Petronet LNG Limited is India’s leading LNG infrastructure company and continues to hold its dominant position even as it navigates short-term operational challenges. With a net worth of over ₹20,000 crore and an ongoing expansion plan worth ₹30,000 crore, the company’s financial strength and its long-term vision for India’s shifting energy landscape highlight the potential for Petronet LNG long-term growth.

Founded in 1998, Petronet LNG is the country’s largest importer and regasifier of LNG. Backed by four major oil PSUs, Petronet operates the two key Dahej Kochi terminals in Gujarat (17.5 MMTPA) and Kerala (5 MMTPA), respectively. These facilities form the backbone of India’s natural gas supply network, meeting the growing energy needs of industries and households alike.

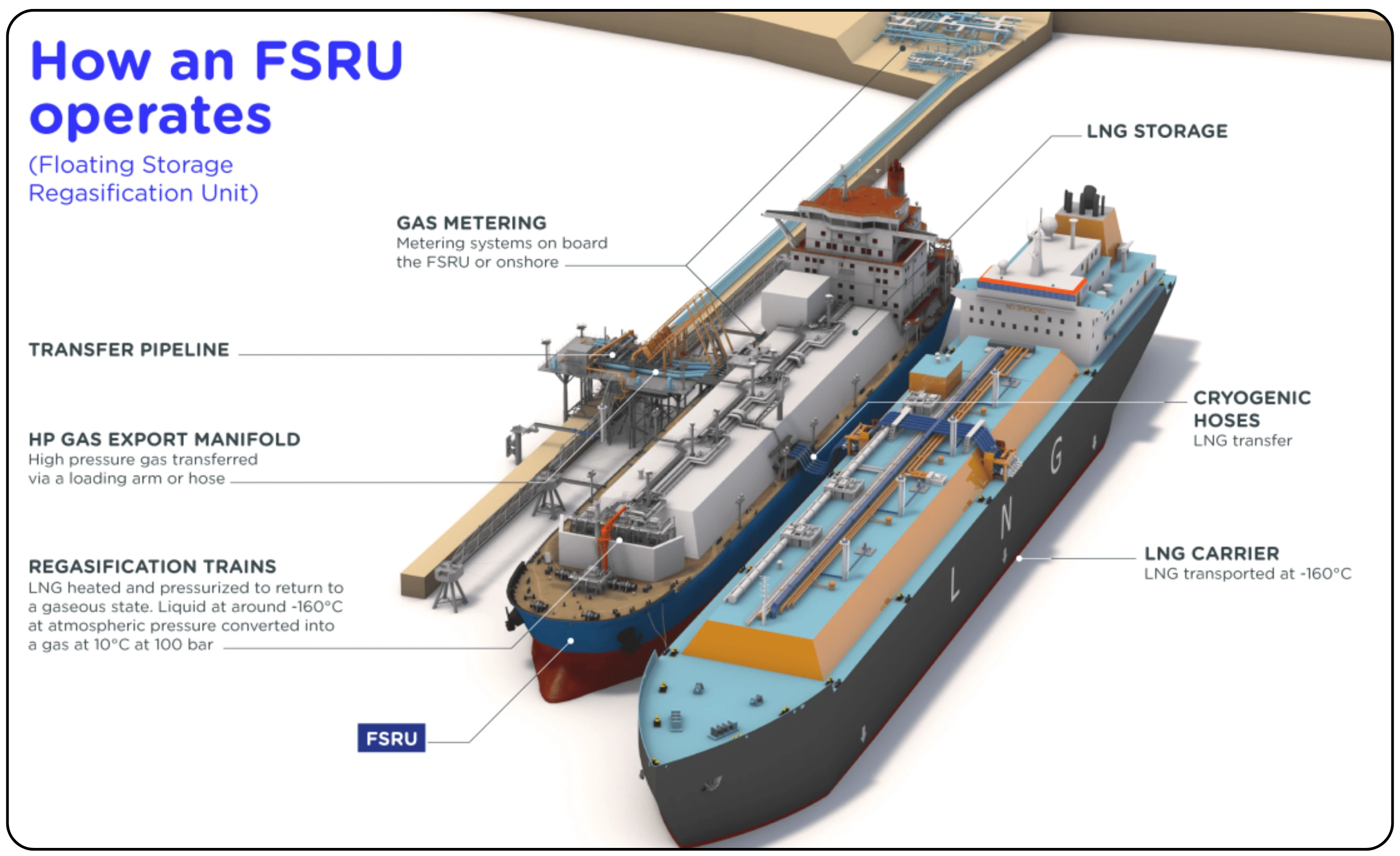

Regasification Explained

Regasification is the process of converting liquefied natural gas (LNG) back into its gaseous form so it can be used as fuel or industrial feedstock.

LNG is natural gas cooled to around –162°C, which shrinks its volume by roughly 600 times, making it easier to transport across long distances. But to be used in homes, factories, or power plants, it must be converted back into gas.

This happens at LNG terminals near ports, where the cold liquid is gently heated using specialized equipment called vaporizers. These vaporizers can use seawater, warm air, or other heat sources to safely warm the LNG. Once vaporized, the gas is fed into pipelines and distributed to end-users.

In simple terms, regasification is like warming a compact, super-cold liquid back into gas so it can be safely and efficiently used to generate energy or heat. It’s a critical step in the LNG supply chain, ensuring flexible transport and a reliable fuel supply from producers to consumers.

Petronet LNG Limited – Business Model

Petronet generates revenue through three primary streams: sale of regasified LNG, terminal usage fees, and long-term supply contracts.

Import and Regasification

The company sources LNG via long-term contracts—mainly from Qatar and Australia—and spot markets. LNG is imported to the Dahej and Kochi terminals, where it is regasified back into natural gas for distribution.

Regasified LNG Sales

Petronet earns ₹47,823 crores for sales of Regasified LNG. Regasified gas is sold directly to industrial consumers, including power plants, fertilizer units, refineries, and city gas distributors. Sales are primarily under long-term contracts, with short-term agreements supplementing volumes.

Volume Insight: Total RLNG send-out 934 TBtu (Dahej: 875 TBtu; Kochi: 59 TBtu).

Terminal Usage Fees

Petronet earns fees from domestic and international clients for using its LNG terminals. These include both fixed and variable charges for handling and regasifying LNG cargoes, providing stable, infrastructure-backed income largely insulated from commodity price swings.

Trading and Optimization

The company also engages in LNG trading and cargo swaps to optimize logistics and balance supply-demand dynamics. As India’s gas market matures, trading has become an increasingly meaningful contributor to revenue.

The Petronet LNG business model operates an integrated “import–regasify–distribute” platform, combining long-term supply security, strong infrastructure, and value-added trading operations. This model delivers predictable cash flows while positioning the company for sustainable growth in India’s expanding gas market.

Financial Performance Analysis

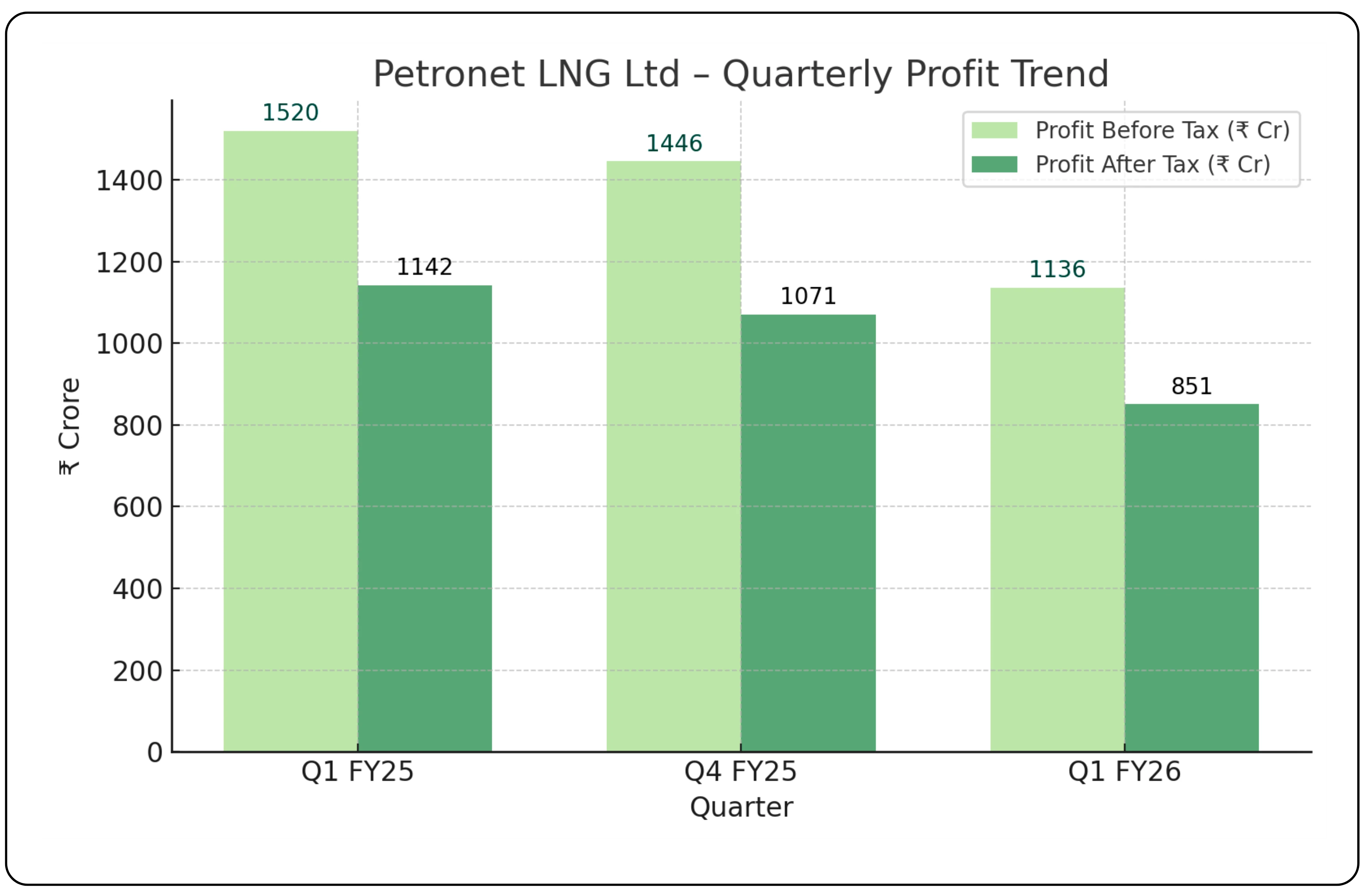

Quarterly Performance (Q1 FY26)

Petronet LNG’s Q1 FY26 results highlight a mixed quarter steady operational gains amid weaker profitability. Profit Before Tax came in at ₹1,136 crore, down 21.4% sequentially from ₹1,446 crore in Q4 FY25 and 25.3% lower year-over-year from ₹1,520 crore in Q1 FY25.

Profit After Tax stood at ₹851 crore, declining 20.5% QoQ and 25.5% YoY. The drop was largely due to muted demand from the power and fertilizer sectors, along with competition from alternative fuels and unfavorable spot-LNG price spreads.

Operationally, however, the company held its ground. Total processed volume rose to 220 TBTU up 7.3% from 205 TBTU in the previous quarter supported by stable LNG prices and higher utilization at the Dahej terminal.

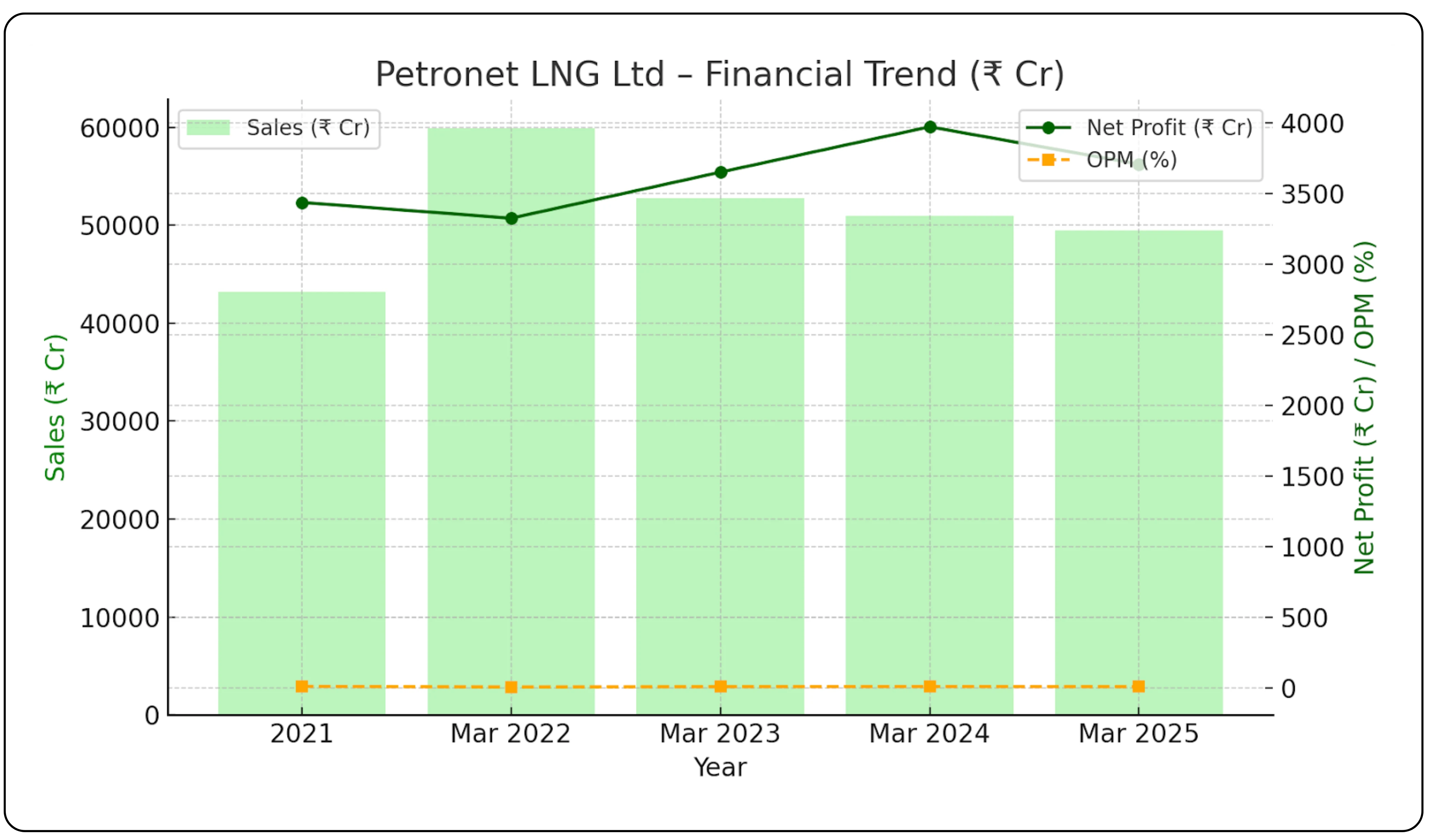

Financial Performance Trend (FY2021–FY2025)

| Year | Sales (₹ Cr) | % | Net Profit (₹ Cr) |

|---|---|---|---|

| FY2021 | 43,169 | 12% | 3,438 |

| FY2022 | 59,899 | 8% | 3,326 |

| FY2023 | 52,729 | 10% | 3,652 |

| FY2024 | 50,982 | 11% | 3,973 |

| FY2025 | 49,447 | 10% | 3,709 |

- Revenue: Sales peaked in FY2022 at ₹59,899 crore, fueled by elevated global LNG prices, before gradually easing to ₹49,447 crore in FY2025 as prices normalized.

- Net Profit: Despite top-line fluctuations, net profit remained at ₹3,709 crore.

Overall, the graph illustrates a post-FY22 revenue correction, steady profitability, and disciplined cost management, reinforcing Petronet’s strong fundamentals and consistent performance in a volatile energy market.

Balance Sheet Strength

Petronet’s balance sheet remains one of the strongest in the energy sector. Total assets grew 6.9% year-on-year to ₹26,800.93 crore in FY25, while net worth surpassed ₹20,000 crore to reach ₹20,233 crore by June 2025—a testament to its consistent earnings and prudent capital management.

The company’s debt-free position offers significant flexibility as it moves ahead with its expansion plans. With no major borrowings on the books, Petronet is well-positioned to raise its planned ₹12,000 crore term loan for upcoming projects without straining its balance sheet.

Operational Performance

Capacity Utilization

The Dahej terminal, Petronet’s flagship asset, processed 207 TBTU in Q1 FY26—up 10% sequentially, though lower on a year-over-year basis. Its strong performance reflects Dahej’s unmatched infrastructure, including five pipeline connections and a strategic coastal location that make it the preferred hub for India’s major LNG offtakers.

The Kochi terminal, on the other hand, continued to operate below optimal levels due to a 1.5-month shutdown at FACT and ongoing connectivity constraints. Utilization is expected to rise meaningfully once GAIL’s long-pending pipeline project is completed by late CY25 or early FY26, unlocking access to new industrial consumers across southern India.

Long-Term Contract Portfolio

Petronet’s long-term contract framework provides a cushion against market volatility through oil-indexed pricing and secure offtake arrangements. Its agreements with leading PSUs ensure steady cash flows and high asset utilization.

A recent supply deal with Deepak Fertilisers for 26 TBTU (minimum 1.1 MMTPA) underscores continued trust from industrial buyers. Additionally, the upcoming Gorgon Phase 2 contract—1.2 MMTPA beginning in late FY26 and ramping up over 15 years—further enhances supply visibility and supports higher utilization at the Kochi terminal.

Strategic Growth Initiatives

Gopalpur Terminal – Expanding to the Eastern Coast

Petronet is expanding its footprint to India’s eastern corridor with a ₹6,355 crore investment in the 5 MMTPA land-based Gopalpur LNG Terminal at Odisha. The company moved away from the earlier FSRU-based design to a land-based model to achieve better cost efficiency and long-term operational reliability.

The terminal will be linked through a 35 km spur line to GAIL’s Angul–Srikakulam trunk pipeline, providing access to major industrial belts, refineries, and steel clusters in Odisha and neighboring states. The management expects Gopalpur to mirror Dahej’s success as gas demand gradually shifts from the western to the eastern region of India.

Dahej Capacity Expansion

At Dahej, Petronet is scaling capacity from 17.5 MMTPA to 22.5 MMTPA. The project has seen minor delays due to the monsoon and security-related issues but remains on track for completion by the end of CY25. The upcoming third jetty, capable of handling LNG, ethane, and propane, is expected to be ready by 2027, offering greater product flexibility and throughput capacity.

Petrochemical Integration

The PDH-PP project marks Petronet’s entry into value-added petrochemicals, aligning with its long-term diversification strategy. With cumulative investments of ₹500 crore and tenders floated for most key packages, the project is progressing on schedule under the company’s broader ₹30,000 crore expansion blueprint.

Market Outlook and Industry Dynamics

Global LNG Supply Landscape

Global LNG capacity is set to expand sharply, with around 180 MMTPA of new supply expected to come online over the next three to four years. Much of this incremental capacity will cater to high-growth markets like India and China. As these new projects start operations, the resulting increase in supply is likely to narrow spot–term price gaps and make LNG more affordable. For India, that means stronger demand momentum consumption is projected to nearly double by 2028 – 30.

Domestic Infrastructure Push

India’s gas infrastructure buildout is gathering pace. Key projects such as the Nagpur–Jharsuguda, Angul–Srikakulam, and Northeast gas grid pipelines are expected to significantly improve regional connectivity and access. This national pipeline integration effort—driven by the government’s “one nation, one gas grid” vision—perfectly complements Petronet’s ongoing terminal expansion and geographic diversification strategy.

Financial Projections and Capital Allocation

Capex Program

Petronet LNG has laid out a ₹5,000 crore capex plan for FY26, covering multiple growth fronts—petrochemical integration, terminal expansions, the Gopalpur project (₹300 crore), a new corporate office (₹100 crore), and the government-mandated setup of 25 compressed biogas (CBG) plants (₹100 crore). Capex intensity is expected to rise further in FY27, backed by the proposed ₹12,000 crore term loan that will fund large-scale expansion and diversification projects.

Revenue Diversification

The LNG regasification revenue segment remains Petronet’s steady earnings base, contributing ₹643 crore in Q1 FY26. However, the company’s entry into petrochemicals opens a new, higher-margin revenue stream. This shift towards value-added products is designed to balance its portfolio, reducing reliance on the cyclical regasification business and strengthening long-term profitability.

Valuation Analysis – Scenario-Based Forward P/E Approach

Assumptions & Methodology

- Current Market Price: ₹281 per share

- FY25 EPS (TTM): ₹24.72

- Market Cap: ₹42,172 crore

- EPS Growth Guidance (Base Case): ~7.8% annually (as per management commentary and analyst estimates)

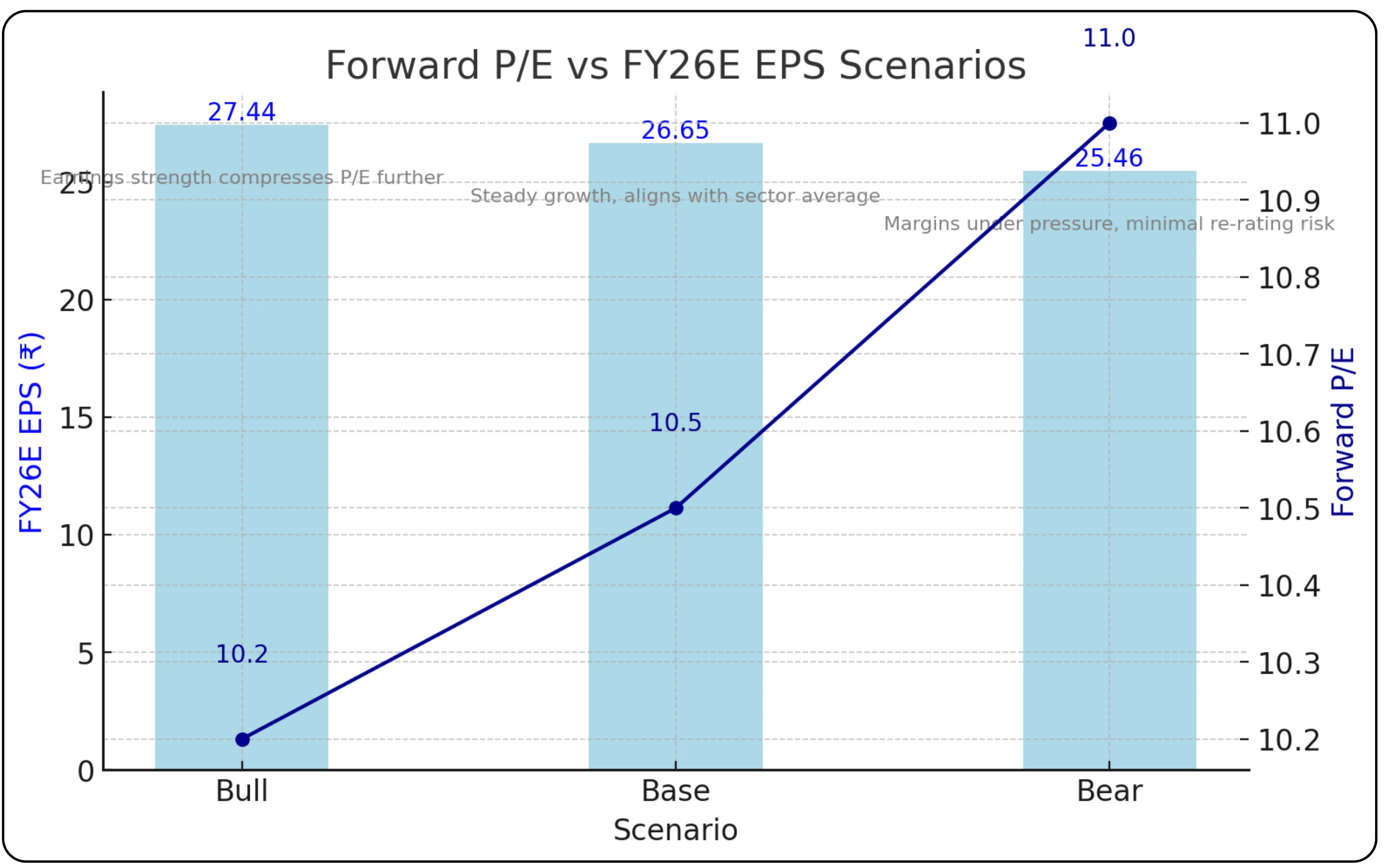

FY26E Base EPS: ₹24.72 × 1.078 ≈ ₹26.65

For scenario testing, three growth cases are used:

- Bull Case: +11% EPS growth

- Base Case: +7.8% EPS growth

- Bear Case: +3% EPS growth

Forward P/E Formula:

Forward P/E = Current Price ÷ FY26E EPS

| Scenario | FY26E EPS (₹) | Forward P/E | Observation |

|---|---|---|---|

| Bull | 27.44 | 10.2 | Earnings strength compresses P/E further |

| Base | 26.65 | 10.5 | Steady growth, aligns with sector average |

| Bear | 25.46 | 11.0 | Margins under pressure, minimal re-rating risk |

Input Summary:

- Bull: 24.72 × 1.11 = ₹27.44

- Base: 24.72 × 1.078 = ₹26.65

- Bear: 24.72 × 1.03 = ₹25.46

- Forward P/E: 281 ÷ Scenario EPS

Valuation Insights

Bull Case:

Strong execution and a volume ramp-up from new contracts could drive the Petronet share price forecast higher, with EPS potentially reaching ₹27.44. The resulting forward P/E of 10.2 still leaves the stock trading at a discount to long-term averages—indicating upside potential if sentiment toward the gas sector improves.

Base Case:

Assuming normalized growth in line with guidance, the Petronet LNG share price forecast based on FY26E EPS of ₹26.65 yields a forward P/E of 10.5. At this level, Petronet appears fairly valued but offers limited downside, supported by predictable cash flows and steady utilization levels.

Bear Case:

If demand softness persists and project timelines slip, EPS may settle at ₹25.46, implying a forward P/E of 11.0—close to the current trailing multiple. This scenario suggests stability rather than deep correction risk.

Key Takeaways

- The Petronet LNG share analysis indicates that valuation support remains intact even in a weak demand environment, thus limiting downside.

- The base case aligns with management’s 7.8% EPS growth guidance, supporting steady long-term compounding.

- The bull case hinges on higher capacity utilization, timely project execution, and margin expansion.

Overall, the Petronet LNG stock analysis based on the forward P/E framework suggests a balanced risk–reward profile. With earnings visibility, a debt-free balance sheet, and major projects nearing execution, the current valuation appears attractive for investors seeking exposure to India’s natural gas infrastructure story.

Risk Assessment

Operational Risks

Petronet faces near-term demand weakness from the power and fertilizer sectors, where cheaper alternative fuels are temporarily gaining share. The persistent gap between spot and term LNG prices has also weighed on overall volumes. However, management expects these pressures to ease as new global LNG supply comes online, stabilizing prices and improving affordability.

Execution Risks

With a ₹30,000 crore expansion program underway spanning terminals, petrochemicals, and infrastructure the company’s growth plan hinges on timely and efficient project execution. Weather-related disruptions and security constraints have already caused minor delays in some developments. Sustaining tight oversight and coordination across multiple projects will be critical to maintaining schedules and budgets.

Market and Contractual Risks

Outstanding “Use or Pay” (UoP) dues of ₹1,421.56 crore (₹952.41 crore net after provisions) reflect ongoing recovery challenges under existing contracts. Management remains confident of full realization backed by contractual rights and bank guarantees, but the timing of cash recovery remains uncertain and could impact short-term working capital flows.

Investment Thesis

The core Petronet LNG investment thesis is that the company stands out as a strong long-term play on India’s growing natural gas market. Its leadership position, steady cash flows, and clean balance sheet give it the resilience to handle short-term pressures and the flexibility to pursue growth opportunities with confidence.

The upcoming Gopalpur terminal marks a key move into the underpenetrated eastern corridor, aligning Petronet with the next phase of India’s gas demand expansion. Meanwhile, the planned petrochemical venture adds a higher-margin layer to its portfolio, reducing reliance on regasification alone.

While near-term profitability remains under pressure, Petronet’s solid fundamentals, prudent capital structure, and forward-looking strategy point to sustained value creation. The Petronet LNG stock offers a well-grounded and strategically positioned opportunity for investors looking to participate in India’s evolving energy infrastructure story.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.