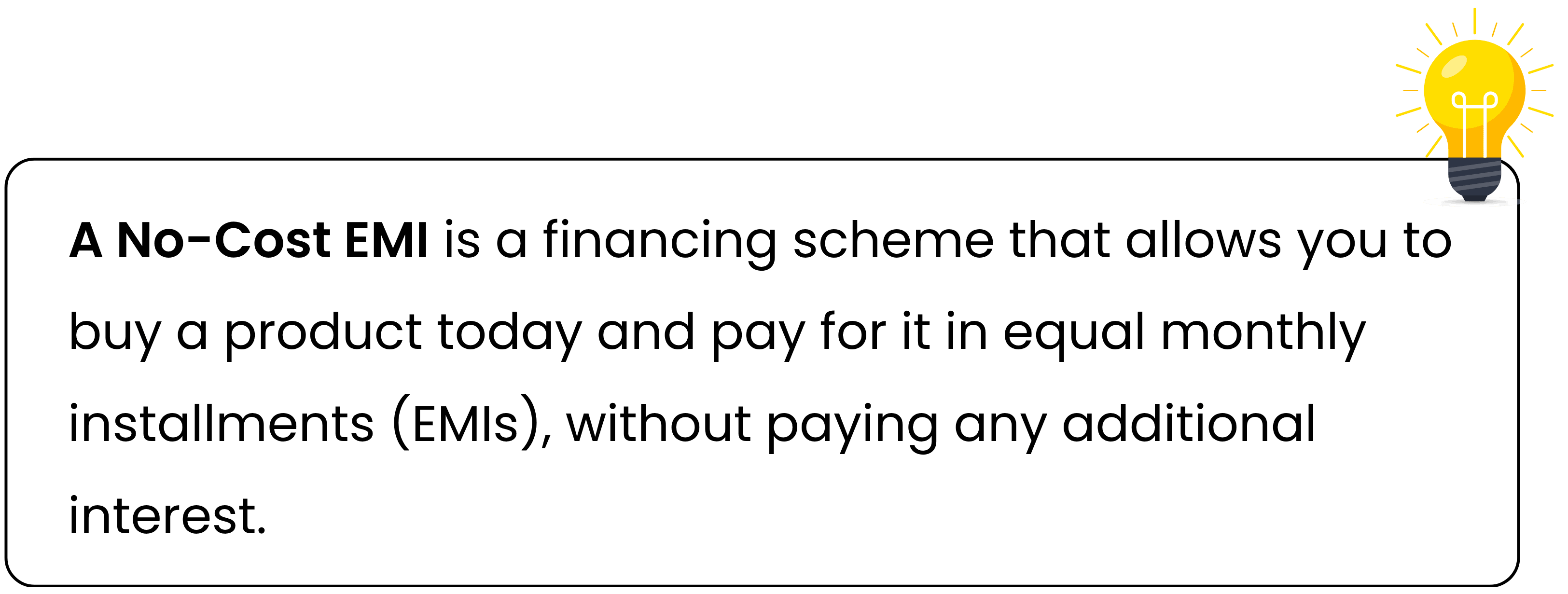

This festive season, every e-commerce app is promoting ‘0% EMI!’, 'No Cost EMI!’, ‘Buy Now, Pay Later.’ Tempting, for sure. But before you swipe right on that offer, pause. What if a smarter strategy is to save first and spend later?

Let me walk you through this with 2025 numbers in true Tradejini style.

Riya’s 2025 Dilemma (A Realistic Example)

Riya’s eyeing a flagship laptop priced at ₹5,00,000. She has two options:

Option 1 (EMI):

Buy today via a 5-year EMI at 12% p.a. (consumer electronics may attract 10%–20% interest depending on bank/OEM deals).

Option 2 (SIP & Wait):

She commits to saving via a mutual fund SIP for 5 years, then spends her corpus (perhaps paying a bit more due to inflation, but with gains from her investment).

Know how our intern made the most of her ₹20,000 stipend at just the age of 20? Read her story now.

The Numbers

First, a caveat: mutual fund returns are never guaranteed. However, let’s use a reasonable benchmark; many equity/multi-cap funds in India yield 12% per annum (with fluctuations). And consumer EMI rates for such purchases often lie in the 10%–16% zone, depending on tenure, brand, and campaign.

Let’s compare both paths EMI vs SIP to see which one truly builds Financial Discipline 2025 and keeps her stress-free.

| Scenario | Present cost/target | Interest/return assumption | Tenure | Monthly outflow | Total outflow/value |

|---|---|---|---|---|---|

| EMI route | ₹5,00,000 (buy now) | 12% p.a. | 5 years (60 months) | ₹11,122 | ₹6,67,333 |

| SIP → Buy later | Future price (inflation 5% yearly) → ₹6,38,000 | 12% p.a. on SIP | 5 years | ₹7,736 | Corpus ₹6,38,000, total invested ₹4,64,179 |

So you see, under these assumptions, opting for the SIP route means you are investing ₹4.64 lakh over 5 years but end up with a corpus of ₹6.38 lakh enough to buy the higher price in future, instead of coughing up ₹6.67 lakh via EMI today.

The difference here is over ₹2 lakh saved (or earned) in relative terms — and zero debt.

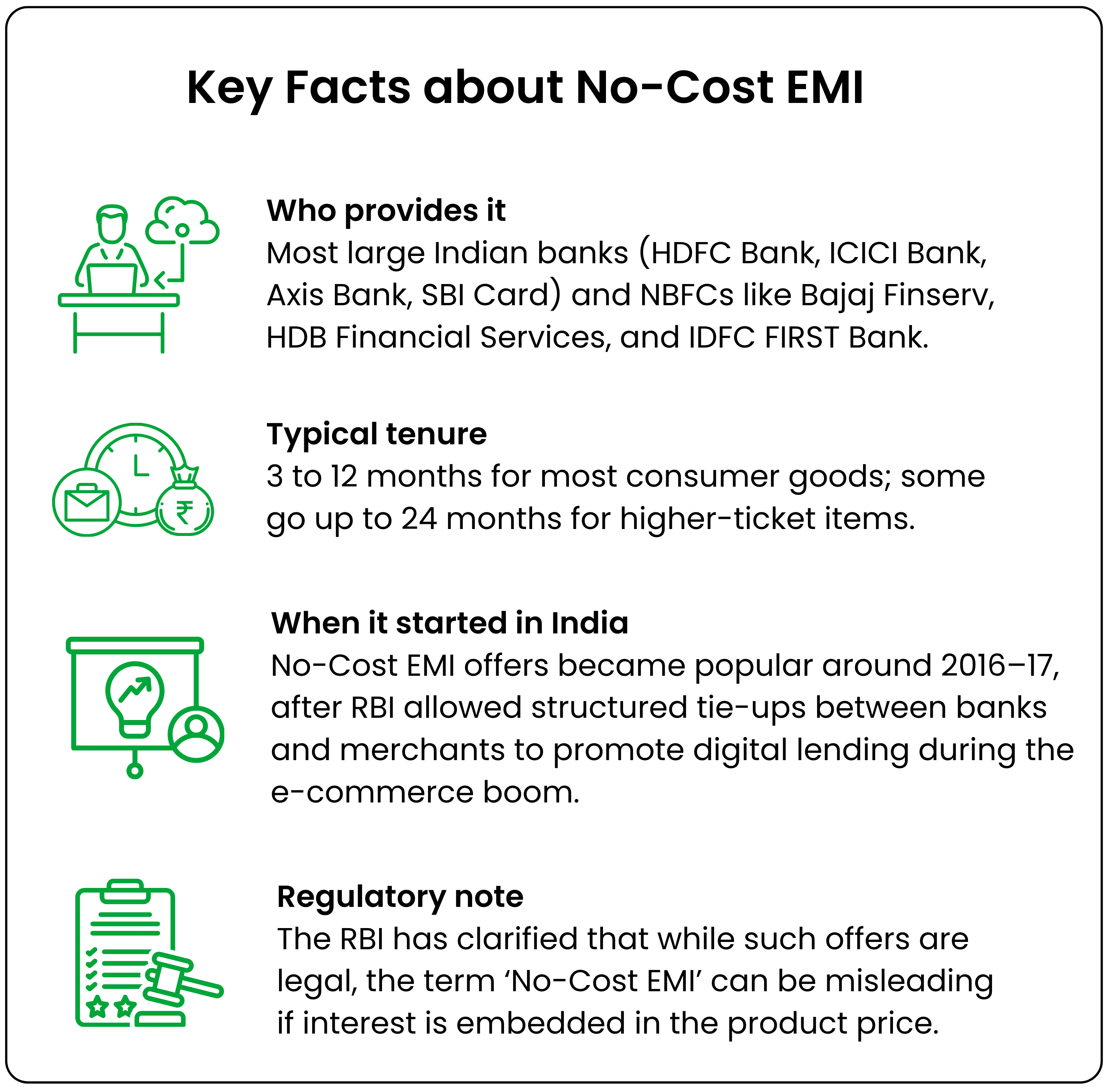

Pros and Cons of No-Cost EMI

| Pros | Cons |

|---|---|

| 1. Easy affordability: Lets you spread out payments without paying visible interest. | 1. Hidden costs: You might lose out on upfront discounts or cashback that others get on full payment. |

| 2. Boosts purchasing power: Helps buy gadgets, appliances, or education courses without an immediate burden. | 2. Short-term credit trap: Encourages impulsive buying and dependence on BNPL schemes. |

| 3. 0% interest (technically): If structured properly by the brand, you truly pay zero interest. | 3. Pre-closure restrictions: You may have to pay extra charges if you close early. |

| 4. Improves credit score (if paid on time): Regular repayments reflect good credit behaviour. | 4. Processing fees and GST: Some cards add a small processing fee plus GST. |

| 5. No collateral: Only a credit/debit card or NBFC link-up is needed. | 5. Not truly free: In many cases, the retailer bears the cost, meaning you pay indirectly via adjusted MRP. |

Why ‘Save First, Spend Later’ Wins

Tradejini always advocates a Debt-Free Buying Strategy, where you plan, save, and invest for what you want instead of committing future income. Here’s why:

You owe nobody:

With EMI, your first few years are heavily interest. With SIP, you own your money and the gains.Life is unpredictable:

Lose a job? Fall sick? With EMI, defaulting is risky. With SIP, skipping an installment doesn’t ruin everything; your invested money still works.Compounding works silently:

Each SIP install ment earns on earnings a core principle of Compounding vs Interest.Inflation is real:

The gadget might cost more later, but your investment can grow too.EMI schemes often have hidden costs:

Processing fees, late fees, GST, etc. Some ‘0% EMI’ offers actually bake cost in other ways.

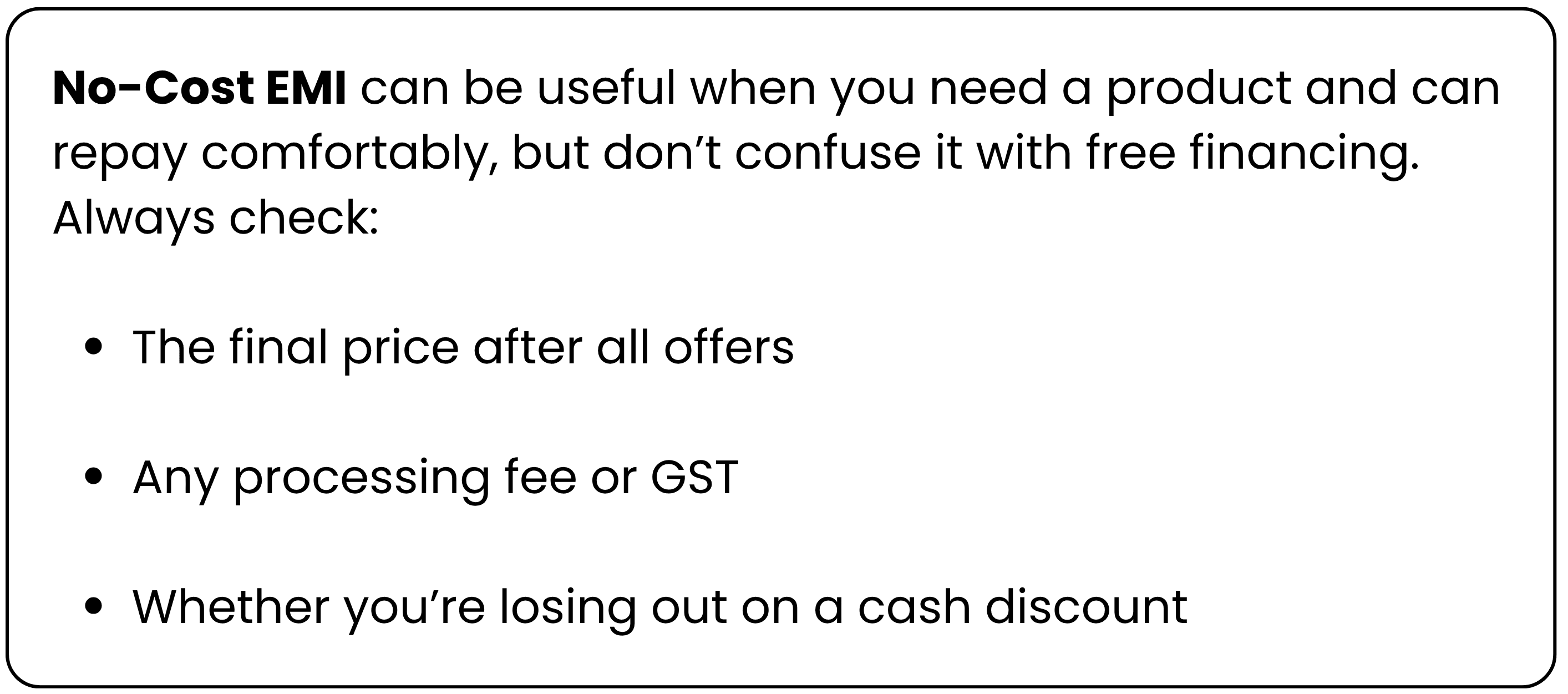

When EMI Might Still Make Sense

- Urgent or medical purchase.

- Genuine No Cost EMI with zero processing fee and no inflated MRP.

- Stable income and low overall EMI burden (below 40% of post-tax income).

Even then, ensure EMI obligations stay well under 40% of your net income.

So, What’s the Smarter Festive Move?

This festive season, make your Festive Season Finances about balance and control. Invest, don’t borrow.

Keep your buying strategy for 2025 simple and build your SIP for Future Purchase plan and start it today with CubePlus on Tradejini. Because in the long run, financial freedom feels better than instant gratification.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.