If there’s one word that broadly captures global markets in 2025, it is adaptation.

The year unfolded against a complex backdrop, persistent geopolitical tensions, trade realignments, policy uncertainty, slowing but resilient growth, and rapid technological change. Headlines often leaned toward caution. Yet markets, across regions and asset classes, continued to find their footing.

Rather than a single dominant narrative, 2025 became a year where multiple forces worked simultaneously, shaping investor behaviour and market performance across the world.

A Broad-Based Market Participation

One of the most striking features of 2025 was the breadth of participation across asset classes.

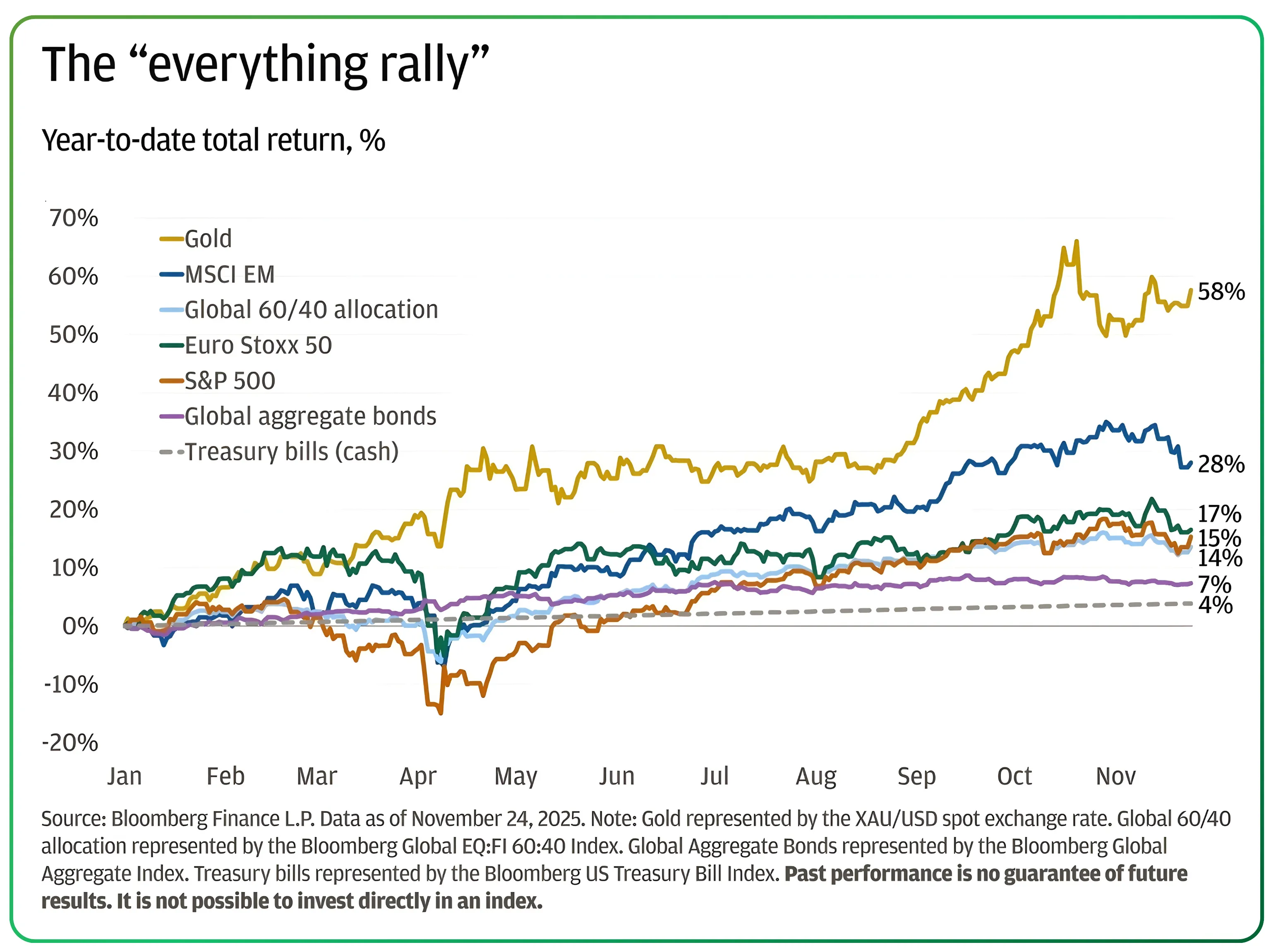

Gold outperformed early, supported by geopolitical risks, central bank buying and easing financial conditions.

Equities outside the U.S. saw renewed interest, particularly in parts of Europe, Japan and select emerging markets, as currency dynamics and valuation gaps became more attractive.

U.S. equities continued to scale new highs, initially led by large technology companies and later supported by financials, cyclicals and segments of the small-cap universe.

Fixed income benefited as expectations shifted toward a more accommodative interest rate environment globally.

This environment created what many described as an ‘everything rally’, not because risks disappeared, but because markets adjusted to them. For investors, this reduced the pressure to rely on a single theme or geography, making diversification more effective than it had been in recent years.

Monetary Policy:

By 2025, global central banks were no longer singularly focused on inflation control. While inflation risks remained uneven across regions, the emphasis gradually shifted toward growth preservation and financial stability.

The U.S. Federal Reserve moved toward precautionary rate cuts as economic momentum cooled, but avoided a sharp downturn.

In Europe, policy easing aimed to support sluggish growth while managing energy and fiscal challenges.

Several emerging market central banks benefited from greater policy flexibility as inflation moderated and currency pressures eased.

Lower yields and a softer U.S. dollar environment provided support not only to equities and credit but also to commodities and emerging markets, reshaping global capital flows.

Markets at Glance of 2025

| Area | 2025 Snapshot (Global Context) |

|---|---|

| Global Equity Trend | Broad-based gains across the U.S., Japan, Europe and select EMs |

| Gold | One of the strongest-performing assets amid global uncertainty |

| U.S. Interest Rates | 3 rate cuts. The Fed lowered the federal funds rate in three consecutive policy decisions through 2025, bringing the target range down to around 3.50%–3.75% by December. |

| Global Growth | Slower than 2024 but more resilient than early-year expectations |

| U.S. Dollar | Moderated after multi-year strength |

| Emerging Markets | Improved stability supported by easing global financial conditions |

| AI Investment | Large-scale capex across data centres, power and semiconductors |

| Geopolitics & Trade | Elevated uncertainty due to conflicts and trade realignments, influencing market sentiment more than economic collapse |

| Reserve Bank of India (RBI) | 3 repo rate cuts. RBI reduced the policy repo rate in February (25 bps), June (50 bps) and December (25 bps), cumulatively lowering the benchmark to 5.25% by year-end |

Economic Durability in a Fragmented World

2025 tested global economic resilience.

The year saw elevated tariffs, disruptions linked to geopolitical conflicts, supply chain adjustments, and political uncertainty across major economies. Growth expectations were repeatedly revised, often downward, before stabilising.

Yet large-scale economic damage was largely avoided.

Corporate balance sheets entered the year in relatively strong shape, allowing firms to absorb higher costs.

Labour markets cooled without widespread layoffs, particularly in developed economies.

Consumer spending proved more resilient than expected, supporting services-led growth even as manufacturing slowed.

Global growth did not accelerate meaningfully, but it endured, reinforcing the idea that post-pandemic economies have developed stronger shock absorbers than in previous cycles.

AI-Led Innovation Cycle Goes Global

While artificial intelligence dominated headlines earlier, 2025 marked the phase where AI shifted from narrative to infrastructure.

The AI cycle was no longer confined to Silicon Valley or the U.S. Market participants across Asia, Europe and emerging economies became part of the broader ecosystem, supplying hardware, energy, talent, data and applications.

This widening footprint reinforced the idea that innovation cycles tend to diffuse across sectors and geographies, rather than remain concentrated indefinitely.

Investor Behaviour

After years of binary positioning, risk-on or risk-off, investor behaviour in 2025 became more selective and pragmatic.

Cash allocations were reassessed as real returns declined.

Portfolios leaned toward balance rather than concentration.

Themes like quality earnings, balance sheet strength and long-term visibility regained importance alongside growth narratives.

Rather than ignoring risks, geopolitical fragmentation, policy uncertainty, valuation concerns or technological bubbles, investors appeared more willing to navigate uncertainty instead of waiting for clarity.

2025 did not eliminate uncertainty. Instead, it demonstrated that markets can function, and even progress, within it.

For investors, the year served as a reminder that opportunity often emerges not from perfect conditions, but from adaptive strategies, diversification and a long-term perspective.

*Source: JP Morgan

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)