_1_11zon.webp%3Falt%3Dmedia%26token%3Dac87e0a7-37b9-47a6-9134-44fee8ac74f6&w=3840&q=85)

Vikram Solar is one of India’s largest pure-play, non-captive solar PV module manufacturers by installed capacity. It runs two module plants (Falta SEZ, West Bengal; Oragadam, Tamil Nadu) totaling 3.50 GW today, is ALMM-enlisted at 2.43 GW (Jul-2024), and has been repeatedly listed as BloombergNEF Tier-1 through 1Q–3Q CY2024. The company began in 2009 with 12 MW and now plans aggressive brownfield/greenfield expansion.

It targets 10.5 GW module capacity by FY26 and 15.5 GW by FY27, alongside backward integration via a 3 GW solar cell facility in Tamil Nadu.

Capacity trajectory (certified by Independent Chartered Engineer)

| Line | Location | FY24 Installed | FY25 Add | FY26 Add | FY27 Add | Cum. Total by Year |

|---|---|---|---|---|---|---|

| Modules | ||||||

| Falta SEZ, WB | 2.20 GW | 1.00 | – | 2.00 | 3.20 / 3.20 / 5.20 | |

| Oragadam, TN | 1.30 GW | – | – | – | 1.30 / 1.30 / 1.30 | |

| Upcoming TN | – | – | 6.00 | – | 6.00 (FY26) | |

| Upcoming USA | – | – | – | 3.00 | 3.00 (FY27) | |

| Modules (cum.) | 3.50 | 4.50 | 10.50 | 15.50 | ||

| Cells | Upcoming TN | – | – | 3.00 | 2.00 | 3.00 / 5.00 |

IPO details

Offer structure & sellers:

| Item | Details |

|---|---|

| Fresh issue | Up to ₹15,000 mn (price band TBD). The 'fresh issue' refers to fresh issues of shares as part of the solar IPO, raising new capital for the company. |

| Offer for sale (OFS) | Up to 17,450,882 shares: Gyanesh Chaudhary (up to 2,500,000), Vikram Capital Mgmt Pvt Ltd (up to 5,000,000), Anil Chaudhary (up to 9,950,882), and Gyanesh Chaudhary Family Trust as one of the promoters selling shares. |

| Pre-IPO placement (optional) | Up to ₹3,000 mn; if done, reduces fresh size (≤20% of Fresh) |

This solar IPO is a significant event in the renewable energy sector, aiming to boost Vikram Solar's manufacturing capacity and market presence.

Objects of the issue (Fresh proceeds):

Vikram Solar IPO objectives: The net proceeds from the fresh issues will be used for the following objects.

The following objects will be funded:

- Part-fund 3,000 MW cell + 3,000 MW module facility in Tamil Nadu (Phase-I) via VSL Green Power, with a focus on capital expenditure for new manufacturing capacity.

- Fund expansion to 6,000 MW modules at the same site (Phase-II).

- General corporate purposes.

Company Overview

Vikram Solar Limited stands as one of India’s largest solar photovoltaic (PV) module manufacturers, with a robust presence in both domestic and international markets. Established as part of the Vikram Group, the company has built a strong brand reputation over more than 15 years, driven by its commitment to quality, innovation, and sustainability.

Vikram Solar’s manufacturing facilities are strategically located at Falta SEZ in West Bengal and Oragadam in Tamil Nadu, providing excellent connectivity to road networks and ports, which supports efficient distribution and export operations.

The company’s core business revolves around the production of high efficiency PV modules, catering to a diverse clientele that includes utility-scale, commercial, and residential solar power installations. With an installed module manufacturing capacity of 3.5 GW and plans to scale up to 10.5 GW by FY26 and 15.5 GW by FY27, Vikram Solar is actively expanding its footprint.

The company is also backward integrating into solar cell manufacturing, with a 3 GW facility under development in Tamil Nadu, further strengthening its position in the solar value chain.

Vikram Solar’s diversified business model includes providing EPC (Engineering, Procurement, and Construction) services for solar projects, as well as operations and maintenance solutions. Its products are listed on the Renewable Energy’s Approved List of Module Manufacturers (ALMM), and the company has earned multiple international certifications, reflecting its focus on quality and reliability.

With a proven track record, strong financial performance in recent years, and a growing international presence, Vikram Solar is well-positioned to capitalize on the ongoing solar revolution and the increasing demand for renewable energy solutions worldwide.

Financial overview (₹ mn, consolidated)

| Metric | FY22 | FY23 | FY24 |

|---|---|---|---|

| Revenue from operations | 17,303.1 | 20,732.3 | 25,109.9 |

| EBITDA | 586.8 | 1,861.8 | 3,985.8 |

| EBITDA margin | 3.39% | 8.98% | 15.87% |

| PAT | (629.4) | 144.9 | 797.2 |

| Net debt | 5,671.5 | 6,335.9 | 6,926.0 |

| Debt / Equity | 2.00× | 2.02× | 1.81× |

| ROE | −16.44% | 4.05% | 19.67% |

| Current ratio | 1.09 | 1.35 | 1.39 |

Mix shift (FY24 vs FY23): Domestic revenue ₹8,978.6 mn (+71.8% YoY); Exports ₹15,462.6 mn (+244.8% YoY); EPC ₹668.8 mn (−93.9% YoY).

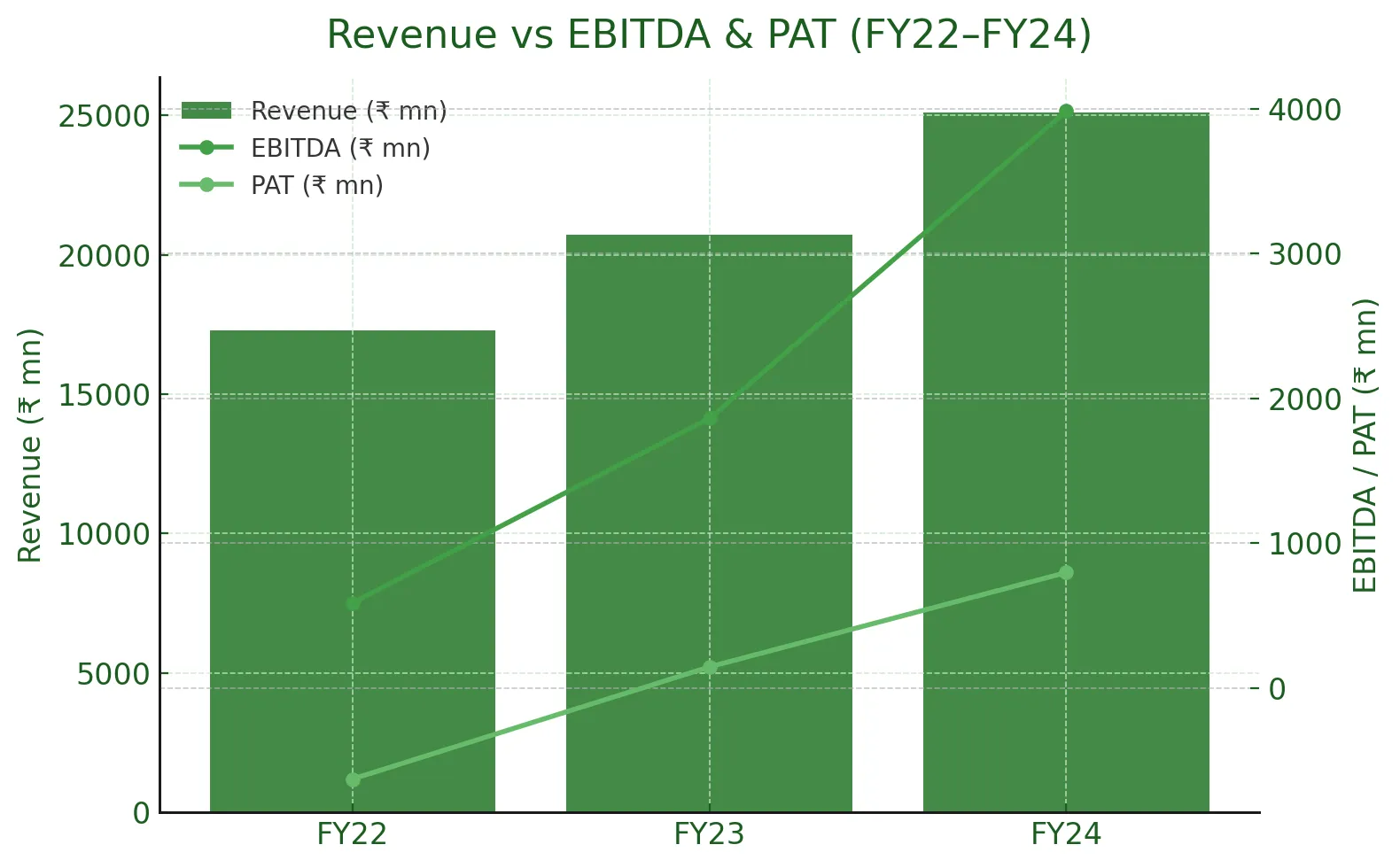

Revenue rose from ₹17,303 mn (FY22) to ₹25,110 mn (FY24) while EBITDA scaled ~7× and PAT swung from a loss (₹-629 mn) to a profit (₹797 mn). This shows both topline growth and a sharp profitability turnaround.

Revenue vs EBITDA & PAT : The company's profit potential is influenced by external factors such as global pandemics, economic conditions, and government policies, which can impact revenue streams and overall financial performance.

Revenue rose from ₹17,303 mn (FY22) to ₹25,110 mn (FY24) while EBITDA scaled ~7× and PAT swung from a loss (₹-629 mn) to a profit (₹797 mn). This shows both topline growth and a sharp profitability turnaround. However, the company's future performance depends on its ability to scale manufacturing, adapt to changing economic conditions, and respond to government policies that may impact profitability and long-term sustainability.

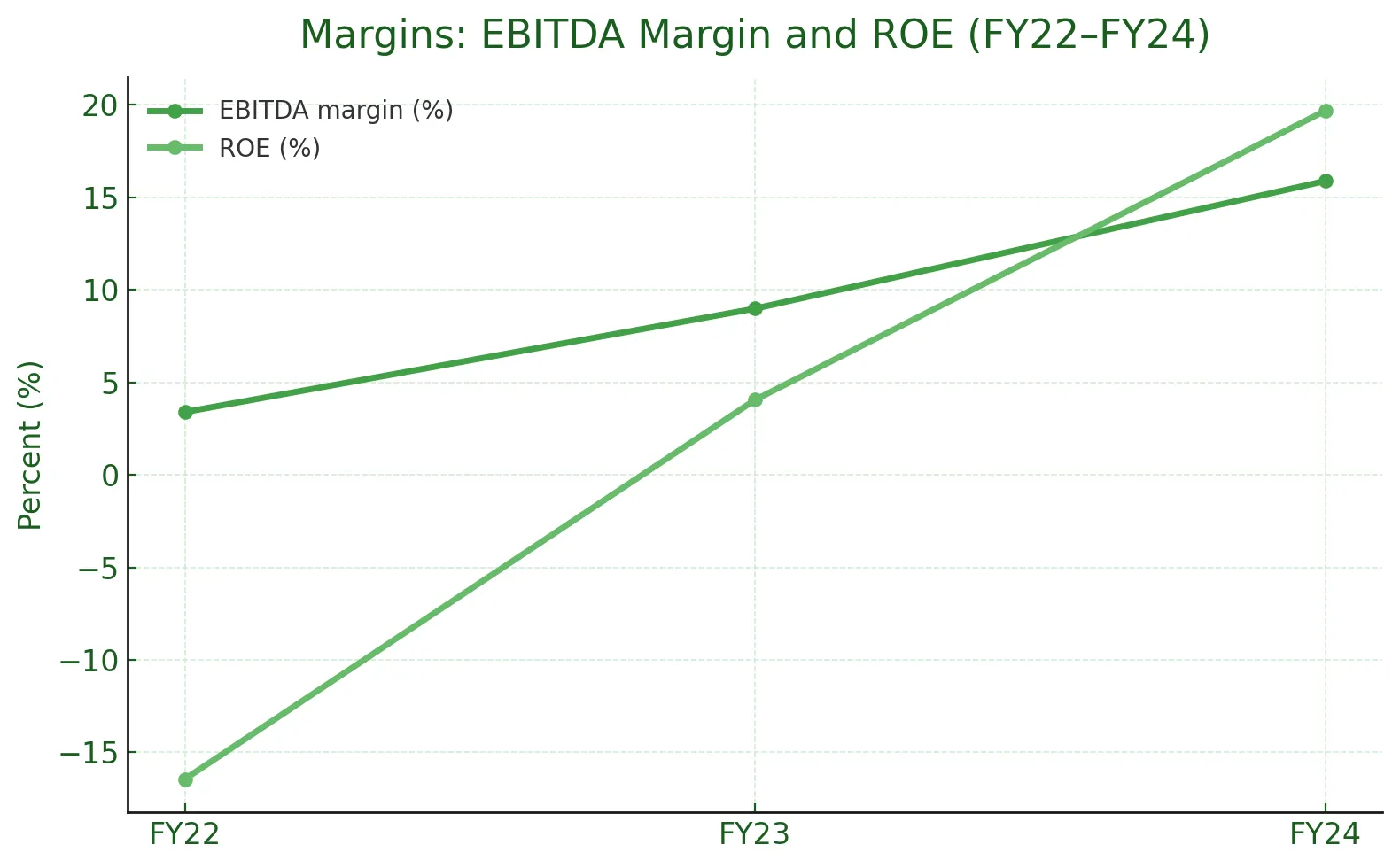

Margins: EBITDA Margin & ROE :

EBITDA margin expanded from 3.39% to 15.87% over FY22–FY24. ROE improved from –16.44% to 19.67%, reflecting stronger operating leverage and better capital efficiency.

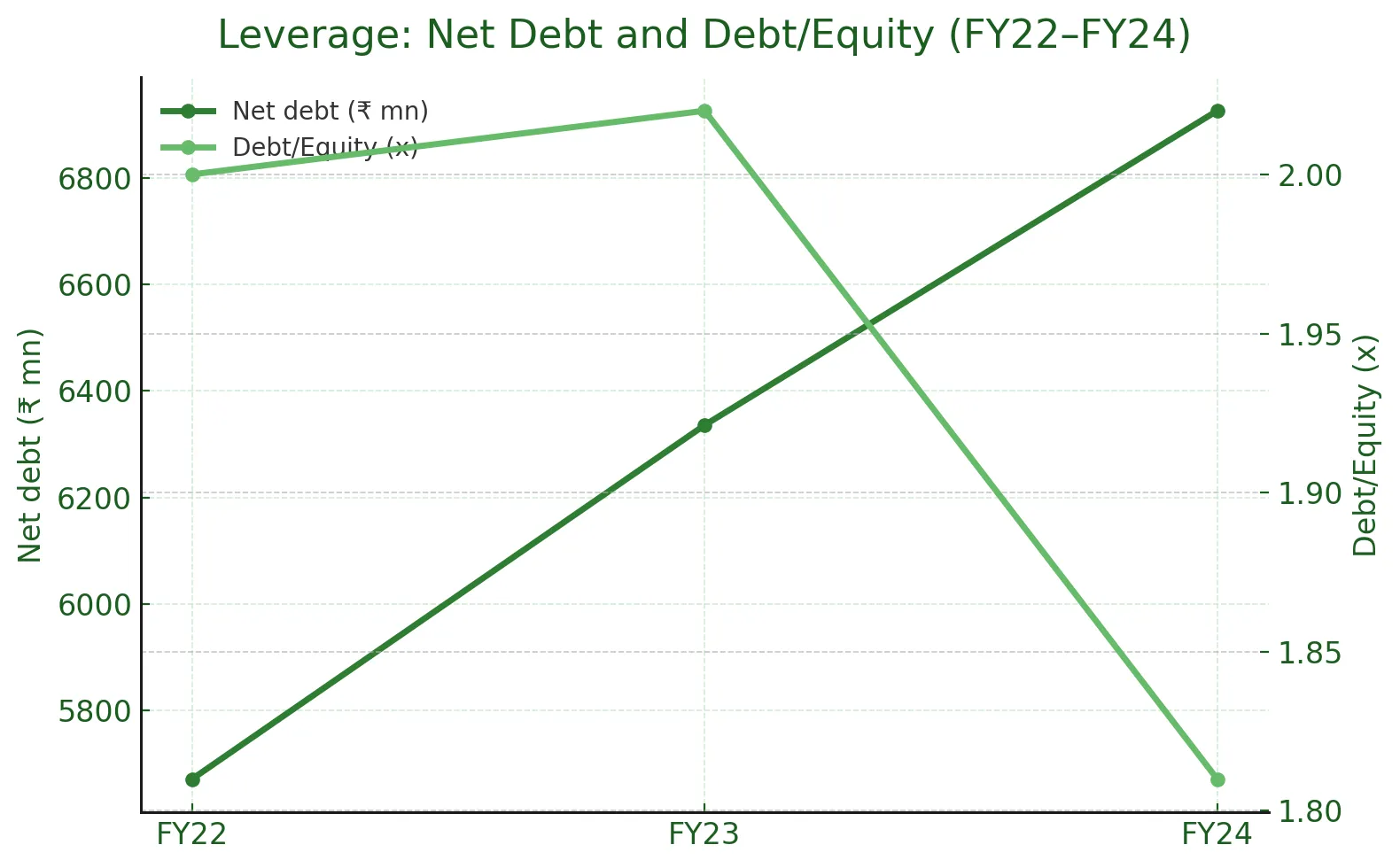

Leverage: Net Debt & Debt/Equity :

Net debt ticked up from ₹5,672 mn to ₹6,926 mn, supporting growth. Even so, Debt/Equity eased from 2.00× to 1.81×, indicating gradual de-risking of the balance sheet.

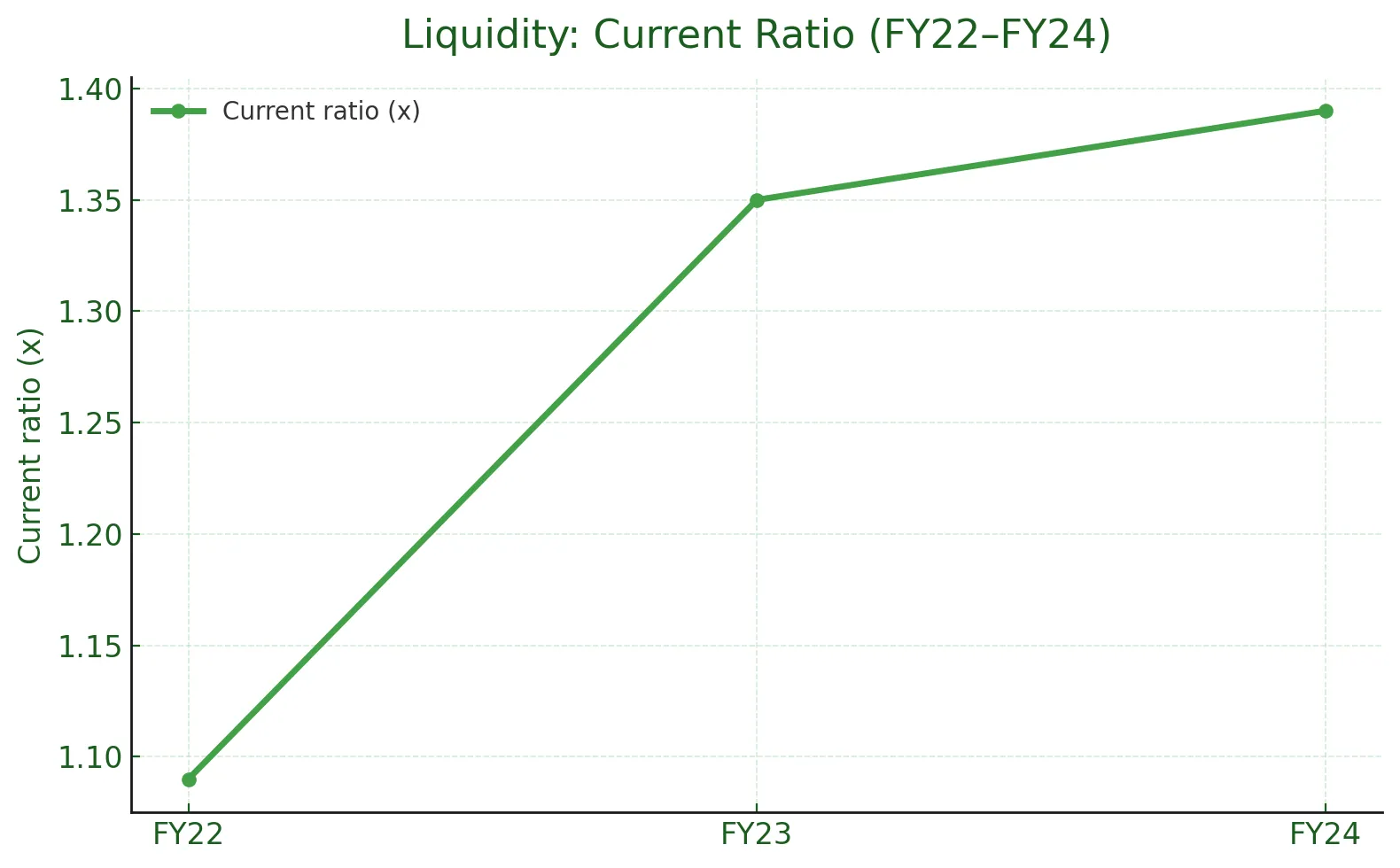

Liquidity: Current Ratio :

The current ratio strengthened from 1.09 to 1.39 across the period. That improvement suggests healthier short-term solvency and working-capital position.

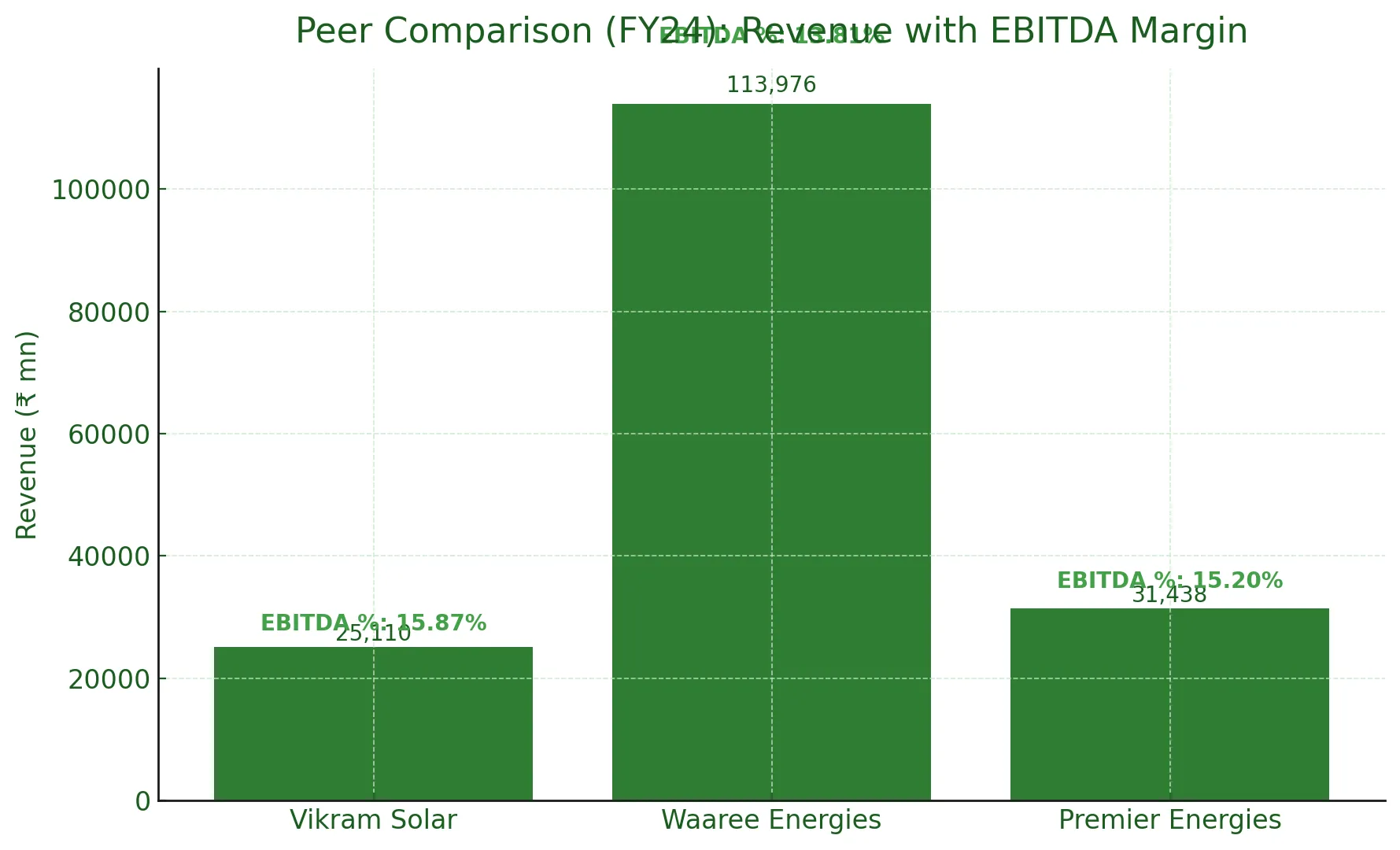

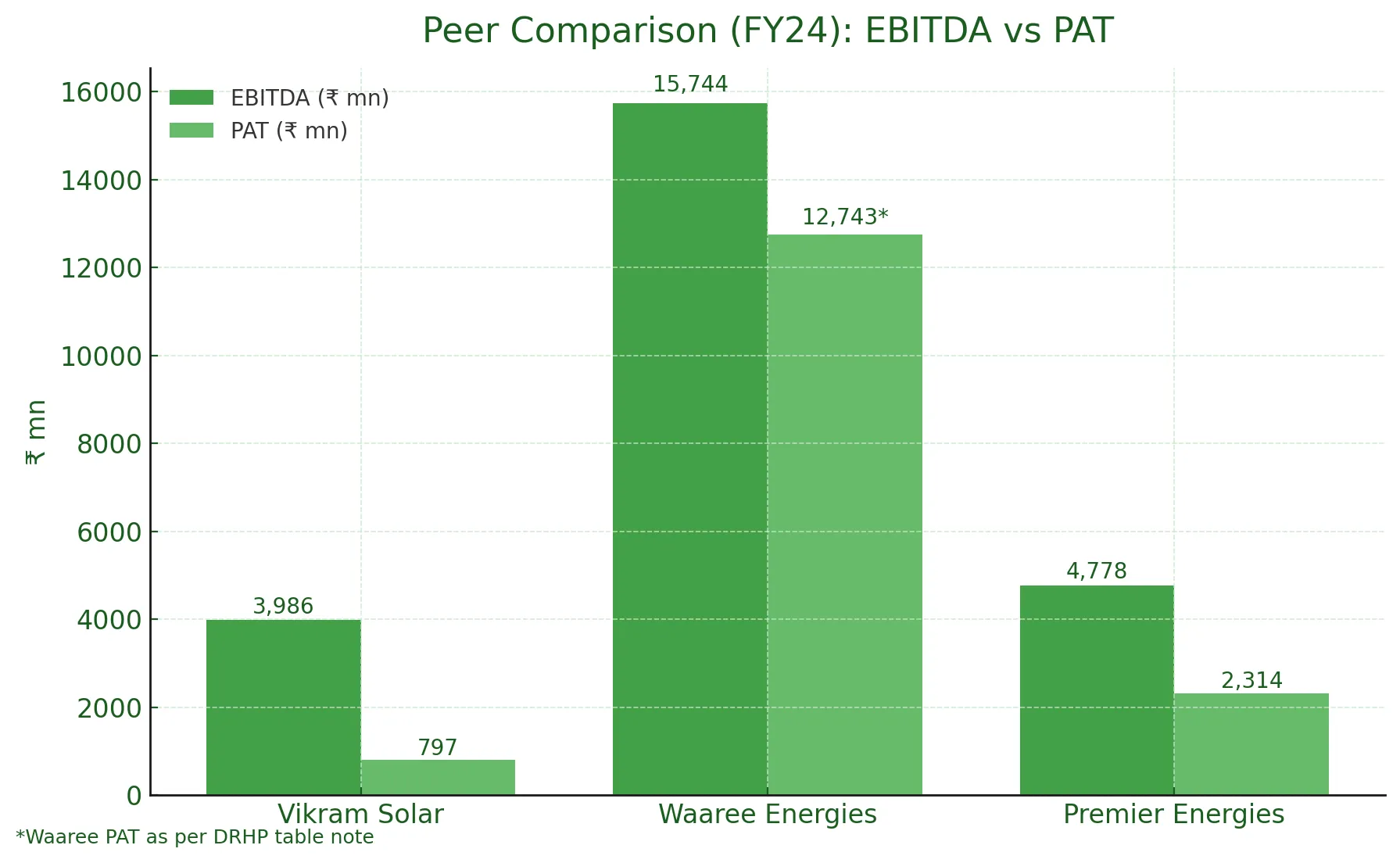

Peer comparison (FY24)

| Company | Revenue (₹ mn) | EBITDA (₹ mn) | EBITDA % | PAT (₹ mn) |

|---|---|---|---|---|

| Vikram Solar | 25,109.9 | 3,985.8 | 15.87% | 797.2 |

| Waaree Energies | 113,976.1 | 15,744.2 | 13.81% | 12,743.* |

| Premier Energies | 31,437.9 | 4,778.0 | 15.20% | 2,313.6 |

(*PAT line continues in the DRHP table.) Data from DRHP’s peer tables.

Vikram Solar is one of India's largest solar photovoltaic manufacturers, with one of the largest enlisted capacities on the Renewable Energy's Approved List (ALMM). The company is often recognized as India's largest solar module manufacturer and is one of India's leading solar companies, with significant installed capacity and strong market presence. Vikram Solar is also a key supplier to major clients such as the National Thermal Power Corporation, underscoring its credibility and market reach.

A broader CRISIL snapshot (Operating income, growth, OPM/NPM, gearing) shows similar relative positioning, with Vikram’s gearing at ~1.8×.

Revenue with EBITDA Margin :

Waaree’s revenue (₹113,976 mn) towers over Premier (₹31,438 mn) and Vikram (~₹25,110 mn). Despite the scale gap, margins are close: Vikram 15.87%, Premier 15.20%, Waaree 13.81%.

Industry Outlook

The solar photovoltaic industry is experiencing unprecedented growth, both in India and across global markets, fueled by the urgent need for clean energy and favourable government policies. India, in particular, has emerged as a key player in the solar revolution, with ambitious renewable energy targets and a supportive regulatory environment that encourages domestic manufacturing and large-scale solar power installations.

The demand for solar PV modules is being driven by a combination of factors: rising energy consumption, declining costs of solar technology, and strong policy incentives such as the Production Linked Incentive (PLI) scheme and the Approved List of Module Manufacturers (ALMM). These initiatives are designed to boost domestic manufacturing capacity, reduce import dependence, and position India as a global hub for solar photovoltaic production.

International markets are also witnessing robust growth, with countries seeking to diversify their energy mix and meet climate commitments. This has opened up significant export opportunities for Indian manufacturers like Vikram Solar, who are recognized for their high efficiency PV modules and strong brand recognition. However, the industry also faces challenges, including unfavourable economic conditions, global pandemics, and evolving trade policies that can impact export dynamics.

Looking ahead, the outlook for the solar PV sector remains positive, with continued investments in capacity expansion, technological innovation, and integration across the value chain. Companies with a proven track record, diversified business models, and the ability to adapt to changing market conditions—such as Vikram Solar—are expected to play a pivotal role in shaping the future of renewable energy, both domestically and internationally.

Waaree’s revenue (₹113,976 mn) towers over Premier (₹31,438 mn) and Vikram (~₹25,110 mn). Despite the scale gap, margins are close: Vikram 15.87%, Premier 15.20%, Waaree 13.81%.

EBITDA & PAT :

EBITDA/PAT stack as: Waaree ~₹15,744 mn / ~₹12,743*, Premier ~₹4,778 mn / ~₹2,314 mn, Vikram ~₹3,986 mn / ~₹797 mn. Profit scale broadly tracks size, with Vikram profitable but smaller versus peers (*Waaree PAT per DRHP note).

Strengths

- Credibility & quality: PVEL Top Performer six consecutive times since 2019; NABL-accredited R&D lab; BIS/IEC/UL certifications; long warranties.

- Scale & expansion visibility: Clear path from 3.5 GW to 10.5/15.5 GW and 3 GW cell integration.

- Track record & locations: >15 years in modules; plants near ports aiding exports & domestic reach.

- Active contributor: Technological innovation, capacity expansion, and policy engagement.

Risks

- Product concentration: 97.34% of FY24 revenue from module sales.

- Customer concentration: Top-5 customers 76.13% of revenue.

- Export/US exposure: 61.58% of revenue from exports; ~99.22% of exports to the U.S.

- Leverage & WC intensity: Pre-offer total debt ₹8,083.3 mn; Debt/Equity 1.81×.

Anything special about the company’s solar IPO?

- Early and repeated PVEL Top Performer

- First Indian company featured in PVEL (2017)

- First 10 kW floating solar in India

- Eligible under PLI scheme

- IREDA sanction for ₹17,000 mn

- Raised ₹7,040.17 mn (Jun-25, 2024) for WC/upgrades

Unlisted shares

Before a company like Vikram Solar Limited lists its shares on a stock exchange through an IPO, its equity is often traded in the unlisted market. Vikram Solar unlisted shares have attracted attention from investors seeking early exposure to one of India’s largest solar photovoltaic module manufacturers, especially given the company’s strong growth prospects and robust financial performance.

In the pre-IPO phase, these unlisted shares are typically bought and sold through private transactions or specialized platforms, allowing investors to participate in the company’s journey before it becomes publicly traded. The price of Vikram Solar unlisted shares in the unlisted market can provide insights into investor sentiment and the company’s perceived value ahead of the IPO.

For retail investors, acquiring pre-IPO shares can offer additional value if the company’s listing is successful and the stock performs well on the listed market. However, it’s important to note that unlisted shares carry certain risks, including lower liquidity and less regulatory oversight compared to listed securities. The transition from the unlisted to the listed market, following the IPO, can unlock new opportunities for both existing and new shareholders, as the company gains broader visibility and access to capital.

As Vikram Solar prepares for its IPO, the interest in its unlisted shares underscores the market’s confidence in its business model, manufacturing capacity, and future performance. The company’s sustainability depends on its ability to execute its expansion plans, maintain strong financial discipline, and navigate the evolving landscape of the solar energy sector.

Conclusion

Vikram Solar enters the market with credible quality markers, a clear expansion/vertical-integration roadmap, and a sharp FY24 profitability step-up. The investment case hinges on execution of TN capex, sustained export demand, and working-capital discipline—while monitoring product/customer concentration, U.S. policy risks, and leverage. Final valuation will depend on the eventual price band.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)