When two experienced investors study the same stock and arrive at opposite conclusions, the disagreement rarely comes down to the data. Both are reading the same annual report, examining the same financials, and watching the same market price movements. What separates their conclusions is the val uation framework each has chosen to apply.

For most retail investors in India, valuation often narrows to a single ratio: the price-to-earnings multiple. Applied without context, that one lens is like judging a building’s structural integrity by its facade. In reality, valuation is a multi-method discipline, with each method answering a different question about what a company is truly worth. Understanding which framework to use, and when, is what separates a reasoned investment decision from a number taken at face value. Valuation is the core of fundamental analysis in India, giving retail investors a disciplined way to assess what they are paying for versus what they are getting. What follows are seven stock valuation methods explained in plain terms, along with the conditions under which each one is most reliable.

Intrinsic Value

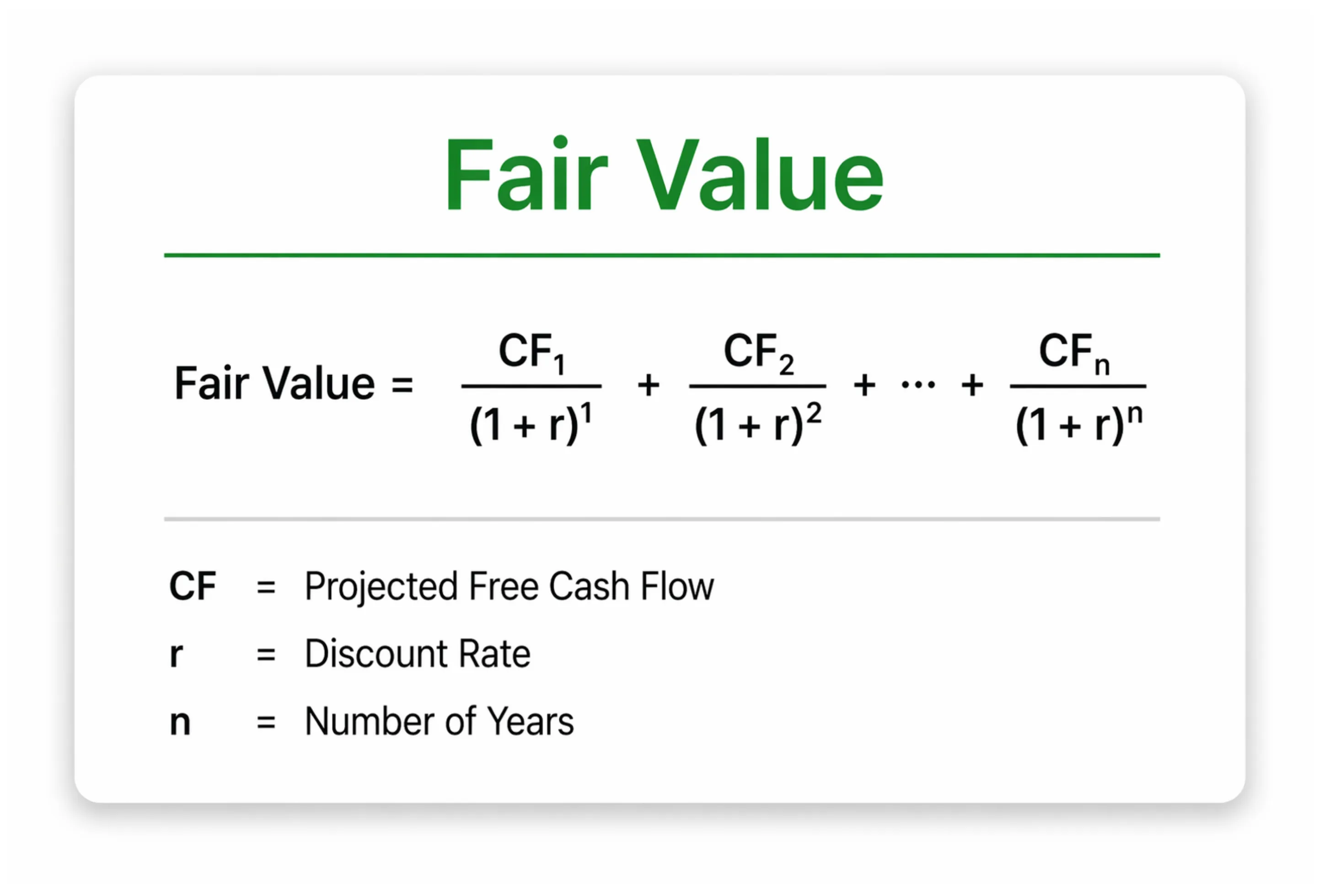

Of all approaches to valuing a stock, intrinsic value comes closest to answering the fundamental question: what is this business actually worth, independent of what the market currently thinks?

Formally known as Discounted Cash Flow analysis, or DCF, this method estimates the cash a business will generate over its lifetime and discounts those future flows back to their present-day equivalent. A rupee expected a decade from now is worth less than a rupee today, and the discount rate applied captures that difference, accounting for risk, opportunity cost, and time. Applying discounted cash flow analysis in India requires particular attention to discount rates, since risk premiums vary considerably across sectors and business cycles.

For businesses with stable, predictable earnings, such as consumer staples companies, established IT services firms, and regulated utilities, DCF produces estimates worth anchoring to. For cyclical businesses or companies in the early stages of growth, the assumptions required are too uncertain to yield anything reliable. A one-percentage-point shift in the discount rate, or an overstated growth projection, can move the final output by a third. Entirely dependent on the quality of its inputs, the method produces estimates only as reliable as the assumptions behind them.

Book Value and the Price to Book Ratio

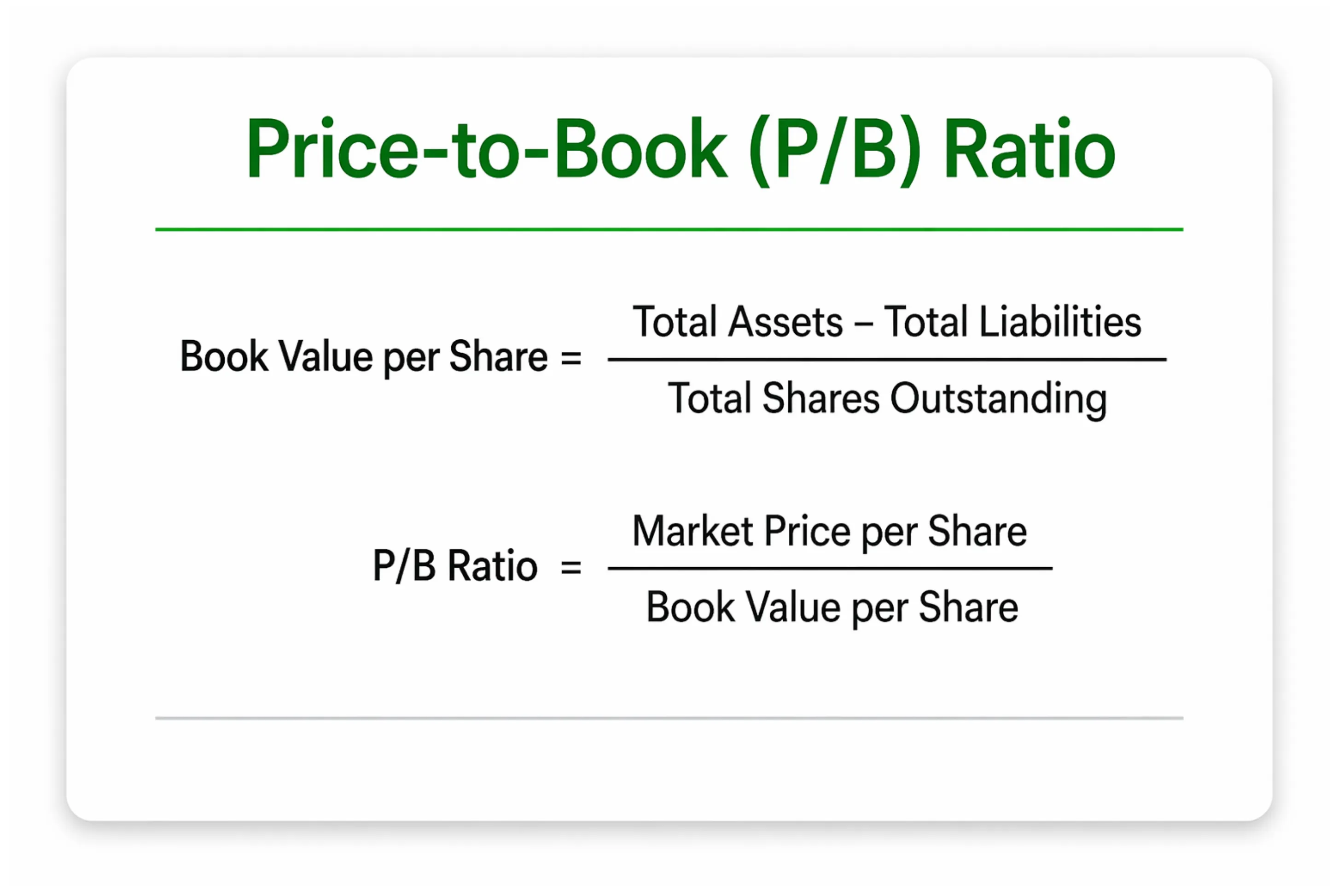

On the balance sheet of every listed company sits a figure derived by subtracting total liabilities from total assets and dividing the remainder by shares outstanding. This is book value per share, representing the accounting worth of the business on a per-share basis.

When the Price-to-Book ratio falls below one, the market is pricing the company below its stated net assets, a starting point historically associated with value investing.

In banking and financial services, book value finds its most natural home. The assets of a bank consist largely of financial instruments, loans, bonds, and government securities, and their accounting value carries genuine meaning. In technology or pharmaceutical businesses, competitive advantage lies in patents, software, and human capital, assets that accounting conventions largely exclude from the balance sheet. Applied to these companies, P/B produces a ratio, but not one that illuminates anything useful about the business.

Earnings-Based Valuation and the Price to Earnings Ratio

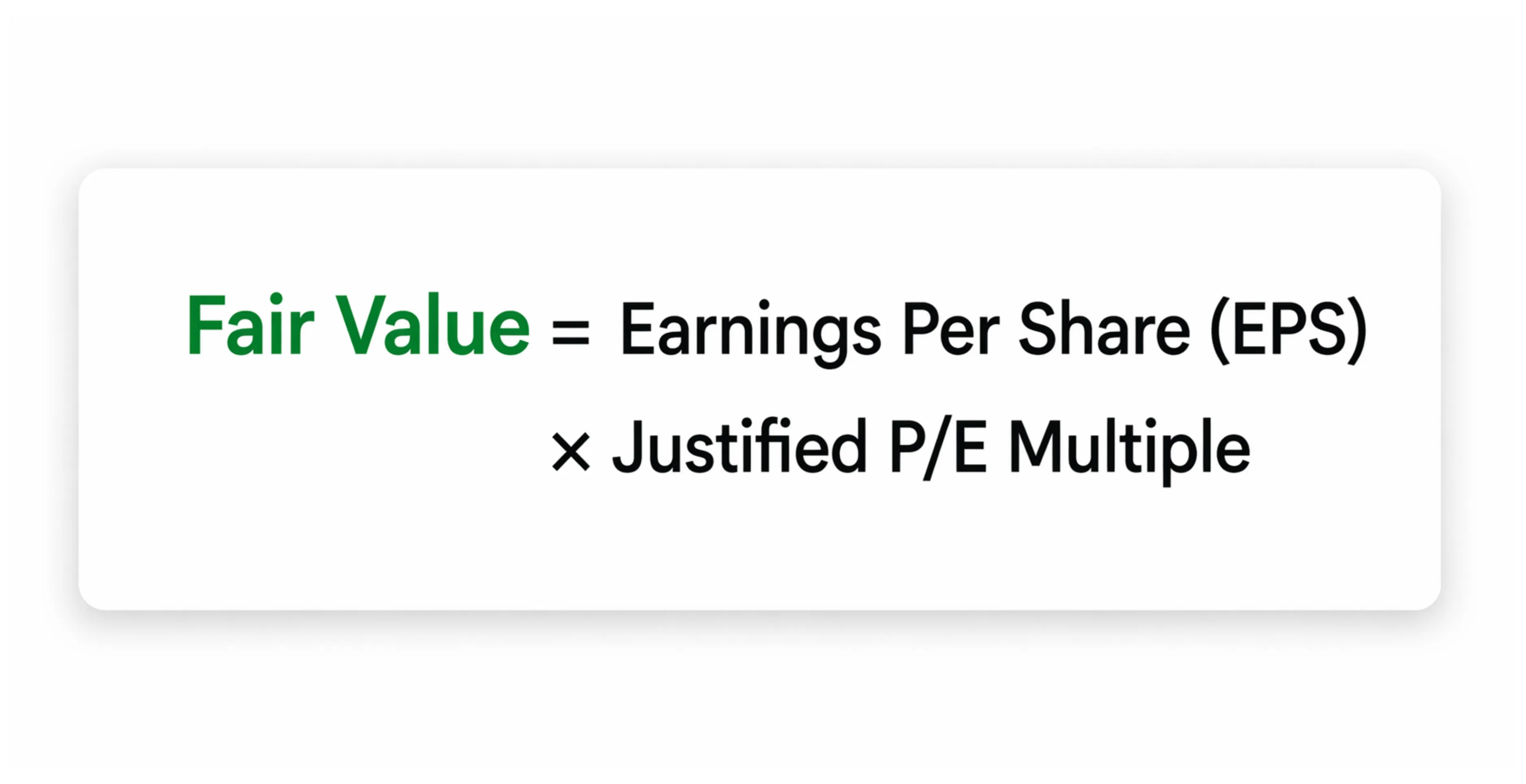

Stock valuation using the P/E ratio starts with a simple equation: divide the market price per share by the earnings per share. Built around a simple equation, the stock earnings-based framework derives a stock's fair value from what the company earns per share and what the market is willing to pay for those earnings.

Working with forward EPS, an estimate of earnings over the next twelve months, analysts calibrate the P/E multiple against the company's historical trading range and its sector peers to arrive at a target price.

Reported earnings, however, are an accounting construct, and accounting permits choices. Revenue recognition policies, depreciation methods, and the treatment of one-time items all shape the final EPS figure. EPS growth can be sustained even as operating cash generation quietly deteriorates. For this reason, earnings-based valuation produces its most reliable output when read alongside cash flow data rather than independently of it.

Also Read: The Crude-Nifty Inverse Relationship, Why Data Disagrees

EV/EBITDA

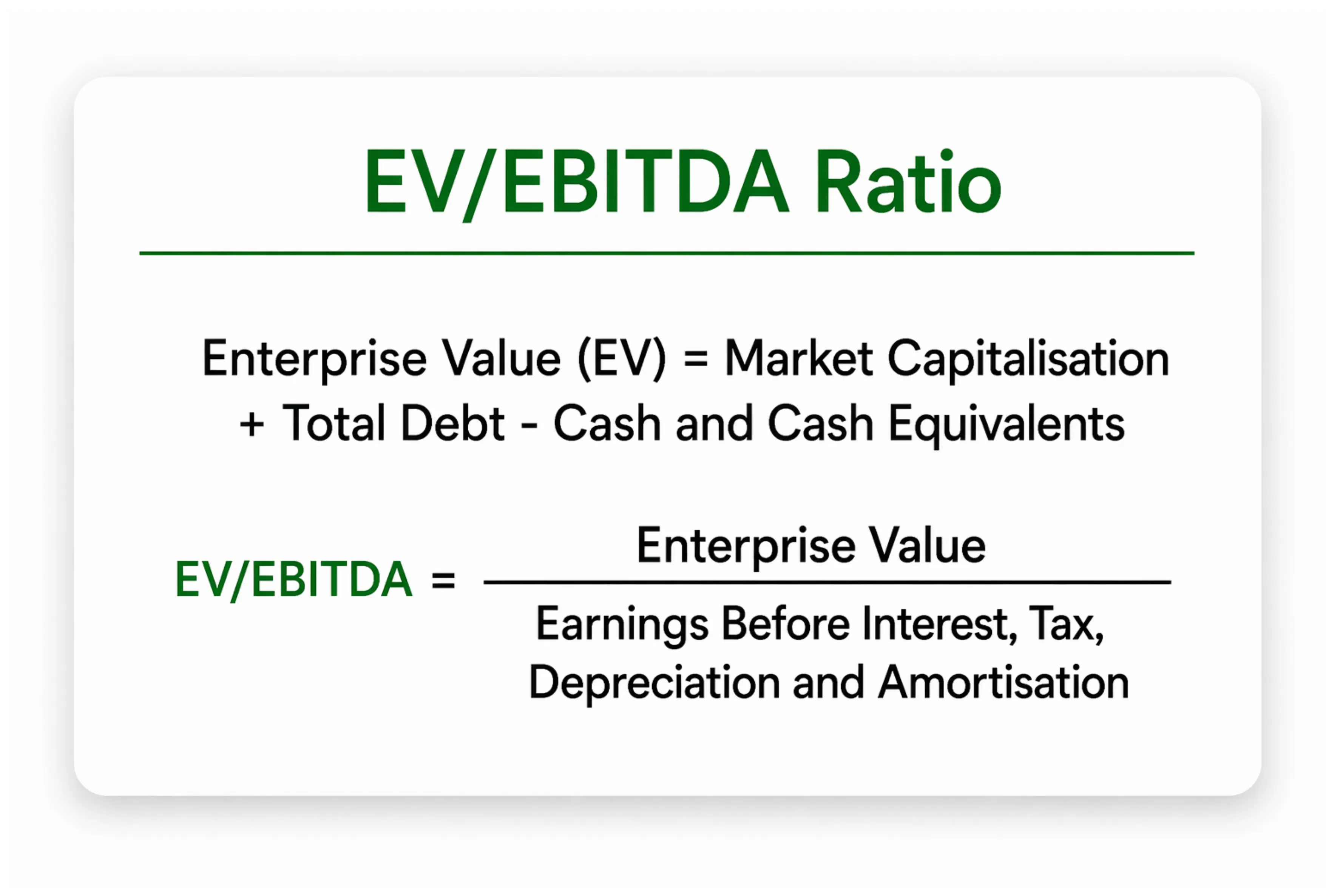

Comparing companies purely on price-to-earnings becomes unreliable when their capital structures differ significantly. A business carrying substantial debt pays higher interest costs, which compresses net profit and makes the P/E appear elevated relative to a debt-free peer conducting identical operations. To make the comparison honest, analysts shift to a metric that sits above the effects of financing decisions.

By comparing EV against EBITDA, the ratio captures operational performance without the distortions introduced by how a company has chosen to finance itself. In capital-intensive sectors where debt levels and depreciation schedules vary considerably between companies, including cement, steel, telecom, and infrastructure, EV/EBITDA provides a cleaner basis for comparison than P/E. For banks and financial companies, where borrowing is the business rather than a financing choice, the ratio loses its relevance entirely. In stock valuation, EV/EBITDA solves a problem that the price-to-earnings ratio cannot: it allows honest comparisons between companies whose debt levels differ significantly.

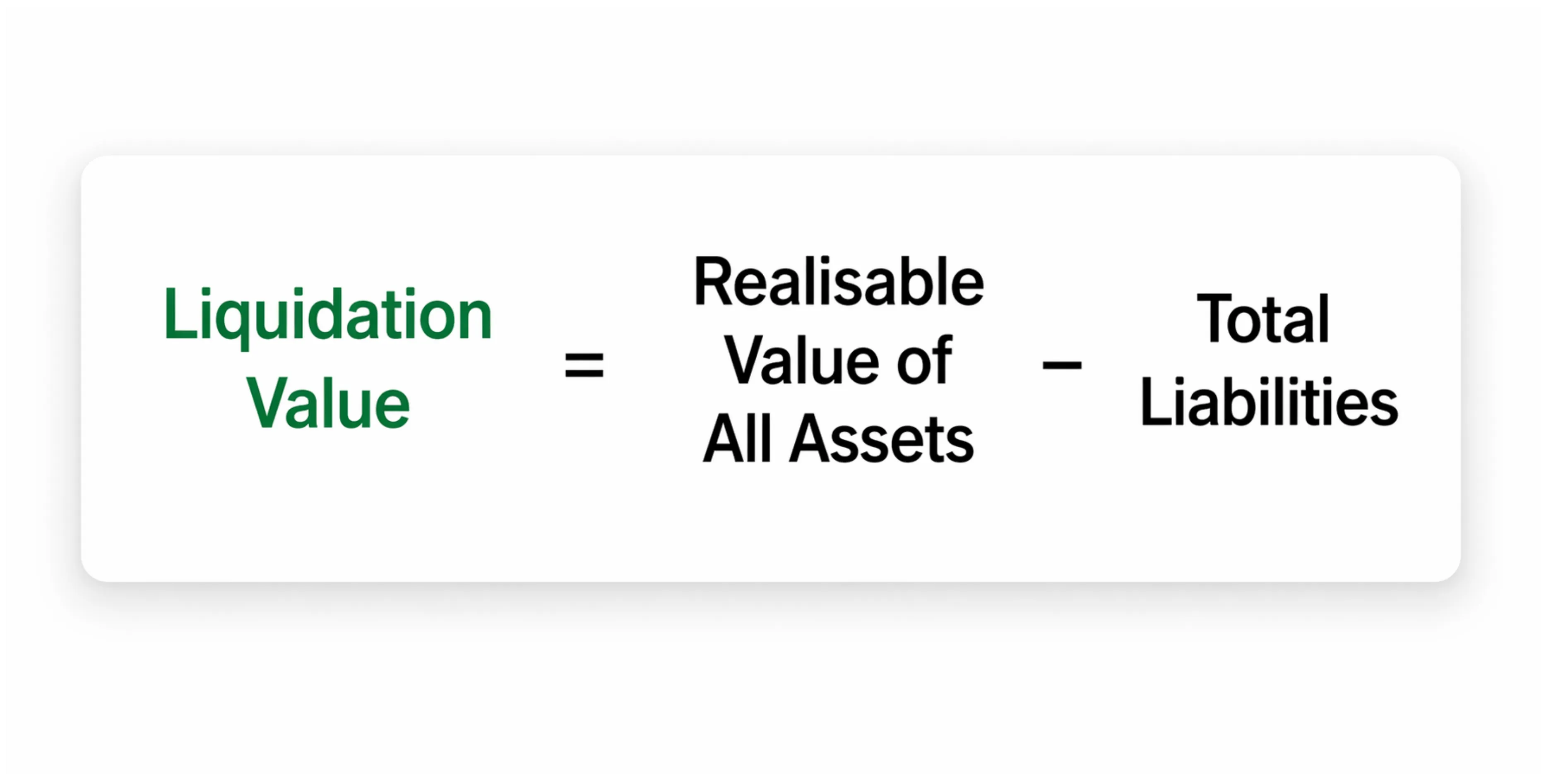

Liquidation Value

The liquidation value of a stock represents the floor of protection shareholders retain if the company stopped operating and sold all its assets today. Among valuation methods, liquidation value takes the most conservative position. Rather than projecting future earnings or assessing operational performance, it asks what shareholders would receive if the company stopped operating today, sold its assets under distressed conditions, and settled every liability in full.

Because a forced sale rarely fetches accounting value, liquidation value typically falls below book value. Fixed assets sell at discounts in distressed conditions. Inventory may be partially obsolete. Certain receivables will not be recovered in full. Excluded entirely is the going-concern premium, the value that exists only because the business continues to operate.

For investors screening stock liquidation value in India, the method is particularly useful in identifying value traps, where a low earnings multiple conceals a weak underlying asset base. In distressed investing, this method tells the analyst what floor of protection shareholders retain in a worst-case scenario. In general screening, it helps surface value traps: stocks appearing inexpensive on earnings multiples whose underlying assets, stripped of operational value, would leave shareholders with very little. As a target price, liquidation value is too conservative to be useful. As a measure of downside, it is indispensable.

Replacement Value

Instead of asking what a company's assets would fetch in a sale, the replacement value of a stock approaches the question from the opposite direction: what would it cost, at today's prices, to build those assets from the ground up? When the market values a company below that cost, acquiring the existing business is cheaper than replicating it.

In industries where physical infrastructure defines competitive position, this carries real practical weight. Establishing a large cement plant today demands several thousand crores in capital expenditure, years of construction, environmental and regulatory clearances, and the development of raw material linkages and logistics networks. Replacement value is especially relevant for stock valuation in the cement sector in India, where land acquisition, kiln installation, and regulatory clearances make replication expensive and time-consuming. A listed cement company available at a market capitalisation below that replacement cost is, in a substantive sense, priced below the cost of competition. Limiting the method's application is the fact that replacement costs must be estimated rather than observed, and those estimates are open to debate.

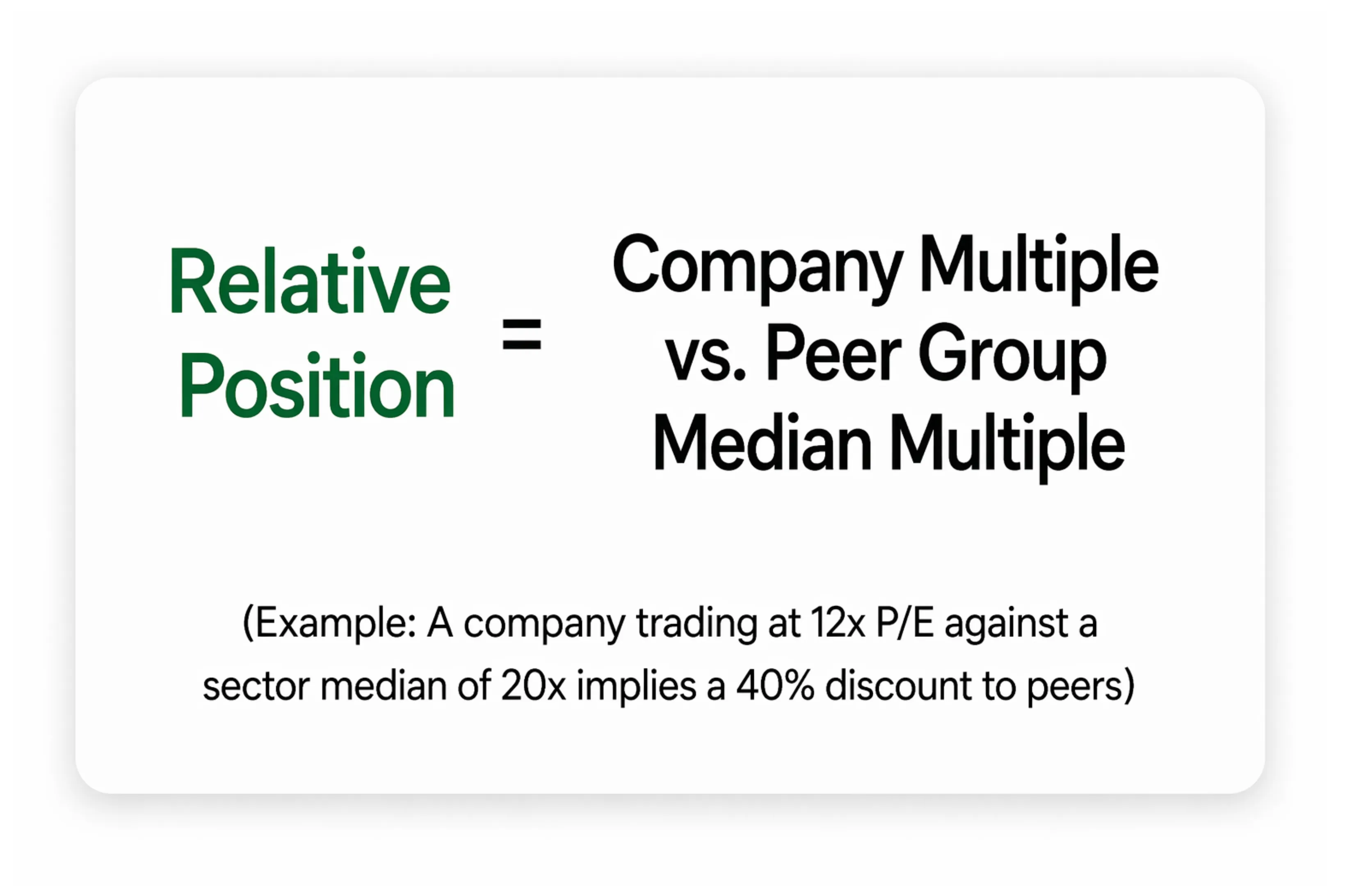

Relative Valuation

Of all valuation frameworks, relative valuation is the most accessible and the most widely applied in practice. By comparing a company's trading multiples, whether P/E, P/B, EV/EBITDA, or Price-to-Sales, against those of its closest listed peers, analysts identify whether the company is priced at a premium or discount relative to the group.

When a fundamentally comparable business trades at a meaningful discount to its peers, that gap demands explanation. Sometimes it reflects a genuine pricing inefficiency the market has been slow to correct. More often, it reflects a risk embedded in the business that the multiples alone do not surface: governance concerns, customer concentration, regulatory exposure, or a balance sheet carrying more stress than the headline ratio reveals.

Structurally, the method cannot detect overvaluation at the sector level. When an entire industry trades at elevated multiples, a company at the lower end of that range appears cheap by comparison while remaining expensive in absolute terms. Relative valuation benchmarks a company within its peer group. It says nothing about whether the peer group itself is reasonably priced.

Using These Methods Together

Rarely does a single valuation method tell the complete story. Capturing one dimension of value apiece, each framework also carries blind spots that the others can partially compensate for. Among professional analysts, the practice is triangulation: running two or three methods in parallel and examining where their outputs converge and where they diverge.

Convergence strengthens the case. Attractively priced on earnings, cheap relative to book value, and available below the replacement cost of its assets, a stock presenting all three signals rests on a more durable argument than one flagged by a single metric alone. When the methods diverge, that divergence is equally instructive. A low P/E sitting alongside weak operating cash flows and an elevated EV/EBITDA relative to peers suggests the headline number may not be capturing the full picture.

| Method | What It Measures | Best Suited For | Key Limitation |

|---|---|---|---|

| Intrinsic Value (DCF) | Present value of future cash flows | Stable, cash-generating businesses | Highly sensitive to input assumptions |

| Book Value (P/B) | Net asset value per share | Banks, NBFCs, asset-heavy businesses | Ignores intangibles and growth potential |

| Earnings-Based (P/E) | Earnings multiple | Mature, profitable companies | EPS is vulnerable to accounting choices |

| EV/EBITDA | Operational value vs earnings | Capital-intensive sectors | Not applicable to financial sector firms |

| Liquidation Value | Worst-case asset recovery | Distressed stock analysis | Excludes going-concern value entirely |

| Replacement Value | Cost to replicate asset base | Cement, steel, infrastructure | Replacement cost requires estimation |

| Relative Valuation | Multiple vs sector peers | Screening and benchmarking | Cannot detect sector-wide overvaluation |

What Benjamin Graham called the margin of safety, the gap between a stock’s estimated value and its market price, sits at the core of every valuation exercise. No method produces a precise answer. At best, valuation defines a range. The discipline lies in waiting for a price that offers a clear margin of safety before committing capital.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.