Eureka Forbes Limited pioneered the idea of healthy living in Indian homes, evolving from the iconic “friendly man from Eureka Forbes” into a digital-first, D2C health and hygiene brand. Founded in 1982 as a joint venture between the Tata Group and Electrolux, the company created an entirely new category with Aquaguard water filter cum purifiers, making Eureka Forbes Ltd synonymous with safe drinking water in India.

By building Asia’s largest direct sales and service network, Eureka Forbes established a strong sales and after-service network, positioning itself as one of the largest direct-selling companies globally. Since Advent International’s acquisition in 2022, the company has accelerated its transition toward a modern, digitally driven business model.

Today, Eureka Forbes Limited is a leading player in the consumer durables and health & hygiene market, offering water purifiers, air purifiers, and vacuum cleaners. The market cap of Eureka Forbes stands at ₹9,838.40 crore, with the price of Eureka Forbes shares at ₹523.65, making it a closely tracked stock for share analysis, intrinsic value assessment, and long-term investment evaluation.

Business Model and Segments

Eureka Forbes operates as a multi-channel organization with a dominant presence in three core areas:

Water Purification: The crown jewel of the company, holding a commanding ~40% market share in the organized segment. It addresses 17 different water conditions across India through technologies like RO, UV, and UF.

Vacuum Cleaners: A virtual monopoly in the Indian market with over 60% market share. The company is now pivoting toward the high-growth Robotic Vacuum Cleaner segment, which is seeing a 29% CAGR.

Air Purification and Home Security: Air purifiers represent emerging segments that capitalize on rising urban pollution and the need for smart home safety.

The AMC (Annual Maintenance Contract) Service Segment

Here's where it gets interesting for investors conducting Eureka Forbes share analysis: 35-40% of their revenue comes from Annual Maintenance Contracts (AMCs). Most customers renew these AMCs year after year. This creates:

- Predictable recurring revenue with strong cash flow (the dream of every investor)

- High margins (service business always beats product sales)

- Customer stickiness (you're locked into their ecosystem)

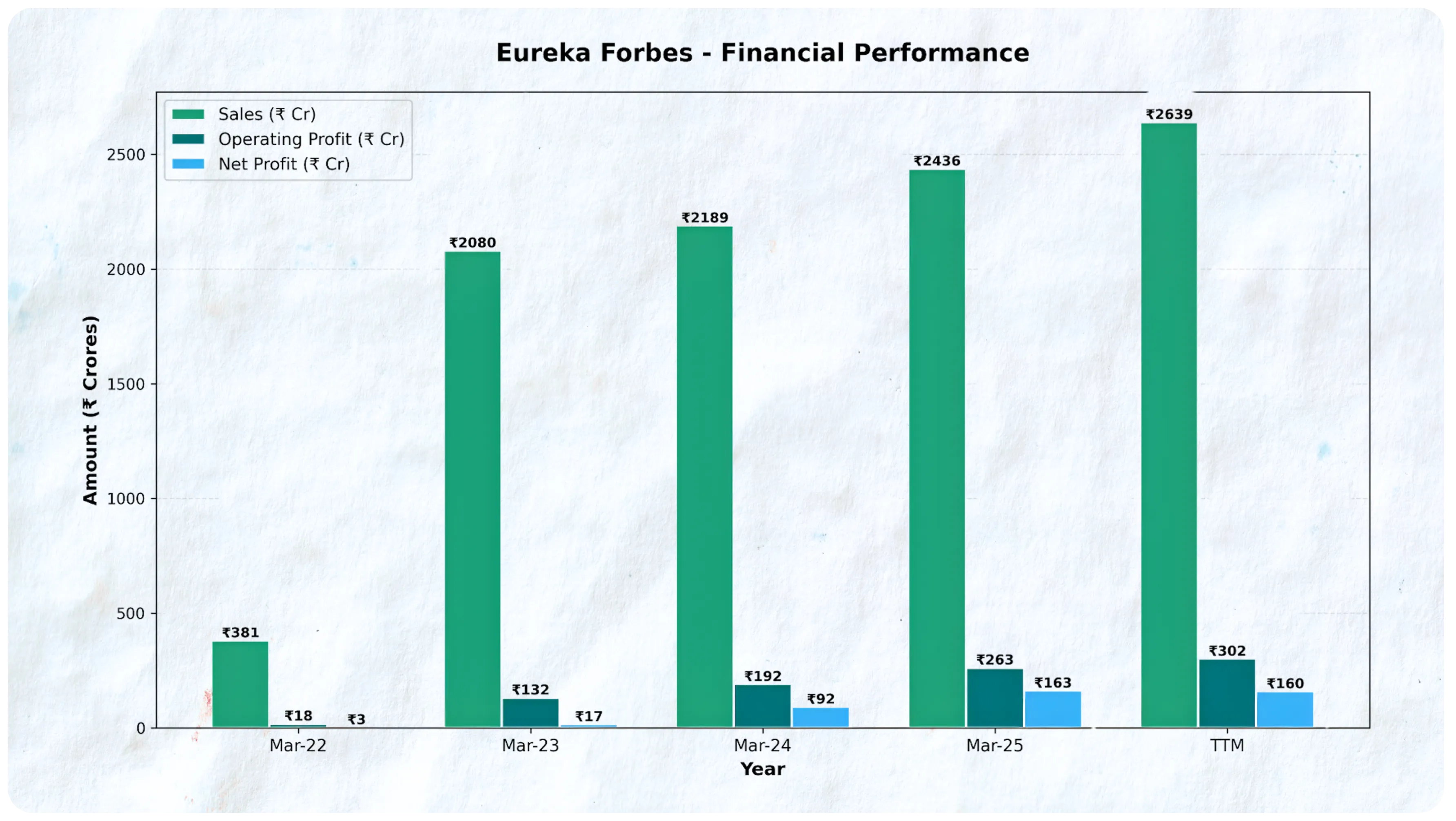

Financial Performance and Financial Stability Based on Annual Reports

| Year | Sales | Operating Profit | Net Profit |

|---|---|---|---|

| TTM | 2639 | 302 | 160 |

| Mar-25 | 2436 | 263 | 163 |

| Mar-24 | 2189 | 192 | 92 |

| Mar-23 | 2080 | 132 | 17 |

| Mar-22 | 381 | 18 | 3 |

Amount in Crores

The company is debt free, which positively affects investor sentiment and highlights its strong financial stability. The company has shown a profit growth of 287% over 3 years, with operating profit growing at an annual rate of 91.47%. Operating margins have improved to 11.3%, supported by a robust cost management program, and the net profit margin improved to 6.75% as of FY2025.

FY25 Highlights:

Revenue: ₹2,436 crore showing good profit growth (↑12% YoY sales growth)

EBITDA: ₹285 crore; EBITDA margin at 11.7%

PAT: ₹163 crore (~10x growth vs FY23)

Product business growth: 17% YoY

- Water Purifiers: ↑18.1%

- Vacuum Cleaners: ↑12.8%

Free Cash Flow: ₹214 crore (FCF/PAT: 131%)with strong net cash flow generation

Net Cash: ₹284 crore; company shows financial stability with net surplus position

ROCE: ~353%, reflecting a capital-light, high-return model

Guidance for FY26:

Revenue: Sustained double-digit growth expected

Margins: To remain healthy with gradual expansion

Capex: ₹50–60 crore

Focus Areas: Product innovation, D2C expansion, service revenue growth

Cash & Returns: Strong cash generation and high ROCE to continue

Industry Outlook, Market Share, and Stock Market Opportunity

Increasing health consciousness among Indian consumers is a major driver for the home health and purification appliances industry. Concerns about contaminated water and poor air quality are translating into real demand for advanced purification solutions. For example, a 2023 survey across 305 districts found that 97% of Indian households use some form of water purification, with only 3% drinking directly from the tap — highlighting the shift toward proactive health protection. At the same time, global health data shows that over 37 million Indians suffer from water-borne diseases annually, underscoring why clean water solutions are becoming essential rather than optional.

On the air quality front, rising pollution levels in urban centres are elevating consumer concern. Markets such as Delhi, Mumbai, and Bengaluru consistently record air quality readings above safe limits, prompting households to adopt air purifiers to safeguard respiratory health. Retail data also mirrors this trend, with major electronics sellers reporting 30%+ year-on-year growth in air purifier sales, driven by heightened awareness of indoor air quality issues.

Low Penetration Across Categories

Water Purifiers: Penetration stands at only 6-7% of 300+ million households, leaving 93% untapped. 40% of households still boil water, while 30% rely on untreated sources. Market size: ₹10,000-12,000 crores, growing at 15-18% CAGR. Urban penetration (15-20%) significantly outpaces rural (2-3%). TAM exceeds ₹50,000 crores as awareness spreads beyond metros to 450+ Tier-2/3 cities.

Air Purifiers: Ultra-low penetration below 2% in a market of 300M+ households. Concentrated in top 8 metros accounting for 70% of sales. 14 of the world's 20 most polluted cities are in India, with Delhi AQI exceeding 400+ for 100+ days annually. Market valued at ₹800-1,000 crores, projected 25-30% CAGR. Post-COVID respiratory health awareness drove a 40% surge. Price erosion from ₹25,000 to ₹8,000-12,000 expanding addressable market to middle-income segments.

Vacuum Cleaners: Penetration below 10% vs. 90%+ in developed markets. Market size ₹2,500-3,000 crores growing 20% annually. Urban households comprise 80% of demand. Dual-income families increased 35% in the last 5 years, driving time-saving appliance adoption. Robotic segment growing fastest at 40% CAGR from low base. Average selling price declined 30% to ₹5,000-8,000, improving affordability for the mass market.

Growth Drivers

- Strong brand recall and trust in water and air purification, with Aquaguard being a category-defining brand

- Large installed base driving recurring revenue from AMC, filters, and service contracts

- Low penetration in core categories enabling steady first-time customer additions

- Shift to D2C and digital channels, improving customer reach and margins

- Premiumisation and product innovation, including smart and IoT-enabled products

- Expansion beyond metros into Tier-2 and Tier-3 cities

Competitive Advantages

Eureka Forbes' competitive advantage lies in its strong brand trust built over decades, with Aquaguard having become synonymous with water purifiers in India. The company benefits from a large installed base, which drives high customer stickiness and recurring revenue through AMC contracts, filter replacements, and service renewals.

Risks

Affordability constraints, especially in non-metro and price-sensitive segments

Intense competition and price discounting, impacting industry margins

Dependence on imported components, exposing players to input cost volatility

Low awareness in rural markets and resistance to shifting from traditional methods

High customer acquisition and service costs, particularly in D2C and service models

Regulatory or policy changes related to water quality, energy efficiency, or imports

Final Assessment

While dominating water purifiers and vacuum cleaners, Eureka Forbes struggles with capital efficiency (2.3% ROE is weak despite high ROCE). The dividend yield remains modest given the company's reinvestment priorities.

To justify current market value and share price levels, the company must execute on guidance, improve margins, and manage working capital better. Mutual fund investments in Eureka Forbes have been mixed, with some funds reducing exposure based on valuation concerns.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.