Mangal Electrical Industries Limited (MEIL) often searched as Mangal Electrical makes transformer components CRGO slit coils, cut laminations, wound/toroidal cores, core/coil assemblies and oil-immersed circuit breakers, anchoring its transformer manufacturing portfolio in India’s power sector. Its offerings support energy efficiency in distribution networks, and together with EPC services for substations, the company also serves renewable energy developers alongside utilities. It also trades CRGO/CRNO coils, manufactures distribution/medium-power transformers (single-phase 5 KVA up to three-phase 10 MVA), and undertakes EPC work for substations. The company was converted to a public limited company on Jul 25, 2024.

MEIL’s manufacturing footprint is in Rajasthan (Jaipur, Reengus/Sikar, Pratapgarh). It holds ISO 9001:2015 and ISO 14001:2015 certifications, has a NABL-accredited lab, and PGCIL approvals up to the 400 kV class, useful differentiators for utility-grade supply.

Key customers span PSU utilities and private developers (e.g., NTPC, PGCIL, BHEL; Voltamp Transformers; Adani/Renew) in India and abroad, including renewable energy players.

As of Jun 30, 2025, the order book stood at ₹29,419.78 lakh.

IPO Details

| Field | Details |

|---|---|

| Type/Size | 100% fresh issue aggregating up to ₹400.00 crore (face value ₹10). Price band/minimum lot will be decided closer to opening. |

| IPO objectives | (i) Debt repayment/prepayment ₹101.27 cr (ii) Capex to expand Unit-IV (Reengus, Sikar) ₹87.86 cr (iii) Working capital ₹122.00 cr (iv) General corporate purposes (≤25% of gross) |

| Schedule | Anchor: Aug 19, 2025 Opens: Aug 20, 2025 Closes: Aug 22, 2025 (UPI mandate cut-off 5 pm on close day) |

| Listing | Proposed BSE & NSE; NSE is the designated exchange. |

| BRLM / Registrar | Systematix Corporate Services (BRLM); Bigshare Services (Registrar). |

| Allocation (book-built) | Up to 50% Net QIB, ≥15% NII, ≥35% Retail; standard NII 1/3 + 2/3 sub-buckets; Mutual Fund 5% carve-out in QIB. |

Portfolio

| Category | What they sell |

|---|---|

| Components | CRGO slit coils & cut laminations, wound/toroidal cores, core/coil assemblies, amorphous cores, oil-immersed circuit breakers |

| Trading | CRGO/CRNO coils and amorphous ribbons |

| Transformers & EPC services | Transformers (5 KVA–10 MVA) and EPC for sub-stations |

Geographic Diversification

Primary markets today include India, UAE, Netherlands, Nepal, Oman, Indonesia and Malaysia.

Top Countries

Exports contributed 3.05% of FY25 revenue top lanes included:

- Netherlands (₹853.12 lakh)

- UAE (₹222.33 lakh)

- Malaysia (₹300.51 lakh)

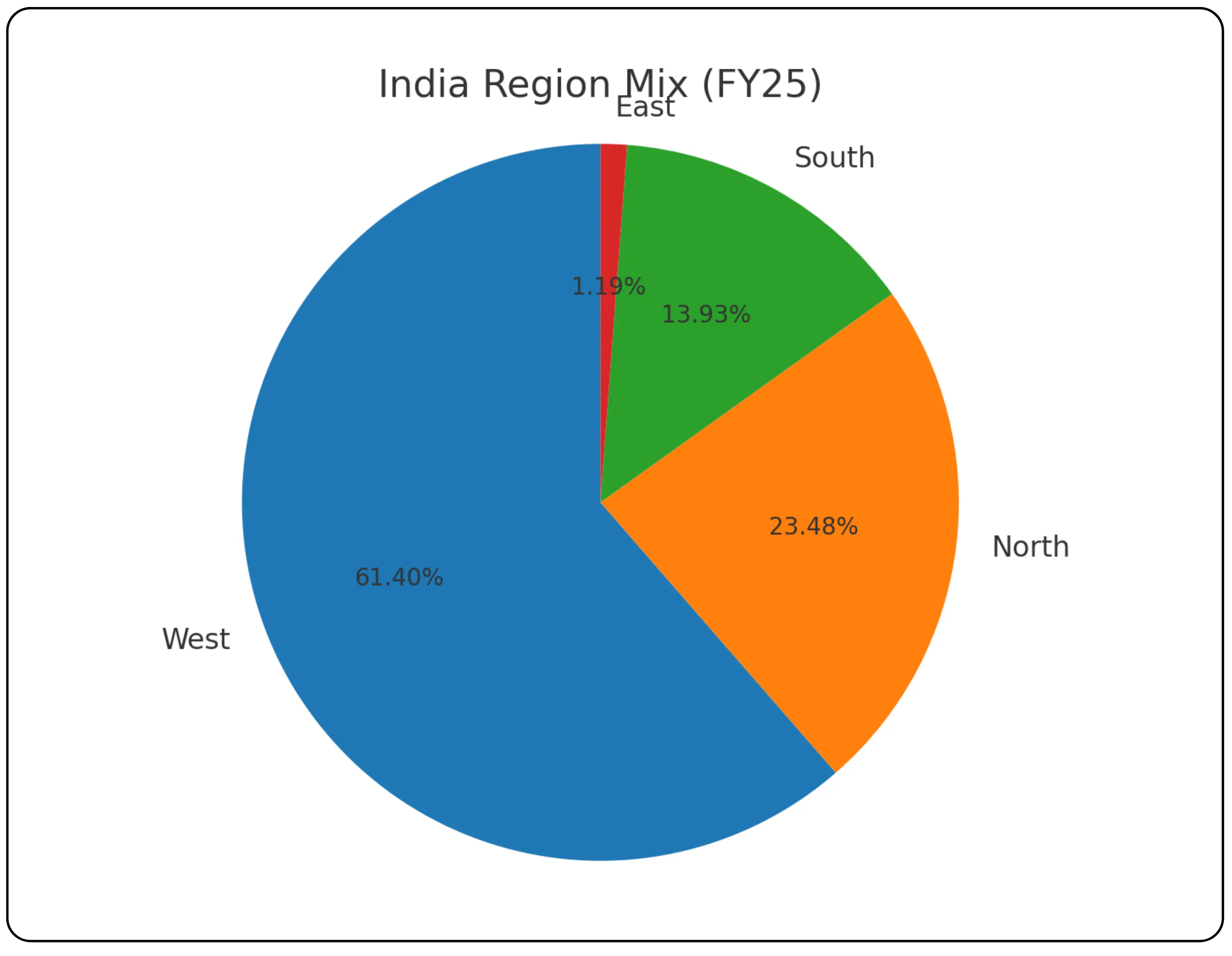

India region mix (FY25):

- West 61.40%

- North 23.48%

- South 13.93%

- East 1.19%

Financial Highlights (In crores)

| Metric | FY25 | FY24 | FY23 |

|---|---|---|---|

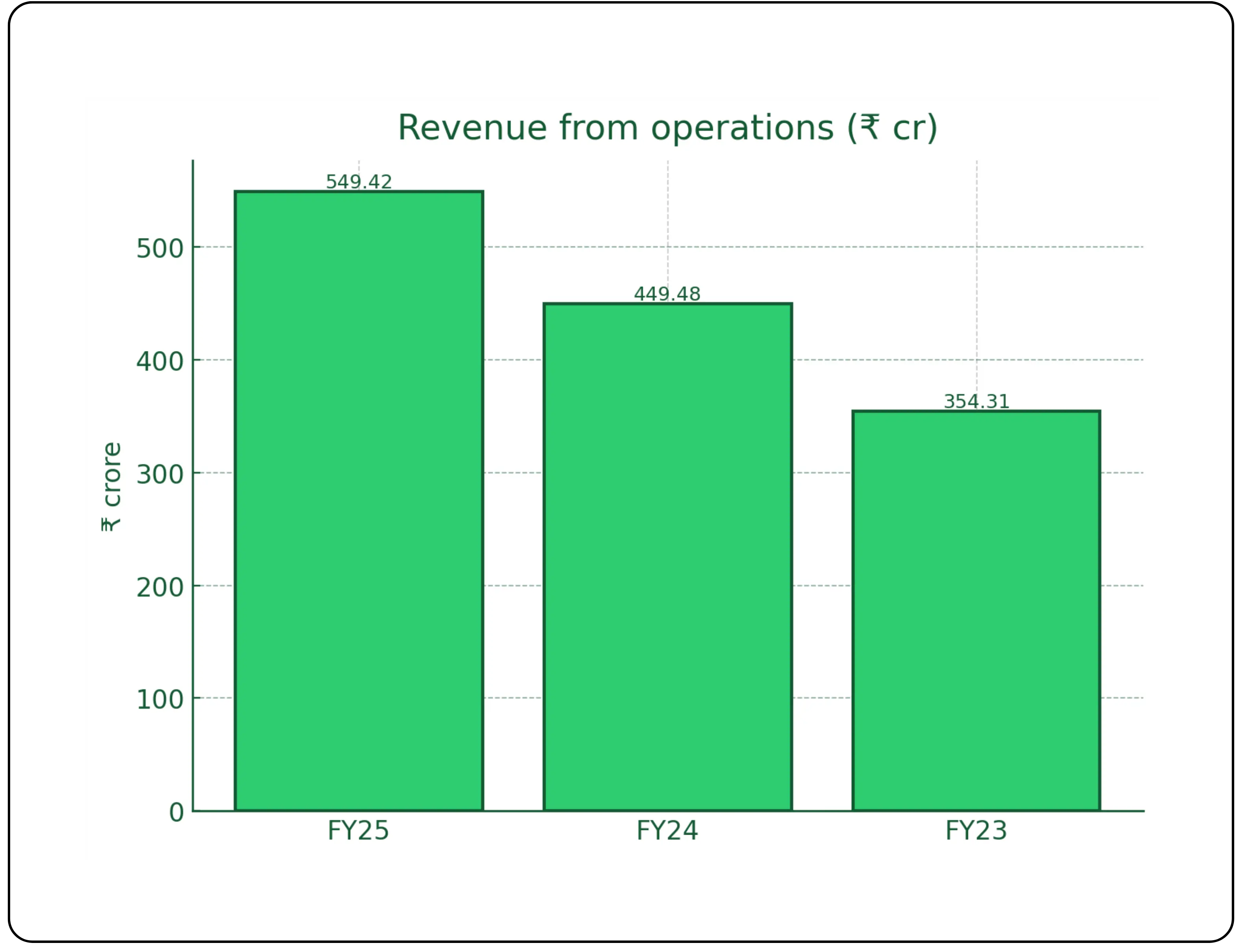

| Revenue from operations | 549.4214 | 449.4845 | 354.3088 |

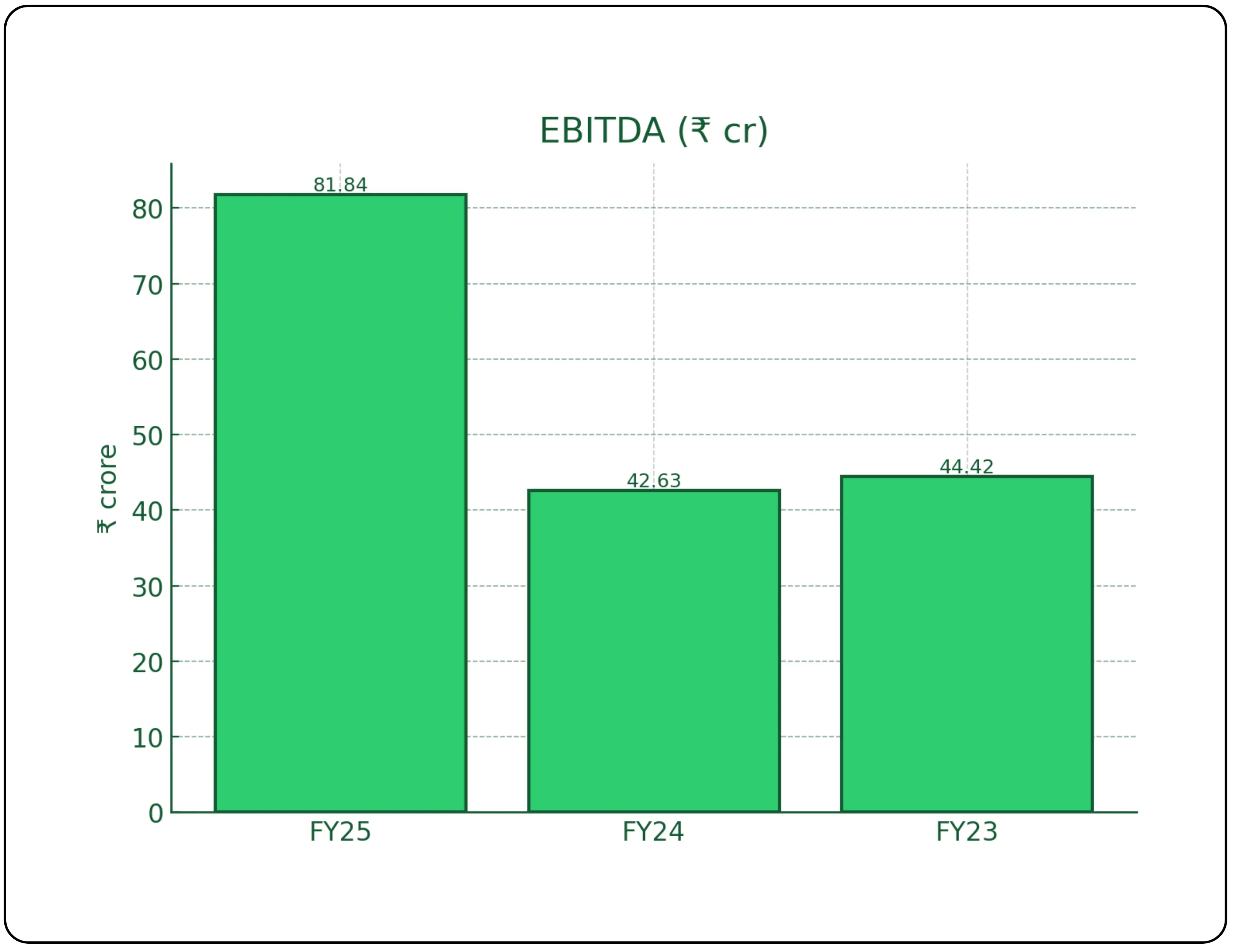

| EBITDA | 81.8409 | 42.6251 | 44.4247 |

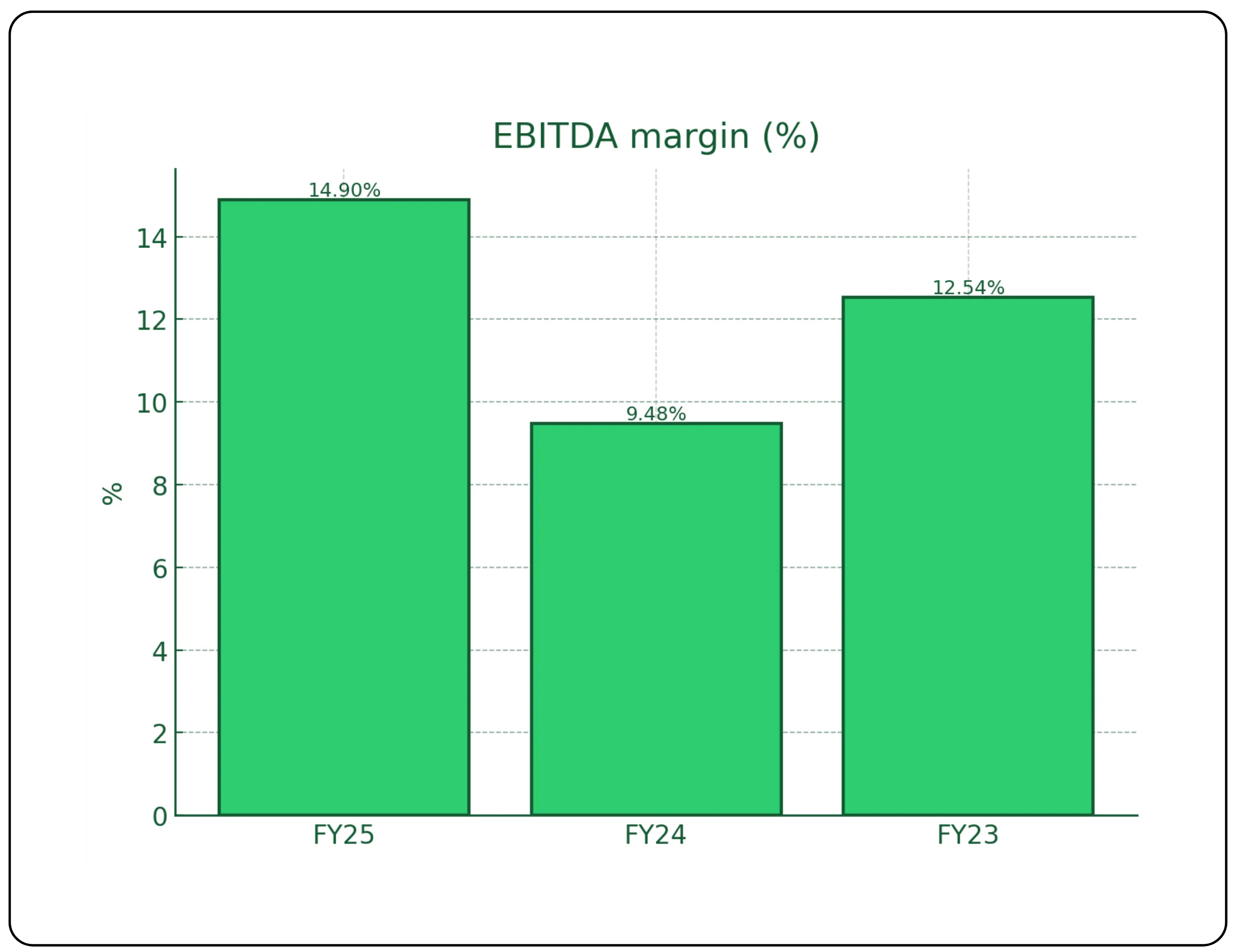

| EBITDA margin (%) | 14.90% | 9.48% | 12.54% |

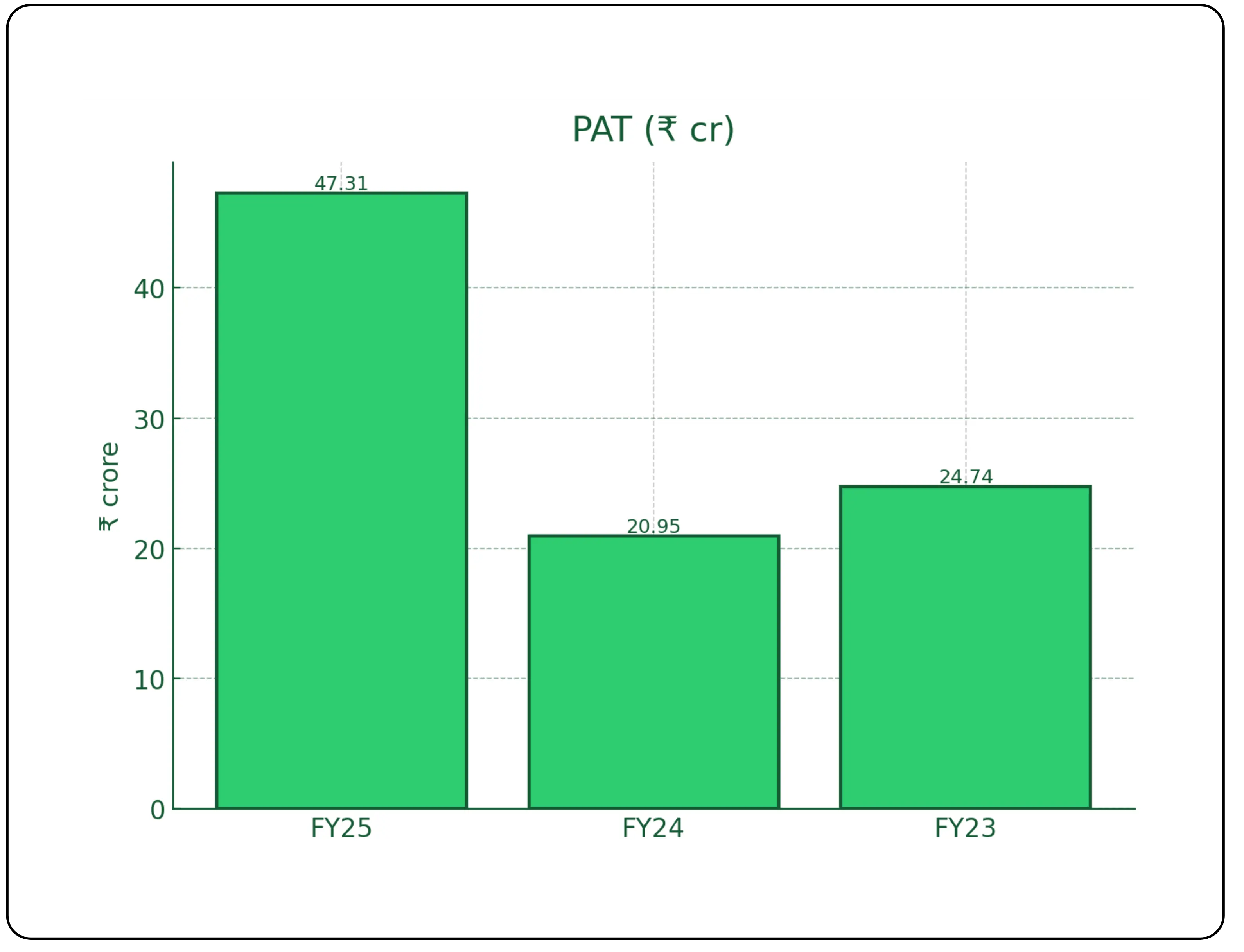

| PAT | 47.3070 | 20.9486 | 24.7381 |

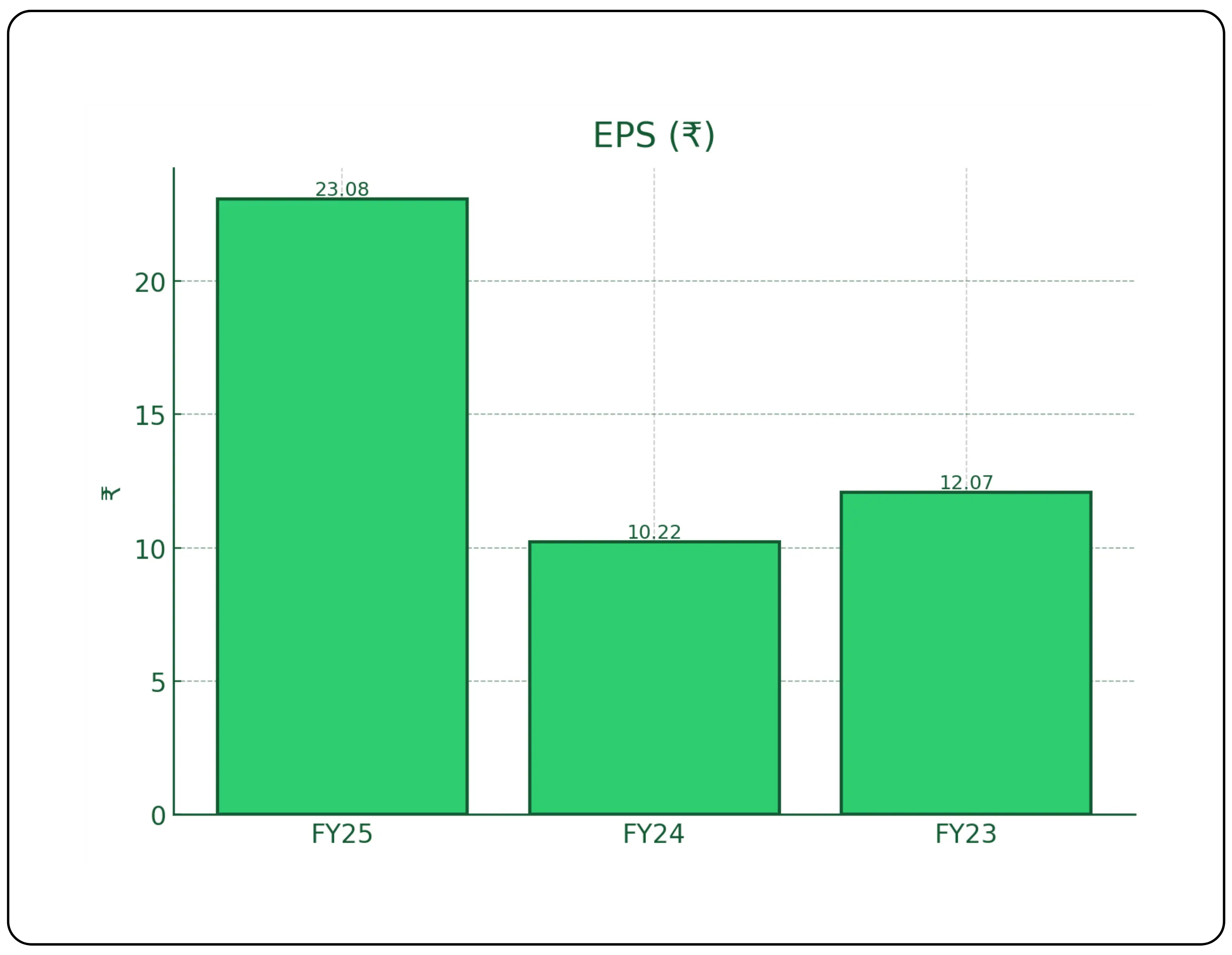

| EPS (basic) | 23.08 | 10.22 | 12.07 |

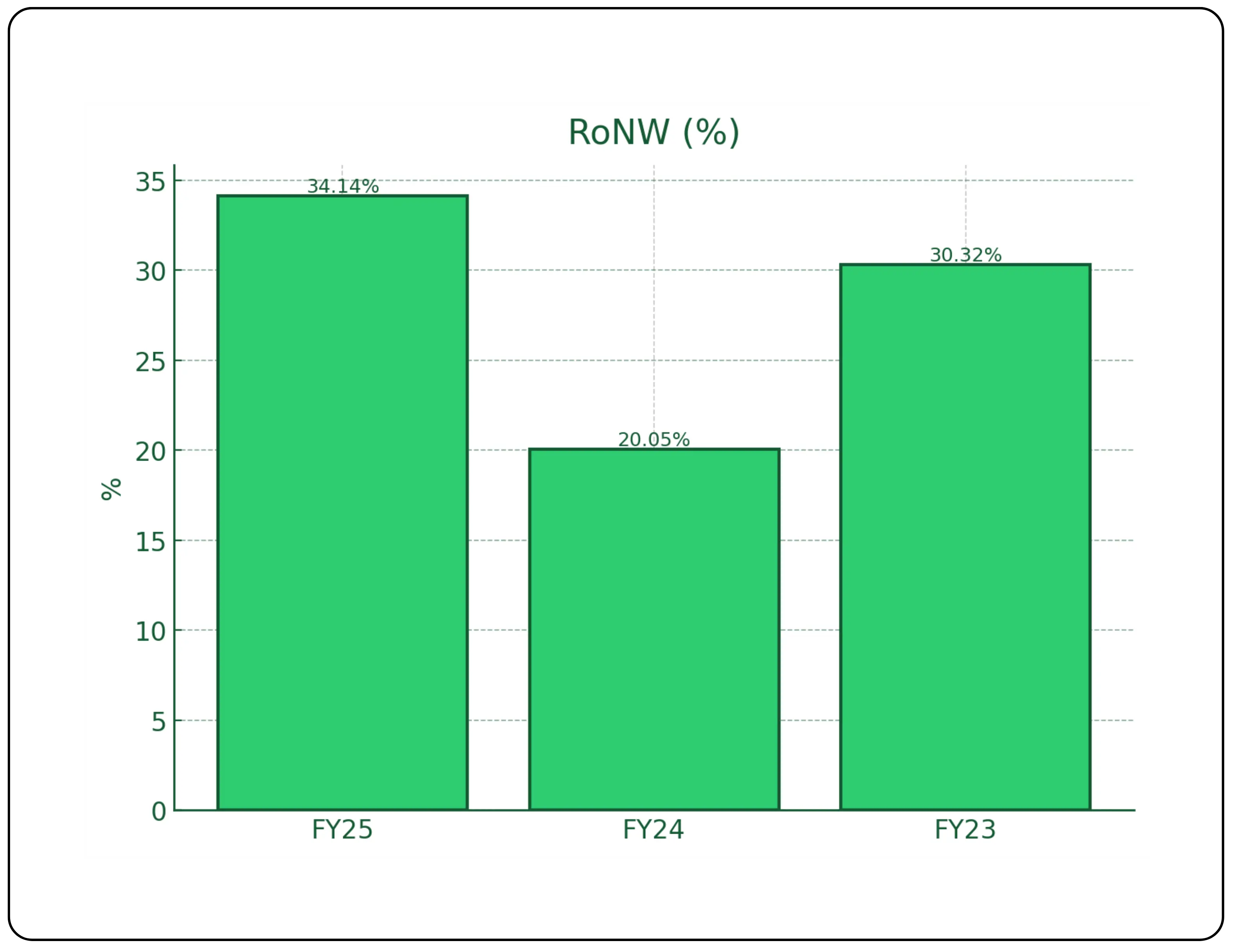

| RoNW (%) | 34.14% | 20.05% | 30.32% |

| Net worth | 162.1635 | — | — |

| Current borrowings | 137.5824 | — | — |

| Total equity & liabilities | 366.4636 | — | — |

Revenue from operations

Revenue reached ₹549.42 cr in FY25, up 22.23% YoY from ₹449.48 cr after a 26.86% rise in FY24. Over two years, revenue is higher by ₹195.11 cr versus FY23, showing solid expansion.

EBITDA

EBITDA jumped to ₹81.84 cr in FY25, a 92.00% YoY increase from ₹42.63 cr. FY24 had dipped 4.05% versus FY23, so FY25 marks a sharp rebound.

EBITDA margin

Margin improved to 14.90% in FY25 from 9.48% in FY24, a +5.42 pp expansion. It is also +2.36 pp higher than FY23 (12.54%), indicating better operating leverage.

PAT

PAT rose to ₹47.31 cr in FY25, up 125.82% YoY from ₹20.95 cr. This more than offsets the 15.32% decline seen in FY24 versus FY23.

EPS (basic)

EPS increased to ₹23.08 in FY25, a 125.83% YoY jump from ₹10.22. FY24 had fallen 15.33% versus FY23, so the FY25 print signals strong earnings recovery.

RoNW

RoNW climbed to 34.14% in FY25, up 14.09 pp YoY from 20.05%. It is also 3.82 pp above FY23 (30.32%), supported by higher profitability.

(pp = percentage points is absolute difference between two percentages, 1 pp = 100 bps (basis points))

Peer Analysis

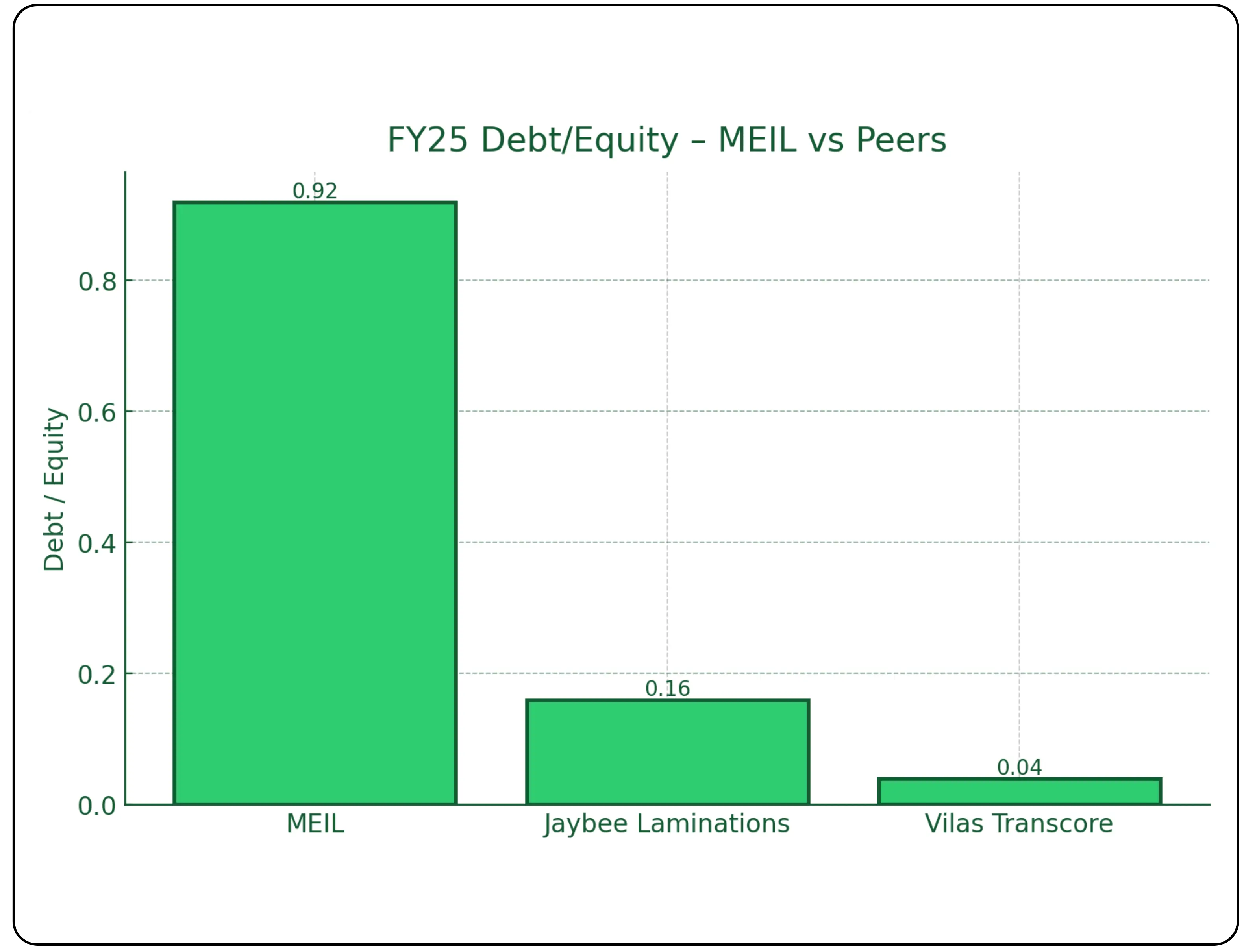

FY25 peers show MEIL at ₹54,940 lakh revenue with 15% EBITDA margin and 9% PAT margin; ROCE ~25%; RoE ~29%. Comparable component makers like Jaybee Laminations and Vilas Transcore sit at smaller toplines with similar/better margins; MEIL’s leverage (Debt/Equity 0.92) is higher than Vilas (0.04) and Jaybee (0.16).

(For FY24, MEIL’s margins (EBITDA ~10%) are mid-pack versus Amod/Vardhaman (≈11%), while ROCE trails the more asset-light stampers, see table.)

Why It Stands Out

- Utility-grade approvals & lab (NABL, PGCIL up to 400 kV, ISO) that de-risk qualification with PSUs and large EPCs.

- Full-stack offering across transformer components → transformers → EPC, aiding wallet-share and cross-selling.

- Healthy order book supporting visibility.

- Capacity expansion (Unit-IV) funded by IPO proceeds to unlock throughput and storage efficiencies.

- Its amorphous-core capability and substation EPC services align with utility and renewable energy needs for higher energy efficiency in the grid.

Strengths

- Specialization in CRGO products and advanced facilities (CTL with V-notch/dual tip-cut, Brockhaus testing).

- Marquee customer relationships across PSUs and private developers.

- Pan-India reach with export presence.

Risks

- Imported raw-material exposure (CRGO is largely imported): imported share of material cost was 24.91% (FY25), 39.07% (FY24). FX/price swings can hit margins.

- Energy intensity: significant power/fuel needs cost spikes or outages can compress profitability.

- Export competitiveness: aggressive Chinese pricing pressured certain lanes (e.g., Oman); strategy is presently domestic-tilted.

- Leasehold land at some plants, renewal/relocation risk.

- No dividends in FY23–FY25; capital is being reinvested.

Conclusion

MEIL is a transformer-component specialist expanding into higher-value assembly/transformer and EPC work, with credible approvals and PSU-grade references. Financials show strong FY25 recovery, higher revenue, margin expansion, and improved RoNW, while the IPO capital is earmarked to reduce debt and expand capacity. Imported material/energy dependence and a still-modest export mix are watch-items, but execution on Unit-IV and order-book conversion could sustain growth and operating leverage.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.