Ever noticed how option premiums can swing wildly even when the underlying barely moves? That’s Vega in options at work. While the delta tracks price sensitivity and the gamma measures acceleration, the Greek vega captures something entirely different, which is how much your option’s value changes when market volatility shifts. Think of Vega (v) for options as your volatility meter, crucial for anyone serious about options trading.

On Nxtoption, understanding Vega transforms how you approach volatile market conditions. When earnings season hits or major announcements loom, Vega becomes your guide to navigating the premium swings that catch unprepared traders off guard.

What is Vega?

Definition: Change in option premium(₹) for a 1 %-point move in Implied Volatility (IV).

Non-directional: Same for calls and puts at identical strike and expiry.

Drivers: Highest for At-the-Money (ATM) strikes, higher for longer tenures, tied to time value.

Example Setup

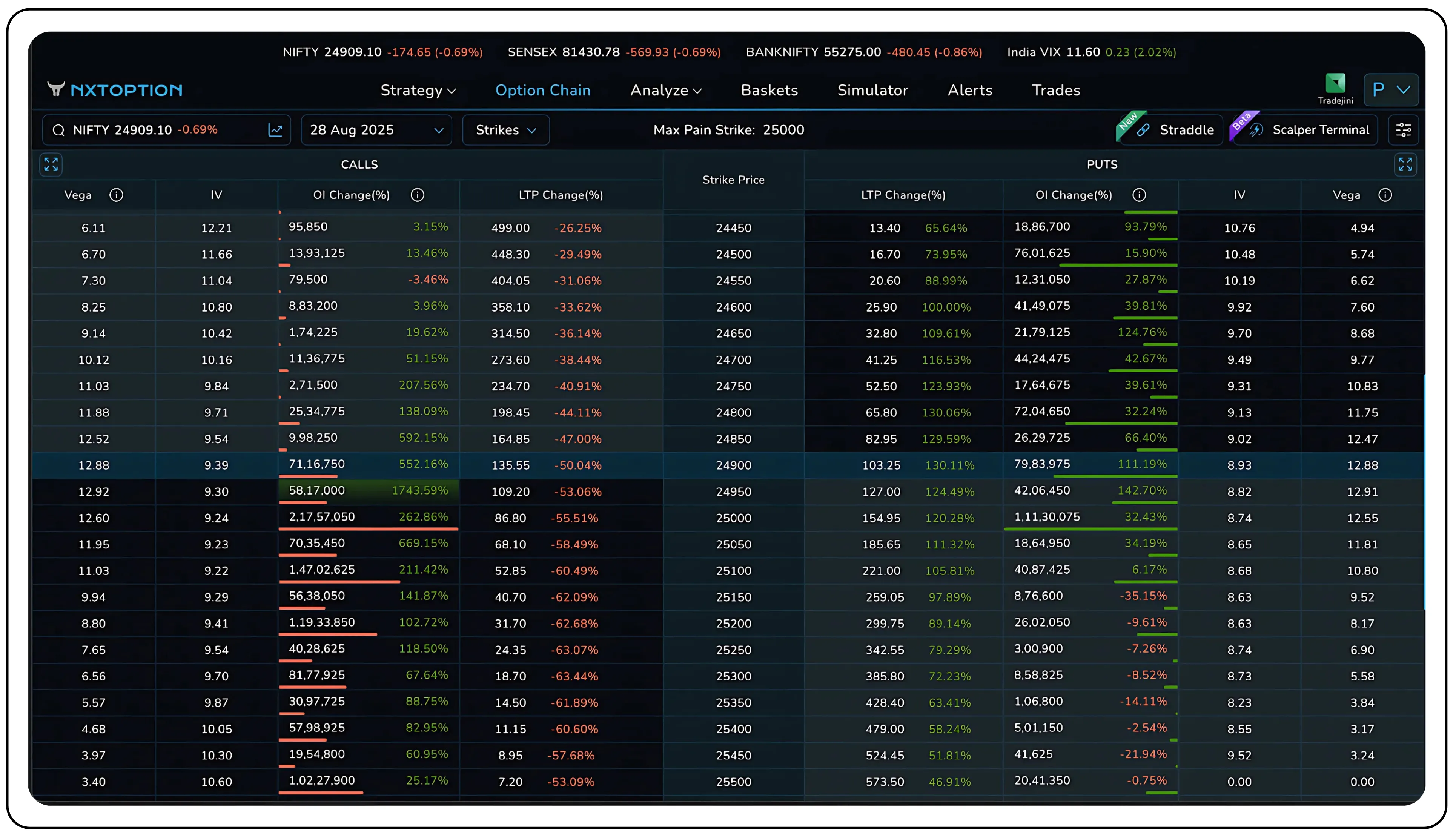

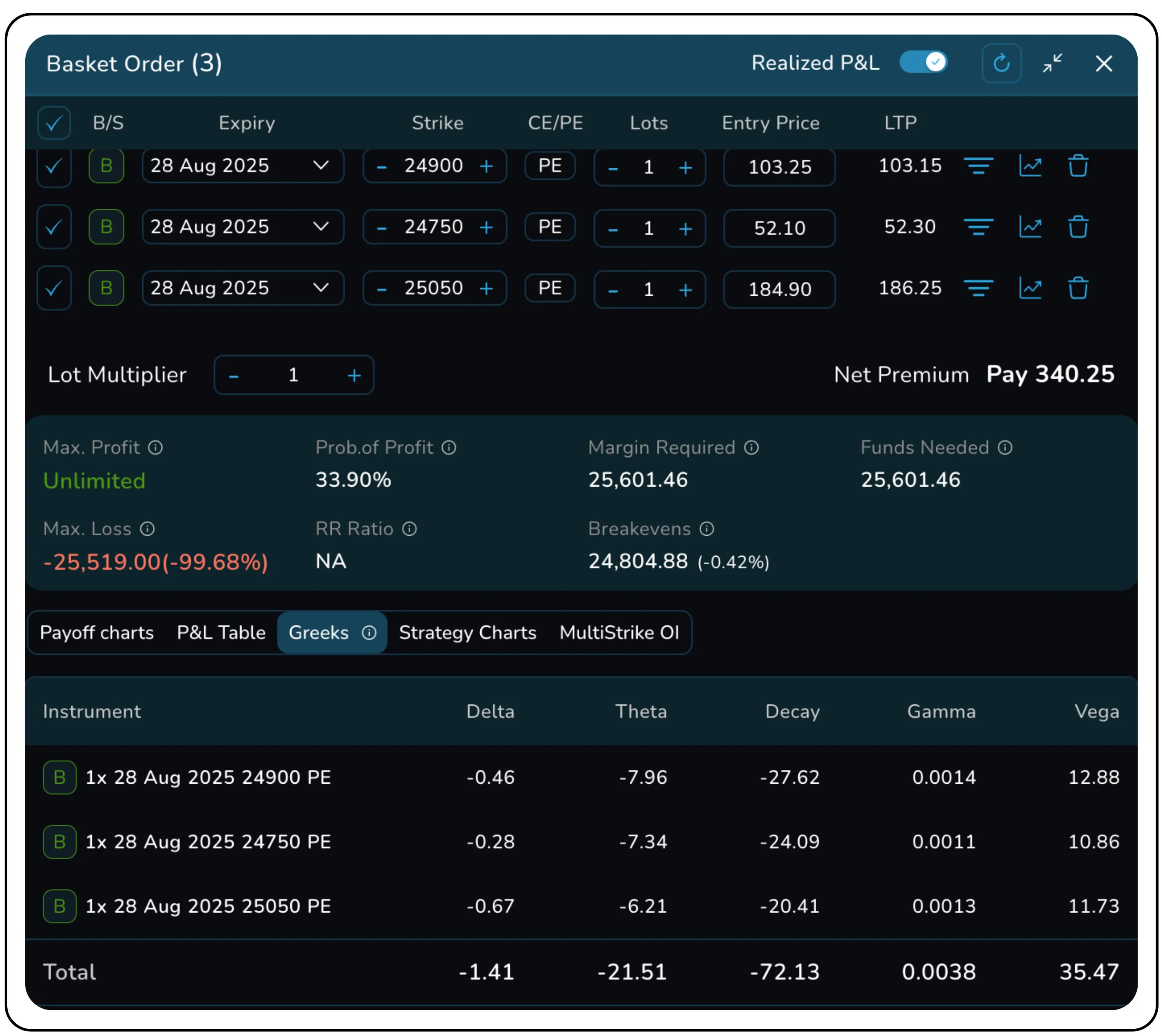

Let’s examine a real position using the NIFTY 24,900 call option of 28 Aug 2025 expiry. (Spot - 24,909.10)

- Position - Long 24,900 CE (near-ATM / slightly ITM)

- Current Premium - ₹135.55

- Vega - 12.88

- Current IV - 9.39%

If implied volatility jumps from 9.39% to 14.39% (a 5% or 500 bps increase)

Premium Change—Vega × IV change = 12.88 × 5 = ₹64.40

New Theoretical Premium—₹135.55 + ₹64.40 = ₹199.95

This is the linear Vega effect only. It assumes the spot, time-to-expiry, and other Greeks remain unchanged during the IV shock.

Because this strike sits near the ATM, Vega is relatively large, which is also a reason why ATM strikes are preferred for volatility plays. Real P&L will also reflect Delta/Gamma if the underlying moves, then Theta will erode value over time: treat the Vega figure as the volatility-driven component of the premium change.

Moneyness and Vega

Vega behaves differently depending on whether the option is At-the-Money (ATM), In-the-Money (ITM), or Out-of-the-Money (OTM). ATM options have the highest Vega. Since ATM options are most sensitive to volatility, their premiums move the most when IV shifts. OTM and ITM options have lower Vega. Deep ITM or far OTM options are less impacted by volatility changes because their outcomes are already tilted toward exercise or expiration, respectively.

With Nifty trading at 24,909, the 24,900 strike sits squarely ATM, which is exactly where the Vega is peaking (12.88). This shows that ATM = highest Vega, because small IV changes reprice the largest proportion of time value at the money.

Strikes further from the spot, like the 24,750 and the 25,050, show lower Vega, since their premiums are more driven by intrinsic/out-of-money probabilities. Practically: choose ATM strikes for pure volatility plays, as they give the largest rupee move per % change in the IV, and choose wings for cheaper premium and higher percentage returns if IV spikes, but expect smaller absolute Vega per contract.

Volatility and Vega

Vega’s real impact shows up when implied volatility (IV) moves and not when the underlying moves. A rising IV inflates premiums for both calls and puts, whereas a falling IV shrinks them.

24,900 Call Options with a Vega of 12.88, LTP of ₹135.55, and IV of 9.39%, it would gain roughly ₹64.40 if IV jumped +5% (12.88 × 5), lifting the premium toward ₹199.95 - even if NIFTY remains constant. That’s how pure volatility plays work.

Event-driven markets show this volatility clearly. Furthermore, IV typically rises before big events (earnings, policy, Budget), which inflates the price of the options. However, after the event, the IV often collapses, a case of classic volatility crush that erases the premium rapidly. Notably, buyers chase IV before the event, while sellers profit if the event passes without realized volatility matching the priced-in IV.

Below is an illustrative Vega profile of a stock, XYZ Ltd., showing how Vega can behave as IV changes across strikes:

| Strike | Vega at 15 IV | Vega at 20 IV | Vega at 25 IV |

|---|---|---|---|

| 22.5 | 0.002 | 0.009 | 0.019 |

| 25 | 0.017 | 0.033 | 0.045 |

| 27.5 | 0.056 | 0.066 | 0.071 |

| 30 (ATM) | 0.085 | 0.085 | 0.085 |

| 32.5 | 0.069 | 0.077 | 0.081 |

| 35 | 0.035 | 0.053 | 0.065 |

| 37.5 | 0.012 | 0.020 | 0.045 |

The Observed Vega and Observed IV columns are taken directly from the option chain

The Vega @X% columns estimate nominal Vega if market IV were X% instead

ATM and near ATM strikes show the largest absolute Vega. They show the strongest absolute sensitivity to volatility changes, delivering the largest rupee move for a given IV shift. Wings (far OTM/ITM) have a smaller observed Vega, which means that they gain more nominal Vega as IV rises, but their starting premium and probability profile differ.

While ATM Vega remains relatively stable across different IV inputs, ITM and OTM Vegas expand disproportionately as IV rises. Lower IV inputs tend to cause ITM and OTM Vegas to decline. Similarly, higher IV inputs tend to cause Vegas to increase for ITMs and OTMs.

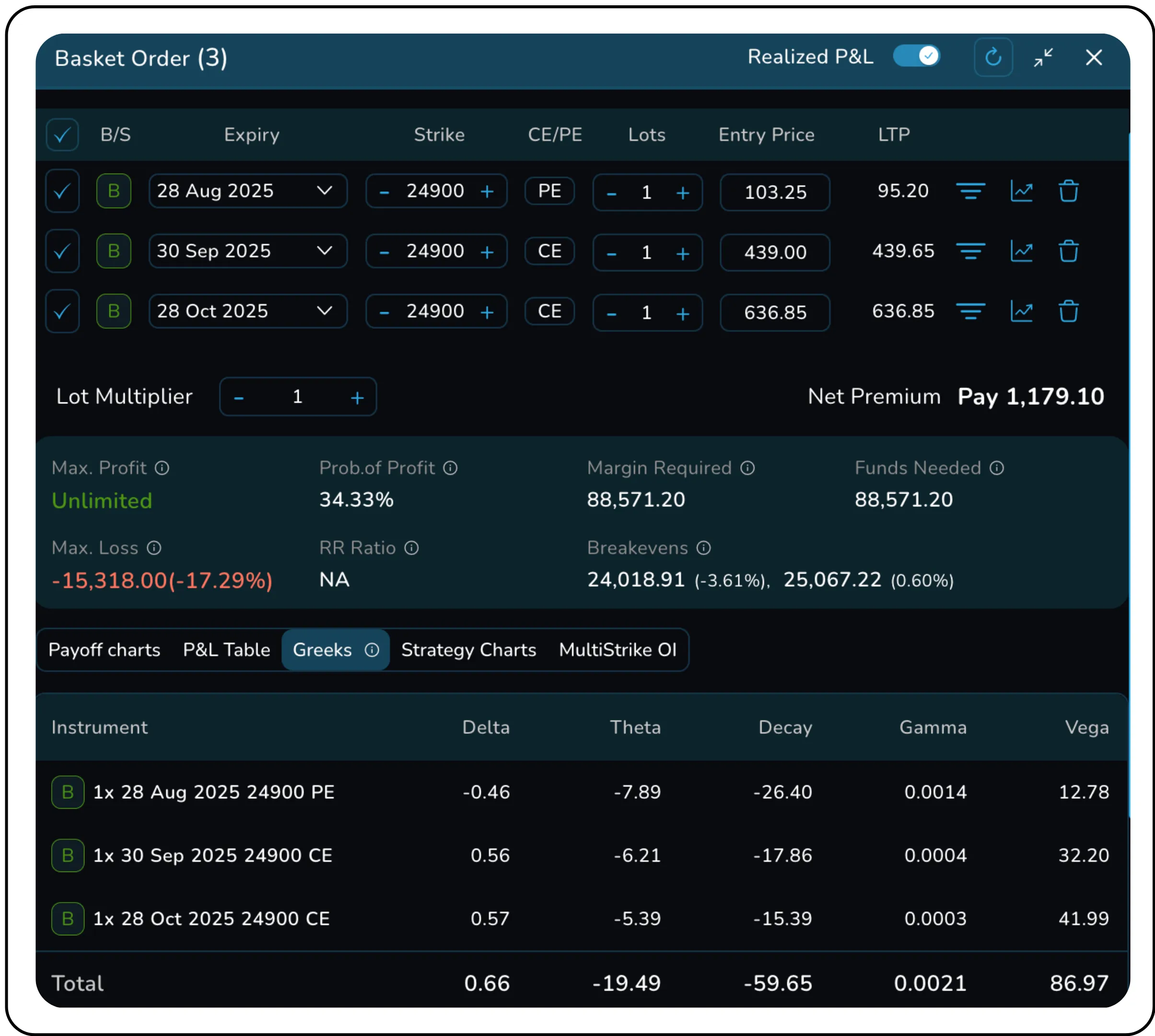

Time and Vega

Time to expiration is a principal determinant of Vega in options behaviour. As the expiry nears, the time value that can be altered or affected by IV also reduces. Consequently, Vega declines. The decline is non-linear, which means that Vega falls slowly for long tenures but accelerates as expiry approaches, particularly for the ATM strikes.

We can see above that the same 24,900 strikes across three expiries have different Vegas. This is a perfect illustration of how Vega scales with time. The long-dated expiry (28th October) carries the highest Vega (41.99), as the IV has much scope to reprice its time value.

Moving from the near expiry to one month adds 19.42 Vega, while adding another month adds only 9.79 Vega. This shows that marginal Vega gains diminish with the tenor.

How to use Vega effectively

Vega is a volatility play, not a price bet. Use it when the trade thesis is “IV will move,” and pick strike, expiration and size to match that thesis. Use Vega when expecting an IV jump, hedging tail risk, or arbitraging term structure. However, avoid it when the IV is already inflated and no catalyst or liquidity exists and spreads make entry/exit costly.

Here’s a quick checklist to follow:

- Prefer ATM or Near-ATM strikes for pure Vega exposure, as they will produce the largest premium changes for any IV moves.

- Choose shorter dated options for event-driven IV spike plays and longer ones for larger absolute Vega and more time for a volatility story to play out.

- Play Vega when IV is cheap relative to historical volatility or when a known catalyst like earnings, policy, or budget news is imminent.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.