defence 30%, auto & auto components 36%, general engineering 26%, others 8%. Order book industry mix is skewed further to aerospace (≈39% of order book), with EMS, auto, and general engineering also well represented. The business deliberately targets higher-value sectors (aerospace, defence, EMS) to lift blended ASPs and margins over time.

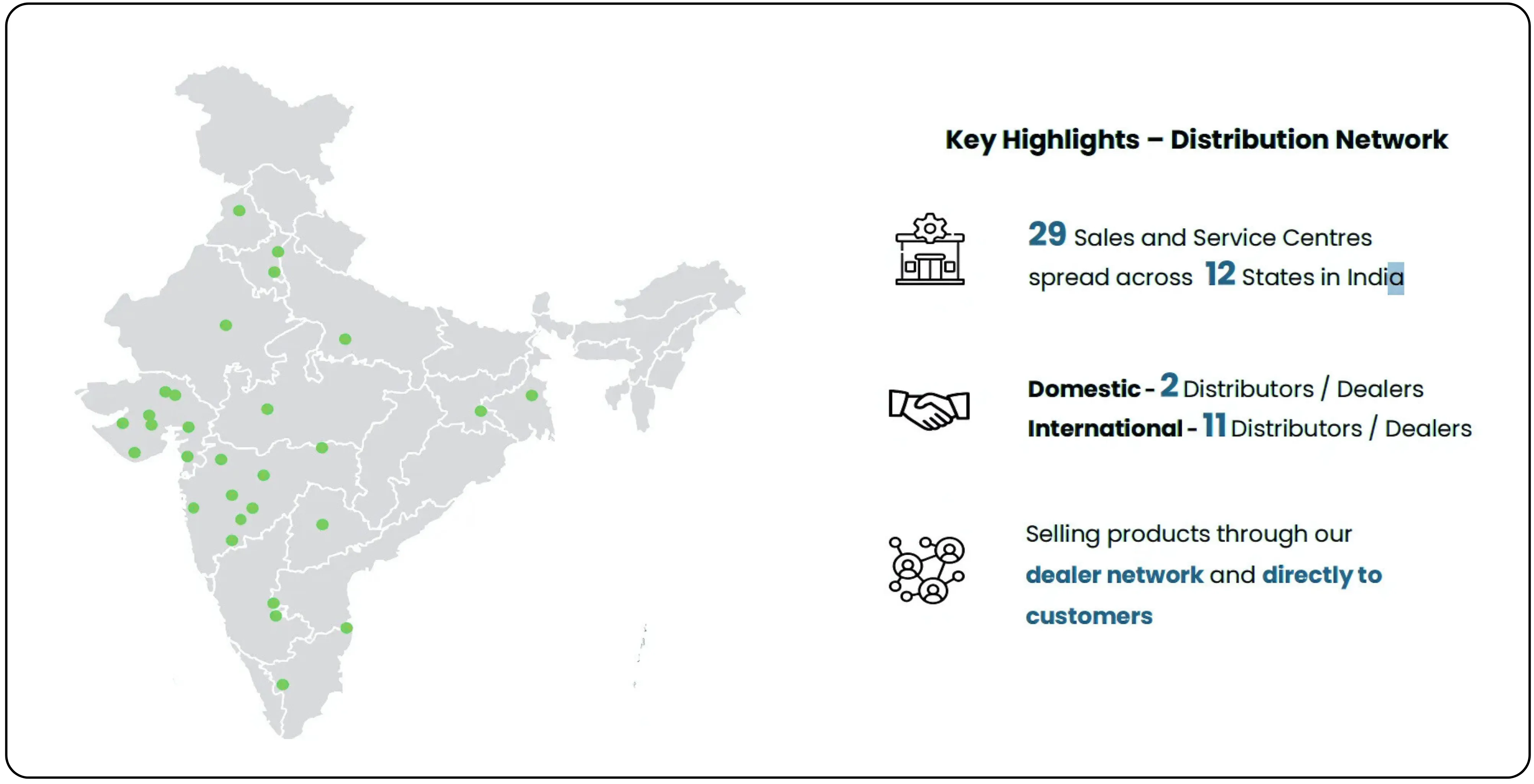

Geography and go-to-market

Picture source: Jyoti CNC investor presentation, Q1FY26

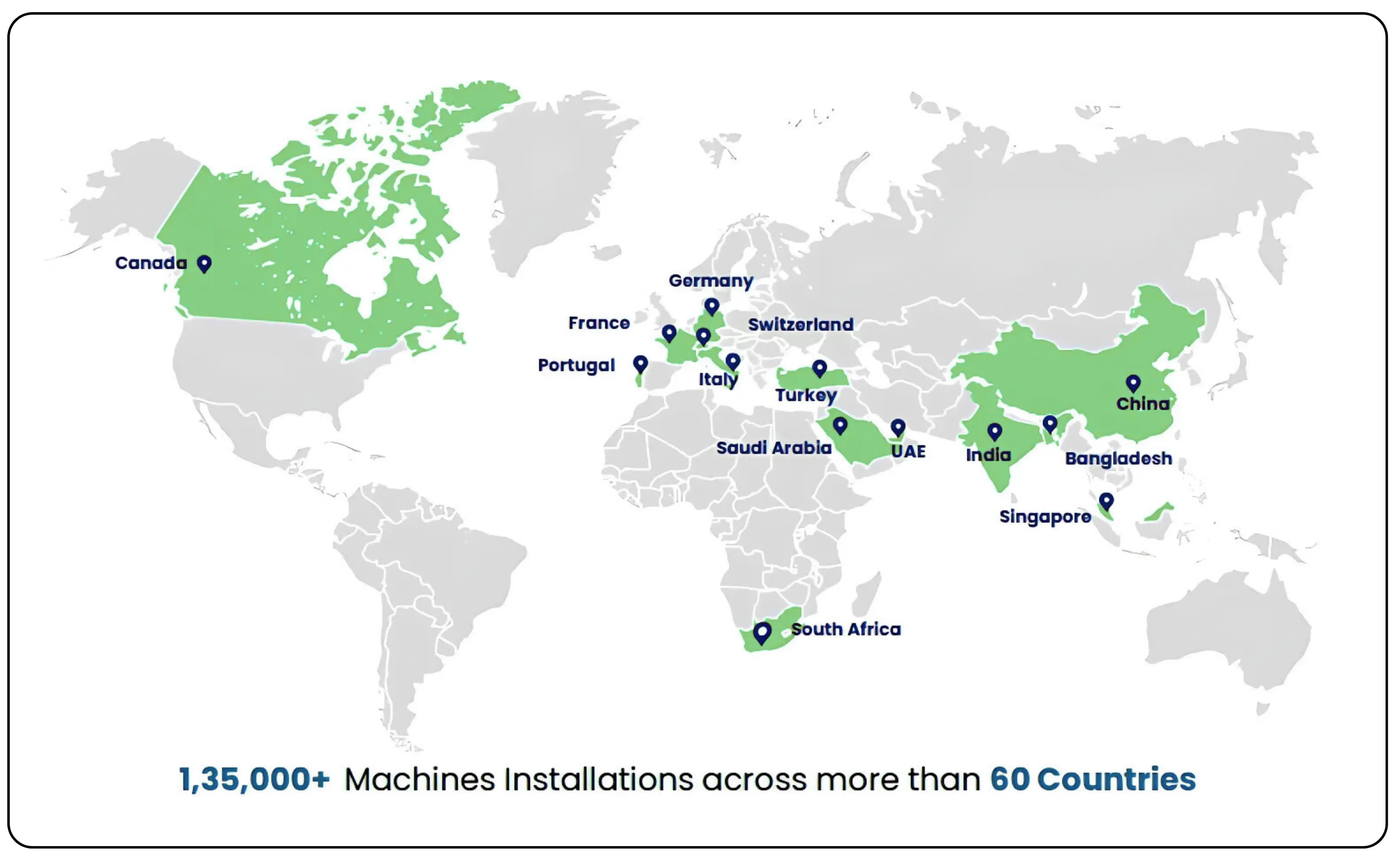

Jyoti CNC is pursuing a two-pronged market strategy. In India, the focus is on scaling operations through a network of 29 sales and service centres, supported by an extensive dealer network. In Europe, growth is driven by its subsidiary Huron, which brings advanced CNC technology and an established sales channel. The company’s export footprint extends across Europe, Canada, Turkey, and several other markets. This combination of a strong global brand in Huron and a deep domestic presence in India provides diversification benefits and creates cross-selling opportunities, particularly in aftermarket parts and service revenue.

Picture source: Jyoti CNC investor presentation, Q1FY26

Manufacturing, capacity and delivery model

Jyoti CNC’s core manufacturing operations are fully vertically integrated, covering in-house machining, sheet metal work, assembly, and paint lines. This reduces reliance on third-party suppliers and helps improve delivery timelines. The company currently has an installed capacity of around 6,000 CNC machine units per year in India, in addition to 121 machines annually from its facility in France. Management is in the process of expanding Indian capacity by an additional 10,000 machines by September 2026. To support this growth, Jyoti has also acquired about 20 acres of land in Tumakuru, Karnataka, for establishing customer support centres, demonstration facilities, and warehousing. The planned capital expenditure for these initiatives will be funded through a combination of internal accruals and a manageable level of debt.

Aftermarket, services and durability of revenue

The aftermarket business which includes spares, service, and training plays a key role in strengthening customer loyalty and reducing sales cycles. Jyoti’s large installed base of over 135,000 machines generates a steady demand for spare parts and maintenance, creating a recurring revenue stream. As the number of machines in operation and their utilisation increase, this aftermarket segment supports consistent cash flow and helps maintain margin stability.

R&D and product differentiation

Jyoti’s R&D team, comprising around 140 professionals, focuses on developing products for higher average selling price segments such as aerospace, electronics manufacturing services (EMS), and defence. Key initiatives include the HUMA control panel, the Tachyon Beta 5-axis machine, and a range of automation kits. The acquisition of Huron brings advanced technology capabilities and strengthens Jyoti Automation’s position in Europe, providing a competitive edge in supplying large-ticket machines to high-value defence and industrial customers.

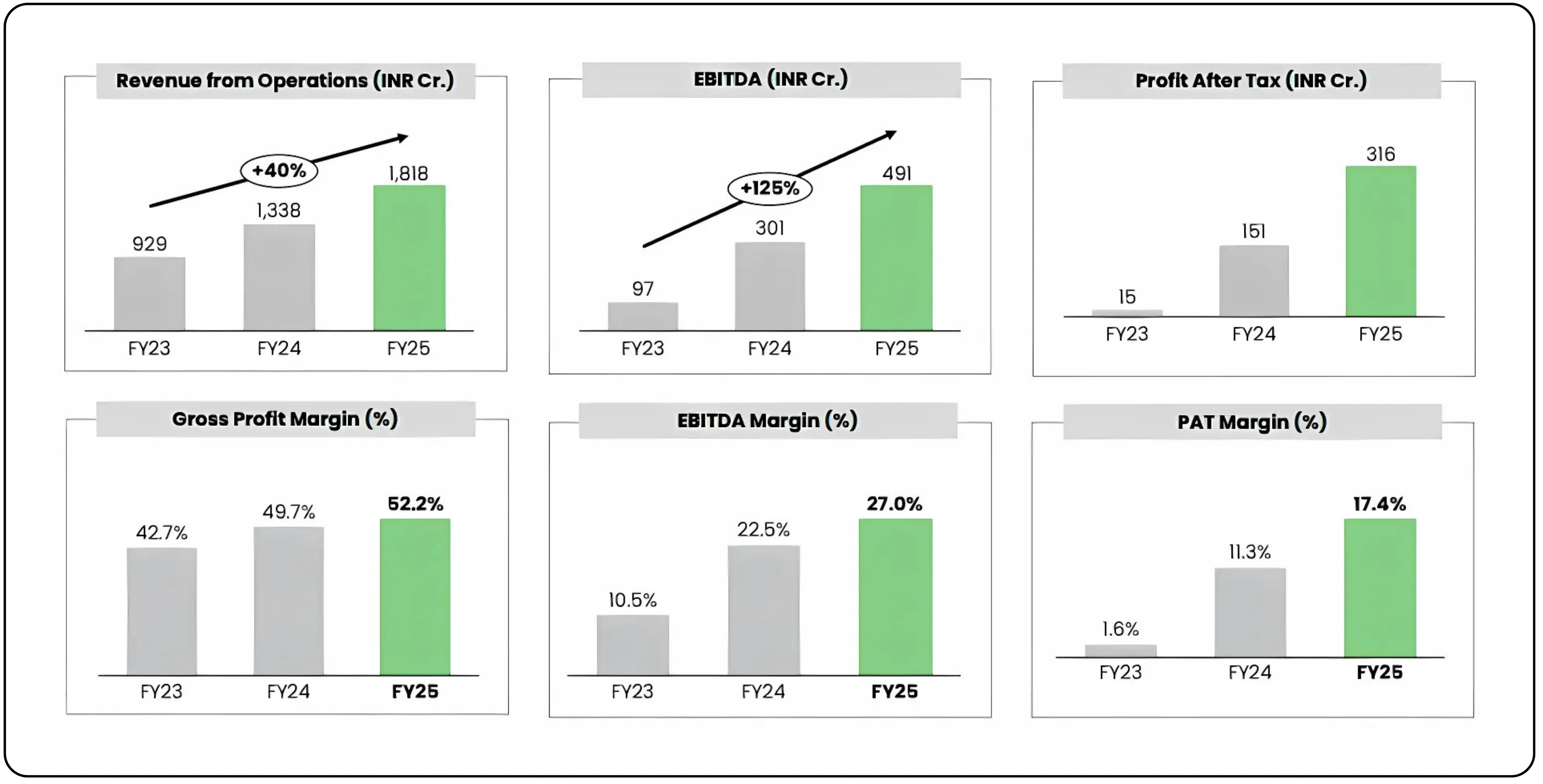

Financial performance

The business has moved from recovery to scale: FY25 consolidated revenue was ₹1,818 crore, EBITDA margin expanded to 27%, and Net profit margin was 17.4%. Market cap is ₹20,800 crore, and the company trades at a premium (P/E 61.9 vs industry ~38.2), reflecting both strong profitability and high growth expectations. The steady growth reflects demand for high-quality Jyoti machine solutions across industries

What this means (practical implications)

Here’s the thing: the combination of a healthy order book (₹4,412 crore), higher margins (EBITDA margin 24–27% run rate), and a capacity expansion plan means revenue growth should accelerate once new lines come online and Huron's scale-up materializes. Execution risk is real (skilled labour, supply chain, working capital), but the business model of high gross margins on high-end machines + recurring service revenue is inherently value accretive if Jyoti converts order backlog at current margin levels.

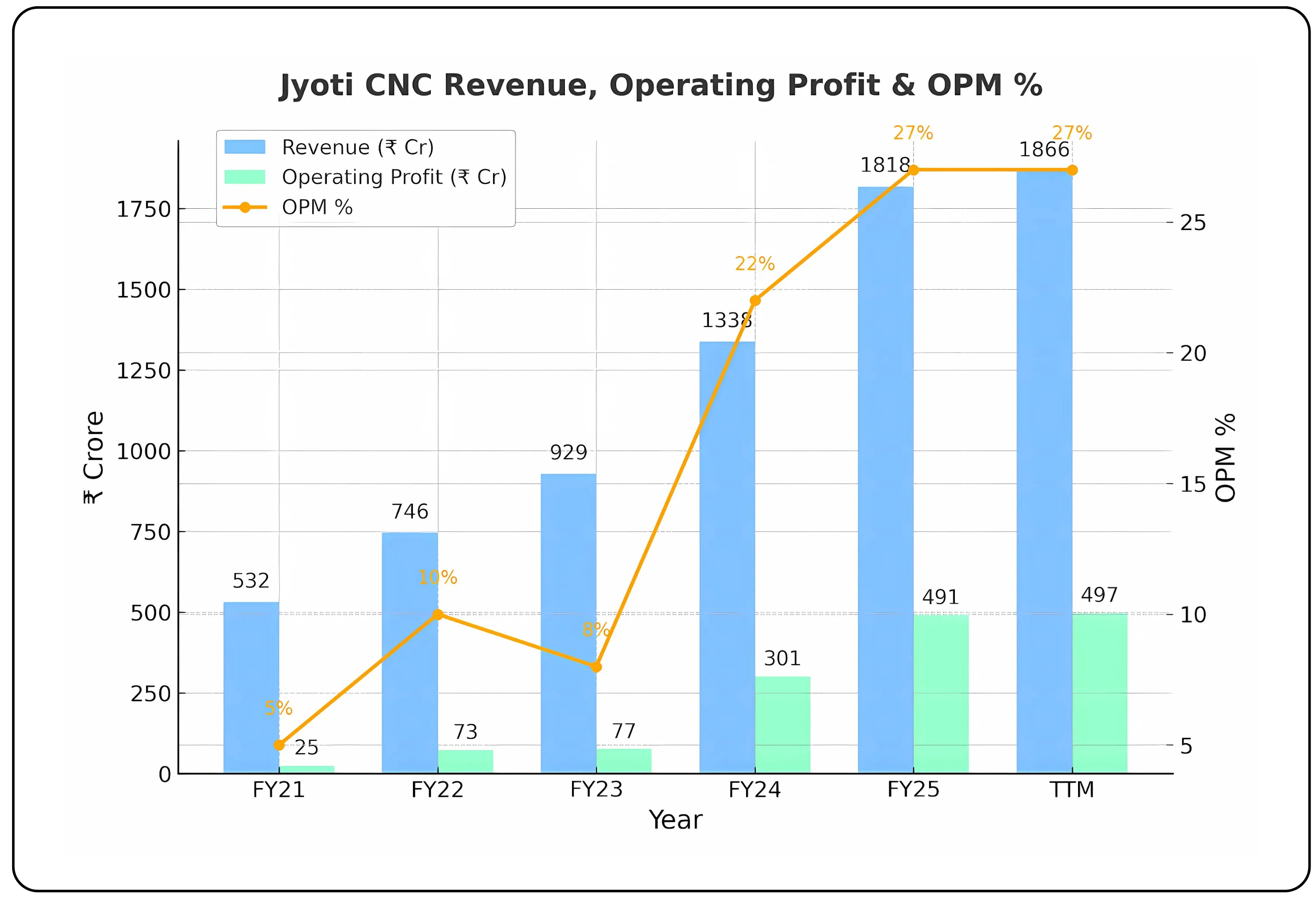

Since FY21, Jyoti CNC Automation has undergone a clear turnaround from a challenging phase into a period of sustained growth and profitability. In FY21, revenue stood at ₹532 crore with an operating margin of 5% and a net loss of ₹77 crore. The business began to recover in FY22 as demand improved across key sectors, with revenue rising to ₹746 crore and margins moving back into double digits.

| Year | Revenue (₹ Cr) | Operating Profit (₹ Cr) | OPM % | Net Profit (₹ Cr) |

|---|---|---|---|---|

| FY21 | 532 | 25 | 5% | -77 |

| FY22 | 746 | 73 | 10% | -48 |

| FY23 | 929 | 77 | 8% | -5 |

| FY24 | 1,338 | 301 | 22% | 151 |

| FY25 | 1,818 | 491 | 27% | 316 |

| TTM | 1,866 | 497 | 27% | 337 |

Growth picked up sharply from FY23, with revenue rising from ₹929 crore to ₹1,818 crore in FY25 and operating margins expanding from 8% to 27%, driven by a higher share of premium CNC machines and better pricing. Net profit swung from a ₹5 crore loss in FY23 to ₹316 crore in FY25, delivering ROE of 21.2% and ROCE of 24.4%. The ₹4,412 crore order book offers 2–3 years of visibility, led by aerospace, defence, auto, and EMS. Debt-to-equity improved to 0.29, though working capital needs remain high. Cash flows were negative in FY24–FY25 due to inventory build-up, but management expects improvement as new capacity and order execution ramp up from FY27. At ₹916, the stock trades at 61.9x TTM earnings, a premium that hinges on flawless execution.

Strategic positioning

Jyoti CNC Automation Limited occupies a rare position in the global CNC market; it is large enough to compete on scale, yet agile enough to customize for high-spec clients in aerospace, defence, and EMS. The vertical integration from casting to software interface keeps gross margins structurally higher than peers. Its presence in both the mass Indian market and the premium European segment (via Huron) provides a natural hedge: India drives volumes, and Europe drives ASPs and technology leadership.

This positioning is reinforced by three factors:

- R&D-led differentiation — Proprietary automation solutions and user interfaces improve machine productivity and lock in customers for repeat orders and service contracts.

- Balanced market exposure — A well-spread order book prevents over-reliance on any single sector or geography, reducing cyclicality risks.

- Capacity runway — The planned scale-up from 6,000 to 16,000 units annually by FY27 could materially shift its market share in India and expand its export base.

The challenge is execution: long manufacturing cycles, high working capital needs, and skilled labour dependence mean that even with a strong backlog, delays can erode margins. Competitively, Jyoti’s premium valuation leaves little room for missteps order conversion, timely capex completion, and integration of European operations must all align for the current growth trajectory to hold.

Industry outlook & growth drivers

The global CNC machine tools market is projected to grow at a CAGR of 5–6% over the next

five years, driven by automation adoption, precision manufacturing needs, and the reshoring of supply chains. In India, the sector is benefiting from the government’s production-linked incentive (PLI) schemes, higher capital expenditure by automotive and aerospace OEMs, and import substitution in high-end machining.

CNC Jyoti technology is well-placed to capture this aerospace and defence momentum, supported by indigenisation programs under the Make in India initiative. This is a key growth lever for Jyoti CNC, as aerospace already accounts for nearly 40% of its order book. Electronics manufacturing services (EMS), another high-margin segment, is growing rapidly as global brands expand Indian assembly lines for telecom, automotive electronics, and consumer devices.

The company’s European presence via Huron offers an additional growth vector: the EU is investing heavily in industrial automation to counter labour shortages, creating demand for multi-axis and large-format CNC machines where Huron’s portfolio is strong. Combined with Jyoti’s cost advantage from Indian manufacturing, this positions the company to expand market share in premium export markets.

The medium-term growth outlook is therefore anchored on three reinforcing trends: rising domestic demand for advanced CNC solutions, premium export opportunities through Huron, and capacity expansion in India to service both.

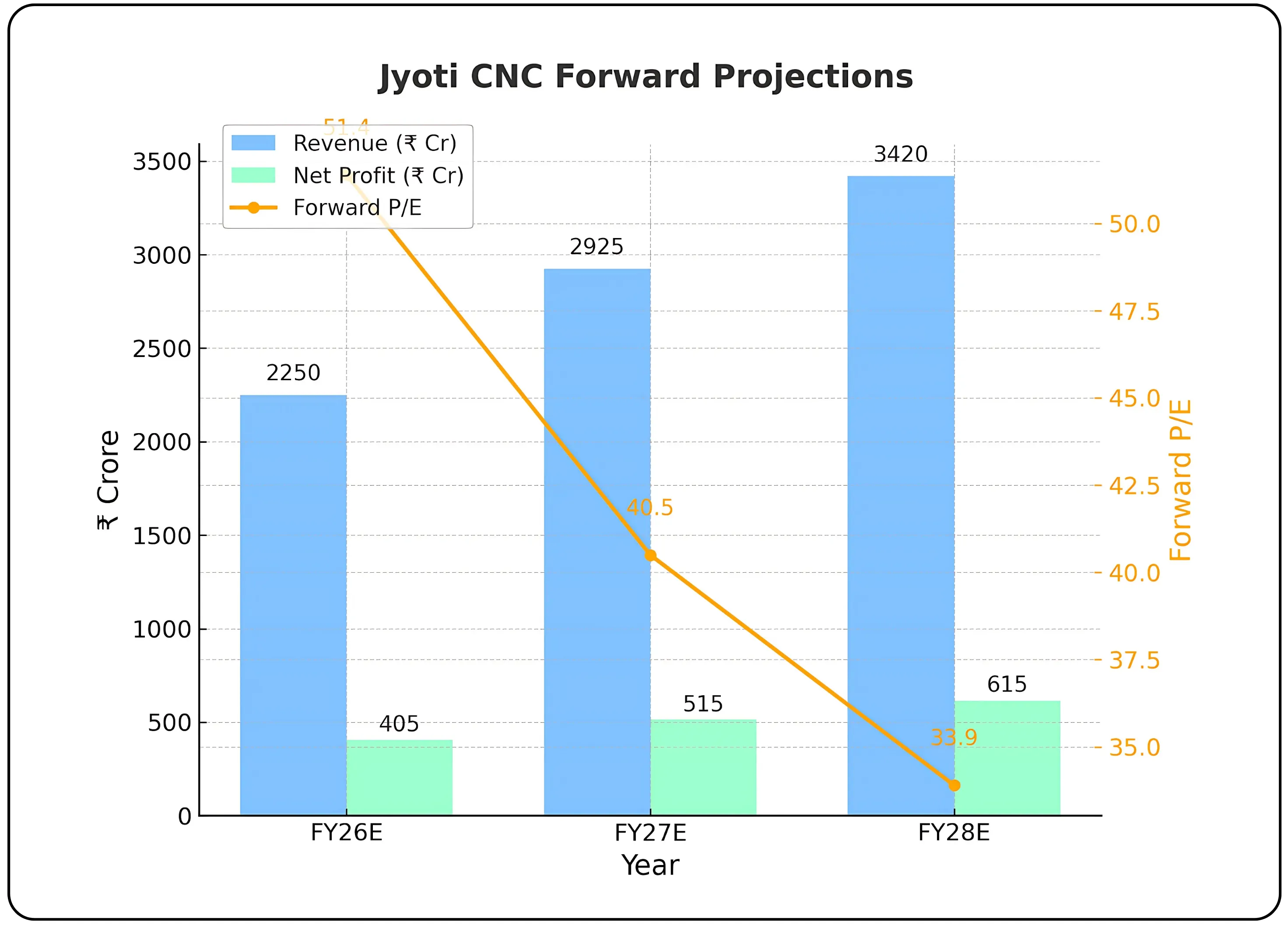

Forward outlook & valuation projection

Jyoti CNC’s order book of ₹4,412 crore, as of Q1 FY26, offers revenue visibility for at least the next two to three years. Assuming a conservative execution rate of 70% of the current order book within this period, this translates into approximately ₹3,088 crore of revenue from the existing pipeline alone. Additional orders from capacity expansion and market share gains would add further upside.

Given management’s focus on higher-value machines and premium segments like aerospace, defence, and complex multi-axis machining, we project EBITDA margins to remain in the 25–27% range and net profit margins at ~17–18% over the medium term.

The planned capacity expansion (increasing annual production from 6,000 to 16,000 CNC Jyoti machines by September 2026) is likely to support accelerated growth from FY27 onwards. The integration of Huron’s European manufacturing expertise and sales network should also open higher-margin opportunities in export markets.

Based on these drivers, our base case projections are:

| Year | Revenue (₹ Cr) | Net Profit (₹ Cr) | EPS (₹) | Forward P/E* |

|---|---|---|---|---|

| FY26E | 2,250 | 405 | 17.8 | 51.4 |

| FY27E | 2,925 | 515 | 22.6 | 40.5 |

| FY28E | 3,420 | 615 | 27.0 | 33.9 |

*Above PE is calculated on the market price of 925 as of 13th Aug 2025.

While the current P/E multiple is elevated at 61.9x TTM earnings, the forward P/E drops meaningfully to 33.9x by FY28 in our projections, assuming execution meets expectations. This valuation compression would be driven by earnings growth rather than share price correction, making consistent order conversion and margin retention critical.

Risks & challenges

While Jyoti CNC’s growth prospects are strong, execution risks remain material. Large-ticket CNC machines have long manufacturing and delivery cycles, which can stretch working capital and create timing mismatches in cash flow already visible in recent negative operating cash flows due to inventory build-up. Any delays in customer acceptance or payment cycles could pressure liquidity despite a healthy order book.

The planned capacity expansion to 16,000 machines by September 2026 is a major operational challenge. Scaling up without compromising quality, lead times, or margins will require the timely hiring of skilled labour, supply chain coordination, and ramp-up of new facilities.

High-end CNC demand is also sensitive to capex cycles in automotive, aerospace, and EMS sectors. A slowdown in these end markets whether due to macroeconomic weakness, geopolitical shocks, or changes in government defence spending could push out order conversion timelines. Balancing growth potential with market pricing

Jyoti CNC has transitioned from a recovery story to a scaled, high-margin global CNC manufacturer with a well-diversified order book and strong market positioning in premium segments. The integration of Huron’s European presence, combined with aggressive capacity expansion in India, sets the stage for sustained double-digit revenue growth over the medium term.

The ₹4,412 crore order book provides revenue visibility for the next two to three years, while the targeted move toward higher-value machines supports the current EBITDA margin band of 25–27%. Execution of the Tumakuru facility and the 10,000-machine capacity addition by FY27 will be key catalysts, as will the ability to maintain product differentiation through ongoing R&D investment.

From a valuation perspective, the stock trades at a rich trailing multiple (P/E 61.9) versus the industry average (38.2), reflecting high growth expectations. Our projections indicate a forward P/E of 33.9x by FY28 if execution remains on track and margins hold, implying that earnings growth, not price compression, will drive a more balanced valuation profile.

Overall, Jyoti CNC’s fundamentals are aligned with sustained growth, but the combination of high market expectations and execution complexity means the margin for error is thin. For investors, the next two years will be the proving ground for whether the company can deliver scale without sacrificing quality, profitability, or balance sheet strength.

Start your trading journey with CubePlus today and stay in control of your investments. [Sign up now] and trade smarter.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.