Sector Backdrop

India’s consumer electricals and durables sector is fast changing and competitive, shaped by long-term growth trends but also short-term challenges. Demand in this sector depends on income levels, consumer confidence, and seasonal factors. For instance, a hot summer or a late monsoon can sharply boost or reduce sales of cooling products, directly affecting the financial performance of V-Guard and its peers. The industry is also highly susceptible to commodity price volatility, with fluctuations in materials like copper directly impacting the profitability of key segments such as wires and cables. Furthermore, the market is marked by intense competition from both organized and unorganized players, which exerts continuous pressure on pricing and margins. Regulatory changes, such as the implementation of new Bureau of Energy Efficiency (BEE) standards, also play a crucial role in shaping product development and pricing strategies within the sector.

Business Snapshot & Evolution

V-Guard started as a stabilizer brand in South India and has grown into a nationwide company offering a wide range of electrical and consumer durable products. Today, the company’s operations are structured across three primary segments: Electronics, Electricals, and Consumer Durables. Its product portfolio is extensive, including voltage stabilizers, UPS systems, wires, pumps, switchgears, fans, water heaters, and kitchen appliances.

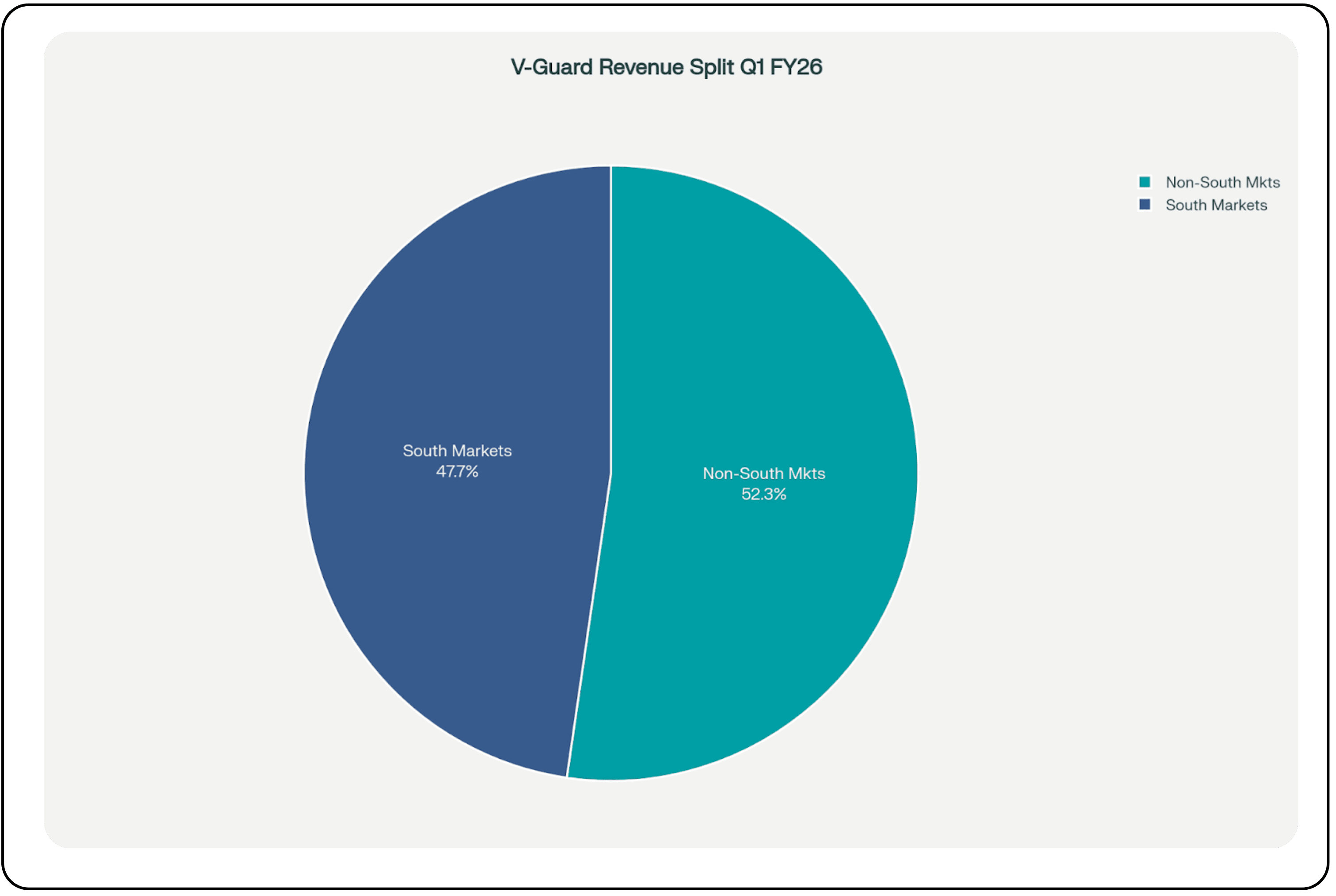

A major turning point was V-Guard’s expansion beyond South India. Non-South markets now contribute more than half of its revenue, making it a truly national player. In a significant move to bolster its presence in the kitchen appliances segment, the V-Guard Sunflame acquisition was completed, which now operates as a distinct business vertical. This acquisition is central to its current strategy, focused on integrating Sunflame’s operations to unlock synergies and establish a stronger foothold in the fast-growing kitchen appliances category.

Financial Performance Overview

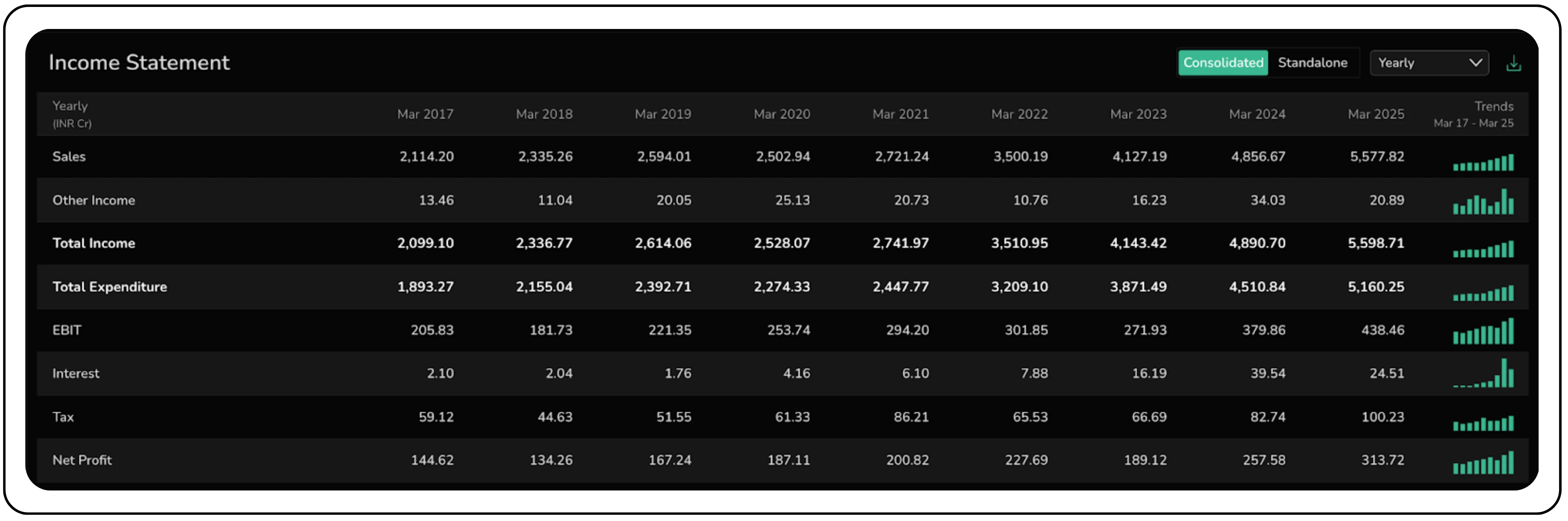

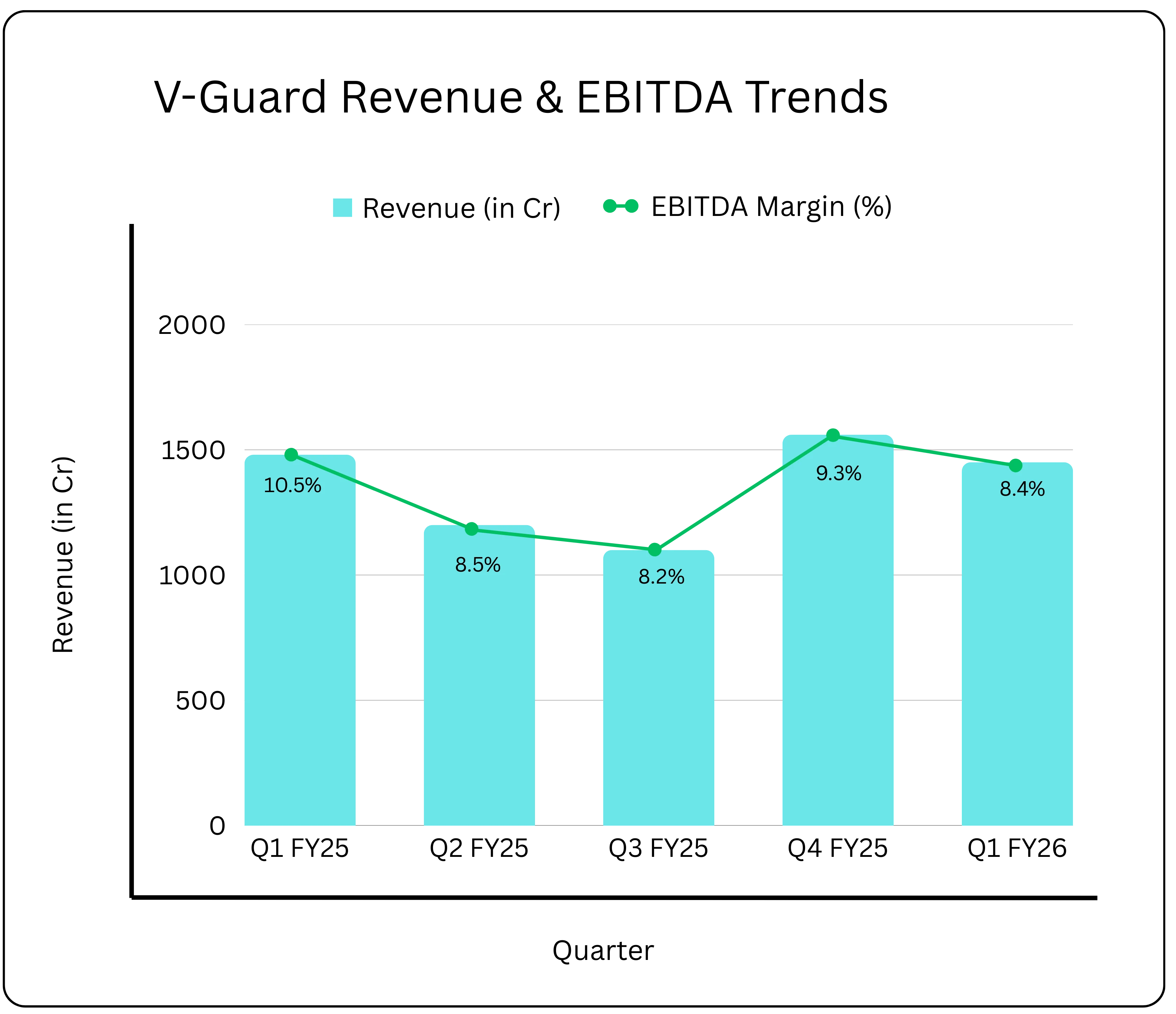

V-Guard saw a strong growth in FY25, though its momentum slowed in early FY26 due to weaker summer demand and an early monsoon, which impacted seasonal product sales. The company achieved its highest-ever quarterly revenue in Q4 FY25, capping a year where consolidated revenues grew by 14.8% to INR5,578 crores, successfully meeting its annual growth target of 13-15%. This performance was accompanied by a consistent improvement in gross margins, which expanded throughout the year, driven by softening commodity prices, strategic pricing actions, and a better product mix. A significant financial achievement in FY25 was becoming a debt-free company after pre-closing the entire term loan related to the Sunflame acquisition.

However, Q1 FY26 presented a sharp contrast, with consolidated net revenue declining marginally by 0.7% YoY to INR1,466 crores. This downturn was primarily driven by a weak summer season and an early onset of the monsoon, which severely impacted demand for cooling products. The resulting lower sales impacted operating efficiency, pulling EBITDA margins down to 8.4% and profits down 25% year-on-year.

Business Segments Breakdown

V-Guard’s diversified business model allows it to navigate varied market conditions, though segment performance can be cyclical, influenced by seasonality, input costs, and demand variability in end-user industries.

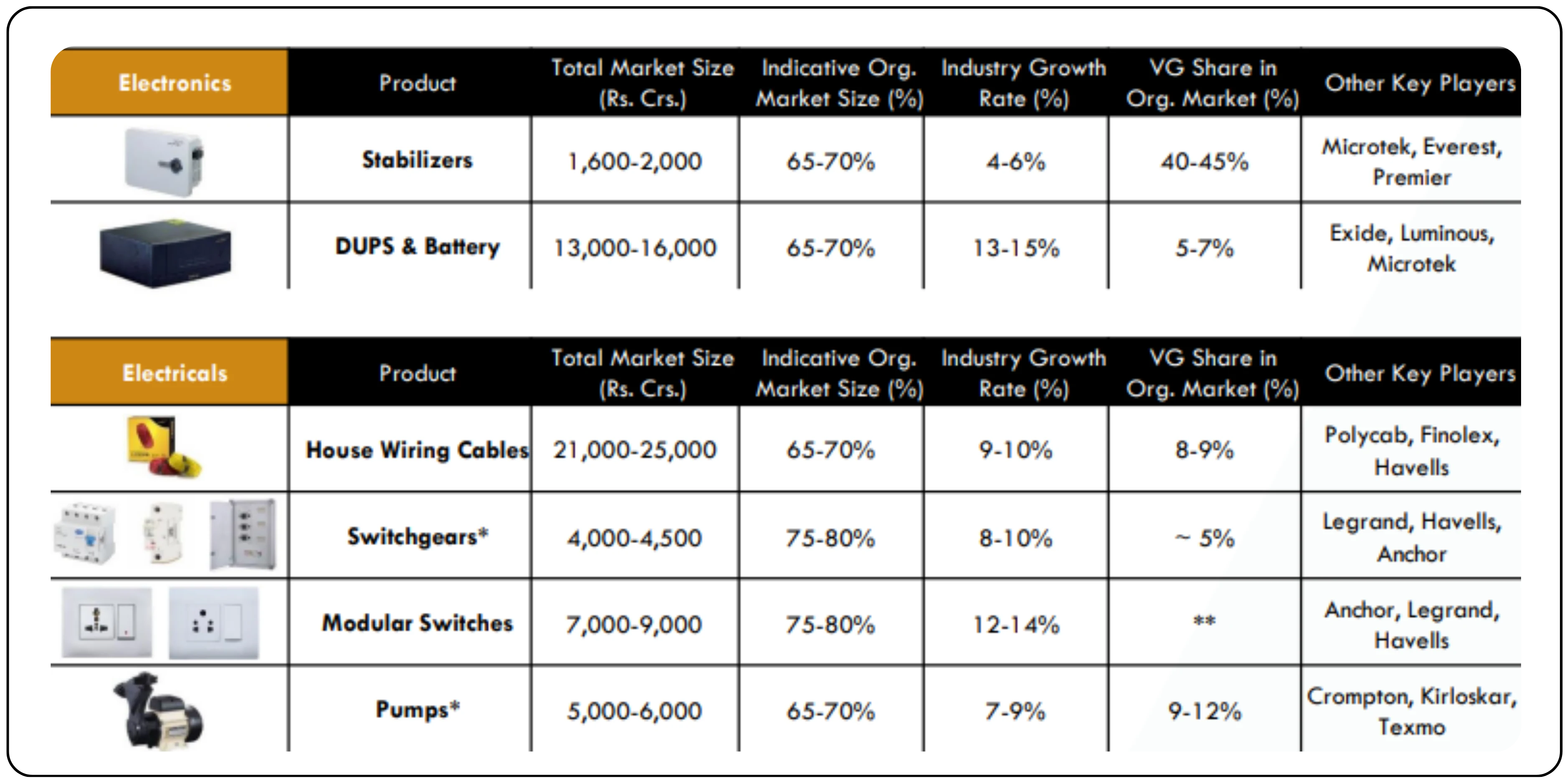

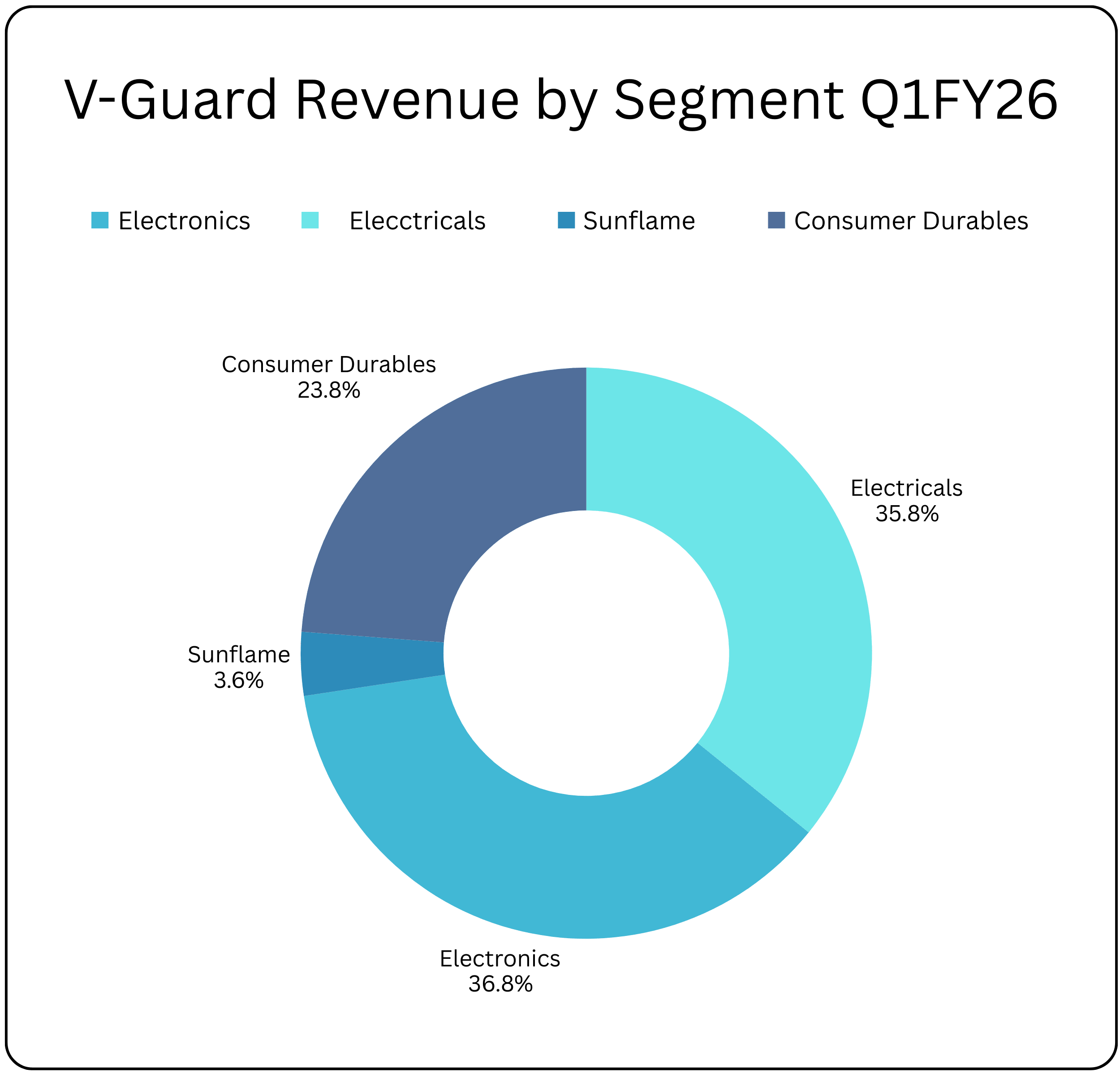

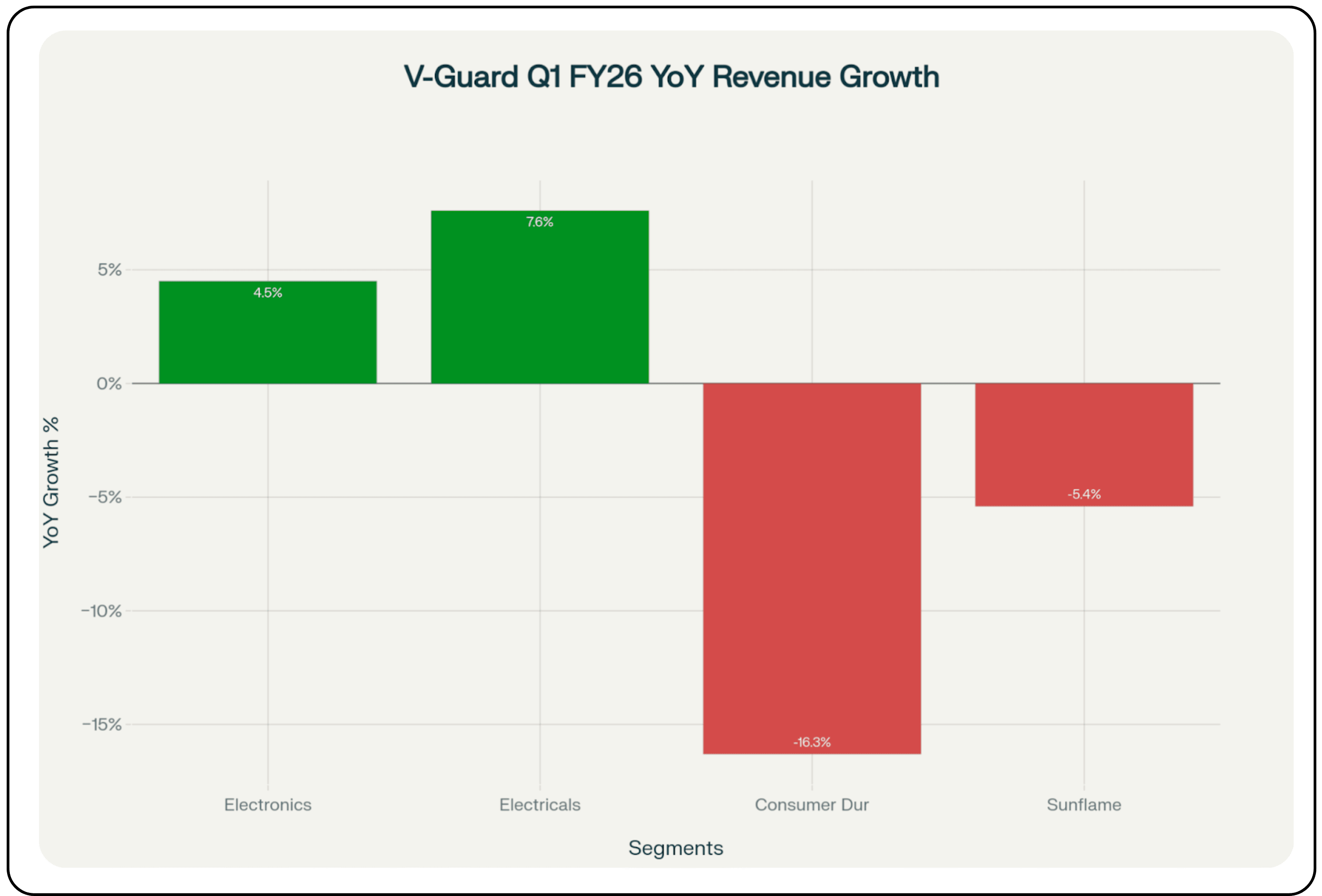

Electronics (36.8% of Q1 FY26 Revenue): This segment includes stabilizers, digital UPS systems, inverters, batteries, and solar power systems. Its Performance is heavily linked to the summer season due to demand for stabilizers and UPS systems during periods of high power consumption and outages. In Q1 FY26, the segment registered moderate growth of 4.5% YoY, as subdued stabilizer demand was offset by strong performance in the inverter battery business and solar rooftop solutions. Margins in the electronics segment have remained consistently strong, benefiting from an increase in in-house manufacturing of batteries.

Electricals (35.8% of Q1 FY26 Revenue): As the company’s largest segment, it comprises house wiring cables, pumps, switchgears, and modular switches. The segment grew by a steady 7.6% YoY in Q1 FY26. Its performance, particularly in the wires category, is significantly influenced by commodity price volatility, with fluctuating copper prices leading to de-stocking or up-stocking by trade channels. Despite this volatility, other categories like switchgears have shown consistent double-digit growth, reflecting healthy demand and category expansion.

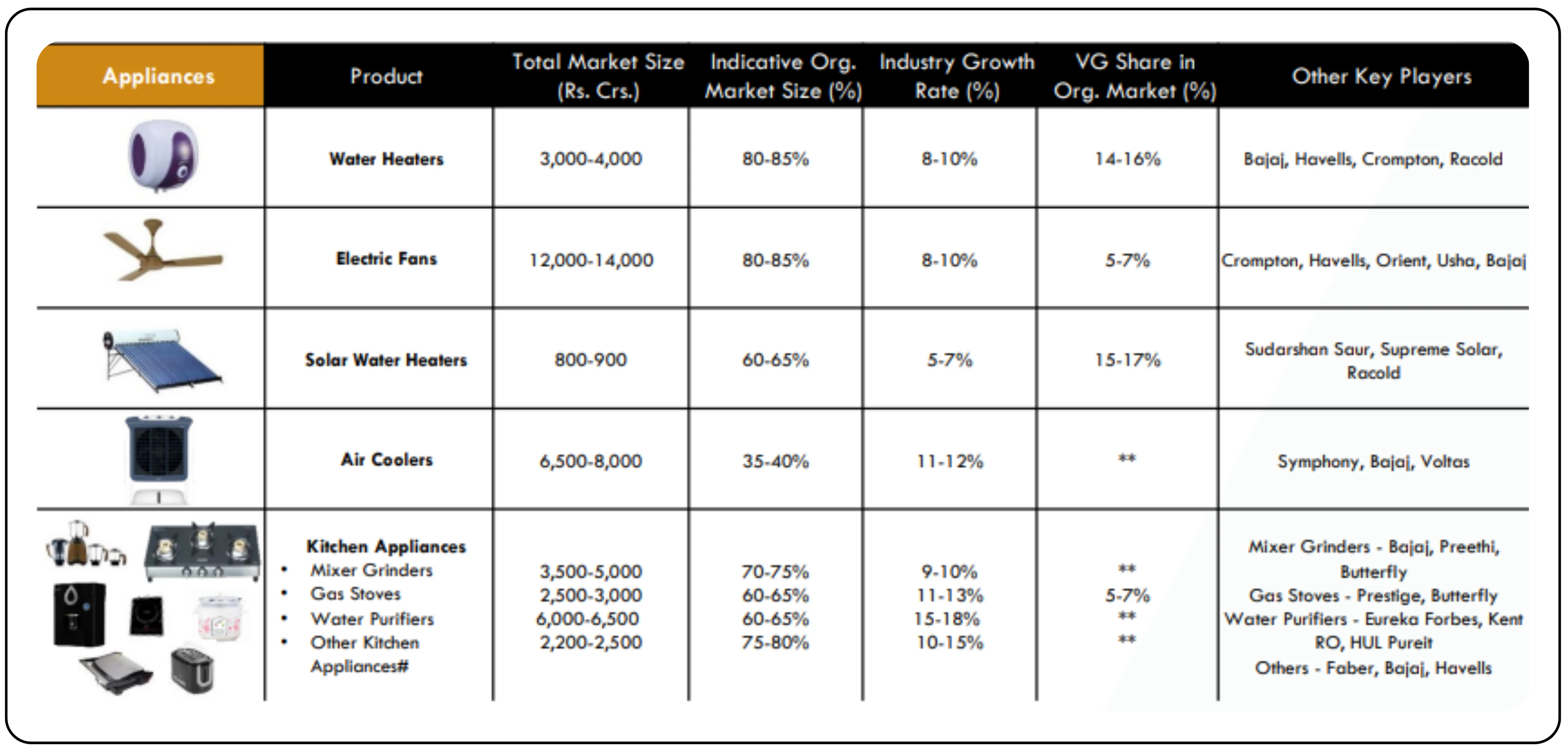

Consumer Durables (23.8% of Q1 FY26 Revenue): This segment, which includes fans, water heaters, kitchen appliances, and air coolers, is the most exposed to seasonality. After a strong performance in FY25 driven by a good summer, the segment experienced a significant 16.3% YoY revenue degrowth in Q1 FY26 due to the weak summer. Sales dropped 16.3% YoY in Q1 FY26, leading to an operating loss of -2.1%. The kitchen appliances business within this segment has faced a persistent industry-wide slowdown.

Sunflame (3.6% of Q1 FY 26 Revenue): This acquired business focuses primarily on kitchen appliances. It has consistently faced headwinds, posting a 5.4% YoY degrowth in Q1 FY26. The underperformance is attributed to a combination of factors, including a broader slowdown in the kitchen appliance industry, a high base effect in certain quarters, and a persistent reduction in orders from the CSD (Canteen Stores Department) channel. Management has initiated a full merger of Sunflame’s operations with V-Guard, aiming to leverage synergies and drive a turnaround.

Strategic Moats or Differentiators

V-Guard’s competitive advantage is built on several key pillars that collectively create a resilient business model.

- Pan-India Distribution and Brand Equity: V-Guard has moved beyond its southern roots to become a strong nationwide brand. Its strong distribution network of over 100,000 channel partners makes it hard for rivals to match. This wide reach, coupled with strong brand equity built over decades, fosters customer trust and loyalty.

Strategic In-house Manufacturing: V-Guard plans to raise in-house manufacturing from 65% to 70-75% in the next few years. This move is driven not by a margin improvement but more strategically by the need for better quality control, supply security, and the ability to innovate and differentiate products, which is a capability difficult to achieve with external vendors.

Diversified Product Portfolio: The company’s presence across three distinct segments mitigates the risk associated with any single product category or season. The strong performance of the Electronics segment in Q1 FY26 helped cushion the sharp decline in Consumer Durables, which was impacted by the weak summer.

Strong Balance Sheet: V-Guard’s financial prudence is a key differentiator. The company’s ability to become debt-free after a major acquisition demonstrates robust cash flow generation and disciplined capital management. This strong balance sheet provides financial flexibility to weather economic downturns and fund future growth without relying on external financing.

Growth Drivers and expansion plans

Management has outlined a clear, multi-pronged strategy for future growth, backed by significant capital allocation.

Capacity expansion through Capex: V-Guard has planned an annual capital expenditure of INR100-120 crores over the next few years to expand its manufacturing facility. Key projects include a INR100 crore investment in a new facility for fans in Hyderabad to enhance product differentiation and supply security, and a INR50 crore investment to expand its battery plant capacity, also in Hyderabad, to support high double-digit growth in that business.

Deepening Pan-India Presence: The strategic focus on non-South Markets remains a primary growth driver. The company continues to invest in expanding its outlet coverage and brand building in these geographies, with a long-term ambition of these markets to contribute 65% of total sales.

Sunflame Turnaround and Integration: The formal merger of Sunflame’s operations into V-Guard is a major strategic initiative. The goal is to leverage V-Guard’s strengths in customer service, quality management, and sales infrastructure to revitalize the Sunflame brand and achieve significant synergies.

New Category Expansion: V-Guard has entered the lighting category, a strategic move to complete its product basket for electrical retailers and leverage its extensive distribution network, initially relying on an outsourcing model, this new vertical represents a long-term growth opportunity.

Risks and Industry Headwinds

V-Guard’s business is subject to several external and operational risks that could impact its performance.

Weather Dependency and Seasonality: V-Gard’s performance strongly depends on seasonal conditions like summer heat and monsoon timing. As demonstrated in Q1 FY26, a weak summer season or an early/extended monsoon can severely impact demand for its high-volume cooling products (fans, air coolers) and stabilizers, leading to revenue and profit volatility.

Commodity Price Volatility: The Electricals segment, particularly wires, is exposed to fluctuations in copper prices. Sharp price movements can lead to channel de-stocking and margin pressure, creating unpredictability in the segment’s performance.

Intense Competition: The consumer durables and electricals space is hyper-competitive, with pressure from organized peers and unorganized players. This intensity makes it difficult to pass on cost increases and puts continuous pressure on margins, especially in categories like fans and kitchen appliances.

Sunflame Integration Risk: The turnaround of the Sunflame business remains a significant challenge. The segment has consistently underperformed due to industry-wide slowdowns and specific issues in the CSD channel. While a merger is underway, successful integration and achieving the desired growth trajectory carry execution risk and may take longer than anticipated.

Valuation and Market View

For V-Guard, valuation multiples provide a useful lens to understand market positioning relative to peers. The stock trades at a P/E of 55.36x and an EV/EBITDA multiple of 32, both of which sit above the sector median of 56. P/E and 23x EV/EBITDA. This suggests the market assigns a valuation premium, particularly against mid-tier consumer durable peers like Crompton and Whirlpool. While it is below higher-growth discretionary players like Amber Enterprises, V-Guard’s premium is noteworthy given its lower quarterly profit growth profile.

The high valuation shows investor confidence in V-Guard’s cash flows and its ability to maintain profits despite demand swings. Its Return on Capital Employed (ROCE) of 19.5% is significantly higher than the median and compared to Blue Star and Crompton, suggesting efficient capital utilization and disciplined balance sheet management. However, quarterly profit contracted by 25.38%, indicating near-term earnings volatility, especially as integration challenges with Sunflame weigh in on profitability.

In essence, the stock’s current valuation reflects a market view that V-Guard deserves to trade at a premium to many established peers due to its stable core business, prudent financial structure, and strong return profile. However, the gap versus high-growth peers indicates that investors remain cautious, waiting for evidence of sustained earnings recovery and the successful turnaround of Sunflame. Any improvements in quarterly earnings consistency or stronger than expected growth in non-seasonal product segments could catalyze a re-rating, narrowing the valuation gap with higher-multiple companies in the sector. Conversely, persistent underperformance on the Sunflame integration or weak seasonal demand could place downward pressure on these stretched multiples.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.