Over the past few quarters, we’ve tracked three standout companies shaping India’s sustainability and energy ecosystem — Gravita India, VA Tech Wabag, and Deep Industries — each playing a key role in India’s capital-efficient growth and infrastructure transformation.

This performance review revisits our earlier reports to see how these companies have delivered through Q2 FY26, across revenue growth, profitability, and execution metrics. Each operates in a different corner of the value chain, yet all share one common thread: disciplined execution and alignment with long-term structural tailwinds.

This review revisits those earlier analyses to see how the story has evolved since then. We compare their latest reported numbers against previous financials to understand what’s changed — in growth, margins, and overall strategic momentum.

Before diving into company-wise updates, here’s a snapshot of how their financial performance has progressed since our last coverage, both on a full-year (FY25 vs TTM) and quarterly (Q2 FY26 vs Q2 FY25) basis.

Quarterly Comparison (Q2 FY26 vs Q2 FY25)

| Metric (₹ Cr) | Gravita India | VA Tech Wabag | Deep Industries |

|---|---|---|---|

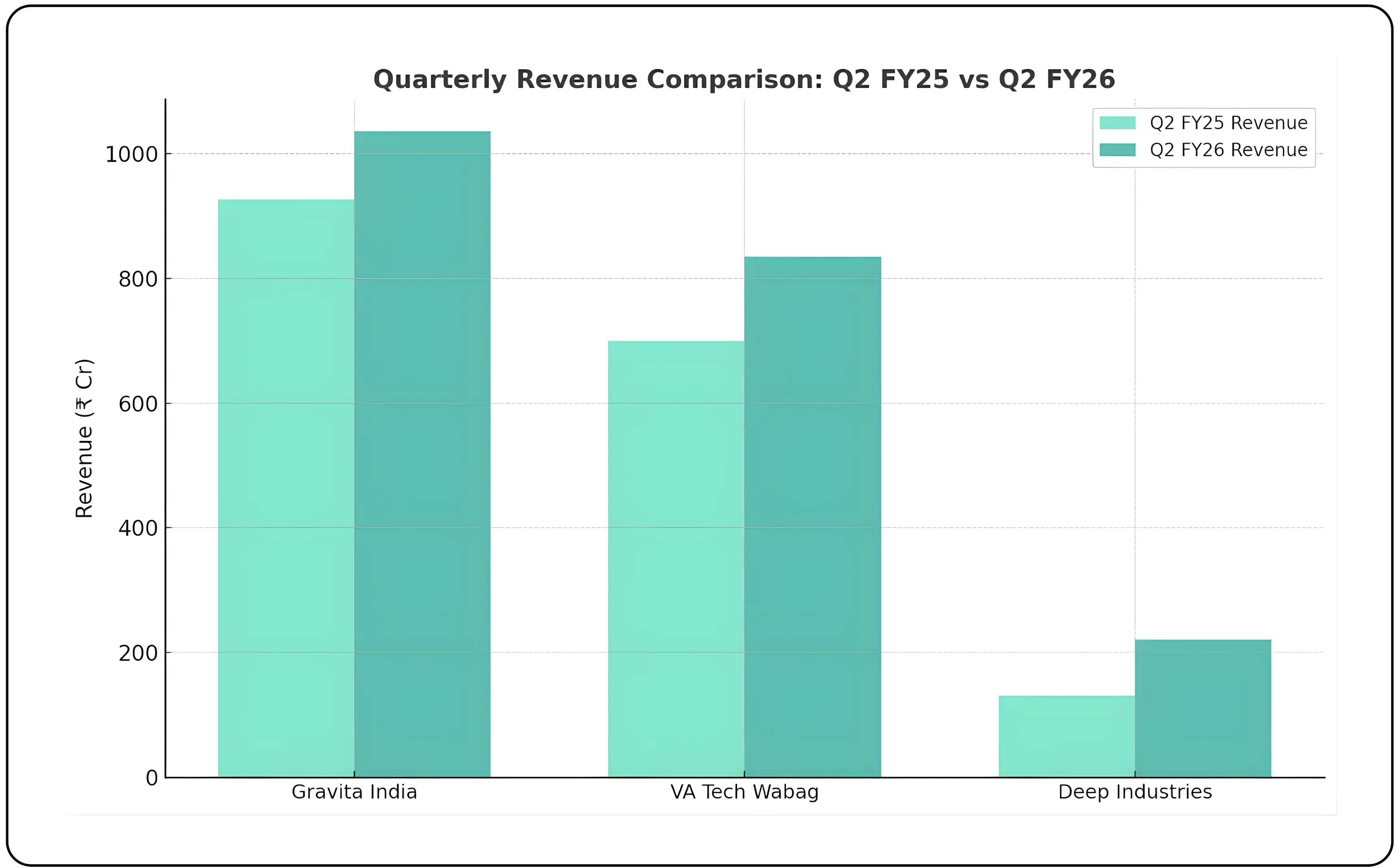

| Q2 FY25 Revenue | 927 | 700 | 131 |

| Q2 FY26 Revenue | 1,036 | 835 | 221 |

| Revenue Growth YoY | +12% | +19% | +69% |

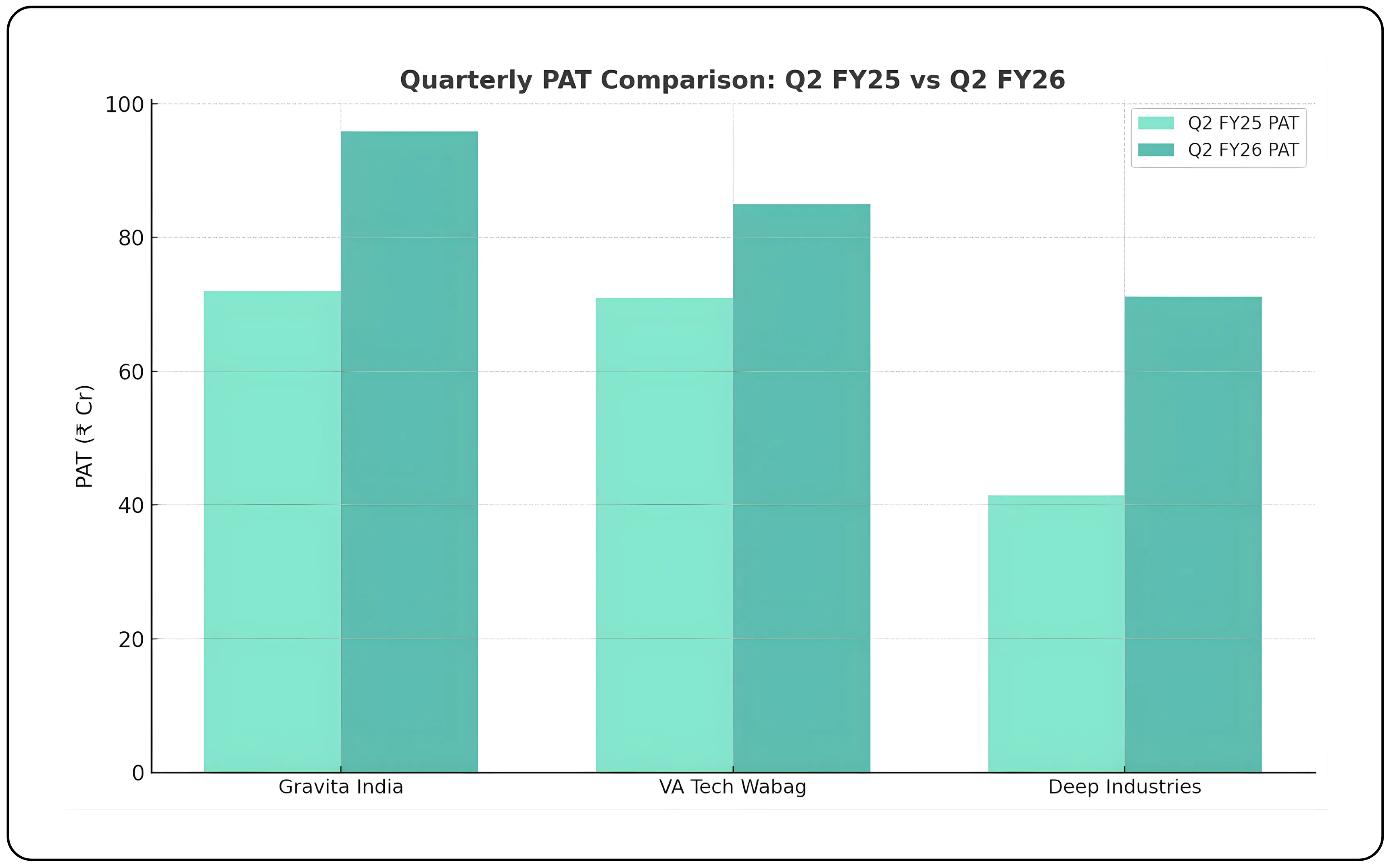

| Q2 FY25 PAT | 72 | 71 | 41.5 |

| Q2 FY26 PAT | 95.9 | 85 | 71.2 |

| PAT Growth YoY | +33% | +20% | +71% |

| EBITDA Margin (Q2 FY25) | 10.7% | 14.7% | 46.9% |

| EBITDA Margin (Q2 FY26) | 10.8% | 14.4% | 46.6% |

| Commentary | Stable margins, strong domestic sourcing |

Consistent project execution | Exceptional quarterly scale-up |

Gravita India: Registered a 12% YoY increase in Q2 revenue, reflecting steady demand and higher domestic scrap availability.

VA Tech Wabag: Revenue grew 19% YoY, with execution gains across desalination and wastewater treatment projects both in India and overseas.

Deep Industries: Led the group with a 69% YoY spike in quarterly revenue, thanks to new contract commencements and incremental offshore activity.

Gravita: Profit jumped 33%, aided by margin stability and operational efficiency.

Wabag: Posted 20% PAT growth, maintaining healthy returns on an expanding project base.

Deep Industries: PAT rose an impressive 71%, translating its top-line surge directly into bottom-line strength, underlining operating leverage in its new contracts.

Financial Performance Snapshot – FY25 vs TTM (as of Q2 FY26)

| Metric (₹ Cr) | Gravita India | VA Tech Wabag | Deep Industries |

|---|---|---|---|

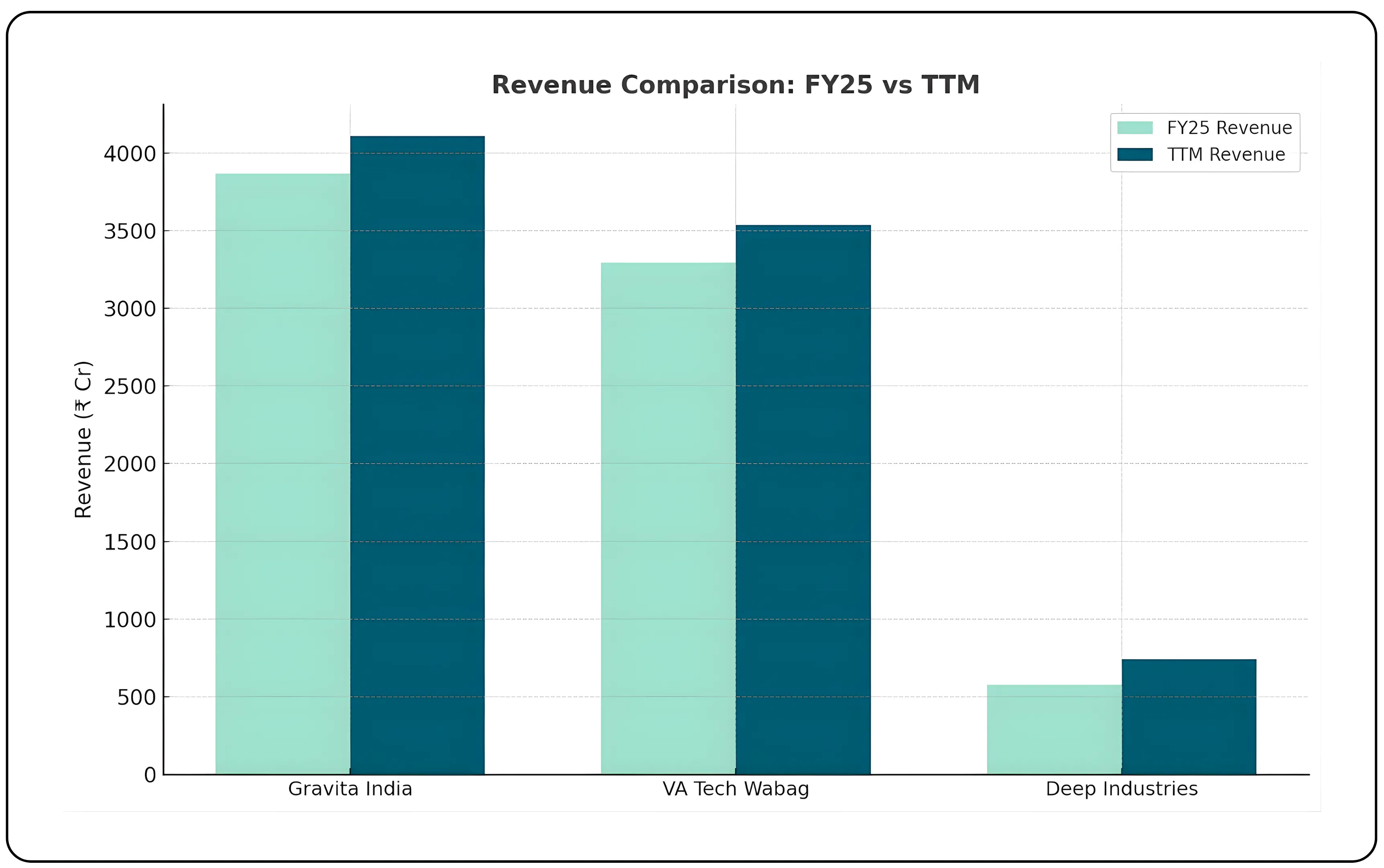

| FY25 Revenue | 3,869 | 3,294 | 576 |

| TTM Revenue | 4,109 | 3,536 | 743 |

| Growth YoY | +6.2% | +7.3% | +29.0% |

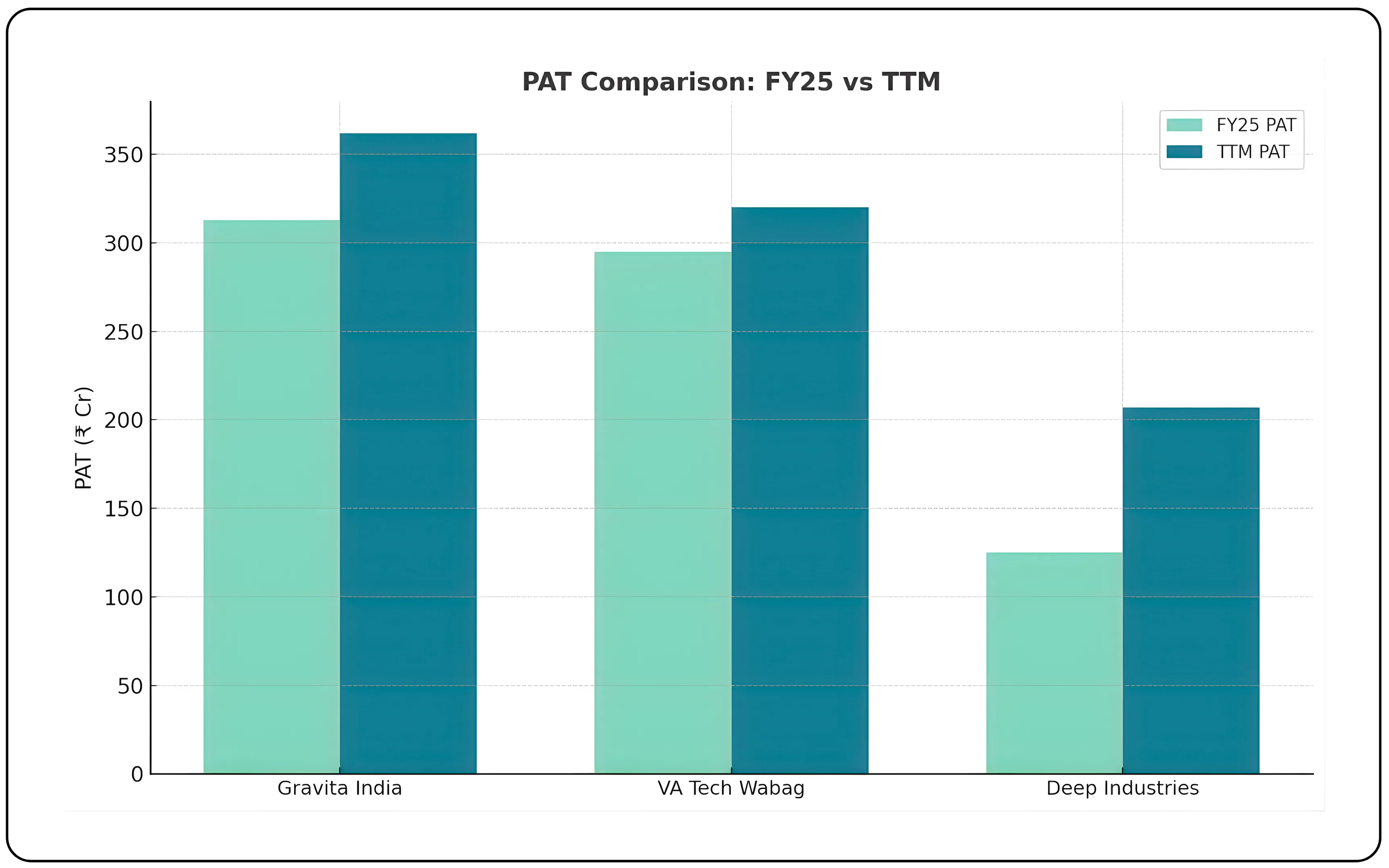

| FY25 PAT | 313 | 295 | 125 |

| TTM PAT | 362 | 320 | 207 |

| PAT Growth YoY | +15.6% | +8.5% | +65.6% |

| EBITDA Margin (FY25) | 8.0% | 13.0% | 42.0% |

| EBITDA Margin (TTM) | 9.0% | 12.0% | 40.0% |

| Key Shift | Margin expansion, higher value-added mix |

Stable execution and order flow |

Profit inflection from PEC & offshore gains |

TTM = Trailing Twelve Months as of Q2 FY26.

Gravita India: Maintained its growth rhythm, with TTM revenue up 6% YoY, crossing ₹4,100 crore, supported by higher recycling volumes and a stronger value-added mix.

VA Tech Wabag: Saw a 7% YoY increase in TTM revenue to ₹3,536 crore, driven by solid project execution and sustained international order flows.

Deep Industries: Delivered the most striking growth — a 29% revenue surge, reaching ₹743 crore, reflecting the ramp-up of its long-term Production Enhancement Contract with ONGC and offshore service contributions.

Gravita: TTM PAT grew 15.6%, reaching ₹362 crore, driven by stable margins and improved product mix.

Wabag: Profit rose 8.5% to ₹320 crore, maintaining consistent performance backed by O&M cash flows and disciplined execution.

Deep Industries: PAT surged 65.6% to ₹207 crore — its highest ever — supported by exceptional margins in PEC and charter-hire operations.

Gravita India – From Stability to Acceleration

When we last covered Gravita in May 2025, management had guided for 25% volume CAGR, 35% profit growth, and a push toward 50% value-added revenue under its Vision 2029 roadmap.

Seven months later, the company looks firmly on track.

What’s Changed Since Our Last Report

Growth Trajectory: Gravita’s H1 FY26 performance validates its scale-up plan — both revenue and profit growth are trending comfortably within management’s multi-year guidance band.

Margins: The company has sustained double-digit EBITDA margins (10.8%) despite volatility in lead prices, helped by a rising share of refined alloys and efficient hedging.

Value-Added Progress: The mix of value-added products has reached 47% of revenue, versus 46% in FY25 — moving steadily toward the 50% medium-term goal.

Geographic Sourcing: Domestic scrap procurement has improved to 52%, up from 36% last year — directly supporting working capital efficiency and margin protection.

Capital Efficiency: The company cut its total capex outlay to ₹1,225 crore (from ₹1,500 crore earlier) by focusing on brownfield expansion. Payback continues to remain under three years per project.

The company’s emphasis on value-added alloys and improved scrap sourcing supports long-term margin expansion and positions Gravita as a leading name among sustainability stocks focused on the circular economy theme.

Management Outlook and Guidance

| Theme | Management Takeaway | Benefit to Company |

|---|---|---|

| 1. Capital-efficient Expansion | Shifted from Greenfield to Brownfield projects at Mundra and Phagi, reducing total capex from ₹1,500 Cr → ₹1,225 Cr. |

Lower capital intensity improves ROIC; faster capacity rollout without straining balance sheet. |

| 2. Lead Business Strength | Sustainable EBITDA guidance raised from ₹18–19/kg to ₹19–20/kg; strong Q2 realization ₹23/kg aided by value-added products (VAP) and arbitrage. |

Improves profitability and earnings predictability in core segment. |

| 3. Value-Added Product Focus | VAP share at 46% of volumes; target 50%. Adds 2.5–3% margin uplift. | Enhances margins and brand positioning; reduces commodity price sensitivity. |

| 4. Feedstock Security via BWMR/EPR | Domestic scrap sourcing rose to 52% (vs 36% YoY). Regulatory tightening improving availability. |

Ensures raw material security, reduces import dependence, stabilizes input cost. |

| 5. Aluminium Optionality via MCX Hedging | Awaiting MCX ADC12 launch; once active, enables hedging and access to OEM/Tier-1 auto customers. |

Unlocks margin stability, scale-up potential, and possible M&A opportunities in aluminium vertical. |

| 6. Diversification into Non-Lead Verticals | Rubber plant (Q4 FY26), lithium-ion pilot (Q3 FY26) to diversify revenue; aim 30% non-lead by FY27/2029. |

Reduces concentration risk; taps new recycling markets (tyre, lithium). |

| 7. Geographic Expansion | Capacity ramp in Romania, Dominican Republic (pending), and Eastern India under planning. |

Broadens geographic footprint, hedges geopolitical/regulatory risks. |

| 8. Strong Balance Sheet | Company remains net debt-free; disciplined capex of ₹206 Cr for FY26. |

Provides flexibility for acquisitions and new ventures. |

| 9. Operational Efficiency | Arbitrage strategy (routing overseas semi-finished goods to India) boosts margins though reduces reported volumes. |

Optimizes profitability despite accounting volume distortion. |

| 10. ESG & Long-Term Vision | Vision 2029: Volume CAGR >25%, profit >35%, ROIC >25%, 30% energy from renewables. |

Aligns financial performance with sustainability goals, appealing to ESG investors. |

Overall, Gravita has delivered exactly as guided — maintaining profitability, capital discipline, and balance sheet strength while setting up new engines of growth. Gravita’s capital allocation discipline and capacity expansion under Vision 2029 remain on track — a clear example of capital-efficient growth in India’s recycling sector.

For a deeper look at Gravita’s business model and Vision 2029 roadmap, read our earlier analysis.

VA Tech Wabag – From Resurgence to Sustainable Growth

When we profiled Wabag in June 2025, management outlined a clear 3–5 year roadmap: 15–20% revenue CAGR, EBITDA margins between 13–15%, ROCE above 20%, and O&M share near 20% of revenue. Wabag’s Q2 FY26 update highlights stable growth momentum and continued leadership in the water infrastructure space, backed by a healthy order book and cash flow position.

What’s Changed Since Our Last Report

Execution and Scale: H1 FY26 results show that Wabag is tracking within its revenue and margin guidance — growth at 18% and EBITDA margin at 13.8% are both in line with the stated range.

Order Visibility: The order book has expanded from ₹15,900 crore at the time of our last coverage to ₹16,020 crore now, maintaining roughly 4x annual revenue visibility.

Cash Position: The company has stayed net cash positive for the 11th consecutive quarter, a key validation of its asset-light execution strategy.

Diversification: New contracts in Compressed Bio-Gas (CBG) and AI-driven digital water management mark tangible progress in its push toward “future energy and water solutions.”

Working Capital Efficiency: Net working capital days have improved to 121, indicating better cash conversion and receivable management — a recurring challenge that Wabag seems to have structurally addressed.

Management Outlook and Guidance

The management reaffirmed its medium-term targets:

Revenue CAGR: 15–20% led by strong international and domestic order inflows.

EBITDA Margin: 13–15% with steady annuity contribution from O&M contracts.

ROCE and ROE: ROCE above 20% and ROE above 15% while maintaining a net cash position.

New Growth Verticals: The company also highlighted Bio-Gas, Green Hydrogen, and Ultra-Pure Water (UPW) as incremental opportunities over the next 2–3 years.

Net result: Wabag continues to deliver exactly what it had promised — steady, capital-efficient growth and consistent margins, now supported by ESG-aligned adjacencies that broaden its addressable market.

Wabag remains well positioned within India’s sustainability and infrastructure theme, balancing growth visibility with asset-light execution.

Explore our earlier research on how VA Tech Wabag is positioning itself as a global leader in sustainable water infrastructure here.

Deep Industries – Capturing the Energy Upswing

Deep Industries’ Q2 FY26 analysis marks a turning point — profit inflection driven by the ONGC Production Enhancement Contract (PEC) and rapid expansion in offshore services.

When we last analyzed Deep Industries, management was entering FY26 with three clear strategic levers:

- Monetization of the ₹1,402 crore ONGC Production Enhancement Contract (PEC) over 15 years.

- Expansion into offshore services via Dolphin Offshore Enterprises.

- Debt-light growth with double-digit returns and 30%+ PAT margins.

What’s Changed Since Our Last Report

PEC Impact Visible: With operations commencing in April 2025, the ONGC PEC has started reflecting in both revenue and margin performance, contributing heavily to the 65% YoY surge in H1 FY26 profit.

Offshore Operations Ramped Up: Dolphin Offshore’s Prabha-DP2 barge began commercial service in May 2025 and has opened new high-margin opportunities in marine logistics and offshore energy support.

Order Book Strengthened: From ₹2,960 crore at the time of our earlier coverage to ₹3,050 crore currently, with robust pipeline visibility from both onshore and offshore contracts.

Financial Discipline: Despite expansion, leverage remains low (Debt-to-Equity 0.10), while ROE has improved to 14.9% (annualized).

Execution Diversification: The company now covers 70% of the post-exploration oil & gas services chain, offering integrated project management, charter-hire, compression, and dehydration services.

Management Outlook and Guidance

Management continues to maintain a positive medium-term stance, projecting:

- 30%+ PAT margins and double-digit revenue CAGR driven by PEC and offshore charters.

- A steady rise in offshore contribution through additional assets under Dolphin Offshore.

- Expansion of integrated onshore services through new charter-hire contracts with PSUs and private operators.

- Continued focus on balance sheet strength with ROE expected to improve further in FY27 as offshore utilization stabilizes.

Overall, Deep’s management has executed ahead of expectations, transforming the company from a niche onshore player into a diversified oilfield services enterprise with long-term cash visibility.

Deep’s high-margin PEC and offshore contracts highlight its capital-efficient business model and position it among India’s emerging energy infrastructure and sustainability plays.

Read our detailed coverage on Deep Industries and its evolving role as a proxy play on India’s oil and gas upcycle here.

Closing View

Comparing today’s results with management guidance from mid-2025 reveals a clear pattern — all three companies are executing in line with or ahead of what they had promised:

Gravita: Has balanced growth with profitability, keeping its Vision 2029 targets intact.

Wabag: Has delivered consistent margins, efficient cash cycles, and strong order visibility.

Deep Industries: Has exceeded early expectations, achieving both scale and profitability faster than guided.

Together, Gravita India, VA Tech Wabag, and Deep Industries reflect the evolving face of sustainability and infrastructure investing in India — combining strong TTM financial performance, margin consistency, and capital-efficient growth models that align with long-term national priorities.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.