The global pharmaceutical and life sciences industry is at an inflection point, balancing persistent pricing pressures in legacy generics against immense opportunities in specialty therapeutics and new healthcare verticals. In India, while the cosmetic pharma market (IPM) is projected to see modest low-to-mid-single-digit growth, the government’s ‘Atmanirbhar Bharat’ (Make in India) initiative is creating a protected ecosystem for domestic manufacturers.

Simultaneously, the global medical devices (MedTech) market is expanding rapidly, projected to reach US$ 670 billion by 2029, with the Indian MedTech market alone expected to hit US$ 50 billion by 2030. This growth is driven by technological advancements, particularly in areas like robotic-assisted surgery, which is becoming a “competitive necessity”. This dual landscape forces companies to navigate short-term generic market volatility while making significant, long-term capital investments in innovation and diversification to ensure future growth.

Business Snapshot & Evolution

Zydus Lifesciences Limited is in the midst of a significant strategic transformation, evolving from a company primarily known as a volume-driven generics player into a value-centric, global life sciences organization. This pivot is focused on differentiated products, innovation, and strategic expansion into specialty healthcare areas.

The company’s business model is built on a global footprint across key segments:

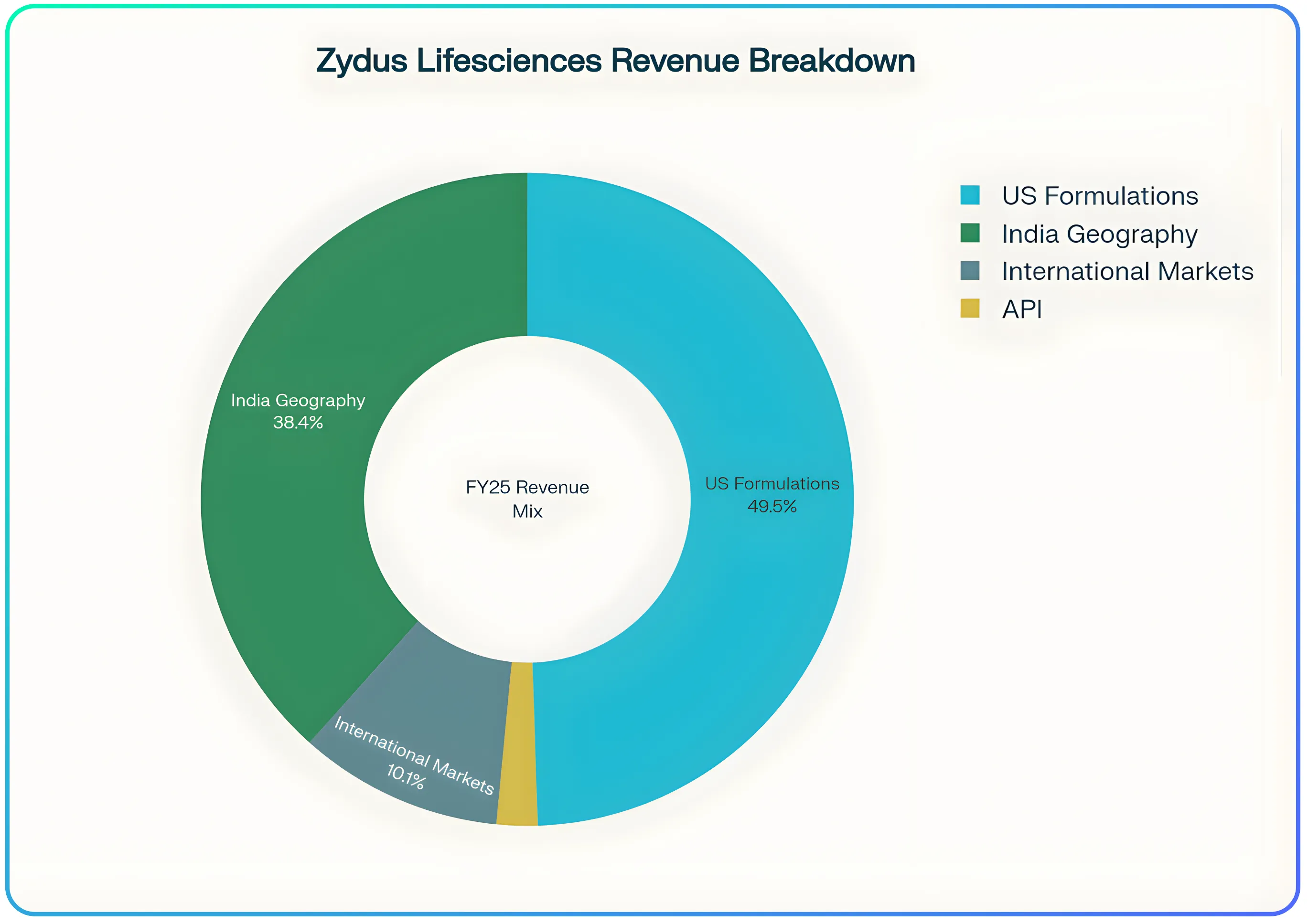

US Formulations: The largest segment, contributing 49% of FY25 revenue, focusing on generics, complex generics, and specialty 505(b)(2) products, which is a US Food & Drug Administration (FDA) regulatory pathway that allows companies to launch improved versions of existing drugs (for example, new dosage forms, or combinations) without going through the full-length approval processes, which gives faster market entry and higher profitability.

India Geography (38% of FY25 Sales): This includes both India Formulations (26%), which emphasizes branded generics and a growing chronic portfolio, and Consumer Wellness (12%).

International Markets (IM): A growing “third pillar” accounting for 10% of FY25 sales, focused on emerging markets and Europe.

API (Active Pharmaceutical Ingredients): A smaller segment (2% of FY25 sales) providing backward integration and external supplies.

The core of its evolution is the establishment of two new strategic pillars through inorganic expansion:

MedTech: A foray into the medical devices space, anchored by the acquisition of a majority stake in Amplitude Surgical SA (France), a European leader in lower-limb orthopaedic technologies.

Entry into the global biologics contract development and manufacturing business through the acquisition of US based manufacturing facilities from Agenus Inc. (CDMO, or Contract Development and Manufacturing Organization, means the company develops and manufactures biotech drugs on behalf of other firms in a growing global industry.)

Financial Performance Overview

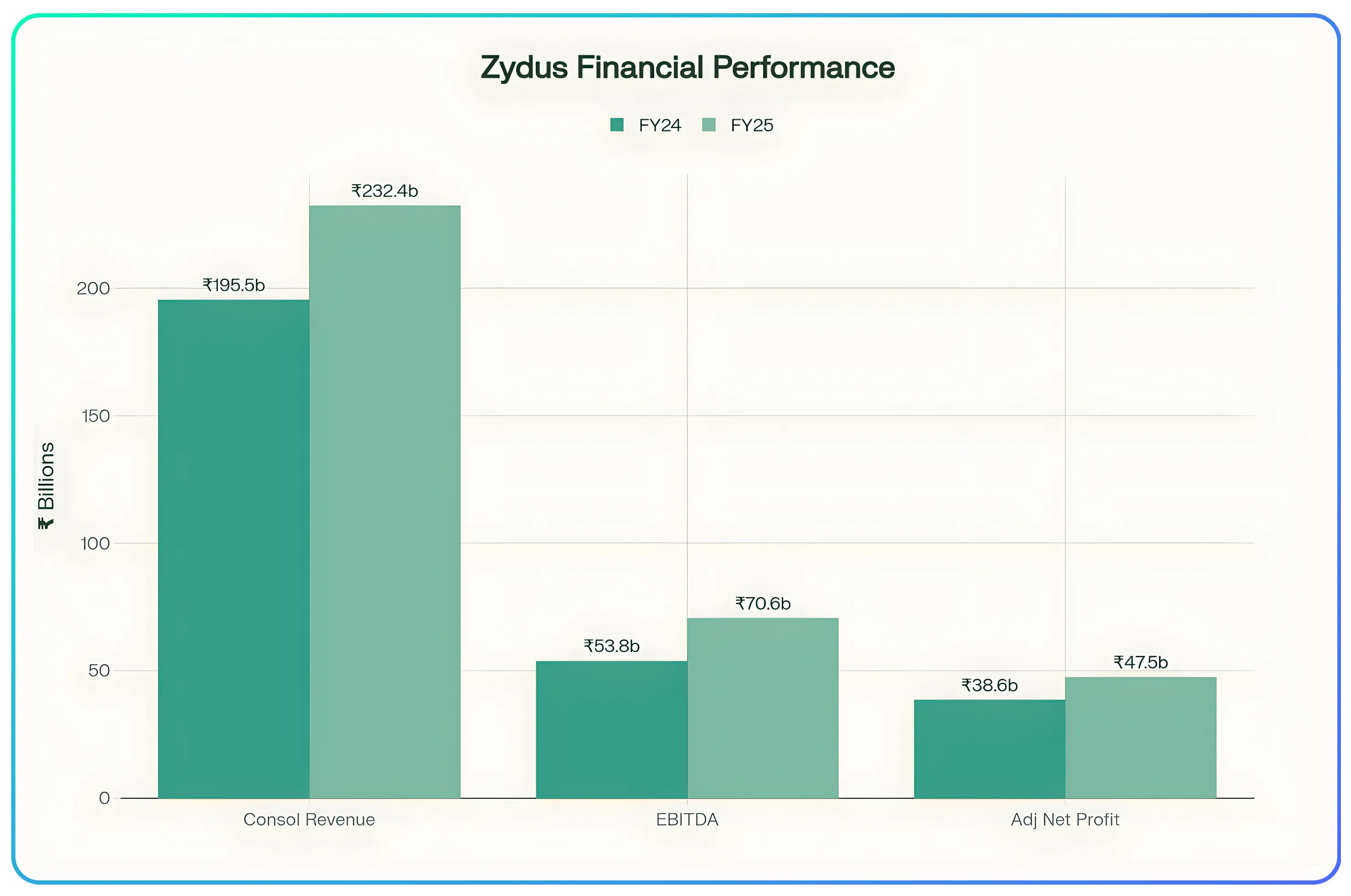

Zydus concluded Fiscal Year 2025 (FY25) on a robust note, achieving its highest-ever operating profit and margins. Consolidated revenues grew 13.9% year-on-year (YoY) to ₹232.4 billion. This top-line growth was amplified by operating leverage and a favorable product mix. Leading to a 31.1% surge in EBITDA to ₹70.6 billion and a 290 basis point (bps) expansion in EBITDA margin to 30.4%. Adjusted net profit for FY25 rose 22% to ₹47.5 billion.

This strong performance continued into the first half of FY26, which saw revenue grow 10.9% YoY and EBITDA margin expand further to 32.3%, driven by a particularly strong Q2 margin of 32.9% (a 500 bps YoY expansion).

A pivotal change in the financial position occurred in Q2 FY26. After building a peak Net Cash surplus of ₹56.3 billion at the end of Q1 FY26, the company deployed significant capital for its strategic acquisitions (notably Amplitude Surgical). This resulted in a shift to a Net Debt position of ₹22.8 billion by the end of Q2 FY26 (September 30, 2025), marking a new capital allocation for the company.

Business Segments Breakdown

US Formulations

This segment, the company’s largest, is characterized by a mix of high-value opportunities and a resilient base business.

Growth Drivers: Performance is driven by a healthy base portfolio and new launches, which are offsetting erosion from mature products. Zydus has benefited from its status as a “resilient supply chain player,” helping it win new contracts. A key new driver is the specialty 505(b)(2) portfolio, particularly the Sitagliptin franchise, which is performing “multi-fold better” than estimated and has secured a five-year national government contract.

Headwinds & Volatility: The segment is managing significant volatility from key products Sales of Lenalidomide (Revlimid), a major contributor, are “lumpy”, and FY25 is expected to be its “peak sales year” as it now faces significant price erosion and competition. The company has also lost market share on Asacol HD.

India Formulations

The domestic branded generics business is a model of consistency, consistently outpacing the Indian Pharma Market (IPM) growth. This outperformance is strategically driven by its focus on the chronic portfolio (drugs used for long-term conditions like diabetes and heart disease), which has grown to 44.5% of the business (a 500 bps increase over three years). The company maintains leadership in super-specialty areas like Oncology and Nephrology.

International Markets (IM)

This segment, covering Emerging Markets and Europe, has emerged as a “reliable third pillar of growth”. It has demonstrated remarkable acceleration, with Q1 FY26 revenues growing 36.8% YoY and Q2 FY26 growing 39.4% YoY. Management is confident this segment can sustain “high teens to mid-twenties growth” going forward.

Consumer Wellness

This business generally delivers strong, volume-driven growth, supported by strategic channel expansion into e-commerce and modern trade (30.9% saliency in Q1 FY26). However, it is subject to seasonal anomalies. Q1FY26 growth slowed to 2.2% YoY, a direct impact of “early monsoon conditions” which affected sales of seasonal brands.

New Strategic Pillars (MedTech & CDMO)

Medtech (Amplitude Surgical): This new vertical is already contributing to the top line, accounting for 3% of revenue in Q2 FY26. The acquisition is expected to be “earnings accretive” for FY26–FY27, positioning Zydus as a leader in the European orthopaedics market.

Global Biologics CDMO (Agenus): This acquisition provides immediate access to US-based manufacturing. It is a long-term strategic play, with meaningful revenue scale-up anticipated in two-and-a-half to three years.

Strategic Moats and Differentiators

Zydus’s competitive advantage is evolving from a large-scale generics manufacturer to a multi-faceted life sciences company.

From Volume to Value-Centric: The core differentiator is the strategic pivot from “volume-centric generics” to “value-centric, differentiated products,” including complex generics and specialty 505(b)(2) assets.

US Markets Resilience: In the US, Zydus leverages its scale as the 5th largest generic player by prescriptions with its reputation as a “resilient supply chain player”. This reliability is increasingly a competitive advantage, leading to new contract opportunities.

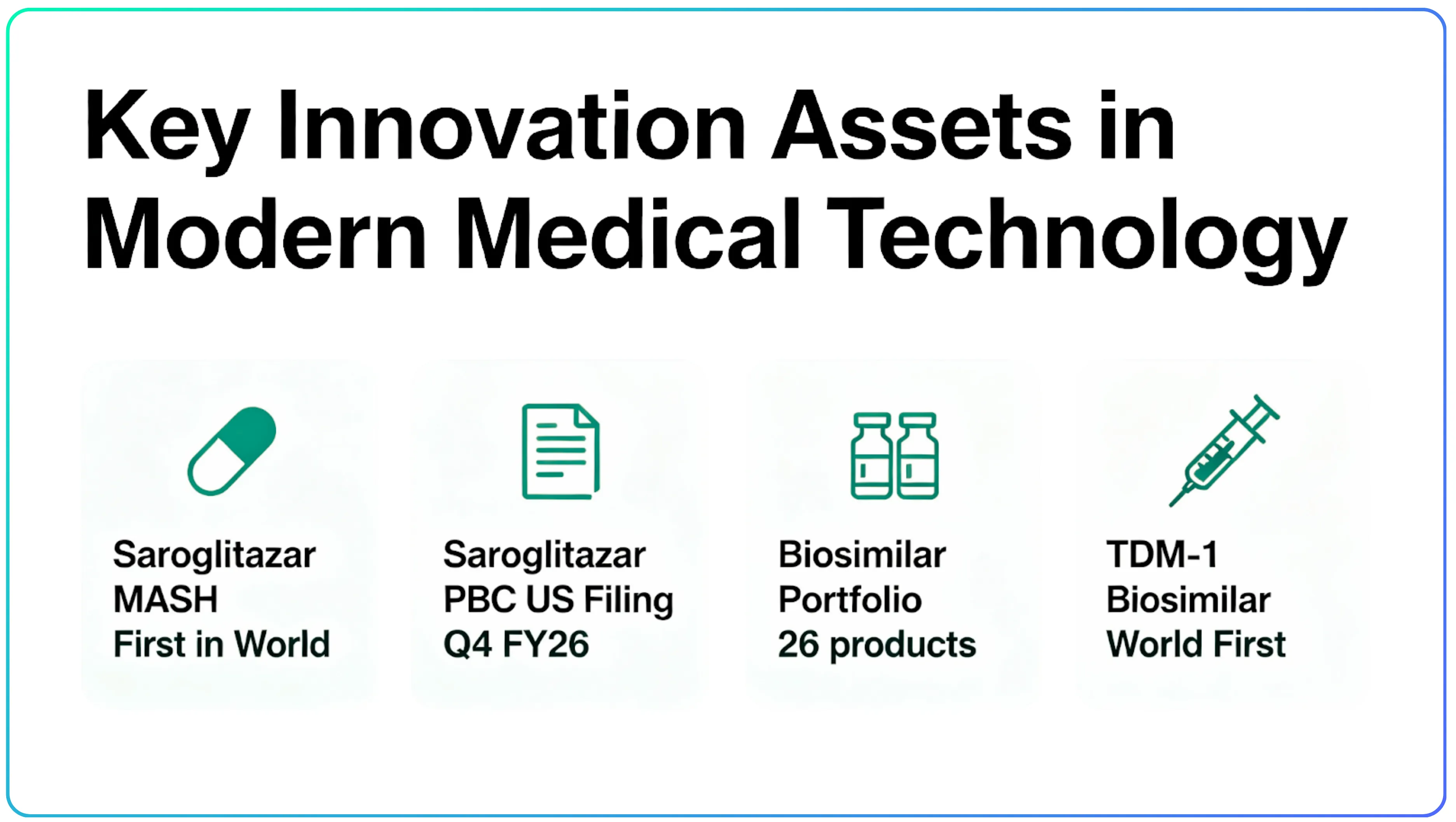

Innovation (NCEs and Biologics): Zydus is investing heavily in innovation to move beyond generic drugs. It has developed Saroglitazar Magnesium, a breakthrough medicine for MASH which is a serious liver condition similar to fatty liver disease that currently has no approved global treatment. This makes Zydus the first company in the world to bring such a therapy to market.

The drug has already shown positive results in US clinical trials for another liver disorder (Primary Biliary Cholangitis or PBC), and the company plans to file for US regulatory approval by the fourth quarter of FY26. If approved, this would mark Zydus’ entry into the global market for specialty drugs developed from its own research. Alongside new drug discovery, Zydus has built one of the largest biosimilar portfolios in India, which is 26 products that replicate high-cost biologic drugs used for cancer and autoimmune diseases. It even launched the world’s first biosimilar version of an advanced cancer drug called TDM-1, used in target antibody therapy.

New Pillar Advantages: The MedTech acquisition provides a “leading position in the attractive orthopaedics market” in Europe, complete with a robotic surgery platform. The CDMO acquisition secures advanced manufacturing capabilities in the key US biotech hub.

Growth Drivers & Expansion Plans

Zydus is in a phase of high strategic investment to secure its next leg of growth.

Financial Guidance (FY26)

Management has provided a cautious but firm outlook for FY26, projecting double-digit consolidated revenue growth. However, it expects EBITDA margins to compress from the 20.4% high of FY25, guiding for margins to “exceed 26% comfortably”. This guided compression is attributed to three main factors:

- Pricing challenges for Revlimid.

- The loss of Asacol

- A significant, planned increase in R&D expenses, which are projected to be 8% of total revenues for FY26 (up from 6.7% in FY24).

Strategic Investments & Capex

The company is funding its expansion through significant capital expenditure. Total organic capex for FY26 is estimated at ₹1,200 crores. A significant portion of this, approximately ₹300 crores, is earmarked for expanding the new MedTech pillar, including a new dialyzer facility and interventional cardiology products.

Key Pipeline & Long-Term Initiatives

Saroglitazar (PBC): Following positive pivotal trial results, the company is preparing its US NDA filing for Q4 FY26, targeting a potential US launch in FY27.

Other NCEs: The company is advancing Usnoflast (for ALS) into Phase II(b) trials in the US and is awaiting approval for Desidustat in China within the next 12 months.

GLP-1 (Semaglutide): Zydus is on track for a “day-one launch in India” with a novel differentiated formulation.

Offsetting the US Cliff: To counter the decline of Revlimid, the company is planning 14 to 15 “important, critical launches in FY27,” many of which are complex or exclusive. This will be combined with a major scale-up of the 505(b)(2) specialty portfolio in FY27.

Long-Term Vision: The goal is to establish MedTech as a “sizable and profitable growth pillar” and achieve meaningful scale-up from the Biologics CDMO business within three years.

Risks & Industry Headwinds

Despite the clear strategic direction, Zydus faces material risks, primarily related to product transitions, market pressures, and the financial impact of its investments.

Product Concentration & Competition: The company faces a significant near-term headwind from its reliance on high-value US generics. Revlimid is experiencing price erosion and competition, and sales of Mirabegron are subject to ongoing patent litigation with a key trial scheduled for February 2026.

Margin & Financial Risks: The strategic decision to increase R&D spend to 8% of revenue directly pressures near-term margins, as reflected in the FY26 guidance. Furthermore, the company’s finance costs have risen sharply (up 303.6% YoY in Q2 FY26). Management clarifies this is not due to operational debt, but primarily an accounting requirement for the “unwinding of interest amount on the contingent payments” related to acquisitions like LiqMeds.

Macroeconomic & Regulatory Factors: The business is exposed to the “uncertainty of the US imposing tariff on pharmaceuticals,” which could impact the US business. On the consumer side, performance can be affected by external factors like the “early monsoon conditions” that dampened Q1 FY26 Consumer Wellness sales.

Valuation & Market View

Based on recent market data, Zydus Lifesciences trades at a Price-to-Earnings (P/E) multiple of approximately 18.77xand an Enterprise Value-to-EBITDA (EV/EBITDA) multiple of 12.59x. These metrics represent a significant discount to the broad pharmaceutical industry median (P/E of 31.79x and EV/EBITDA of 17.09x) and also place it competitively against its large-cap peers.

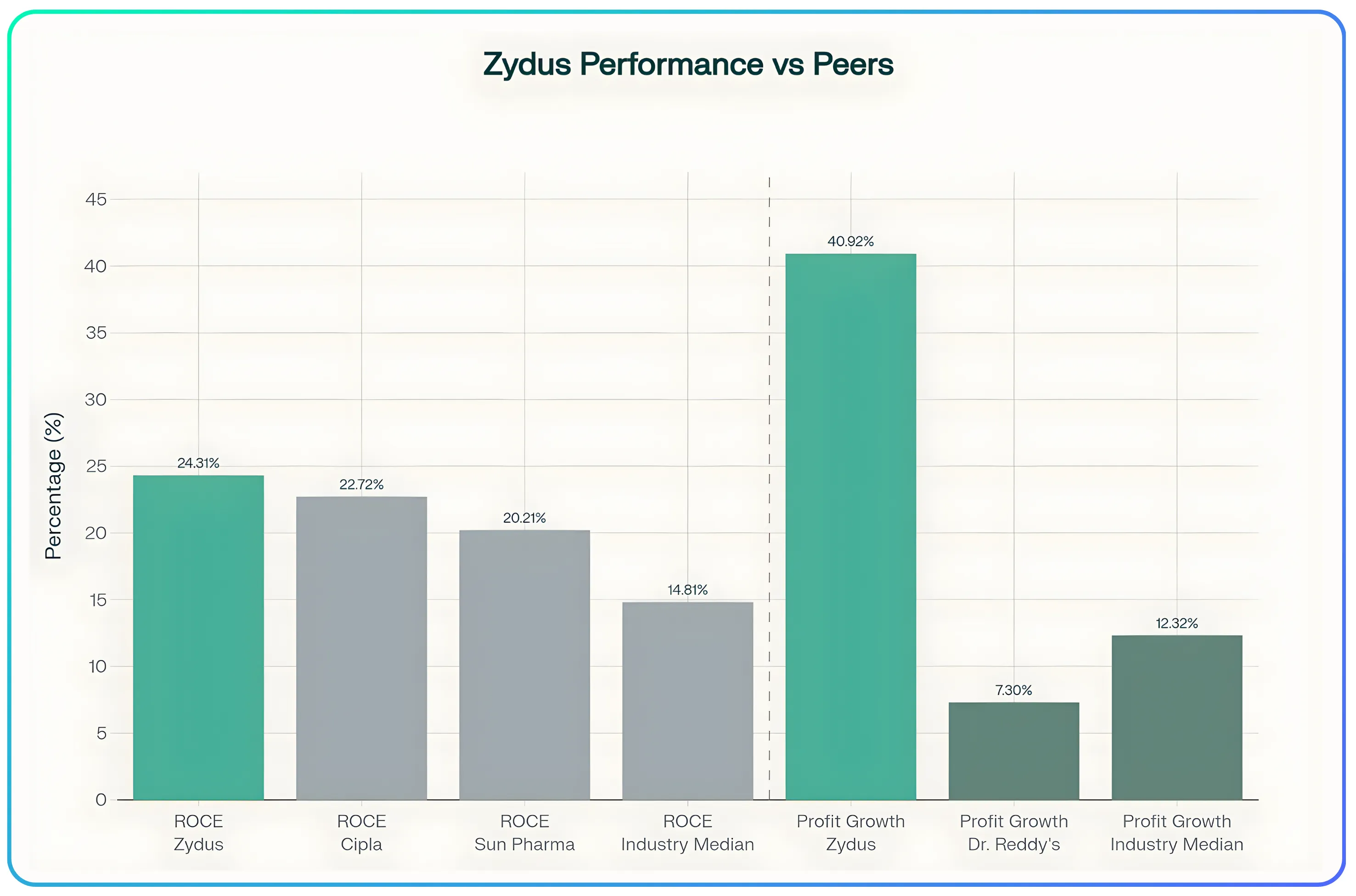

This valuation discount is noteworthy given the company's superior recent performance. Zydus reported a robust quarterly profit growth of 40.92% and quarterly sales growth of 16.92%, both significantly outpacing the industry medians of 12.32% and 10.56%, respectively.

Furthermore, its Return on Capital Employed (ROCE) of 24.31% is among the strongest in its peer group, substantially higher than the 14.81% industry median and ahead of peers like Cipla (22.72%) and Sun Pharma (20.21%). When compared to its closest valuation peer, Dr. Reddy's (P/E 17.98x), Zydus demonstrates a far stronger recent growth profile (40.9% profit growth vs. 7.3% for Dr. Reddy's).

The market appears to be balancing this superior growth and high-return profile against the known risks of its strategic transition. The valuation discount likely reflects investor caution regarding three key factors:

Near-term Margin Compression: Management’s own cautious FY26 EBITDA margin guidance (around 26%) is well below its recent H1 performance (32.3%). This guidance factors in the erosion of high-margin products like Revlimid and the high 8% R&D spend.

Execution and Integration Risk: The company is in a complex phase of simultaneously integrating major acquisitions (Amplitude Surgical, Agenus) while managing the decline of legacy products.

Increased Leverage: The acquisitions were funded by deploying its large net cash surplus, shifting the balance sheet to a net debt position. This is reflected in a Debt-to-Equity ratio of 0.38, which, while moderate, is above the industry median of 0.22.

The current valuation suggests a "wait-and-see" approach from the market. Investors appear to be pricing in the near-term headwinds and execution risks while not yet fully rewarding the long-term, high-growth potential of its new MedTech and Biologics CDMO pillars or the successful clinical progress in its NCE pipeline.

Bottom LIne

Zydus Lifesciences is a compelling transformation story. It is a mature, highly profitable, and operationally excellent genetics company that is strategically using its financial strength to execute a high-conviction pivot. The company is in a deliberate investment phase, sacrificing near-term margin certainty by simultaneously absorbing the erosion of legacy blockbusters and funding heavy investment in its future.

The core challenge and investment thesis rest on the timing of this transition. Zydus must successfully navigate the next 18-24 months, managing the decline of its high-value generics while its new, long-gestation investments like the Sarogilitazar US launch, the 505(b)(2) portfolio, and the MedTech business, scale up to become the company’s new , sustainable growth engines. Success in this execution will justify its transformation from a generic player to a diversified, value-centric global life sciences leader.

Check out more fundamental metrics about Zydus Wellness on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.