For an updated look at FY26 performance trends, read our latest analysis – A Performance Review of Gravita India, VA Tech Wabag, and Deep Industries. It revisits these companies’ financials, margins, and strategic progress since our previous analyses.

Deep Industries Limited (DIL) is a leading service provider in India’s energy sector, established in 1991. The company offers a complete range of equipment and services for oil and gas field operations, especially for upstream and midstream activities. These are provided on a rental and charter-hire basis, making it a convenient ‘one-stop solution' for exploration, production, and processing work in varied and tough environments.

Based in India but growing internationally, DIL uses its fleet of fuel-efficient machines, skilled technical staff, and strong project management to meet the complex needs of the oil and gas industry. By renting out equipment and services, DIL helps its clients avoid the high costs of ownership, allowing them to focus on their core business without heavy investments.

Service portfolio

1. Upstream services– Where energy exploration begins

The upstream segment deals with the exploration and production of oil and gas. DIL plays a key role here by providing technical expertise and turnkey project execution.

Drilling and workover services

Drilling and workover is the actual digging and maintenance of oil wells. DIL is among the top onshore service providers in India with over 13 years of hands-on experience. The company operates a robust fleet of rigs, including workover rigs ranging from 150 HP to 1000 HP and drilling rigs from 350 HP to 1500 HP. It also has specialized rigs for Coal Bed Methane (CBM) fields, such as air drilling and slim hole rigs.

DIL offers a full suite of services like well stimulation, fishing, casing retrieval, logging, perforation, multi-zone completions, and coil tubing. Its teams work in challenging terrains like deserts, hilly areas, and ecologically sensitive zones. All services are provided on either a charter hire or dry lease basis, giving clients flexibility based on their project needs.

Integrated project management (IPM) services

In 2016, DIL introduced a game-changer — Integrated Project Management (IPM). This model brings all necessary services under one contract, ensuring smooth project delivery from start to finish. Key offerings include turnkey solutions for drilling, workover, and coring operations. It also covers essential support services like mud engineering, logging, cementing, well testing, and hydro-fracturing, along with pipeline laying, accommodation, fuel supply, and maintenance.

DIL maintains a vast rental inventory that includes well control tools, cementing units, solid control systems, portable cabins, and other critical equipment. In short, DIL’s IPM services are built to deliver cost-effective, high-quality, and time-sensitive execution for oil and gas companies.

2. Midstream services – connecting the flow

Midstream services ensure that gas extracted from the earth is treated, processed, and transported safely and efficiently. DIL has built a dominant presence here too.

Air and gas compression services

DIL is India’s largest private player in high-pressure Natural Gas Compression, commanding a market share of over 95%. The company operates more than 100 natural gas compressors, with a combined capacity exceeding 100,000 HP. It offers flexible service models, including Build-Own-Operate (BOO), Build-Own-Operate-Transfer (BOOT), and Build-Own-Operate-Maintain (BOOM). With a fully trained in-house team and round-the-clock support, DIL ensures minimal downtime and maximizes operational uptime.

Gas dehydration, conditioning & processing

This service focuses on making natural gas “pipeline-ready” by removing moisture and impurities. DIL provides mobile, scalable, and modular gas processing solutions. Currently, the company operates 11 gas dehydration plants with a combined capacity of 140 MMSCFD. Their offerings include dew point reduction and EPC work for surface facilities and gas treatment units. DIL also provides mobile treating fleets that are available either for rent or as turnkey projects. Multiple engagement models are offered, including Build-Own-Operate (BOO), Build-Own-Operate-Transfer (BOOT), bare rental, or operations and maintenance (O&M)-only options.

Execution efficiency

Deep Industries demonstrates industry-leading execution timelines, completing projects in just 4–6 months, significantly faster than the typical 10–12 month cycle. This is achieved through the deployment of mobile and reconfigurable units. With an operational efficiency rate of 99.6%, driven by strong asset utilization and readiness, the company ensures minimal idle time and rapid contract turnaround.

Strategic positioning

Deep Industries Limited (DIL) has established itself as a leading integrated oilfield services provider in India, with a dominant position in the post-exploration segment. Through its multi-vertical offerings across gas compression, dehydration, drilling, project management, and processing, the company is uniquely positioned to capitalize on India's evolving upstream and midstream oil & gas infrastructure.

Market leadership

Deep Industries commands over 70% market share in India’s post-exploration oil and gas services segment, driven by technical depth, operational agility, and long-standing partnerships with clients like ONGC, Oil India, and Vedanta. In FY24, ONGC contributed ~44% of revenues, with Oil India and Vedanta accounting for ~10% each—ensuring strong revenue visibility.

The company holds a competitive position across verticals:

Drilling & workover: Significant share supported by PSU contracts and international approval from Kuwait Oil Company.

Integrated project management (IPM): Turnkey execution model reduces client coordination and project costs.

Gas compression: Market leader with domestic dominance and global exposure via Deep International DMCC.

Gas dehydration: One of India’s largest BOO service providers.

Gas processing & EPC: First Indian firm to offer end-to-end gas processing on a charter-hire basis.

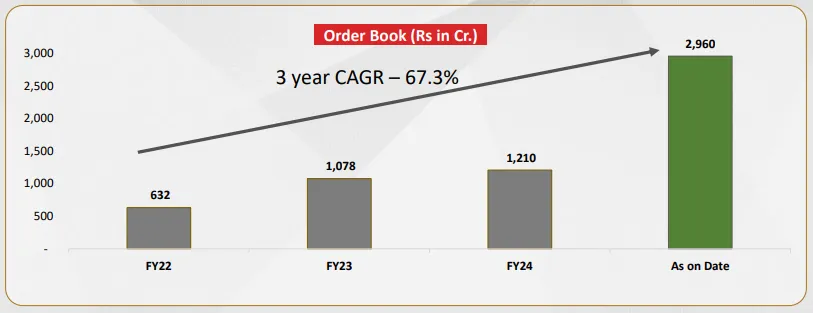

Expanding order book

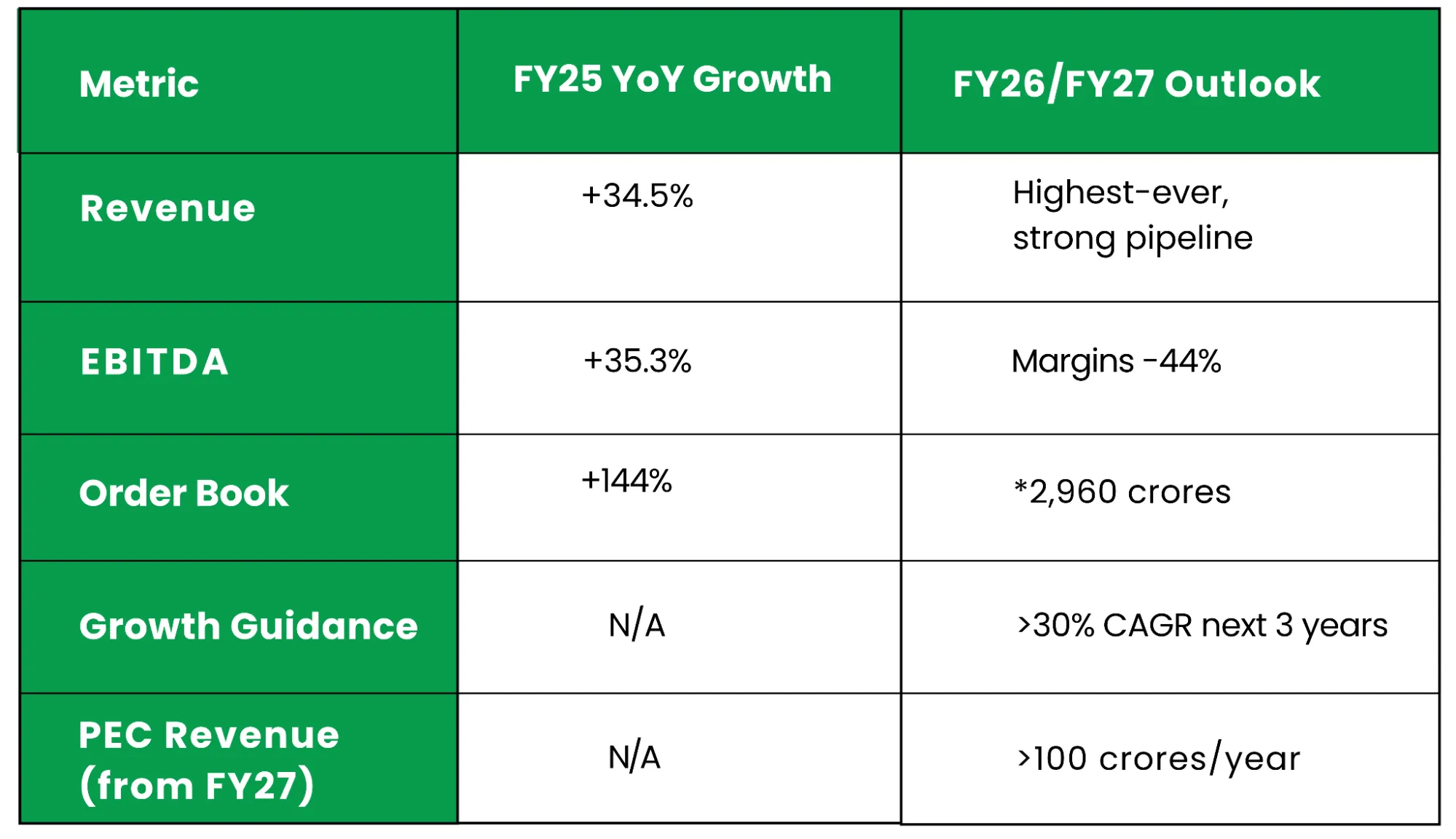

As of Q4 FY25, Deep Industries’ order book expanded to ₹2,960 crores, marking a more than fourfold increase from FY22 levels (~₹630 crore). This growth underscores the company’s execution capabilities and increasing demand for its specialized services.

Recent key wins include an ₹81 crore contract from Oil India for a 1000 HP mobile rig and an ₹82 crore order from ONGC for 100MT and 150MT workover rigs. These awards reflect DIL’s strong positioning in the charter-hire segment and its ability to efficiently convert opportunities into firm orders.

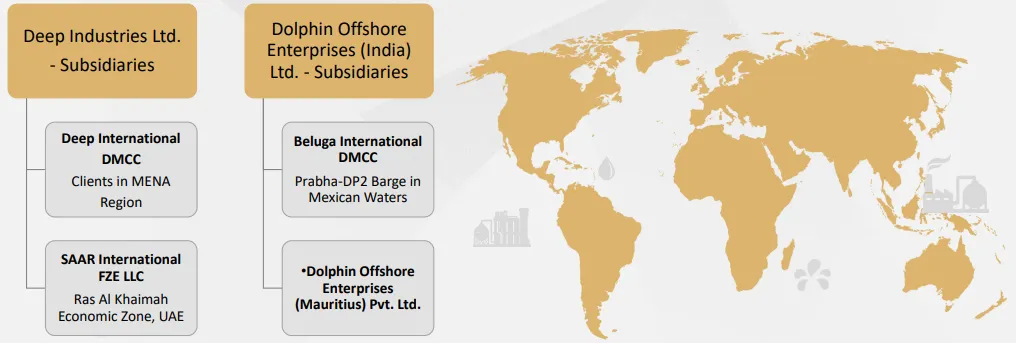

Strategic acquisitions & global expansion

Deep Industries has pursued strategic acquisitions and international expansion to strengthen its service portfolio and geographical reach. A 75% stake in Dolphin Offshore Enterprises (market cap: ₹2,670 crore as of July 2024) brings the high-margin barge Dolphin Vikrant (Prabha) into operation, with revenue contribution expected in H1 FY25 and EBITDA margins of ~60%.

The company also incorporated SAAR International FZ-LLC in the UAE in March 2024, marking its entry into the Middle East through oilfield equipment, solar systems, and trading operations.

Further diversification includes acquisitions via the IBC route—Dolphin Shipping, enhancing offshore support capabilities, and Kandla Energy & Chemicals Ltd, aimed at strengthening energy logistics and asset utilization.

These strategic moves position Deep Industries for long-term domestic and international growth across the energy services value chain.

Financial performance

Deep Industries Limited delivered strong financial results in Q4 FY25, highlighting strong operational momentum and strategic execution.

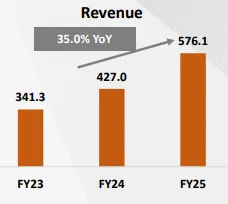

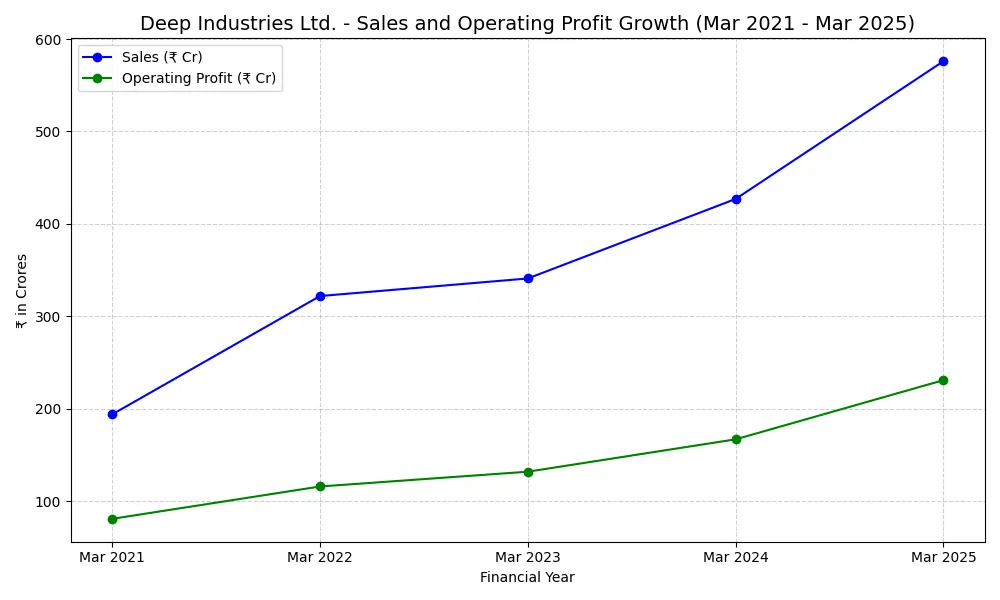

Operating revenue for FY25 rose 35% YoY to ₹576.1 crores. This growth was supported by healthy execution across gas services and drilling segments. FY25 became the company's highest-ever year for revenue, EBITDA, and net profit.

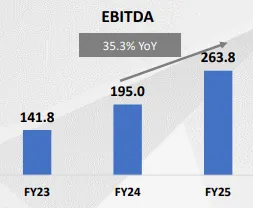

EBITDA surged 35.3% YoY in FY25 to ₹263.8 crores, with margins improving to 43.4%, compared to 39% in FY24. This reflects improved operating leverage, disciplined cost control, and higher realization from existing contracts.

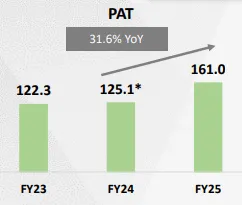

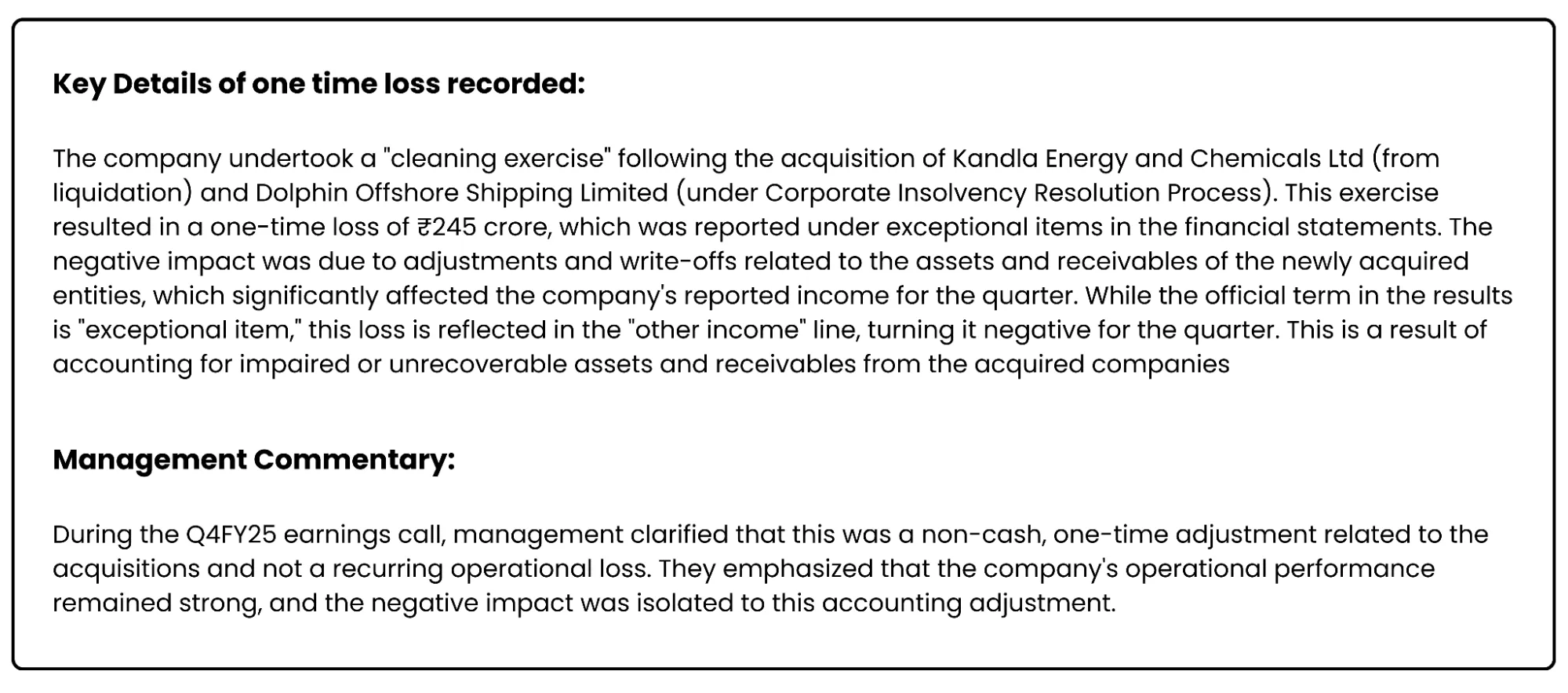

Net Profit: Deep Industries Ltd reported a significant negative figure under "other income" in its Q4FY25 results, amounting to approximately ₹245 crores. The primary reason for this negative other income is linked to a one-time loss recognized as an exceptional item during the quarter. The actual PAT attributable to owners has risen to ₹161 crores for FY25, excluding the ₹44 crore exceptional gain in FY24 and the exceptional loss in FY25. This means the ₹161 crore profit reflects the company's core operational performance, without the impact of one-time gains or losses recorded in FY24 and FY25.

Future revenue visibility

The barge project (Dolphin Vikrant) is almost complete, with deployment expected in Q4 FY25. Management anticipates this asset to generate substantial EBITDA, with early revenue contributions expected from Q1 FY26.

Deep Industries has secured a ₹1,402 crores Production Enhancement Contract from ONGC for 15 years, aimed at boosting output from one of ONGC’s mature fields, with service revenue linked to 64% of the incremental production revenue. Ground-level operations began in April 2025, with the majority of revenue expected in the first 10 years. The company also owns the DP2 barge Prabha through its subsidiary Beluga International DMCC, Dubai. DP2-class barges are in high demand due to their advanced capabilities and are expected to deliver strong daily rentals with EBITDA margins around 60%. A lease agreement has been signed with Mexico-based Ballast Shipping S.A. DE C.V. for three years, with an estimated contract value of US$32.85 million (~₹281 crores).

Management has guided for 30%+ CAGR in revenue for the next three years, supported by the scale-up of PEC projects, charter hiring services, and international expansion. From FY27 onward, PEC contracts alone are expected to contribute over ₹100 crore annually, offering long-term annuity-like income streams.

In summary, Deep Industries is on a strong financial trajectory, marked by consistent revenue growth, margin expansion, and record order inflows. These trends, alongside policy tailwinds and execution capabilities, suggest continued earnings momentum over the medium term.

Financials future outlook

Industry outlook

India’s oil and gas services sector is poised for robust growth, supported by structural reforms, rising domestic energy demand, and government initiatives aimed at reducing import dependency. Deep Industries stands to benefit significantly from these industry tailwinds. With growing pipeline infrastructure, demand for reliable compression solutions is expected to rise.

Policy Support and Sector Reforms

Recent amendments to the Oilfields Regulation and Development Act signal a more transparent and stable regulatory framework. These reforms are expected to attract private and foreign investments, streamline exploration and production activities, and improve lease tenure certainty. Incentives for enhanced oil recovery (EOR), formal dispute resolution mechanisms, and lower entry barriers provide a conducive environment for service providers like Deep Industries to scale operations.

Rising Domestic Production Focus

India currently imports over 85% of its crude oil needs, prompting the government to aggressively push for enhanced domestic exploration and production (E&P). State-run companies like ONGC and Oil India are ramping up project activity, offering long-term visibility to upstream service providers. The Production Enhancement Contract (PEC) model, in which Deep Industries is an early mover, is expected to become a key channel for reviving marginal and mature fields.

Energy Security and Diversification

The broader policy shift towards energy self-reliance ("Atmanirbhar Bharat") and security is accelerating investment in both conventional and unconventional hydrocarbons. This includes coal bed methane (CBM), shale gas, and tight oil—all areas where Deep Industries has the technical capability and prior execution experience. Expansion into these verticals aligns with the company’s strategic intent to diversify and future-proof its service offerings.

Growth in Gas Infrastructure and Services

As India aims to increase the share of natural gas in its energy mix to 15% by 2030 (from ~6% currently), infrastructure development—including pipelines, gas processing, and dehydration—is expected to grow substantially. Deep Industries’ leadership in gas compression, dehydration, and charter-based gas processing services makes it a direct beneficiary of this macro trend.

Competitive Landscape and Differentiation

Despite a fragmented and contract-based market structure, Deep Industries has emerged as a dominant player by offering integrated services, faster project turnaround, and value-added offerings like EPC-based gas processing facilities. Its entry into high-margin, long-duration projects like PEC and offshore support (via Dolphin Vikrant) will further enhance its competitive positioning.

Global Opportunities

Through subsidiaries in the Middle East and potential offshore service expansion, Deep Industries is strategically placed to capture international opportunities. The Middle East, in particular, remains a high-growth, service-intensive market, and Deep’s expanding fleet and execution track record are key enablers.

Deep Industries is well-positioned to capitalize on strong sector tailwinds, with a record order book, robust financial performance, and a growing presence across core and emerging service segments. Strategic expansion into Production Enhancement Contracts and offshore support, along with consistent execution and sector reforms, provide long-term growth visibility. With over 30% expected revenue CAGR, the company is poised for sustained value creation.