India's wires and cables industry has emerged as one of the more understated beneficiaries of the country's electrical infrastructure expansion, quietly powering everything from power transmission networks to renewable energy installations. Unlike sectors that depend on a single policy cycle or government programme, this industry draws demand from several structural growth drivers at once: power transmission, residential and commercial construction, railways, telecommunications, and renewable energy. Each of these is scaling independently, and each requires cables at every stage of development. Few industries can claim that kind of demand breadth, and fewer still can claim that it is growing across all fronts simultaneously.

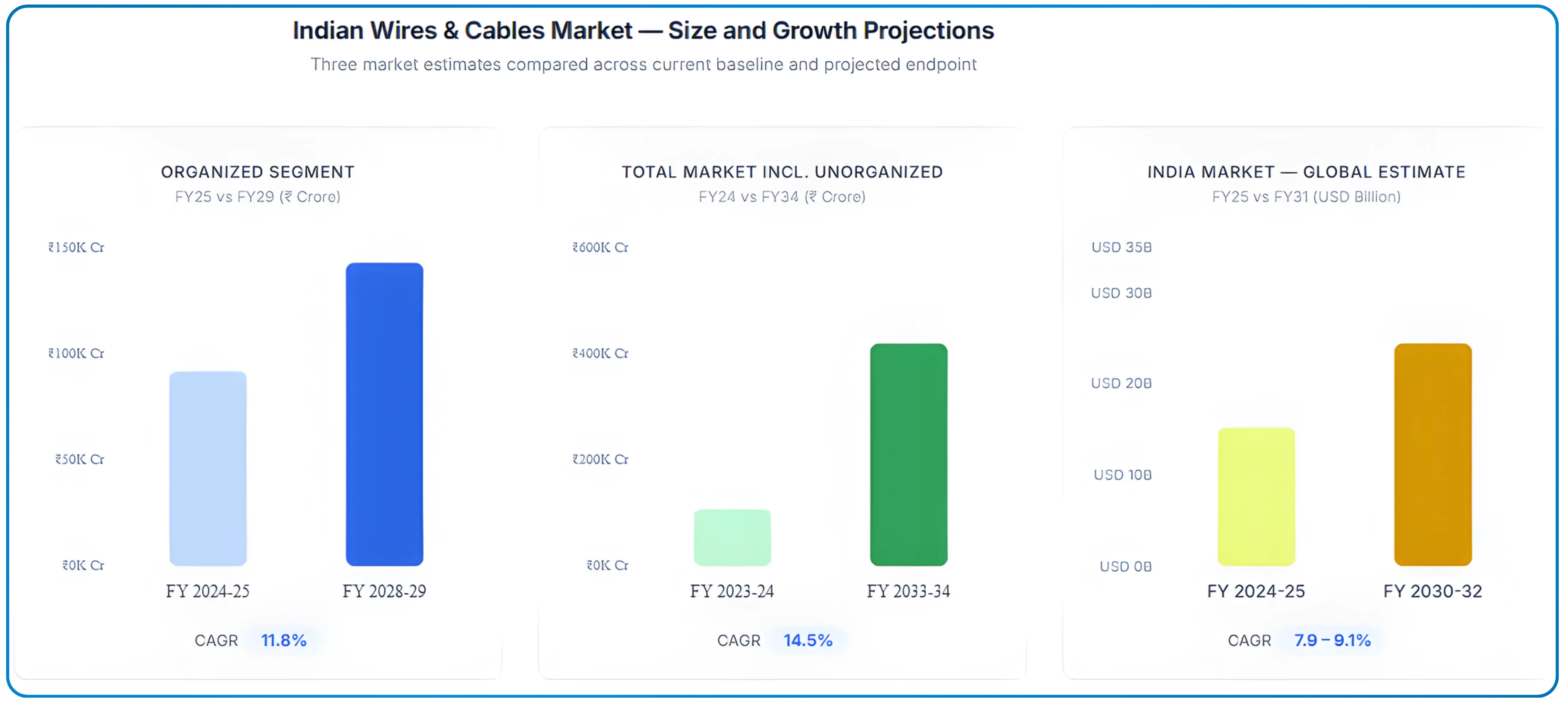

The organized segment of the Indian cables market was valued at approximately ₹92,000 crore (around ₹920 billion) in FY 2024-25 and is projected to reach ₹1,43,000 crore by FY 2028-29, implying a compounded growth rate of around 11.8% annually. On a broader basis that includes the unorganized segment, the total market is estimated at ₹1,08,370 crore in FY 2023-24 and could scale to ₹4,19,728 crore by FY 2033-34 at a 14.5% CAGR. Global estimates put the Indian market at USD 9.32–21.22 billion in 2024-25, rising to USD 17–32 billion by 2030-32, with growth rates ranging from 7.9% to 9.1% CAGR.

The global wires and cables industry was valued at USD 214.5 billion in 2023 and is expected to reach USD 402 billion by 2032 at a 5% CAGR. India's share in the global market currently stands at approximately 5%, with room to grow significantly as domestic manufacturing scales up under the China+1 supply chain shift.

The key factors shaping the next phase of growth include backward integration, export certifications, and product premiumization

Indian Wires and Cables Industry: Market Structure

The industry broadly falls into two segments: organized and unorganized. The organized sector currently commands around 72% of the market and is expected to cross 80% by FY 2027 as quality mandates, BIS certifications, and brand preference push buyers away from unbranded products. This formalization trend is one of the structural tailwinds benefiting listed manufacturers. Organized players are gaining ground as BIS enforcement and brand awareness push buyers away from unbranded alternatives.

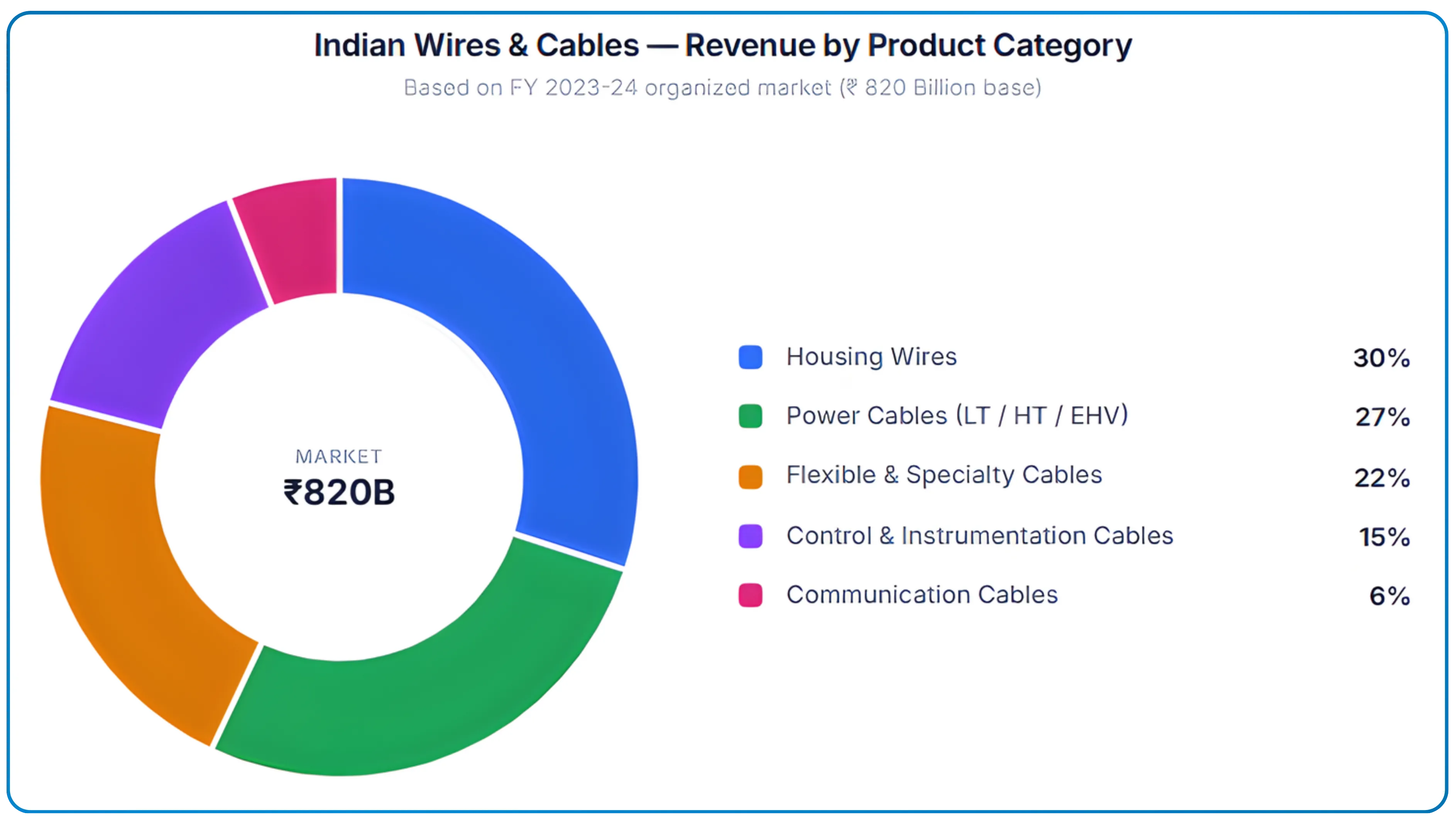

By product category, housing wires account for 30% of industry revenues, followed by power cables (LT/HT/EHV) at 27%, flexible and specialty cables at 22%, control and instrumentation cables at 15%, and communication cables at 6%. The mix is shifting toward higher-value-added products as infrastructure complexity increases.

Low voltage cables alone are widely used across residential, commercial, and industrial buildings, making them the single most consumed category by end user volume. Medium voltage cables are essential for power distribution in urban infrastructure projects, and their demand is scaling alongside city expansion and smart grid deployments.

The industry is also clearly bifurcated between companies that are primarily retail-facing (selling building wires and house wires to electricians and contractors through dealer networks) and companies that are project-oriented, supplying power cables and conductors to utilities, EPC contractors, and government bodies through tendered orders. Several large players straddle both. The retail segment typically carries better margins, while the institutional segment offers scale and long-term order visibility.

Key Factors Driving Demand in the Cables Market

Power Sector: Solar and Wind Power Transmission

The single biggest driver for the industry is India's energy transition. The government has targeted 500 GW of non-fossil fuel installed power capacity by 2030. India reached 475 GW of total installed capacity in FY 2024-25, with renewable energy accounting for 86% of all new additions in the year. Every solar park, wind farm, and battery storage system needs specialized cables to move power from the generation point to the grid. A 1 MW solar installation alone requires approximately 50 kilometres of cable; scaling that to India's 100 GW solar target gives a sense of the volume involved. Every solar and wind power installation adds to cable demand at the generation, transmission, and distribution stage.

The Revamped Distribution Sector Scheme (RDSS), with a total outlay of ₹3.03 lakh crore over 2021-2026, is funding upgrades to the distribution network across states (smart metering, underground cabling, and feeder separation) all of which are cable-intensive activities. At the transmission level, over ₹3.5 lakh crore in investment is planned across T&D infrastructure over the next five years.

Smart grid projects are increasing the demand for advanced power cables that enable real time monitoring, automated load management, and bidirectional power supply, making cable infrastructure a core component of the country's grid modernization agenda.

Smart grid technology is increasingly viewed as a strategic infrastructure investment that will support long term economic growth and help India achieve its carbon reduction goals, directly expanding the addressable market for specialized cables.

The increasing demand for cables is directly linked to India's shift toward renewable energy sources, with every new solar and wind installation requiring substantial cabling across the value chain.

Electrical Wires Demand: Infrastructure and Construction Industry

The Union Budget for FY 2025-26 allocated ₹11.21 lakh crore for capital expenditure, representing 3.1% of GDP. This is the highest-ever infrastructure budget and essentially guarantees a multi-year order pipeline for the cables sector. Railways alone received a ₹2.52 lakh crore allocation for FY 2025-26. Indian Railways has electrified 62,119 route kilometres (94% of the broad gauge network) as of March 2024, with metro rail expansion, high-speed corridors, and signalling upgrades adding further cable demand.

The Pradhan Mantri Awas Yojana (PMAY) housing scheme had an outlay of ₹88,327 crore, supporting residential construction and therefore demand for housing wires. Construction capex is projected to grow 1.4x, from ₹12.5-13.5 lakh crore (FY 2019-24) to ₹18-19 lakh crore (FY 2024-29). Rapid urbanization is generating rising demand for electrical wires across Tier 1 and Tier 2 cities, where new residential and commercial developments require fully wired buildings that comply with BIS safety standards.

Data Centers, Fiber Optic and Communication Cables

India had 770 million 5G subscribers projected by 2028. The BharatNet Phase III project, aimed at deploying 100 GB of broadband to gram panchayats across the country, has begun awarding contracts and will drive substantial optical fibre cable demand. Data center capacity in India is set to nearly double from 1,150 MW in December 2024 to around 2,000 to 2,100 MW by March 2027, driven by AI workloads, cloud services, and enterprise digitization, all of which require specialized communication cables and low loss data cables in large volumes.

Real Estate

India's urban population will reach 600 million by 2031. Real estate demand is translating into sustained housing wire consumption, especially as the market moves toward branded products for safety compliance.

By end user, the power sector remains the dominant buyer, followed by construction, railways, and telecommunications.

Raw Materials: Copper and Aluminium

Copper and aluminium are the two dominant inputs in the cables industry and together account for 55-70% of total material costs, making commodity prices a central variable in margin management.

Copper averaged around USD 9,370 per tonne in FY 2024-25, with LME prices peaking at USD 9,751 per tonne in March 2025. RR Kabel noted that copper fluctuated between USD 8,800 and USD 11,500 per tonne during 2025.

The structural case for higher copper prices remains strong. Its growing role in EVs, semiconductors, renewable energy systems, and data centres continues to drive demand, while supply additions lag. As a result, copper prices are expected to grow at a 3–5% CAGR through FY 2030.

Copper remains the dominant conductor material, accounting for over 64% of the cables market, and its pricing directly shapes the cost structure and margins of every manufacturer in the industry. Domestic capacity for copper refining falls short of demand, making India structurally dependent on imports for this core input.

Aluminium averaged USD 2,526 per tonne in FY 2024-25 and is expected to stabilize around USD 2,200–2,400 per tonne in the medium term. India also runs a domestic copper deficit, meaning imports and global price movements directly influence input costs.

To manage this volatility, most cable companies rely on pass-through pricing in institutional contracts, back-to-back procurement, or backward integration into copper or aluminium rod manufacturing. For instance, Diamond Power Infrastructure (DICABS) operates four in-house rod mills, while Polycab and other players have gradually expanded backward integration.

In FY 2025-26, the Bureau of Indian Standards (BIS) introduced Quality Control Orders (QCOs) on copper wire rods and copper cathodes, adding another layer of supply chain complexity for companies sourcing raw materials from smaller or non-certified vendors.

The Directorate General of Foreign Trade regulates copper and aluminium imports, and any policy shift on duties or licensing directly affects input costs for cable manufacturers.

Current Performance: Nine Months of FY 2025-26

The nine months through December 2025 (9M FY26) have been the strongest in the industry's recent history, driven by a combination of genuine end-demand growth and significant commodity price inflation, particularly copper, which rose around 35% between April and December 2025. Revenue numbers have benefited from both, though the commodity pass-through dynamic has also created some short-term margin pressure at companies managing it in a staggered way.

The following table captures Q3 FY26 (October-December 2025) and 9M FY26 performance for the four largest listed players:

| Company | Q3 FY26 Revenue | Q3 YoY Growth | Q3 EBITDA Margin | 9M FY26 Revenue | 9M YoY Growth |

|---|---|---|---|---|---|

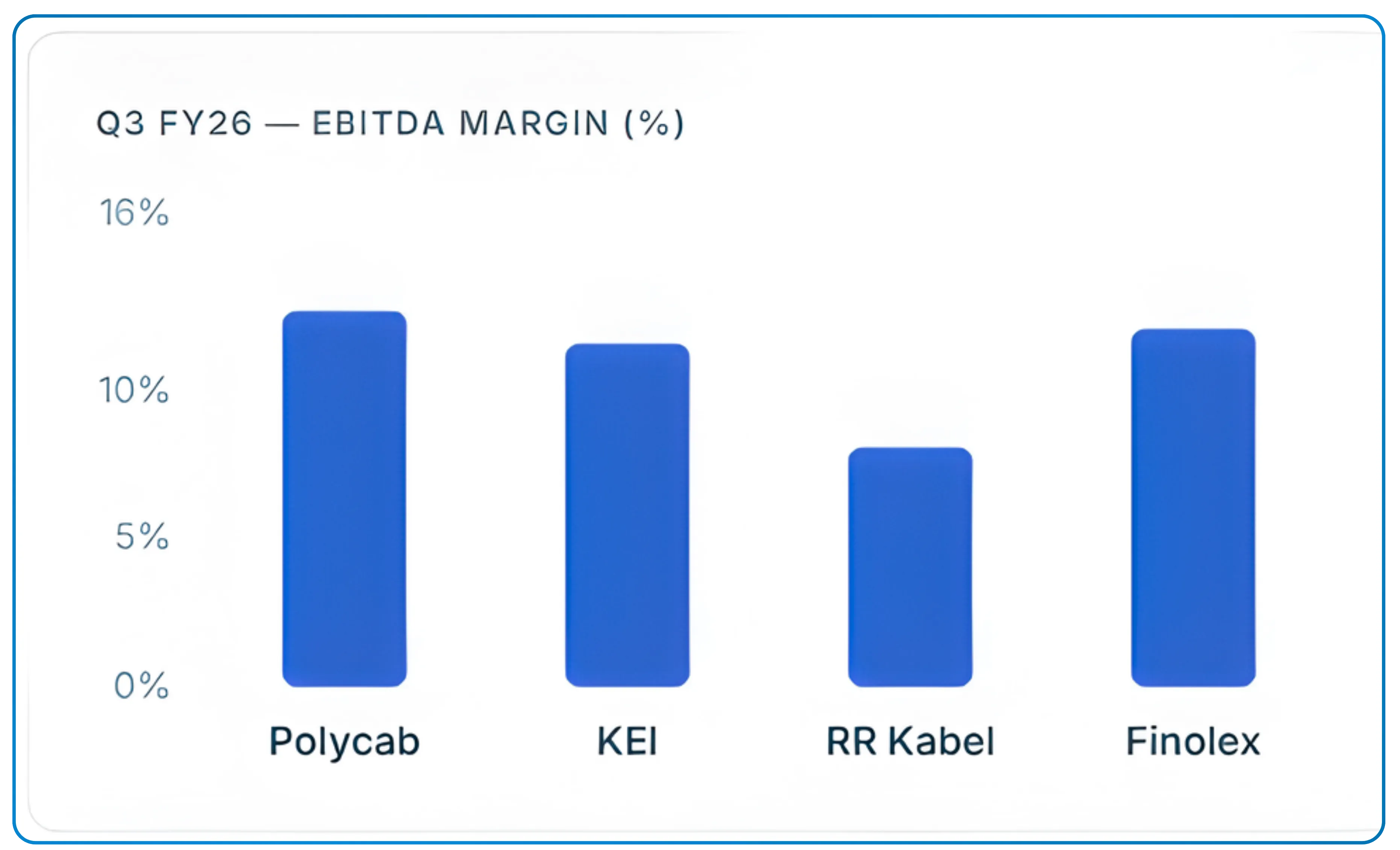

| Polycab India | ₹7,575 crore | 46% | 12.7% | ₹20,000+ crore | 30% |

| KEI Industries | ₹2,955 crore | ~21% | ~11.6% | ₹8,271 crore | 21.3% |

| RR Kabel | ₹2,536 crore | 42.3% | 8.1% | ₹6,758 crore | 25.1% |

| Finolex Cables | ₹1,599 crore | 35% | ~12.1% | ₹4,370 crore | 17% |

Polycab India posted its highest-ever Q3 PAT of ₹630 crore (+36% YoY) with a net cash position of ₹3,030 crore. The wires and cables segment was the engine, domestic W&C revenue grew 59% YoY in Q3, with volume growth of approximately 40%. Both wires and cables delivered similar volume growth, but wires outpaced in revenue terms as channel partners pre-stocked ahead of further price increases, with dealer inventory moving from a typical around 30 days to around 40-45 days by quarter-end. Management was explicit that it made a deliberate strategic choice to pass through copper cost inflation in a staggered manner rather than all at once, accepting near-term margin pressure to protect volumes and channel relationships. Around 75-80% of the approximately 35% copper inflation (vs. April 2025) had been passed through by December, with the remainder expected in Q4. Capacity utilization in W&C was in the early 80% range. On FMEG, solar was the standout category, growing more than 2x YoY. International business grew only 5% YoY, with the US market specifically affected by tariff uncertainty; a headwind also flagged for the coming quarters. The 9M FY26 picture is striking: revenue crossed ₹20,000 crore, EBITDA margin expanded to 14.2%, and PAT grew 47% YoY.

KEI Industries delivered 9M FY26 revenue of ₹8,271 crore, up 21.3% YoY, with EBITDA of ₹963 crore (11.6% margin) and PAT of ₹634 crore (+35% YoY). Exports jumped sharply, accounting for 17% of revenues in 9M FY26, up from 13% in FY25. The company's order book stood at ₹3,724 crore as of December 2025, with healthy representation across LT/HT cables, EHV, and exports. A new greenfield plant in Sanand, Ahmedabad commenced first-phase commercial production in December 2025, adding fresh LT/HT cable capacity. Cable capacity utilization across existing plants was 83% in 9M FY26. The company's credit ratings stand at AA+ (stable) long-term and A1+ short-term, reflecting balance sheet strength following the FY25 QIP. Return on capital employed was 25% in FY25 and is tracking well in FY26.

RR Kabel reported Q3 FY26 revenue of ₹2,536 crore, growing 42.3% YoY its highest-ever nine-month revenue, EBITDA, and PAT. The wires and cables segment drove growth, with segment revenue up 48.6% YoY in Q3. EBITDA grew 86% YoY in Q3, though the starting base was low (Q3 FY25 margin was 6.2%). The 9M FY26 EBITDA margin stood at 7.8%, with Q3 at 8.1%, trending toward the company's stated target of ~10.5% by FY28. FMEG continued to operate at a small loss, though the year-to-date loss has narrowed significantly compared to 9M FY25. Exports were a steady 27% of revenues in both Q3 and 9M FY26.

Finolex Cables grew Q3 FY26 revenue by 35% YoY to ₹1,599 crore, the strongest quarterly performance in recent years. The electrical cables segment led, growing 28% in wires broadly. A key positive was OFC: volumes in optical fibre cables grew 34% YoY in Q3, a meaningful reversal from the FY25 narrative of pricing pressure overwhelming volume growth. The 9M FY26 PAT of ₹462 crore was up 18% YoY. One nuance is that EBITDA fell 23% quarter-on-quarter (from Q2 to Q3) due to a large dividend income booking in Q2 that did not repeat; excluding that, the sequential EBITDA trajectory has been improving. Volume growth in some newer product categories (conduits, switches) was temporarily held back by trade partners managing inventory ahead of the January 2026 BEE energy-efficiency norm changes for fans.

Across the industry, the story of 9M FY26 has been strong top-line momentum built on real demand plus commodity tailwinds, with margin trajectories recovering as companies progressively pass through higher copper and aluminium costs. The Q4 FY26 picture (January-March 2026) should show cleaner margins as pass-through completes and the seasonally strong summer demand season gets underway.

Capacity Expansion and Energy Infrastructure Investment

The industry is in an active investment phase. Companies are collectively spending billions to expand capacity, backward-integrate into raw materials, and enter new product segments. This reflects strong confidence in the medium-term demand outlook but also raises some caution about near-term margin compression and return cycles.

Polycab invested ₹958 crore in property, plant, and equipment in FY25. RR Kabel has committed ₹1,200 crore in capex between FY 2025-26 and FY 2027-28, adding 36,000 MT of cable capacity at Waghodia and 6,000 MT of wire capacity at Silvassa. Finolex has lined up ₹500 crore for FY 2024-26 for an e-Beam facility, EV battery cables, railway instrumentation cables, and an optical fiber preform facility. Paramount allotted 31 acres of land in Narmadapuram, Madhya Pradesh, for a greenfield facility. DICABS is adding 10 new medium voltage cable production lines and setting up dedicated EHV cable production up to 400 kV.

The industry's total capex in FY 2025-26 is expected to exceed ₹8,500 crore. This is a significant number for an organized market currently sized at around ₹92,000 crore, and indicates a degree of capacity-ahead-of-demand positioning that is justified by the long lead times of infrastructure projects.

Exports: The Opportunity Ahead

Exports remain small but are increasingly strategic for most players. Polycab's exports were ₹1,345 crore (6% of revenue) in FY25 but were impacted by Red Sea disruptions and a deliberate transition in its US business model. KEI targets export growth in Australia, the USA, and Europe. RR Kabel aims to grow its export business 1.8x, targeting markets benefiting from global supply chain shifts. Paramount's export order book stood at ₹323 crore, nearly 50% of its total order book, a notable shift for a mid-sized player. DICABS is pursuing GCC, Africa, and Southeast Asia markets and expects exports to grow at 40-50% CAGR over three years.

The global China+1 supply chain realignment is a genuine opportunity. European and North American utilities and EPC companies are increasingly looking at India as an alternative supply source for cables and conductors, particularly as Chinese manufacturers face tariffs, restrictions, and supply chain scrutiny in Western markets. India's cost advantage, combined with improving quality certifications (BASEC-UK, UL-US, GMark-Gulf), is beginning to open doors that were previously closed.

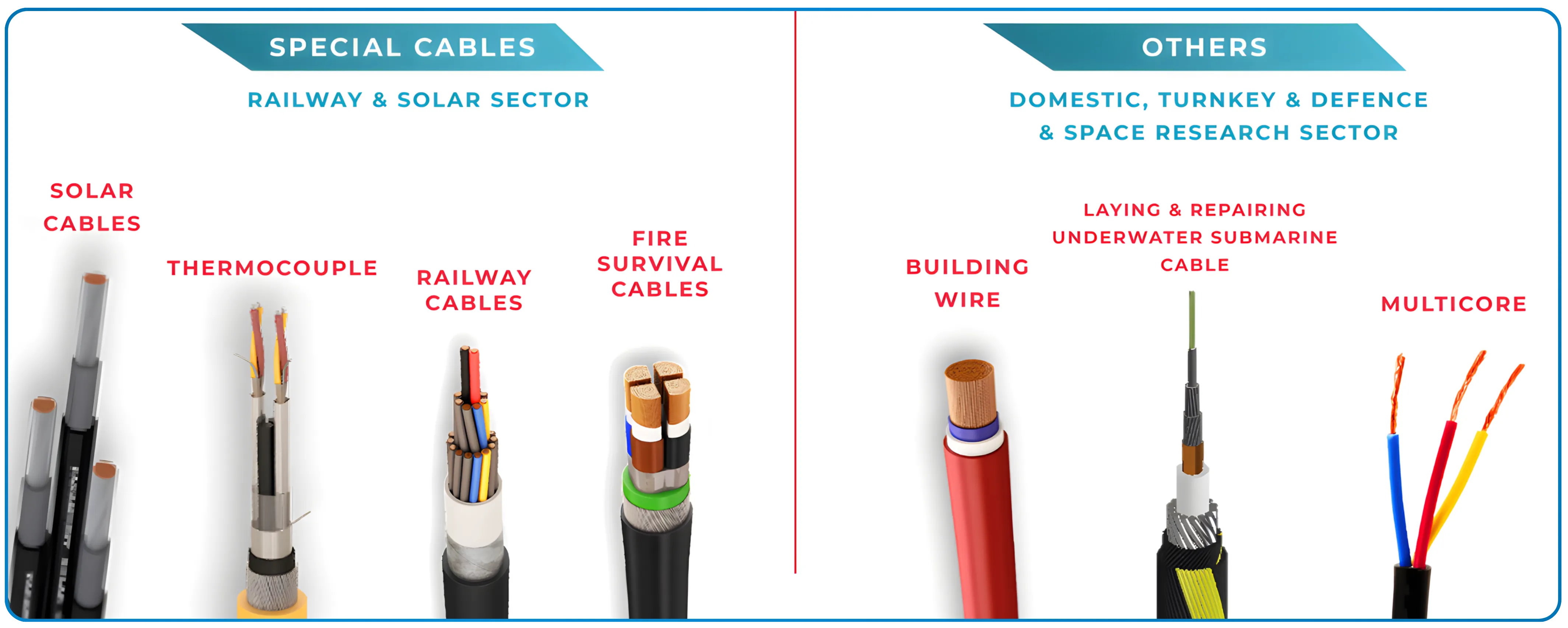

Extra High Voltage, EV, Consumer Electronics and Specialty Cables: New Product Frontiers

Companies are expanding into product categories that did not exist in cable manufacturer portfolios five years ago. Several themes are consistent across the industry: EPC projects for power transmission and urban infrastructure are among the largest end markets for institutional cable suppliers. Consumer electronics and home appliances are adding to the downstream pull for flexible and specialty wiring.

EV charging cables are in early-stage development and production across companies including Finolex, DICABS (Type 2 and CCS2 compliant variants), and others. Battery Energy Storage System (BESS) cables, which must withstand thermal and vibration stress in grid-scale storage projects, are another frontier. Solar DC and AC cables with UV resistance are a natural extension for companies already supplying power cables. Fire survival and halogen-free cables for tunnels, airports, metros, and defense applications are a growing specialty segment. There is also a structural shift in the industry toward Low Smoke Zero Halogen cables and fire retardant wires, particularly for use in tunnels, airports, metro stations, and defense facilities, where safety compliance is non-negotiable. Optical fiber preform manufacturing (typically imported) is an area Finolex is investing in to reduce dependency. Both 5G and anticipated 6G rollouts will sustain OFC demand, even as near-term pricing has been suppressed by oversupply. The trend toward hybrid cables, which combine power cables, data cables, and sometimes pneumatic hoses within a single sheath, is gaining ground in industrial automation and EPC projects requiring integrated solutions.

Distribution and Retail Networks

Retail distribution depth is a major competitive differentiator. Finolex operates with over 600 distributors, 5,000 channel partners, and more than 2,15,000 retailers. It is targeting 2,50,000 retail touchpoints with a focus on Tier 2 and Tier 3 cities. Polycab's distribution network spans tens of thousands of outlets across India. KEI's retail segment grew to 52% of revenues in FY25, a key indicator that its brand-building investments are converting institutional credibility into retail pull. DICABS is targeting appointments in all 28 states and UTs by FY 2025-26, supported by regional warehouses and logistics hubs promising 72-hour delivery to Tier 1 and Tier 2 industrial clusters. Distribution reach in East India remains underpenetrated compared to the west and south, and companies expanding into this region stand to gain incremental volume.

Also Read: Retail reach and channel strategy can make or break an industrial business. Vaibhav Global's niche retail playbook offers a different lens to think about scale.

Competitive Analysis: Key Players in the Indian Cables Industry

The key players in the Indian cables industry operate across three distinct tiers.

Tier 1: Large, Diversified National Players

Polycab India holds an estimated 26-27% share of the organized market. It is the only company that combines large-scale wires and cables manufacturing with a meaningful FMEG business and EPC project execution capability. Its backward integration, manufacturing scale across multiple plants, and the widest distribution network in the sector make it the benchmark. The fast moving electrical goods segment, which includes fans, switches, and lighting, is a growing revenue diversifier for cable companies like Polycab and RR Kabel.

KEI Industries is the second-largest pure-play cables company. Its EHV cable capability, strong institutional relationships, and a quickly growing retail presence differentiate it. With a debt-equity ratio of just 0.03 following a recent QIP fundraise, it has the balance sheet flexibility to invest aggressively.

Finolex Cables is the established market leader in building wires and a trusted brand, but its growth has been moderate. It has the deepest retail penetration in the industry and is diversifying into specialty products. Its balance sheet is conservatively managed with strong cash generation.

RR Kabel is a relatively recent listing but a serious player, with 88% of revenues from wires and cables and an active strategy to scale FMEG and exports. Its ₹1,200 crore capex commitment and double-digit EBITDA margin target by FY28 reflect an ambitious growth trajectory.

Apar Industries, primarily a conductor and specialty oil company, also competes in the cables adjacency space and benefits from the same demand cycle.

High voltage cables for transmission infrastructure are among the highest-margin and most technically demanding products in the portfolio.

Tier 2: Specialized Mid-Caps

Paramount Communications (around ₹1,587 crore consolidated revenue) focuses on defence, telecom, and power cable applications and is among the very few Indian companies producing undersea cable systems. Exports make up nearly half its order book. Diamond Power Infrastructure (around ₹1,115 crore revenue) operates as India's largest single-location producer of power cables and conductors under Adani Group ownership. Its rapid revenue ramp has been partly driven by intra-group orders, but its product portfolio expansion and R&D investments suggest a genuine long-term build. Cords Cable Industries is a specialty player serving industrial automation, hydrocarbons, railways, and defense segments; sectors that require complex, certified cable products with strong margins but have slower buying cycles. Universal Cables, part of the BK Birla group, is another mid-tier player with a long history in power cables serving utility and industrial segments.

Tier 3: Smaller and Focused Players

Precision Wires India is a niche manufacturer of copper winding wires for rotating electrical equipment motors, transformers, and appliances. It doesn't compete in the commodity cable space but benefits from the same downstream demand drivers. Plaza Wires is a small-cap in house wires and fans with a regional focus. Despite revenue growth of ~9.7%, its PAT declined 21.6% in FY25 due to margin compression, reflecting the profitability pressure on smaller players when raw material costs rise without adequate pricing power.

Birla Cable, a specialist in optical fibre and structured LAN cables, saw revenue decline in FY25 as the OFC segment hit a pricing floor. It is a strong recovery candidate if and when fibre cable pricing normalizes.

A competitive analysis of the organized segment reveals a clear three-tier structure

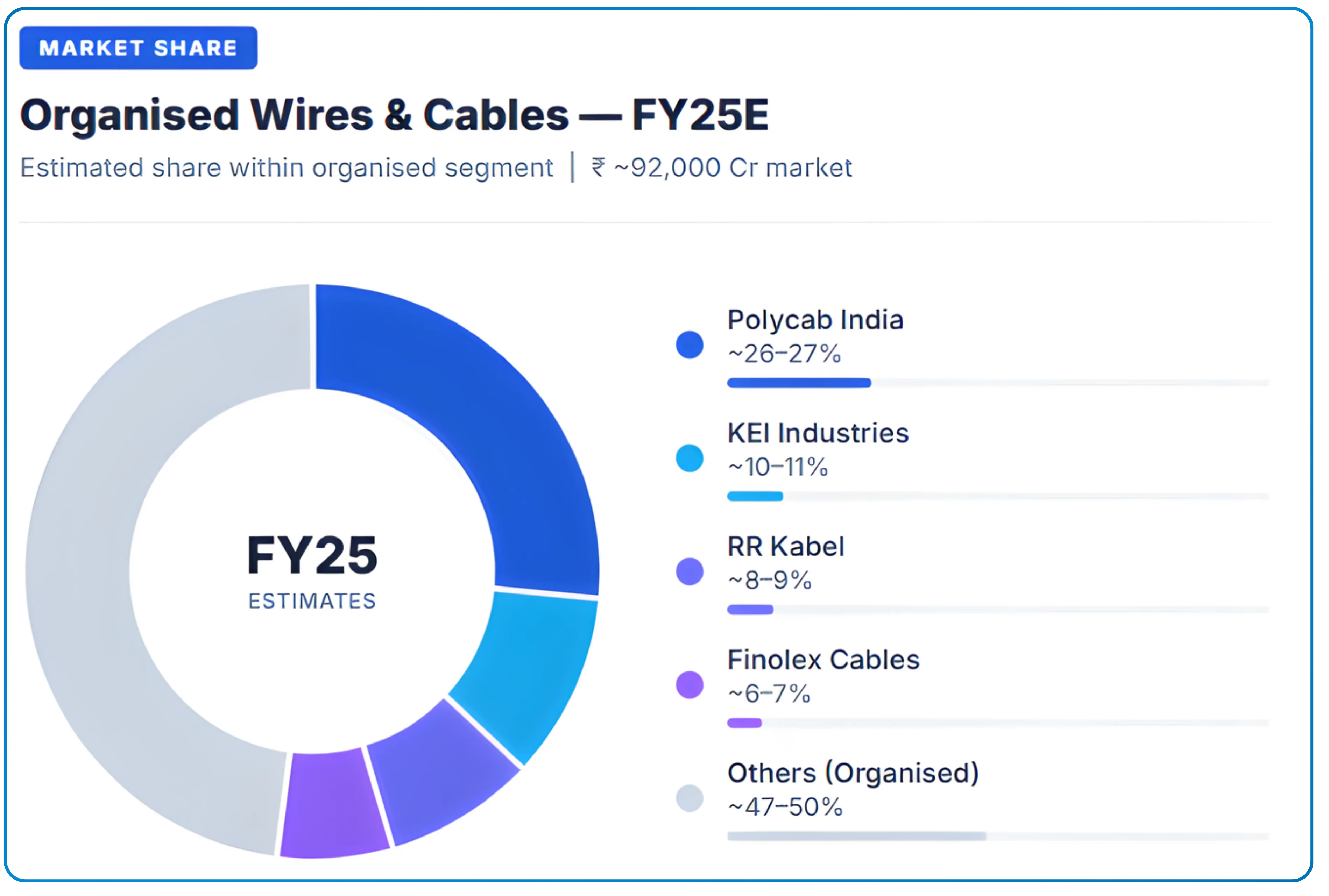

Market Share Summary (Organized Segment, FY25 Estimates)

| Company | Est. Market Share (Organized) |

|---|---|

| Polycab India | ~26–27% |

| KEI Industries | ~10–11% |

| RR Kabel | ~8–9% |

| Finolex Cables | ~6–7% |

| Others (organized) | ~47–50% |

Havells India Ltd holds a 15 to 17% share of the broader wires and cables market, primarily driven by its strong consumer brand presence in housing wires.

End User Breakdown: High Voltage, Low Voltage and Who Is Buying

The end user base for cables in India spans power utilities buying high voltage and extra high voltage cables for transmission, construction companies purchasing low voltage cables for residential and commercial projects, railways and defense buying specialty certified cables, and consumer electronics and appliance manufacturers sourcing flexible wiring. No single end user dominates, which is precisely what makes this industry resilient across economic cycles

Key Risks

Raw material price volatility is the most immediate and persistent risk. Copper and aluminium prices can move sharply and quickly. Companies that cannot pass through price increases, particularly smaller players or those with fixed-price project contracts, face direct margin impact.

Competition from the unorganized sector remains a factor in the building wires segment, where price is often the deciding consideration among electricians in smaller towns. The rollout of BIS QCOs partially addresses this but enforcement is uneven.

Geopolitical risks include the impact of Red Sea shipping disruptions on export logistics, potential US tariff changes that could alter global trade flows, and the India-Pakistan situation. US tariffs on Chinese goods could benefit Indian exporters in the short term but could also suppress global demand broadly if they trigger a trade slowdown.

Project execution and counterparty risk apply to companies with large institutional order books. Government scheme implementation delays (RDSS rollout has been slower than originally planned), land acquisition delays, and state utility payment cycles create timing and cash flow risks.

Overcapacity risk exists at an industry level if the current wave of capex across all players creates excess supply before demand absorbs it. In commodity-ish product segments like housing wires, this could compress margins across the industry. The higher-specification segments (EHV, OFC, specialty cables) are more insulated.

OFC pricing weakness is a near-term structural headwind. Global optical fibre cable production capacity, much of it Chinese has expanded rapidly, and pricing has been very weak. Companies with significant OFC revenue (Birla Cable, Finolex) felt this in FY25 and the near-term may not materially improve.

Keeping pace with technological advancements in insulation materials, conductor design, and fire safety standards is increasingly a competitive necessity for manufacturers aiming to serve premium segments.

Cables Market Size, Key Trends and the Road Ahead

The medium-term demand environment for the cables industry is among the strongest of any industrial sector in India. The alignment of government infrastructure spending, the energy transition, digitization, and real estate activity creates a durable, multi-year demand backdrop. The organized market is expected to grow revenues 15-16% in FY 2025-26, and incremental demand of around ₹20,000 crore in the organized segment is forecast for that year alone. Government initiatives like Make in India and the Production Linked Incentive scheme are reinforcing this trajectory by encouraging manufacturers to expand domestic capacity, invest in R and D, and reduce import dependency across the cables industry. Cables are a foundational input across core industries including power, construction, railways, and telecommunications, which is why demand for this sector tracks so closely with overall economic activity.

The sector competes for raw materials with global demand, which means input cost management and backward integration will increasingly separate the companies that earn sustainable margins from those that do not. Export growth (particularly in higher-specification cable categories where Indian companies are building international certifications) is a meaningful medium-term opportunity that could improve the revenue quality and diversity of the larger players.

The structural shift from unorganized to organized manufacturing still has a runway. As real estate, utilities, and infrastructure projects tighten quality specifications and compliance requirements, demand will increasingly concentrate among manufacturers with certified products, adequate capacity, and reliable delivery. The companies that have invested ahead of this cycle (in capacity, certifications, distribution depth, and product range) are well positioned to benefit.

Indian manufacturers are projected to grow exports by 20 to 22% in FY26, as global buyers diversify supply chains toward India, a trend that could meaningfully improve revenue quality and geographic diversity for the leading Indian manufacturers. Investment in energy infrastructure across generation, transmission, and distribution is the single largest structural driver for the cables sector. The cables industry has recorded strong growth across all major categories, with significant growth expected to continue through FY29 as infrastructure and energy investments scale up.

Turn research into action, trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.