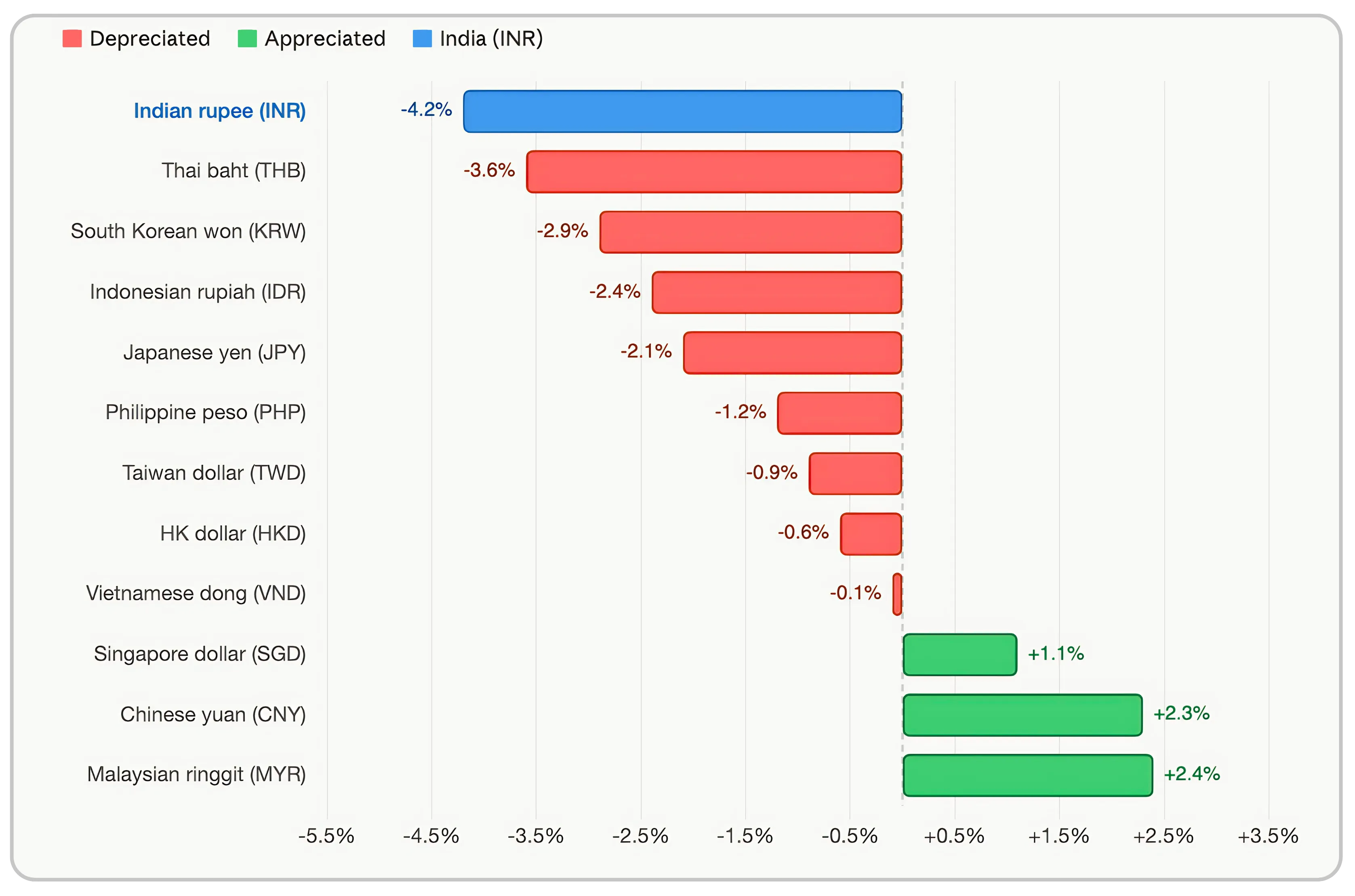

As of April 23, 2026, the Indian Rupee (INR) has reached a significant milestone, depreciating to 94 against the US Dollar. This marks a notable weakening, with the INR being identified as the worst-performing currency in Asia, having depreciated by 4.1% since January 1, 2026. This depreciation is influenced by a confluence of factors, including global geopolitical tensions, particularly the US-Iran ceasefire extension, and domestic economic indicators such as a persistent trade deficit and foreign institutional investor (FII) outflows. A weaker domestic currency typically presents a dual impact on an economy, offering advantages to exporters while simultaneously increasing the burden on importers.

ASIAN CURRENCIES' PERFORMANCE AGAINST THE USD

Why ₹94 is a number every Indian investor must understand

The Indian Rupee's slide to 94 per US Dollar on April 23, 2026 isn't just a forex footnote — it's a market-moving event that's quietly reshaping your equity portfolio, your SIP returns, and the cost of your next international trip. India has officially become Asia's worst-performing currency of 2026, down 4.1% since January 1. This isn't a single-cause story. It's a perfect storm: a stubbornly strong US Dollar, Iran-US ceasefire uncertainty sending crude oil bids higher, relentless FII outflows from Indian equities, and a structural trade deficit that refuses to narrow. The RBI is fighting back — but the rupee is losing ground.

What's actually driving the Rupee down?

Global Headwinds

The US Federal Reserve's higher-for-longer rate stance continues to prop up the Dollar globally, making emerging market currencies — including the INR — structurally weaker. Add the Iran-US ceasefire extension stoking crude oil uncertainty, and you have a recipe for sustained rupee pressure. Capital is fleeing to safe havens: USD, gold, US Treasuries.

Domestic Vulnerabilities

India's merchandise trade deficit hit a staggering $333.19 billion in FY26 — reflecting the structural gap between what we export and what we import. FII outflows have been relentless, pulling dollar demand away from Indian assets. Meanwhile, inflation has reduced the real yield advantage that once attracted foreign capital.

“The J-Curve Effect: In the short run, rupee depreciation actually worsens the trade deficit before improving it — imports cost more immediately, but export volumes take 6–18 months to respond. We're currently in the painful first phase of this curve.”

Sectors celebrating a weaker rupee – The Exporters

India's total exports reached $860.09 billion in FY 2025-26, growing 4.22% year-on-year. A weaker rupee is a natural tailwind for these segments — every dollar earned translates to more rupees at home.

Information Technology (IT) Sector

The Indian IT sector is among the greatest beneficiaries of rupee depreciation. With the majority of revenues in USD and a predominantly INR cost base (salaries, infrastructure), a weaker rupee mechanically improves margins. However, analysts caution that while rupee depreciation improves reported earnings optics, it does not reflect underlying business growth. The sector has faced headwinds in Q4 FY26 from AI-driven disruption of traditional service models and cautious enterprise IT spending globally. Major players such as HCL Tech reported below-expectation results, and Infosys and TCS have signaled moderated growth guidance for FY27.

Pharmaceutical Sector

India's pharmaceutical industry — the world's largest supplier of generic medicines — is a natural beneficiary of INR depreciation. With over 50% of revenues from exports (primarily to the US and Europe), pharma companies see meaningful margin expansion when the rupee weakens. Additionally, Indian pharma is increasingly diversifying into branded generics in emerging markets (Africa, Latin America, Southeast Asia), which further amplifies the revenue benefit from a weaker INR. Key companies to watch include Sun Pharma, Dr. Reddy's Laboratories, Cipla, and Aurobindo Pharma.

Textile and Apparel Sector

India's textile and apparel industry employs over 45 million people and is the country's second-largest export earner. A weaker rupee enhances the price competitiveness of Indian garments and fabrics versus competitors like Bangladesh, Vietnam, and Cambodia — all of which have relatively stable currency dynamics. This can drive incremental order wins, particularly from global fashion retailers looking to diversify their manufacturing base away from China. Key export destinations include the USA (27%), EU (22%), and the UAE (12%).

Agriculture and Processed Food Exports

India is a major exporter of rice, spices, marine products, and processed foods. Rupee depreciation boosts the competitiveness of these commodities in global markets. Rice exports, in particular, have benefited from both rupee weakness and elevated global prices triggered by climate-related supply disruptions in competing nations such as Thailand and Vietnam. Basmati rice exports grew significantly in FY26, with the weaker INR acting as a natural price hedge against global competition. Spice exports to the Middle East and Southeast Asia also showed positive momentum.

Who's getting squeezed – The Importers

India's imports hit $979.40 billion in FY 2025-26 (April-March), growing faster than exports at 6.47% YoY. This structural imbalance means a weaker rupee has a larger negative impact than positive — the import bill pain outweighs the export gain in absolute rupee terms. While exporters benefit, a depreciating rupee substantially increases the cost of imports. Indian importers must spend more rupees to purchase the same foreign currency, raising input costs, squeezing margins, and feeding through to consumer prices.

Oil and Energy Sector

India imports approximately 85-90% of its crude oil requirements, making the energy sector acutely sensitive to rupee depreciation. For every 1 rupee depreciation against the dollar, India's annual oil import bill rises by approximately Rs 10,700 crore (roughly US$ 1.14 billion at current rates). With the INR at 94 versus ~89 at the start of FY26, the incremental import cost burden is estimated at Rs 50,000+ crore for the full year. This has downstream consequences: oil marketing companies (OMCs) like HPCL, BPCL, and Indian Oil face margin compression, and retail fuel prices (petrol, diesel, LPG) come under upward pressure. Higher energy costs cascade into transportation, manufacturing, and agricultural costs, with broad inflationary implications.

“Every Rs 1 depreciation against USD adds approx. Rs 10,700 crore to India’s annual crude oil import bill. At 94 vs the 89 level in January 2026, the incremental burden is approx. Rs 50,000 crore+.”

Electronics and Capital Goods

India remains heavily dependent on imports for electronics (semiconductors, displays, motherboards), capital machinery, and industrial equipment. The rupee's depreciation increases the landed cost of these products, affecting both consumer electronics prices and manufacturing competitiveness. Smartphone prices, for instance, are sensitive to INR movements given that most components (chips, OLED panels) are imported from Taiwan, South Korea, and China. The ongoing PLI (Production Linked Incentive) scheme for electronics is gaining relevance as a policy tool to reduce import dependence over the medium term, but short-term vulnerability remains high.

Edible Oil and Pulses

India imports significant quantities of edible oils (palm oil from Indonesia/Malaysia, sunflower oil from Ukraine/Russia) and pulses from Australia, Canada, and Myanmar. Rupee depreciation raises retail prices for these essential food commodities, disproportionately affecting lower and middle-income households.

Fertilizers and Agricultural Inputs

India is a large importer of potash and diammonium phosphate (DAP) fertilizers. A weaker rupee inflates the subsidy burden for the government (which subsidizes fertilizer for farmers), potentially widening the fiscal deficit. Fertiliser subsidy expenditure in FY26 has already exceeded the revised estimates by February, indicating a likely overshoot by year-end, driven by higher global fertiliser prices and rupee depreciation.

Sectoral Impact Summary

| Sector | Type | Impact |

|---|---|---|

| IT / Software Services | Exporter | Positive |

| Pharmaceuticals | Exporter | Positive |

| Textiles & Apparel | Exporter | Positive |

| Agriculture / Rice | Exporter | Positive |

| Crude Oil / Energy | Importer | Negative |

| Electronics & Semiconductors | Importer | Negative |

| Edible Oils & Pulses | Importer | Negative |

| Fertilizers | Importer | Negative |

| Aviation | Importer (fuel/leases) | Negative |

The bigger picture: inflation, deficit, RBI response

Inflation Pass-Through

The RBI estimates that a 5% rupee depreciation adds 40 basis points to inflation. With INR already down 4.1% YTD, the inflation transmission is happening right now.

RBI's Balancing Act

India's forex reserves stand at approximately $700.9 billion — adequate buffer but not unlimited ammunition. The RBI has been selling dollars to smooth volatility, but the priority is preventing disorderly moves, not defending a specific level. A rate cut cycle, if pursued, could widen the INR-USD rate differential further and add depreciation pressure.

Fiscal Implications

India’s external debt, which stood at $765.5 billion as of December 2025, becomes more expensive to service whenever the rupee weakens against the US dollar. A weaker rupee raises the cost of interest payments and principal repayments on foreign currency debt, especially for government-linked obligations and sectors dependent on external borrowing.

Conclusion

The depreciation of the Indian Rupee to 94 against the US Dollar is both a symptom and a catalyst. As a symptom, it reflects India's structural trade imbalances, energy import dependency, and sensitivity to global capital flows. As a catalyst, it reshapes the competitive dynamics of key industries, creating winners and losers in the corporate landscape. Export-oriented sectors — IT, Pharmaceuticals, Textiles, and Agriculture — stand to gain from improved dollar revenue realizations and global price competitiveness. Import-heavy sectors — Energy, Electronics, Edible Oils, and Fertilisers — face margin compression, cost inflation, and fiscal challenges. The policy response must be multi-layered: the RBI can smooth volatility, but structural remedies require sustained investment in domestic manufacturing, export diversification, and energy transition. India’s long-term economic ambitions — becoming a US$ 10 trillion economy by 2035 — will require a currency that is competitive but not chronically weak. Ultimately, navigating the INR's depreciation calls for coordinated macroeconomic stewardship — monetary prudence from the RBI, fiscal discipline from the government, and strategic adaptability from India’s corporate sector.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)