Life Insurance Corporation of India (LIC) is not just a legacy brand. It is a critical pillar of India’s financial ecosystem, known for its unmatched scale, trust, and commitment to insuring lives across generations. Established in 1956 through the nationalisation of over 240 private insurers, LIC has grown into a public financial powerhouse serving millions of Indians.

Legacy built on reach and purpose

LIC was formed with a national mandate to provide life insurance to every insurable individual, especially in underserved and rural regions. Over the decades, it has built an expansive network that remains unmatched in its scope. Today, LIC operates with a vast distribution network:

- Over 1.3 lakh agents actively serving customers across India

- More than 2,000 branch offices, 113 divisional offices, and 8 zonal offices

- An increasingly digital interface via mobile apps and online services

- Strategic partnerships with leading banks for premium collection and policy servicing

LIC reported a claim settlement ratio of 98.45% in FY 2023–24, which is among the highest in the Indian insurance sector.

How LIC runs its business

LIC’s business model is simple yet deeply strategic. It collects premiums from customers, invests them wisely, and offers life protection and long-term financial benefits.

Premium collection

Customers pay periodic premiums for insurance coverage. The amount depends on their age, health, income, and policy type. LIC’s rigorous underwriting process, supported by actuarial methods, ensures premiums are priced fairly and sustainably.

Investment strategy

LIC’s high solvency ratio is maintained by investing over 75% of collected premiums in government securities and sovereign-backed bonds, ensuring capital safety and long-term stability. The remaining corpus is strategically deployed across equities, corporate bonds, and infrastructure projects, achieving diversification to enhance returns while managing risk. These investments fuel claim payouts, bonuses, and operational expenses.

Risk cover and claims

In the event of a policyholder’s death, LIC pays the assured sum to the nominee, supported by reinsurance arrangements to manage large or unexpected claims effectively. On maturity, the insured receives accumulated benefits along with any applicable bonus. The claim process is carefully audited to maintain transparency and prevent fraud.

Bonus payouts

LIC shares part of its surplus with policyholders holding participating plans. These annual or final bonuses increase the total benefit received at maturity or claim.

Loans and surrender options

Several plans allow policyholders to take loans or exit the policy early through a surrender, offering financial flexibility when needed.

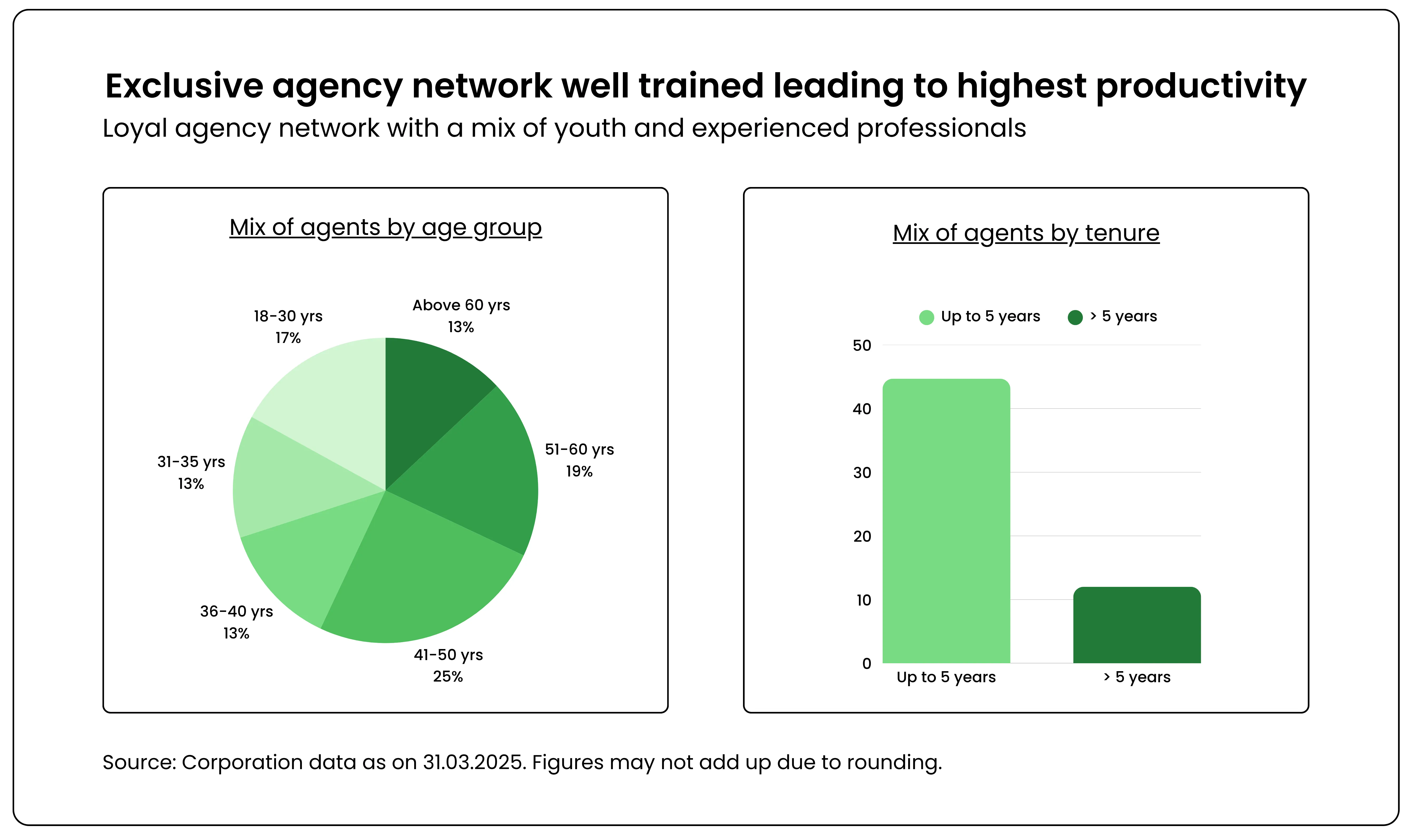

LIC’s agent network and training strength

LIC’s strong distribution network is one of its greatest strengths, with a vast agent and employee base ensuring last-mile insurance delivery across India. As of March 31, 2025, LIC has a total of 14.87 lakh agents, backed by an extensive organizational structure that includes 1,584 satellite offices, 2,130 branch offices, 113 divisional offices, 8 zonal offices, and the corporate office. A significant 94.81% of LIC’s total employees are stationed at the branch and divisional offices, directly supporting operational and customer-facing functions. To maintain and upgrade agent capabilities, LIC has built a comprehensive training ecosystem, comprising 576 agent training centers, 113 divisional training centers, 35 sales training centers, and 8 zonal training centers. In FY25 alone, 5.31 lakh agents were trained, highlighting LIC’s commitment to field readiness and customer service excellence. Products that serve every generation.

LIC agents and their commissions

LIC agents earn money primarily through commissions paid on the sale and servicing of insurance policies. Their income is categorized into three main types: first-year commission, renewal commission, and performance-based bonuses. When an agent sells a policy, they receive a first-year commission, which can range from 5% to 35%, depending on the policy type and tenure. For example, endowment plans with terms of 15 years or more offer up to 25%–35% commission in the first year. After that, LIC agents continue to earn renewal commissions, typically 5% to 7.5% for every year the policy remains active. This creates a stable stream of recurring income, making the profession financially rewarding in the long run. Beyond this, LIC also incentivizes agents with performance bonuses, foreign trips, and rewards for meeting sales targets. Special plans like single-premium policies have a flat 2% commission. Importantly, agents who build a sizable client base can enjoy lifetime passive income as long as their clients continue paying premiums. Over time, high-performing agents may move into managerial roles, mentoring new agents and earning additional incentives. Thus, LIC agents earn not just from sales but also from service, performance, and leadership growth within the organization.

LIC offers diverse portfolios of plans to meet financial goals, including protection, savings, retirement, and investment. Its product categories include:

- Term Insurance for pure life cover

- Endowment and Savings Plans for guaranteed returns

- ULIPs for market-linked growth

- Money-back Policies for periodic returns

- Whole-life Plans for lifelong coverage

- Annuity-based Pension Plans for steady income in retirement

- Child and Women-focused Plans tailored to family needs

Going digital while staying grounded

LIC is modernizing its customer experience by strengthening its digital presence while retaining its traditional service model. Through the LIC mobile app and online portal, policyholders can now pay premiums, track policy status, download premium receipts, apply for loans or surrender their policies, and check maturity values or claim status, all from the comfort of their home. This digital shift has made policy management more accessible and efficient, especially for younger, tech-savvy customers, without disrupting the familiarity and trust associated with LIC’s vast agent network.

These services offer convenience without removing the personal touch of LIC’s agent network.

Also Read: The story behind Hindustan Unilever

LIC IPO and market presence

LIC launched its Initial Public Offering (IPO) on May 4, 2022, becoming the largest IPO in Indian history at the time, raising over ₹21,000 crore, and marking a strategic move by the Government of India to unlock value from its crown jewel. Priced at ₹949 per share, LIC listed at a discount and has since seen a mixed journey on the bourses. In its early days post-listing, the stock witnessed pressure due to market volatility, global cues, and concerns around profitability and growth amid rising competition from private insurers.

However, over time, investor confidence has improved, supported by consistent premium collections, a high claim settlement ratio, and LIC’s long-term investment strength. As of mid-2025, LIC's share price has recovered significantly and is being watched closely for dividend potential, stability, and its role as a defensive stock in a volatile market. Analysts often view LIC as a long-term value play given its dominant market share, vast distribution network, and strong embedded value. The IPO not only broadened LIC's investor base but also introduced a more performance-driven structure to what was once a purely state-run entity.

LIC Investment Portfolio (General Fund, FY 2024–25)

| Asset Class | Approx. Allocation |

|---|---|

| Central Government Securities | ~37 % |

| State Government Securities | ~25 % |

| Corporate Bonds (inclusive of debentures) | ~30 % |

| Equities | ~5–6 % |

| Others (real estate, policy loans, cash) | ~3–4 % |

Beyond insurance

LIC is also a major institutional investor. It plays a significant role in funding infrastructure, housing, power, and public sector projects, channelling long-term savings into national development. Its investments often align with government priorities, contributing to the larger economic framework.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.