What if you could replicate the exact payoff of buying a stock without actually buying it? Sounds like a financial hack, right? Welcome to the world of Synthetic Long positions, a powerful tool for traders looking to gain equity-like exposure using options.

In this blog, we’ll explain what a synthetic long is, how it works, why it’s different from simply buying the stock in the cash market, and when you might want to use it. Whether you’re an intraday trader or just looking to optimize your capital, this strategy deserves your attention.

What Is a Synthetic Long Position?

A synthetic long position is created using options to mirror the payoff of underlying stock. Instead of buying the stock in the cash market, you

- Buy an ATM (At-the-Money) Call Option

- Sell an ATM Put Option

Both must have the same strike price and expiry date. This combination mimics the risk/reward profile of owning the underlying stock.

Advantages of Synthetic long

When deciding between a synthetic long and buying stock in the cash market, a synthetic long offers several advantages. It requires low capital, using only margin instead of the full stock price, making it more capital-efficient. It also provides leverage, allowing greater exposure with less money, and eliminates the need for delivery, avoiding settlement hassles. Additionally, its high flexibility and intraday-friendly nature make it ideal for short-term directional trades

When to Use Synthetic Long?

- You’re confident about the stock moving up.

- You want stock-like exposure but want to free up capital.

- You’re looking for intraday or short-term positions without delivery.

Synthetic Long in Action on NXToption

On the NXToption platform, freely accessible to all Tradejini customers, setting up a Synthetic Long position is straightforward and efficient. The platform’s intuitive interface enables users to:

- Navigate to the Strategy Builder section

- Search and select the desired stock

- Click on Build your Strategy, then Buy a Call Option and Sell a Put Option ( Make sure to select the same strike and lot size for both call and put).

- Click on Trade and Execute. And Just like that, the Synthetic Long strategy is executed.

It’s a smart way to participate in market moves with lower capital and higher flexibility.

Also Read: Beginner's Guide to Option Trading

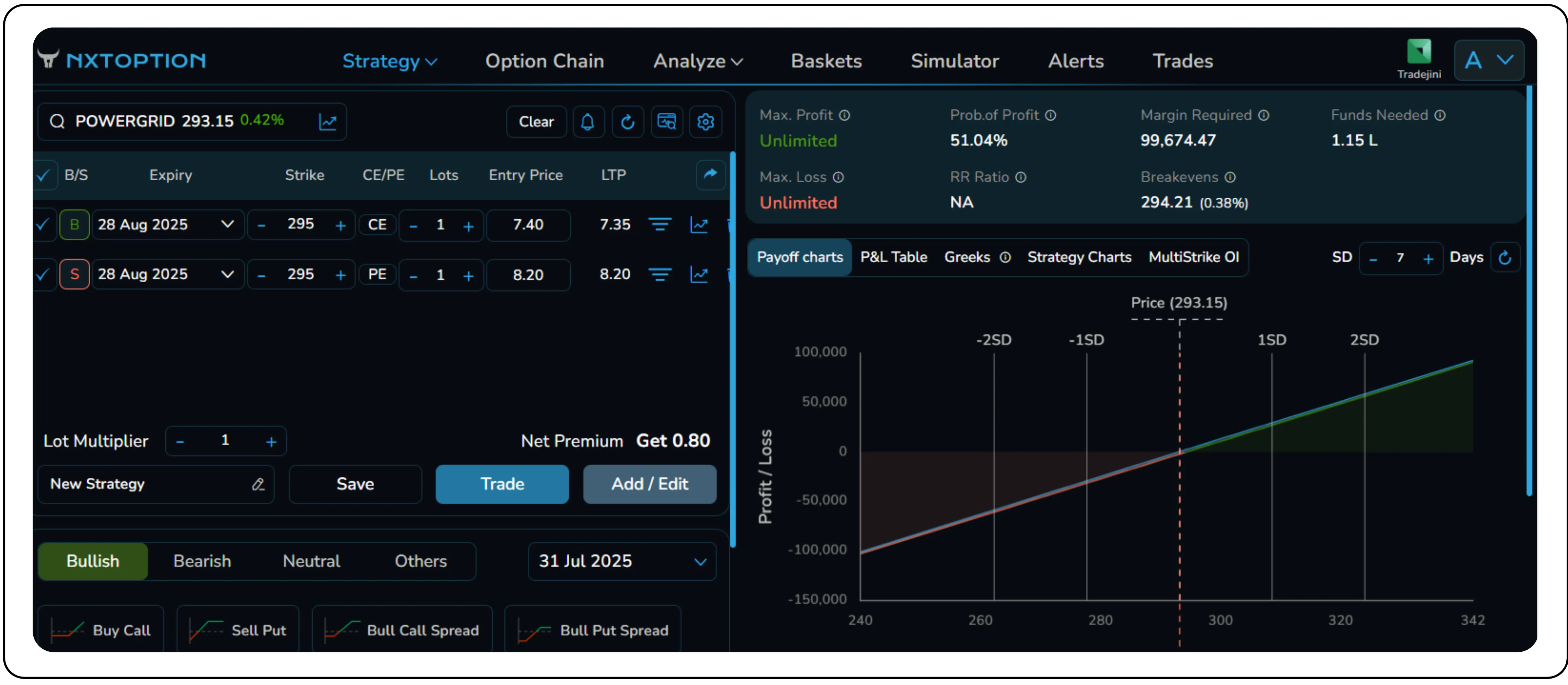

The strategy shown in the image is a synthetic long position on PowerGrid, created using options with the same strike and expiry. This involves buying a 295 Call at ₹7.40 and selling a 295 Put at ₹8.20, both expiring on 28th August 2025.

Since the strike price is the same and the expiry matches, this position mimics the payoff of buying the stock directly. The net premium received is ₹0.80 (₹8.20 – ₹7.40), which makes the breakeven point ₹294.21 (strike price minus net credit). The maximum profit is unlimited if the stock moves upward beyond ₹294.21, and the maximum loss is also unlimited if the stock falls below ₹294.21, just like holding the stock itself.

This strategy is typically used when a trader is bullish and wants to gain long exposure without buying the stock outright. Compared to directly purchasing PowerGrid shares (which would require ₹5,59, 000 for 1900 shares, the margin required here is ₹99,664.50

The NXTOption payoff chart clearly shows profits beyond ₹294.21 and losses below that level. While the upside potential is attractive, traders must be cautious, as the downside risk is significant due to the short put position.

The Greeks table shown in NXT Options here explains how your synthetic long position on PowerGrid (295 CE Buy + 295 PE Sell) reacts to various market factors. Here's a breakdown of each Greek and its interpretation:

Delta = 1.00 (Total)

- Call Delta = +0.50, Put Delta = +0.51

- Combined = 1.00, which mimics the Delta of a long stock.

- Interpretation: For every ₹1 move in PowerGrid’s price, your position gains (or loses) ₹1 — just like holding the stock.

Theta = -0.04

- Call Theta = -0.15, Put Theta = +0.11

- Combined net = -0.04, meaning the position loses ₹0.04 per day due to time decay.

- Interpretation: Slightly theta negative — you're paying a small daily cost to hold this position. That's because long calls lose more time value than the gain from short puts.

Decay = -0.03

- Similar to Theta but shown as a combined decay effect. You’re losing ₹0.03 daily due to time passage (decay of extrinsic value).

Gamma = -0.0006

- Call Gamma = +0.0202, Put Gamma = -0.0208

- Combined = Very close to zero

- Interpretation: Your Delta won’t shift dramatically with small changes in stock price. This gives you a stable directional exposure, like stock ownership.

Vega = 0.00

- Call Vega = +0.34, Put Vega = -0.34

- Combined = 0.00

- Interpretation: The position is not sensitive to implied volatility changes, which is a key feature of synthetic stock. Rise or fall in IV won’t affect your P&L significantly.

Ready to trade smarter? Explore NXToption

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.