Yuken India Limited, founded in 1976 in technical collaboration with Japan’s Yuken Kogyo, is a leading Indian manufacturer of oil-hydraulic equipment. Headquartered in Bengaluru, the company manufactures hydraulic pumps, valves, cylinders, and power packs for various industries, including automotive, construction, steel, and power generation. It exports to nearly 19 countries. Its marquee clients include Tata Steel, JSW Steel, Mahindra, Honda, JCB and others. Yuken operates through two segments: (1) Hydraulics (pumps, control valves, power units and custom systems) and (2) cast-iron castings via subsidiary Grotek Enterprises and renewable-energy investments). In recent years, it has also invested in wind power through its associate Aepl Grotek Renewable Energy (wind farms).

Hydraulic systems are Yuken India’s core products, serving sectors from construction to defense. Yuken India’s production footprint spans nine plants across Karnataka, Maharashtra and Haryana. Its combined capacity is substantial, with approximately 90,000 pumps, 780,000 valves, and 20,000 hydraulic power packs per year, enabling it to meet large OEM orders. The company also operates Grotek Enterprises (a wholly owned subsidiary making precision castings and assemblies) and holds an increasing stake in Aepl Grotek Renewable Energy Pvt Ltd, a wind-power developer. This diversification into renewables aligns with India’s clean-energy ambitions.

Sector and Clients

| Sector | Clients |

|---|---|

| Power | BHEL, Alstom, Jyoti Ltd. |

| Steel | TATA Steel, SAIL, ESSAR |

| Machine tools | NIEHOFF, MAKINO, Tussor |

| Plastics | TOSHIBA MACHINE, MODTECH |

| Mobile equipment | JCB, ESCORTS |

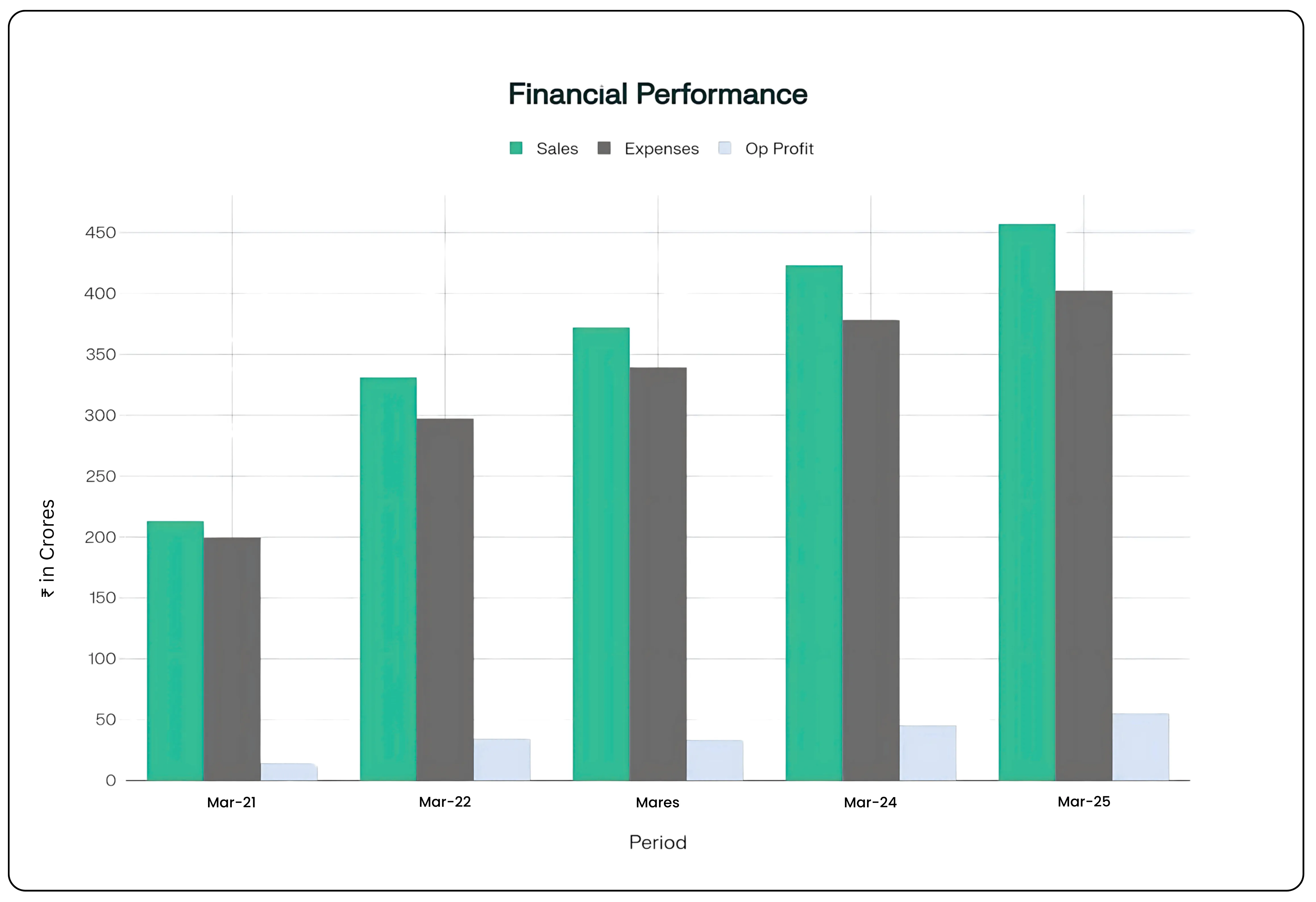

Financial performance

Yuken India’s FY2024-25 results show strong growth in sales, though profitability was under pressure from higher costs. Key financials (consolidated) are:

Revenue

₹457.36 crore in FY25 (up 8.2% from ₹423 cr in FY24). This growth was driven by higher volumes in automotive, infrastructure and capital-goods segments.

Net profit

₹25 crore in FY25 (up 30.8% from ₹19 cr in FY24). The profit jump reflects operating leverage, as expense growth was partially contained.

Q4 FY2025

In the Jan–Mar 2025 quarter, revenue was ₹124.65 crore (+4.55% YoY) and net profit ₹7.85 crore, showing a rebound from the previous quarter.

| Particulars | Mar-21 | Mar-22 | Mar-23 | Mar-24 | Mar-25 |

|---|---|---|---|---|---|

| Sales | 213 | 331 | 372 | 423 | 457 |

| Expenses | 199 | 297 | 339 | 378 | 402 |

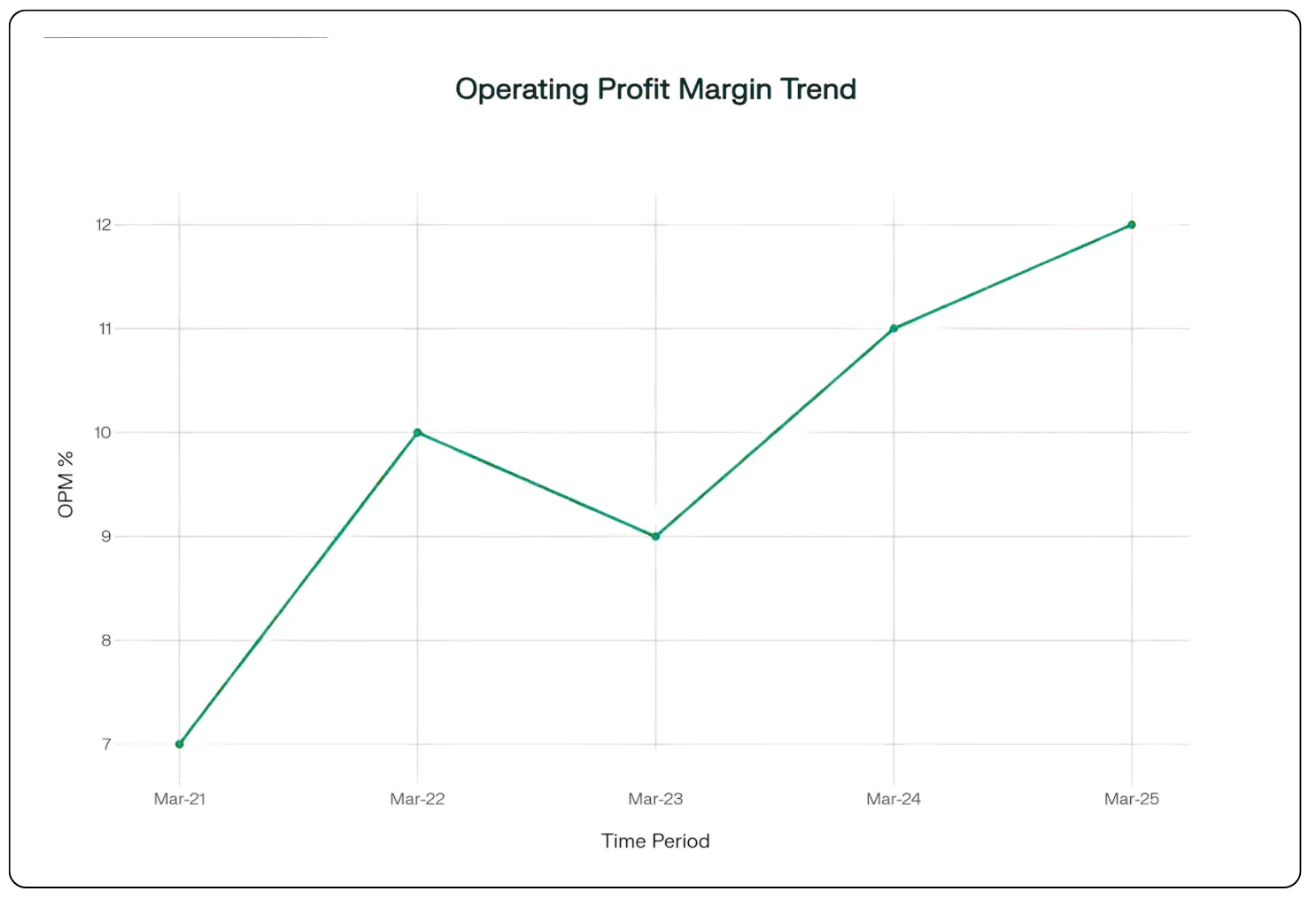

| Operating Profit | 14 | 34 | 33 | 45 | 55 |

| OPM % | 7 | 10% | 9 | 11% | 12% |

| Other Income | 10 | 4 | 5 | 5 | 4 |

| Interest | 10 | 8 | 10 | 8 | 10 |

| Depreciation | 9 | 10 | 13 | 15 | 17 |

| Profit before tax | 6 | 19 | 16 | 27 | 32 |

| Tax % | 11% | 32% | 40 | 30% | 22% |

| Net Profit | 5 | 14 | 10 | 19 | 25 |

| EPS in Rs | 4.38 | 11.42 | 7.98 | 14.48 | 18.94 |

Despite the good topline growth, management noted cost inflation pressures (especially steel and electronic components) that squeezed margins. Yuken pointed to rising input expenses and global supply-chain volatility as key challenges. In FY25 the company also absorbed investments in new projects and R&D. Yuken also declared a 15% final dividend (₹1.5 per share) for FY25, reflecting steady cash flow and shareholder returns.

Market position and outlook

Yuken India is a well-regarded player in the domestic hydraulics market, alongside global competitors like Bosch Rexroth and Parker Hannifin, and faces low-cost imports from China. Its technical tie-up with Yuken Japan gives it an edge in advanced designs and quality. It has built solid in-house capabilities (e.g. ISO-certified design and testing labs) and an extensive service network (45+ channel partners nationwide).

Wind turbines symbolize Yuken India’s entry into renewable energy. The company’s stake in wind-power projects positions it to benefit from India’s clean-energy targets.

The company offers a variety of environmentally friendly products designed to promote sustainability and operational efficiency:

Kiriko Automatic Chip Compactor Machine: This metal chip briquette machine is capable of processing various types of ferrous and non-ferrous scrap. It contributes to workplace safety by reducing accidents and diminishing power consumption, as well as minimizing fumes and blast risks within factory premises.

Power saver valves: These valves are designed to reduce overall power consumption in industrial operations.

AC servo motor-driven pump: Widely supplied for use in injection moulding machines, this product helps lower noise levels and electrical interference through the use of EMC filters.

Looking ahead, Yuken is well-placed to benefit from India’s infrastructure and industrial growth. Its entry into wind-energy (via Aepl Grotek) aligns with national goals. Yuken’s renewables push could open new revenue streams in the coming years.

However, challenges remain. The company itself flags “rising input expenses” and stiffening global competition. Higher commodity prices (steel, copper, electronics) may continue to pressure margins. Yuken plans to mitigate this through localization of parts, cost controls and the higher-value product mix.

In summary, Yuken India remains a leader in Indian hydraulics with a long track record of quality and customer service. Its recent Tata award and financial results underscore operational strength, while the foray into wind energy and capacity expansion indicate a drive toward future growth. By leveraging its global partnerships, diversified products and improving domestic demand, Yuken is positioned to navigate near-term headwinds and capitalize on India’s infrastructure and renewable energy boom.

Investment implications

P/E Ratio:

The high P/E of 59.5 reflects market optimism but also increases valuation risk. Investors should assess whether future earnings can justify this premium, particularly given the company’s exposure to high-growth sectors.

Sales growth

Consistent double-digit sales growth (11% YoY) is a positive signal, supported by Yuken India’s strong market position and promoter backing (Rs 59 crore investment in July 2025). This growth aligns with industry tailwinds in infrastructure and manufacturing.

PEG Ratio

The elevated PEG ratio 1.16 suggests the stock may be overvalued relative to its growth potential. Investors seeking value may prefer to wait for a price correction or stronger earnings growth to improve the PEG ratio.

Risks

Profit Margin Pressure

Despite strong sales,the company faces potential cost pressures that could impact EPS growth and the PEG ratio.

Market Volatility

The stock’s high beta (1.38) and recent volatility (4.68%) increase risk, particularly for short-term investors.

Sector Cyclicality

The hydraulic equipment industry is sensitive to economic cycles, which could affect sales and earnings growth.

Hydraulic precision and renewable energy

Yuken India Ltd. demonstrates robust sales growth and benefits from strong sector tailwinds, but its high P/E ratio and elevated PEG ratio suggest the stock is priced at a premium. Investors should weigh the company’s growth potential against its valuation risks and monitor upcoming financial results for signs of sustained earnings improvement.

*Sources: Yuken India annual reports, BSE/NSE disclosures (listed entity filings), Business Standard/Capital Market financial news, MarketScreener press release, Moneycontrol/Trendlyne summaries, Yuken AR (FY24), Tickertape market data, LinkedIn announcement.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.