India is the second largest producer and consumer of tea globally and ranks among the top ten coffee producing nations. The Indian tea and coffee sector is one of the largest organized employers of rural labor and a critical pillar of India's broader beverage sector. India produced 138 crore kgs of tea in the calendar year 2025, a roughly 5% increase over 130 crore kgs in CY2024. Assam remained the single largest producing state, contributing 50% of national output. North India accounted for 83% of total output, while South India contributed 23 crore kgs. The Indian tea market in 2025 is estimated at approximately $11 to $12 billion (USD), and the Indian coffee market in 2025 is projected to grow in line with the global expansion of the instant and specialty coffee segments.

The global coffee market is estimated at approximately $177 billion in 2025 (per Mordor Intelligence), with projections ranging between $186 billion and $249 billion by 2026. The market is expected to grow at a CAGR of approximately 5% to 6% through the end of this decade. Global coffee production for 2024-25 reached an estimated 17.75 crore bags (up 5.2% YoY per ICO data), while consumption stood at 17.51 crore bags (up 1.4%), resulting in a surplus of 24 lakh bags, the first positive global balance since 2021-22. The expected record 2026 to 27 Brazilian coffee harvest is projected to maintain this surplus, while Vietnam's dominance in Robusta processing continues to shape global instant coffee supply chains, with Indian processors benefiting from similar cost-structure advantages.

India's domestic tea market is estimated at approximately $11 to 12 billion (USD) in 2025, with the organized and branded segment continuing to gain share from unorganized players. The branded tea market has been growing steadily, driven by consumer preference for quality assurance, hygiene, and premiumization.

Production Dynamics and Supply Structure

One of the most consequential structural shifts in India's tea production landscape over the past two decades has been the rise of Small Tea Growers in India. As of March 2024, 2,47,887 registered STGs contribute 53.42% of India's total tea production (per Ministry of Commerce data), up from approximately 7% in 1991. In Assam, 1,33,626 STGs contribute 47.25% of state production. Assam tea production continues to be the backbone of national output, but the quality inconsistency from the STG segment often pulls down average auction prices and places competitive pressure on organized plantation companies.

The organized sector (comprising large estates and corporate groups) operates at the other end of the spectrum: higher overheads, labor compliance costs, and estate maintenance expenses, but with the advantage of quality control, brand building capability, and access to premium markets.

On the coffee side, India's relevance lies primarily in the instant coffee processing segment. The country's green coffee production is modest by global standards, but Indian processors (particularly in the freeze-dried and spray-dried instant coffee segments) have carved a significant niche as contract manufacturers for global brands. India and Vietnam together serve as key low-cost manufacturing bases for the global instant coffee trade.

Demand Trends: Premiumization, Branded Tea, and India's Growing Coffee Cafe Culture

Several durable demand drivers support long-term consumption growth in both tea and coffee.

In tea, domestic consumption remains the primary growth engine. The shift from loose tea to packaged tea in India is accelerating, particularly in semi-urban and rural markets. This transition is driving the growth of branded tea in India, as consumers increasingly associate packaged formats with quality assurance and hygiene. The India tea premiumization trend is equally visible: consumers are trading up from basic CTC blends to specialty tea, orthodox, and single-origin varieties, creating a new growth layer above the mass market. India's FMCG tea segment, led by Tata Consumer Products and Hindustan Unilever, continues to expand distribution to capture this shift.

The premiumization trend is visible across both categories. In tea, consumers are trading up from basic CTC blends to specialty, orthodox, and single-origin varieties. Tata Consumer Products, the industry's largest branded player, reported that its "Growth Businesses" (including NourishCo, Tata Sampann, Tata Soulfull, Capital Foods, and Organic India) surpassed ₹1,000 crore in quarterly revenue in Q3 FY26 (growing 29% YoY) and now contribute 30% of India business revenue (up from 6% in FY20 and 28% in FY25). This underscores how the broader beverage and food portfolio is expanding well beyond traditional tea.

In coffee, India's growing coffee cafe culture is one of the most visible demand shifts of the past decade. The proliferation of café chains, rising exposure to Western lifestyles among younger demographics, and the expanding ready-to-drink (RTD) beverages segment are creating new consumption occasions that extend well beyond traditional South Indian filter coffee households. CCL Products noted that India's coffee market is expanding beyond its traditional South Indian base into Western and Northern India, driven by modern trade and e-commerce channels. India coffee premiumization, mirroring the global specialty coffee movement, is creating demand for single-origin, cold brew, and freeze-dried formats at accessible price points.

Export markets continue to strengthen. In instant coffee, over 90% of CCL Products' TTM revenue of ₹4,069 crore is derived from exports to more than 100 countries, and global demand for instant and specialty coffee continues to grow.

India Growth Outlook

India's position as the world's fastest growing major economy provides a favorable macro backdrop for the tea and coffee sector. With GDP growth projected at 6.5% (RBI, FY2025-26) and a young, consumption-oriented population, the structural case for domestic beverage consumption growth remains intact.

The organized branded tea market is expected to continue gaining share from the unorganized segment, driven by distribution expansion, rising brand awareness, and improving accessibility through e-commerce. Tata Consumer Products remains the second largest branded tea player in India, with less than 1% volume gap and approximately 4% to 5% value gap separating it from market leader Hindustan Unilever (as of September 2025). E-commerce now contributes 13% of Tata's India sales. The company is aggressively expanding rural distribution to close this gap.

In coffee, CCL Products' branded retail business (under Continental Coffee) is on track to generate approximately ₹430 to 440 crore in FY26 revenue, growing at 40% to 50% annually. Branded sales offer 1.5x to 2x gross margins relative to bulk B2B exports, making this segment a key strategic lever for improving overall EBITDA per kilogram.

The broader shift toward health and wellness beverages, coupled with the expansion of out-of-home consumption (cafes, QSRs, workplaces), adds further momentum to coffee penetration in Indian urban markets.

Pricing, Commodity Dependence, and Cyclicality

The tea and coffee sector is inherently tied to commodity cycles, weather patterns, and auction market dynamics. Understanding this is central to evaluating industry profitability.In tea, the auction system remains the primary price discovery mechanism. The all-India average tea auction price for 2025 stood at approximately ₹187 per kg, compared to around ₹199 per kg in 2024, reflecting a decline of about 6% year-on-year. However, this broad trend masks significant variation within the market. Premium Assam teas sold through the Guwahati Tea Auction Centre (GTAC) continued to command higher realizations, averaging close to ₹227 per kg, highlighting the persistent demand for quality even in a softer pricing environment. The market remains selective: high quality orthodox and specialty teas continue to command premiums, while lower quality CTC teas face downward pressure from increased STG volumes and competition from Kenyan and Nepalese imports.

In coffee, green bean prices (both Robusta and Arabica) are the key input variable. Arabica futures peaked above US$4.40/lb in 2025 before retreating to the US$2.80 to 3.00/lb range by early April 2026, driven by expectations of a record 2026-27 Brazilian harvest. Despite the improved crop outlook, prices remain volatile due to geopolitical shipping route disruptions and elevated freight costs. However, a critical distinction exists in the coffee processing business model: companies like CCL Products operate on a cost-plus pricing basis, meaning per-kilogram EBITDA is largely insulated from fluctuations in raw material costs. CCL's EBITDA per kg has improved to the ₹135 to 140 range, and the company targets 25% EBITDA growth for FY26. This model provides significantly more margin stability compared to tea plantation companies, which bear the full brunt of auction price movements against largely fixed cost structures.

Cyclicality in tea is pronounced. Plantation companies face a unique cost rigidity problem: labor, estate maintenance, and social overhead costs remain largely fixed regardless of crop output, which is highly weather-dependent. A poor monsoon or extended dry spell can simultaneously reduce crop volumes and lower realized prices, creating a double margin squeeze. This dynamic was visible in Q3 FY26, where Jay Shree Tea's EBITDA margin contracted sharply to 4.0% (from 14.2% in Q3 FY25) as margins came under pressure despite a 25.7% rise in revenue, and Peria Karamalai's TTM profitability hovered near breakeven despite improved quarterly operating margins.

Also Read: Samhi Hotels Limited - A Fundamental Analysis of the Turnaround Case

Government Policy and Regulatory Environment

The Tea Board of India regulates production standards, promotes exports, and supports sustainability initiatives such as the Trustea certification program, which improves the global positioning of Indian teas in premium and ethical sourcing markets. Trustea certification has become increasingly important as European and other developed-market buyers tighten sustainability and traceability requirements for imported teas.

In Assam, the state government introduced relief measures from January 2023 to December 2025, including withdrawal of the green leaf cess, exemption from agricultural income tax, and interest subvention on loans. With these benefits now expired, the industry is awaiting clarity on any extension. Their withdrawal could increase cost pressures for plantation companies in India’s largest tea-producing region.

Labour regulation remains a key variable. Tea plantations operate under the Plantation Labour Act, which mandates housing, healthcare, and other social benefits for workers. Wage costs have been rising steadily, and the eventual implementation of the Code on Wages (2019) could further increase operating costs for organized players.

On the coffee side, export-oriented companies benefit from schemes such as RoDTEP and SEZ incentives. While not directly linked to tea or coffee, the ethanol blending program has supported diversified players like Jay Shree Tea through its sugar business.

Geographical Distribution

The Indian tea industry is divided across two distinct regions with different dynamics. North India, including Assam and West Bengal, dominates production, accounting for roughly 83% of total output. Assam alone remains the largest contributor. This region primarily produces CTC tea, which caters to domestic consumption. Darjeeling, though small in volume, occupies a premium niche with GI-tagged teas that command higher prices globally. Darjeeling, though small in volume, produces GI-tagged teas that command significant premiums in global markets. Darjeeling tea exports remain a flagship for Indian premium tea in Europe and Japan, where orthodox leaf teas continue to attract strong demand.

South India, covering Tamil Nadu, Kerala, and Karnataka, contributes the remaining share and is more export-oriented. South India tea production has been relatively weaker in recent periods, partly due to labor scarcity and erratic rainfall. Estates in the Nilgiris and Valparai focus more on orthodox teas, which typically achieve better realizations in international markets.

In coffee, cultivation is concentrated in Karnataka, Kerala, and Tamil Nadu, while India's coffee processing infrastructure has a wider footprint. Companies like CCL Products operate facilities in India and Vietnam, leveraging cost advantages and proximity to major Robusta-producing regions. Vietnam coffee processing, particularly for freeze-dried formats, has become a competitive advantage for Indian companies with cross-border manufacturing presence.

Internationally, the competitive landscape includes Kenya (through the Mombasa auction), Vietnam (a dominant force in Robusta coffee, and a key production base for Indian processors like CCL Products), and Sri Lanka (which has partially recovered from its 2022 production collapse). Brazil's projected record 2026-27 coffee harvest is expected to meaningfully alter global supply dynamics.

Challenges and Risks

Several structural challenges confront the industry. Labor availability is declining across tea-growing regions, as younger generations increasingly migrate to urban centers. This remains particularly acute in South India, where Peria Karamalai continues to flag a "dwindling labour force" as a major concern. Climate change is manifesting as erratic rainfall patterns, prolonged dry spells, extreme heat events, and increased pest and disease incidence. South India's tea production decline of approximately 14% in early 2025, contrasting with North India's 14% increase, illustrates how climate volatility is creating increasingly divergent regional outcomes.

For plantation companies specifically, the gap between input cost inflation (fertilizers, fuel, labor) and auction price movements remains the key profitability variable. The 6% decline in all India auction average prices, even as production costs continued to rise, underscores the ongoing margin squeeze. Sharp margin compression seen in companies like Jay Shree Tea and McLeod Russel's TTM net loss of ₹225 crore exemplify how this dynamic plays out at the company level.

The coffee segment faces a different set of risks: concentration of sourcing in climate-sensitive regions (Brazil and Vietnam account for a disproportionate share of global supply), geopolitical disruptions affecting shipping routes and freight costs (the Strait of Hormuz disruption has elevated logistics costs in 2025-26), currency fluctuations affecting export realizations, and the challenge of building retail brands in a market dominated by large FMCG incumbents.

Long-term Tailwinds

The tea and coffee industry in India benefits from several long-term structural tailwinds. Rising incomes and urbanization expand the addressable market. Health and wellness trends favor both tea (antioxidants, functional blends) and coffee (energy, alertness). The premiumization trajectory supports improving price realizations over time. Although the global coffee market returned to a modest surplus of 2.4 million bags in 2024-25 (production of 177.5 million bags versus consumption of 175.1 million bags), long-term supply constraints from climate change in key producing regions and rising global consumption (particularly in Asia Pacific) continue to support a structurally favorable pricing environment for processors.

However, these tailwinds are unevenly distributed. Large branded FMCG companies (like Tata Consumer Products) and value-added processors (like CCL Products) are better positioned to capture these trends than traditional plantation companies, which remain exposed to commodity cycles, weather risk, and labor cost inflation. The structural shift toward STGs continues to erode the competitive position of organized estate companies in the mass-market CTC category, and only those plantations that successfully pivot toward quality differentiation, orthodox tea, or organic certification are likely to sustain acceptable margins over the long term.

Also Read: Evaluating India's Cement Industry Amid Structural Tailwinds

Competitive Landscape

The competitive landscape in India’s tea and coffee sector is clearly divided between branded FMCG players, processors, and plantation companies. Branded companies create value through sourcing, blending, and distribution. Processors focus on value addition and exports, while plantation companies remain directly exposed to agricultural output and commodity pricing. This structural divide is central to understanding differences in profitability and valuation across the sector.

Tata Consumer Products Ltd (TCPL)

Tata Consumer Products’ competitive moat rests on a multi-brand portfolio (Tata Tea, Tetley, Tata Coffee, Eight O'Clock Coffee) supported by deep distribution reach and cross-selling across beverage and food categories. The company has aggressively diversified beyond tea into what it calls "Growth Businesses" now contributing 30% of India business revenue, up from just 6% in FY20. E-commerce accounts for 13% of India sales. Its partnership with Starbucks (a 50:50 JV) gives it a presence in the premium out-of-home coffee segment. TCPL operates as a pure FMCG business with no plantation exposure, meaning it sources tea and coffee as commodities and adds value through branding, blending, and distribution.

When comparing Tata Consumer Products and CCL Products as investment options, the distinction is fundamental: Tata Consumer Products is an FMCG company with diversified revenue streams, brand leverage, and domestic consumption exposure, while CCL Products is a B2B and B2C processor with global export dependency and a cost-plus margin model. Both represent structurally superior alternatives to plantation companies, but they serve different investor profiles.

CCL Products (India) Ltd

CCL Products occupies a unique position as one of the top 3 coffee brands in India and one of the world's largest instant coffee manufacturers. Its business model is fundamentally different from plantation companies: CCL is a processor and exporter that converts green coffee beans into spray-dried and freeze-dried instant coffee, primarily for B2B customers (white-label supply to global FMCG brands) across more than 100 countries, with over 90% of revenue from exports. The company operates manufacturing facilities in India and Vietnam (the latter being the largest freeze-dried plant in that country), providing both cost advantages and sourcing flexibility across the two largest Robusta-producing nations. Its cost-plus pricing model, a critical structural advantage over tea plantations. CCL has also been building a domestic B2C brand ("Continental Coffee"), targeting ₹430 to 440 crore in branded revenue for FY26 through an expanding retail footprint of 140,000 outlets.

What drives CCL Products' export revenue is a combination of long-term B2B supply contracts with global FMCG brands, a cost-plus pricing structure that protects margins, and manufacturing facilities in both India and Vietnam that give it flexibility across Arabica and Robusta sourcing. The Continental Coffee brand, CCL's domestic B2C label, represents an incremental growth layer that improves blended margins without replacing the core export engine. For investors evaluating which Indian coffee company offers the best investment case, CCL Products' combination of margin stability, export diversification, and the early-stage domestic brand opportunity makes it a differentiated option within the broader India beverage sector.

Jay Shree Tea & Industries Ltd (B.K. Birla Group)

Jay Shree Tea is one of the largest plantation companies in India, with estates spanning Cachar, Assam Valley, Darjeeling, Dooars, Terai, and Tamil Nadu, and a workforce exceeding 18,400 employees. What sets Jay Shree apart from other estate companies is its deliberate diversification beyond tea: it has built meaningful revenue streams in chemicals/fertilizers (through its Annapurna SSP brand) and sugar, reducing its dependence on a single seasonal commodity. On the tea side, the company has launched "Bagicha by Jay Shree Tea" as a retail brand to capture value further down the chain. However, at its core, the business remains a traditional plantation operation with the attendant cost rigidity (high fixed labor and estate maintenance costs) and weather sensitivity that defines this segment.

McLeod Russel India Ltd

McLeod Russel was historically India's largest tea company by volume, with a vast estate network spanning Assam, Dooars, Darjeeling, and overseas operations in Uganda and Vietnam. The company employs approximately 67,303 personnel (over 56% women), making it one of the largest private employers in Northeast India. Its business model is purely plantation-based, with no meaningful branded retail or value-added processing presence, leaving it fully exposed to auction price cycles and the structural cost disadvantages of large organized estates competing against small tea growers. The company is currently under severe financial distress, with borrowings assigned to the National Asset Reconstruction Company (NARCL) for debt resolution. Financial statements continue to be prepared on a "going concern" basis, contingent on the successful implementation of restructuring plans.

McLeod Russel is under debt resolution primarily because its large, fixed-cost plantation operations generated insufficient cash flows to service accumulated borrowings during a sustained period of weak auction prices, rising labor costs, and weather-affected crop output. The company's inability to diversify into branded or value-added segments left it fully exposed to commodity cycle downturns. Borrowings have been assigned to NARCL, and the resolution timeline remains uncertain.

The Grob Tea Co Ltd

Grob Tea is a focused, single-region Assam CTC estate company that differentiates through quality rather than scale. Its estates are Trustea-certified, and the company has invested in climate change mitigation through its Project Work on Climate Change (PWCC). Grob's strategy centers on producing above-average quality CTC teas that command premium price realizations at auction compared to broader market averages. However, the business remains a traditional plantation model, and core operating margins are modest, with profitability materially supported by non-operating "Other Income" rather than tea operations alone.

United Nilgiri Tea Estates Co Ltd

United Nilgiri Tea Estates is a niche, high-quality South Indian orthodox tea producer based in the Nilgiris (Tamil Nadu) with a strong export orientation. The company's business model is built around specialty and organic tea production, deliberately targeting the premium end of the market where price realizations are significantly higher than mass-market CTC. This quality-first strategy, combined with a debt-free balance sheet and lean operating structure, has allowed United Nilgiri to achieve net margins that are exceptional for a plantation company. The company's geographic concentration in the Nilgiris positions it well for the growing global demand for single-origin, high-altitude orthodox teas.

Peria Karamalai Tea & Produce Co Ltd

Peria Karamalai is a small South Indian estate company based in Valparai, Tamil Nadu. The company is in the midst of a strategic transition from CTC tea production toward orthodox tea, seeking to access the higher price realizations that orthodox and specialty grades command. It is also investing in field automation to address what management has consistently flagged as a "dwindling labour force" in the region. As a single-estate, single-geography operation, Peria Karamalai has limited diversification and scale, making it highly sensitive to local weather patterns, labor availability, and regional auction dynamics.

Unlike CTC tea, which is produced through a crush-tear-curl mechanical process optimized for high volumes and domestic masala chai consumption, orthodox tea is produced through a more labor-intensive withering, rolling, and drying process that preserves the full-leaf structure. Orthodox teas command significantly higher price realizations in international markets, particularly in Europe, Japan, and the Middle East, and United Nilgiri Tea Estates has built its entire business model around this premium format.

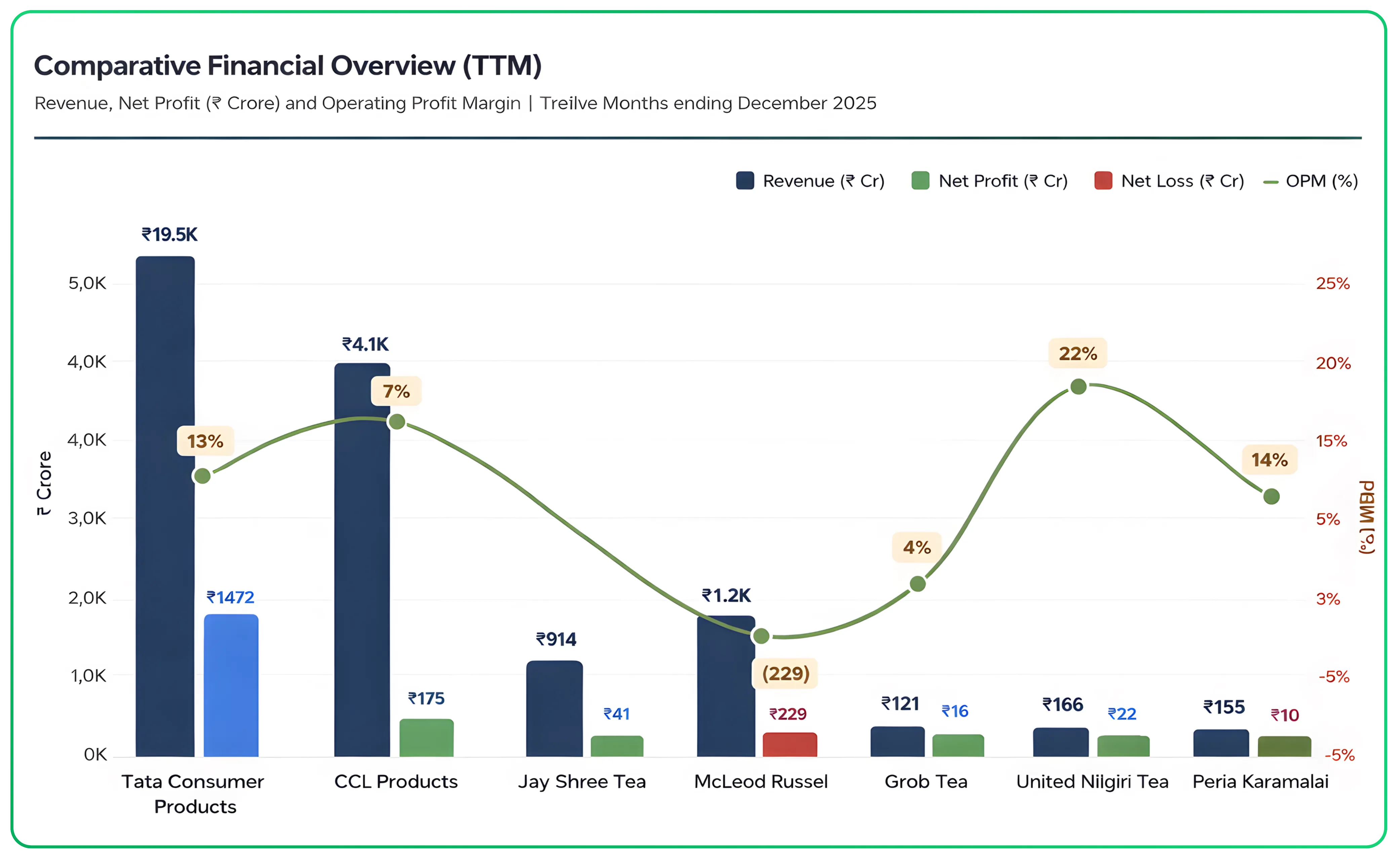

Comparative Financial Overview (TTM)

| Company | Revenue TTM (₹ Cr) | Net Profit TTM (₹ Cr) | OPM (%) | ROCE (%) | P/E (x) | Market Cap (₹ Cr) |

|---|---|---|---|---|---|---|

| Tata Consumer Products | 19,465 | 1,472 | 13 | 9.16 | 72.2 | 1,04,656 |

| CCL Products | 4,069 | 375 | 17 | 13.1 | 39.6 | 14,824 |

| Jay Shree Tea | 914 | 41 | N.A. | 3.74 | 200 | 228 |

| McLeod Russel | 1,190 | (225) | (1) | (1.85) | N.M. | 365 |

| Grob Tea Co | 121 | 6 | 4 | 12.71 | 18.0 | 101 |

| United Nilgiri Tea | 86 | 22 | 22 | 10.06 | 11.6 | 257 |

| Peria Karamalai Tea | 55 | (0.2) | 14 | 1.20 | N.M. | 254 |

Investment Implications and Outlook

The Indian tea and coffee industry is at an inflection point. On the demand side, structural tailwinds (premiumization, rising incomes, health consciousness, export recovery) are robust and likely to endure. On the supply side, the industry remains fragmented: the gap between branded FMCG players and commodity-exposed plantation companies continues to widen.

The competitive advantage is shifting decisively toward companies that can either build brands (Tata Consumer Products in tea), add processing value (CCL Products in coffee), or differentiate through quality and specialty positioning (United Nilgiri in orthodox tea). Traditional plantation companies face an increasingly challenging operating environment characterized by rising costs, climate uncertainty, labor scarcity, and competition from the STG sector.

The coffee segment, particularly the instant coffee processing vertical, offers structurally superior unit economics due to its cost-plus pricing model, global demand growth, and supply-demand imbalance. In tea, the branded segment offers the most attractive risk-adjusted returns, while specialty and orthodox tea estates occupy a defensible niche. Mass-market CTC plantations, exposed to commodity cycles and cost rigidity, represent the most challenged sub-segment within the sector.

Investors evaluating this space should pay close attention to the fundamental distinction between brand-driven and commodity-driven business models, as the performance divergence between these two categories is structural and likely to persist.

Turn research into action. Trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.