Ask any active Indian trader what happens to the stock market when crude oil prices spike. You'll get the same answer every time, delivered with total confidence:

"Crude goes up, Nifty goes down. Everyone knows that."

Except the data doesn't agree. And if you've been trading on this assumption without questioning it, it may have cost you more than a few bad calls.

Let's break it down.

Where the Belief Comes From

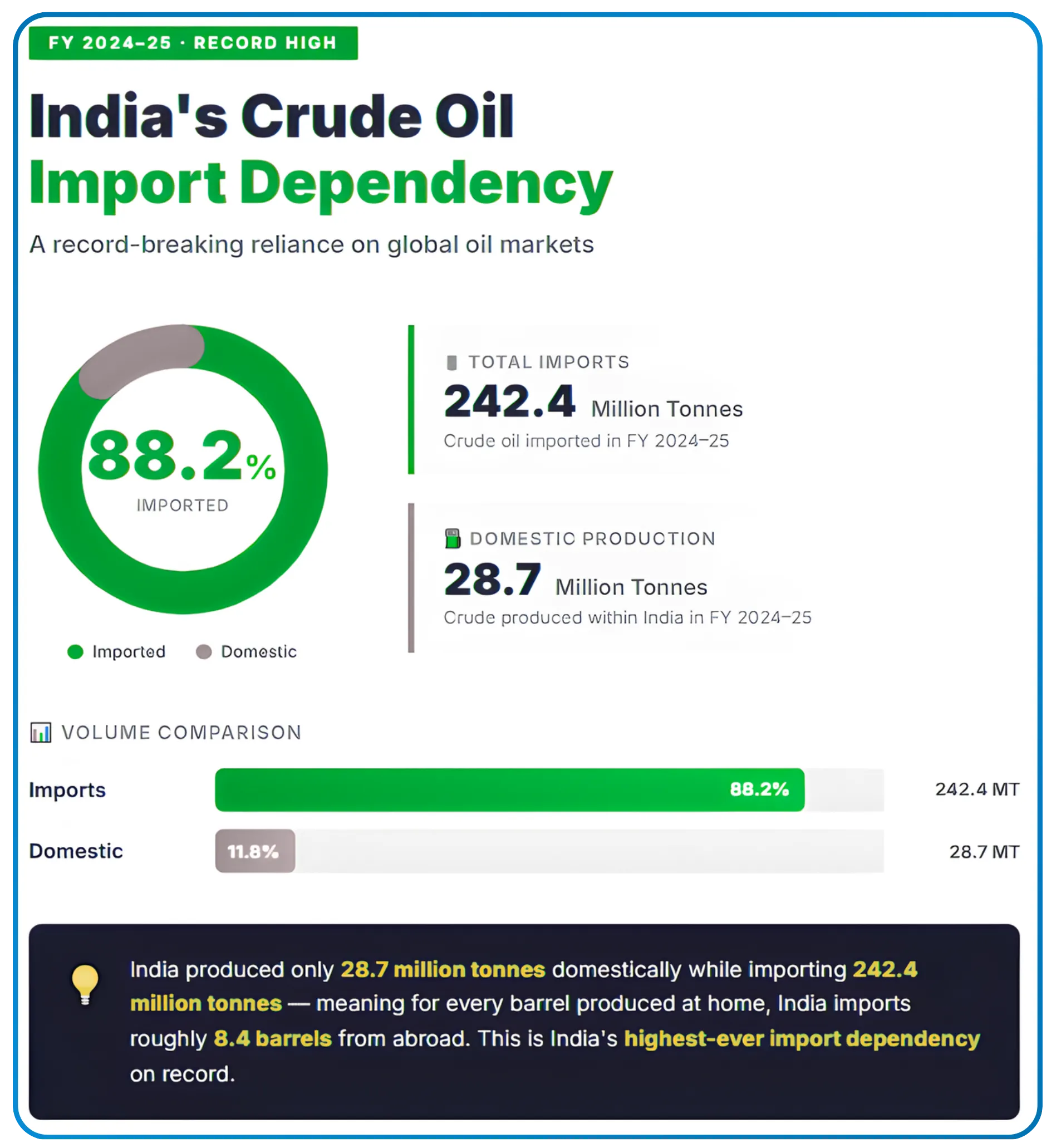

The logic, on the surface, is airtight. India imports 88.2% of its crude oil requirement; a record high in FY 2024–25, with imports exceeding 230 million tonnes against domestic production which remains below 30 million tonnes (Ministry of Petroleum & Natural Gas, PPAC). When crude prices rise, India's import bill swells, the current account deficit widens, the rupee weakens, and foreign investors pull money out. That chain reaction, in theory, hammers Nifty.

Higher crude prices naturally spark inflation concerns across India. This reliance on global oil means energy markets dictate much of the expected economic growth. Many worry that a rising dollar against the Indian rupee will trigger intense selling pressure on the index. The bulk of this pressure usually impacts companies highly dependent on oil and gas.

Every $10 increase in global oil prices can increase India's annual import bill by $12–$15 billion.

Every 10% rise in crude oil prices could reduce India's GDP growth by around 20 to 25 basis points.

It's a clean, logical story. The kind traders love because it gives them a rule they can act on immediately.

The problem is that markets rarely reward clean stories.

Technical analysis and price action often reveal a different reality for these markets. Relying solely on the price per barrel to sell equities introduces unnecessary risk.

What the Data Actually Shows

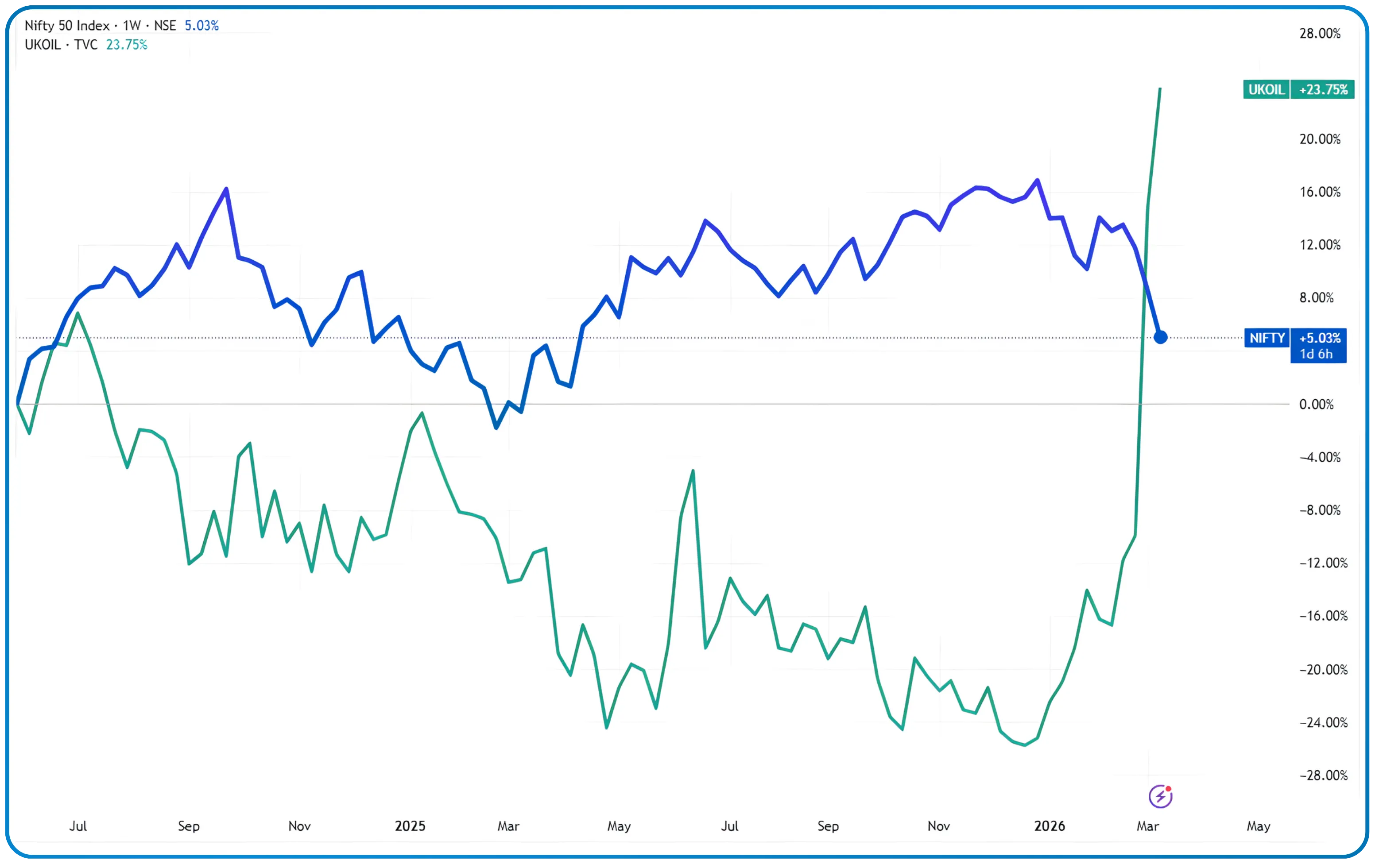

A 2025 peer-reviewed study on the crude oil–Nifty relationship found something that most traders would find deeply uncomfortable: crude oil and Nifty 50 share a moderate to strong positive correlation. Meaning they often move together, not in opposite directions.

This specific data challenges the traditional view of rising oil prices causing an automatic decline in the broader market. Rising crude prices can sometimes indicate strong global markets rather than impending doom.

Below $90–$100 per barrel, oil prices and the Nifty 50 often move together, reflecting healthy global economic growth

This isn't a short-term anomaly. Several stretches between 2016 and early 2020 saw crude and Nifty rising together as global growth improved. On shorter timeframes like daily or weekly moves, the correlation is often weak or inconsistent, meaning crude and Nifty can move together or diverge depending on broader global conditions. Only on a quarterly basis does a negative relationship begin to emerge, and even then, it is not consistent.

Technical indicators applied to spot prices and crude oil futures show high volatility but not a guaranteed inverse correlation. Amid uncertainty, factors like the total number of option contracts and open interest heavily influence short-term trading volume.

To put it plainly: the "crude up, Nifty down" rule holds sometimes, over long stretches, in specific conditions. But as a trading rule applied day-to-day or week-to-week, it fails more than it works.

Why Do They Move Together?

This is the part that changes how you think about it. When crude oil prices are rising globally, it is usually because global economic activity is strong. Factories are running, shipping lanes are busy, demand for energy is high. That same environment (one of global growth) tends to be positive for equity markets worldwide, including India.

Strong demand for energy naturally supports equity markets across various countries.

Foreign Institutional Investors (FIIs) are not just watching crude in isolation. They are watching global growth signals. When those signals are strong, FIIs tend to increase exposure to emerging markets like India, pushing Nifty higher, even as crude is rising simultaneously.

These foreign institutional investors allocate capital based on comprehensive market value, not just the barrel mark of brent crude

The 2016 to early 2020 period is a clear example. Both crude oil and Nifty moved broadly in the same direction across multiple stretches of that period, confounding traders who were positioned for an inverse relationship.

The rise in the market during this period broke through key resistance levels despite the cost per barrel going up.

The "crude up, Nifty down" relationship tends to hold most forcefully in one specific scenario: when crude rises sharply and suddenly due to a supply shock, a geopolitical event, a conflict, a major production cut. In that case, the inflation and currency pressure hits before any growth signal can offset it.

A sudden middle east conflict or escalating conflict can inject immediate fear into currency markets. Middle east war tensions historically cause a sharp spike in futures before the physical delivery expiry date.

The ongoing conflict involving the U.S., Israel, and Iran triggered fears of disruptions in global oil and gas supplies, leading to a sharp selloff in equities.

The International Energy Agency has warned that the ongoing conflict could lead to one of the largest disruptions in global oil supply in years

This is exactly what Indian traders witnessed in early 2026, when rising US–Iran tensions triggered a broad market decline. A large share of India’s crude imports passes through the Strait of Hormuz, making the country vulnerable to disruptions in the region. Nifty 50 fell approximately 4.6% and Nifty Smallcap 250 dropped 5.1% in response, a textbook supply-shock scenario.

The ongoing conflict and fear of a broader iran war severely impacted crude oil prices. Geopolitical tensions in the middle east are prime catalysts for this specific type of market shock. If oil prices had previously hit a record low, the sudden surge from the conflict amplifies the impact on the currency.

Crude isn't the only commodity with a complex market story. Also worth reading: How Silver Shaped Empires, Markets, and Modern Investing

The Sector Story Is Even More Nuanced

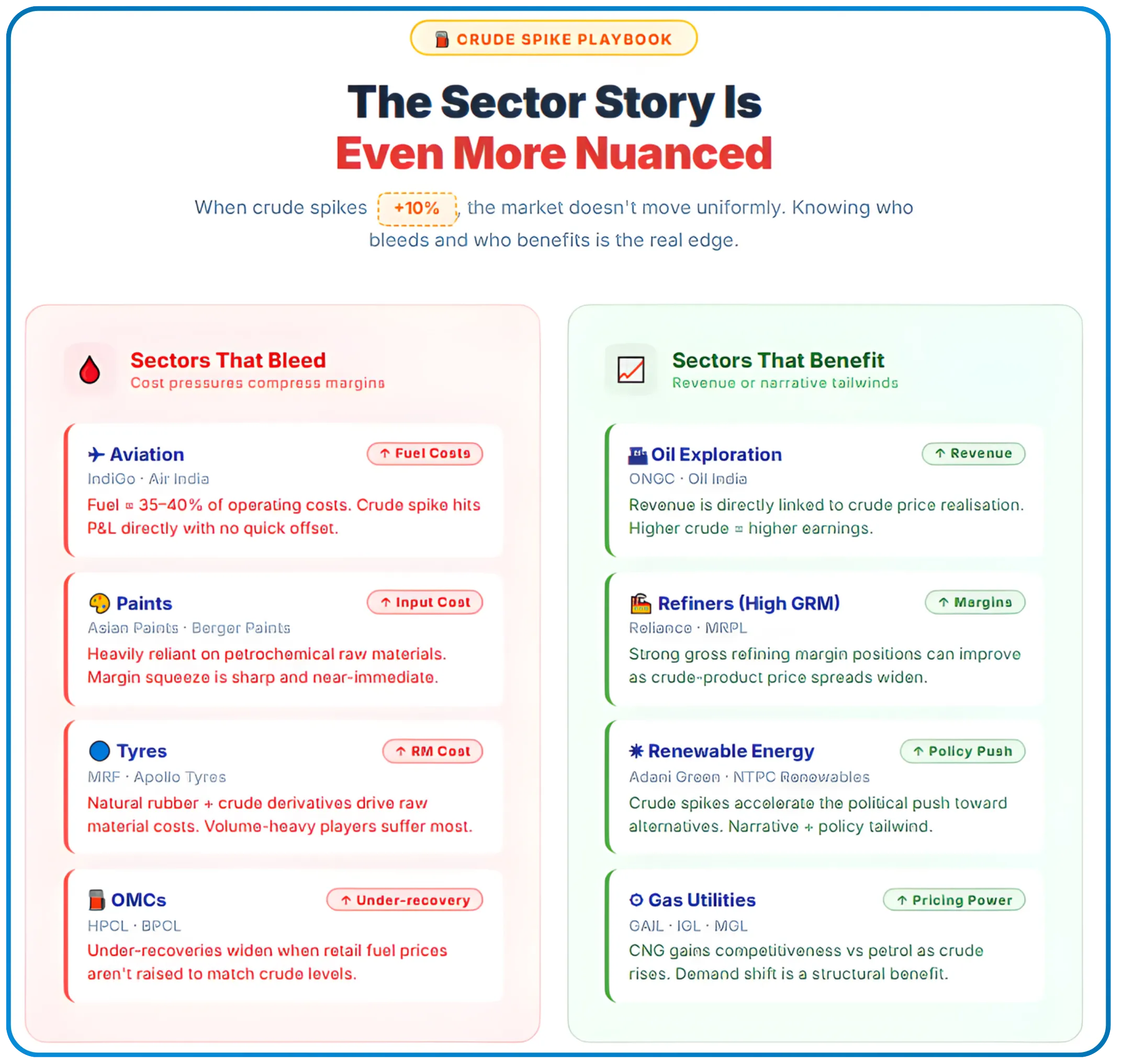

Here is where active traders need to pay the most attention, because even in a crude spike, the market does not move uniformly.

When crude oil prices surge, it leads to higher transportation and raw material costs, reducing profitability for sectors such as paints, tyres, aviation, and oil marketing companies.

The impact of crude oil heavily depends on the specific sector.

Upstream oil and gas producers may benefit from higher crude production prices, while refiners may improve gross refining margins during price volatility.

Sectors that typically suffer when crude rises sharply:

- Aviation (IndiGo, Air India, fuel is 35–40% of operating costs)

- Paints (Asian Paints, Berger, petrochemical raw material dependency)

- Tyres (MRF, Apollo, natural rubber and crude derivatives)

- OMCs like HPCL and BPCL, under-recoveries widen when retail fuel prices aren't raised

Sectors that often benefit or stay neutral:

- Oil exploration companies (ONGC, Oil India, their revenue rises with crude)

- Refiners with strong GRM (gross refining margin) positions

- Renewable energy stocks, crude spikes accelerate the political push toward alternatives

This means a 10% crude spike should not trigger the same trading response across your entire portfolio. The trader who blindly sells everything when crude moves is leaving money on the table, or worse, exiting positions that were about to work in their favour.

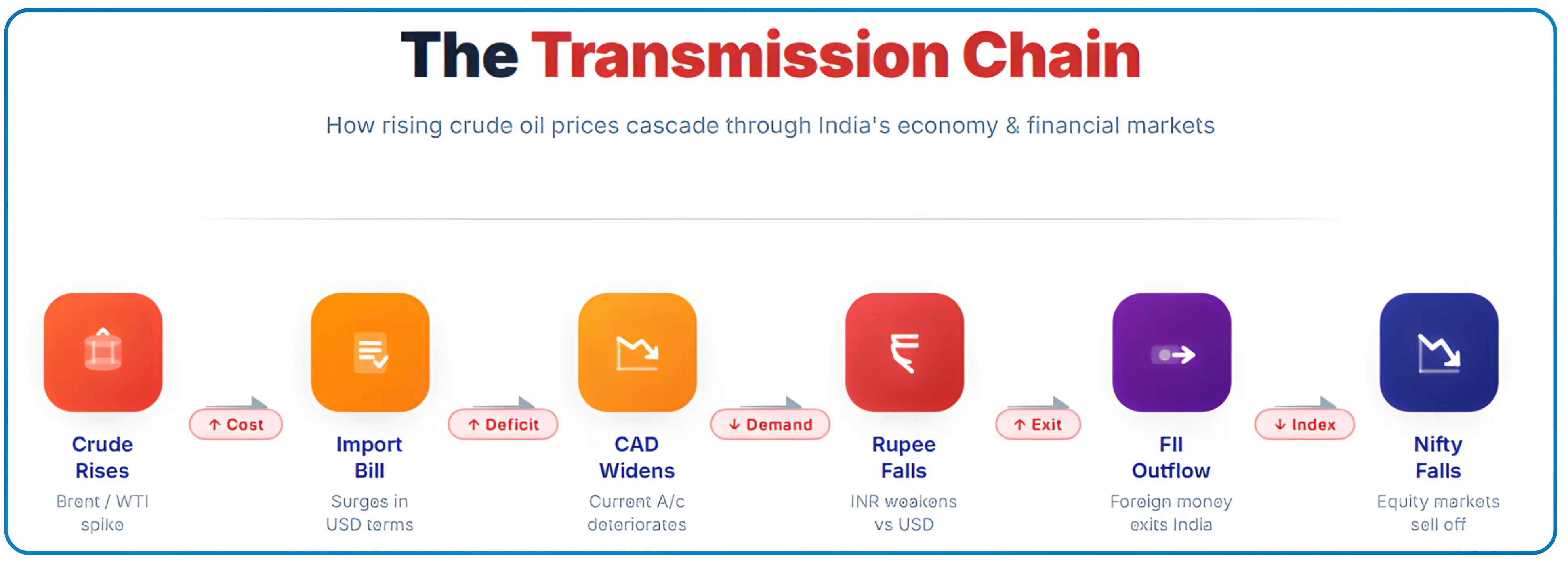

The Rupee Is the Real Transmission Belt

If you want a cleaner, more reliable indicator of how crude will affect Nifty, watch the rupee, not crude directly.

The chain that actually damages Indian markets looks like this:

Crude rises → Import bill expands → CAD widens → Rupee depreciates → FIIs pull out → Nifty falls

Higher oil costs increase demand for US dollars, leading to depreciation of the rupee; in March 2026, it hit a record low of 92.47 against the dollar.

The Indian rupee weakened against the USD to touch a record low of 92.3750, pressured by energy supply disruptions and rising crude oil prices.

Each link in that chain takes time. And the RBI actively intervenes at the rupee stage, selling dollars through PSU banks to defend the currency. When that intervention is strong, the full chain never completes, and Nifty is partially insulated even during a crude spike.

This is why tracking USD/INR alongside crude gives a far more actionable read than tracking crude alone. If crude is up but the rupee is holding, the Nifty impact is likely to be contained to sector-specific moves rather than a broad index fall.

What This Means for Your Trading

Stop using crude as a binary Nifty signal. It works in extreme supply-shock scenarios. In normal market conditions, the relationship is far too noisy to trade on directly.

Identify which sectors you're holding before reacting to a crude move. Your OMC position and your aviation position need completely different responses to the same crude spike.

Watch USD/INR and FII flow data alongside crude. Those two data points will tell you whether the crude move is actually transmitting into the broader market or staying contained to specific sectors.

The Bottom Line

India's dependency on crude oil is real, structural, and growing. At 88.2% import dependence, no serious trader can ignore oil prices.

But ignoring the complexity of how crude actually interacts with Indian equities is equally dangerous. The data shows a relationship that is conditional, sector-specific, and frequently positive, not the clean inverse rule that dominates trader conversations.

The market doesn't reward the rule everyone knows. It rewards the trader who knows when the rule breaks.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.