India’s skies are busy again. After the pandemic hit in FY21, air travel in India bounced back strongly by FY25, driven by affordable fares, a growing middle class, and better connectivity across the country. Airlines are adding planes, airports are expanding, and more people are choosing to fly– both within India and overseas. The main reason for this is simple: flying is becoming the easiest way to connect India’s big and small cities, and that demand is here to stay.

KEY NUMBERS AT A GLANCE (FY19–FY25)

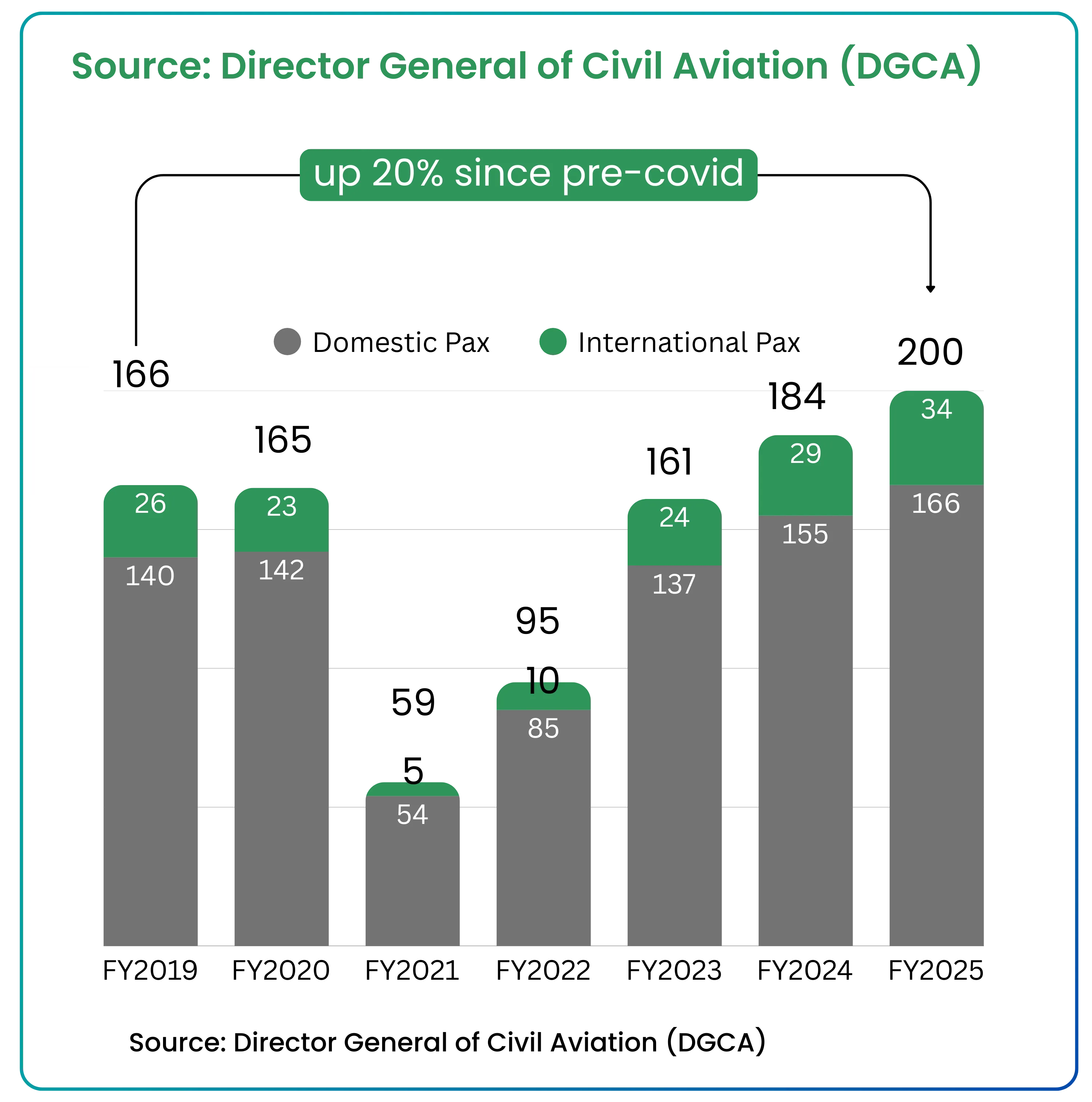

The Indian aviation sector has staged a remarkable comeback, surging 20% past pre-COVID levels to hit a landmark 200 million total passengers in FY2025. The data reveals a sharp V-shaped recovery from the pandemic lows of FY2021, driven heavily by domestic demand which climbed to 166 million. International traffic has also seen healthy growth, expanding to 34 million. This trajectory underscores the resilience of the Indian market and a booming appetite for travel as connectivity improves across the board.

"Passenger Traffic Growth (2023-2043E)", illustrates the projected growth rates for various regions globally, highlighting India as having the highest projected growth at +6.4%. The map details growth forecasts for areas like China (+5.3%), the United States (+3.1%), and Vietnam (+6.5%), and it also emphasizes that the subject market (implied to be India or the broader region) is the "3rd largest aviation market" in the world.

India’s aviation market is projected to grow from USD 14.78 billion in 2025 to USD 26.08 billion in 2030, implying a 12% CAGR for FY25-FY30. This supports the view that the industry’s FY21-FY25 rise was a powerful rebound followed by steady, sustainable growth.

Also Read: https://www.tradejini.com/blogs/the-business-of-fun-an-industry-report

AIRLINES MARKET SHARE IN INDIA

| Airline | Domestic Market Share | Total Aircraft |

|---|---|---|

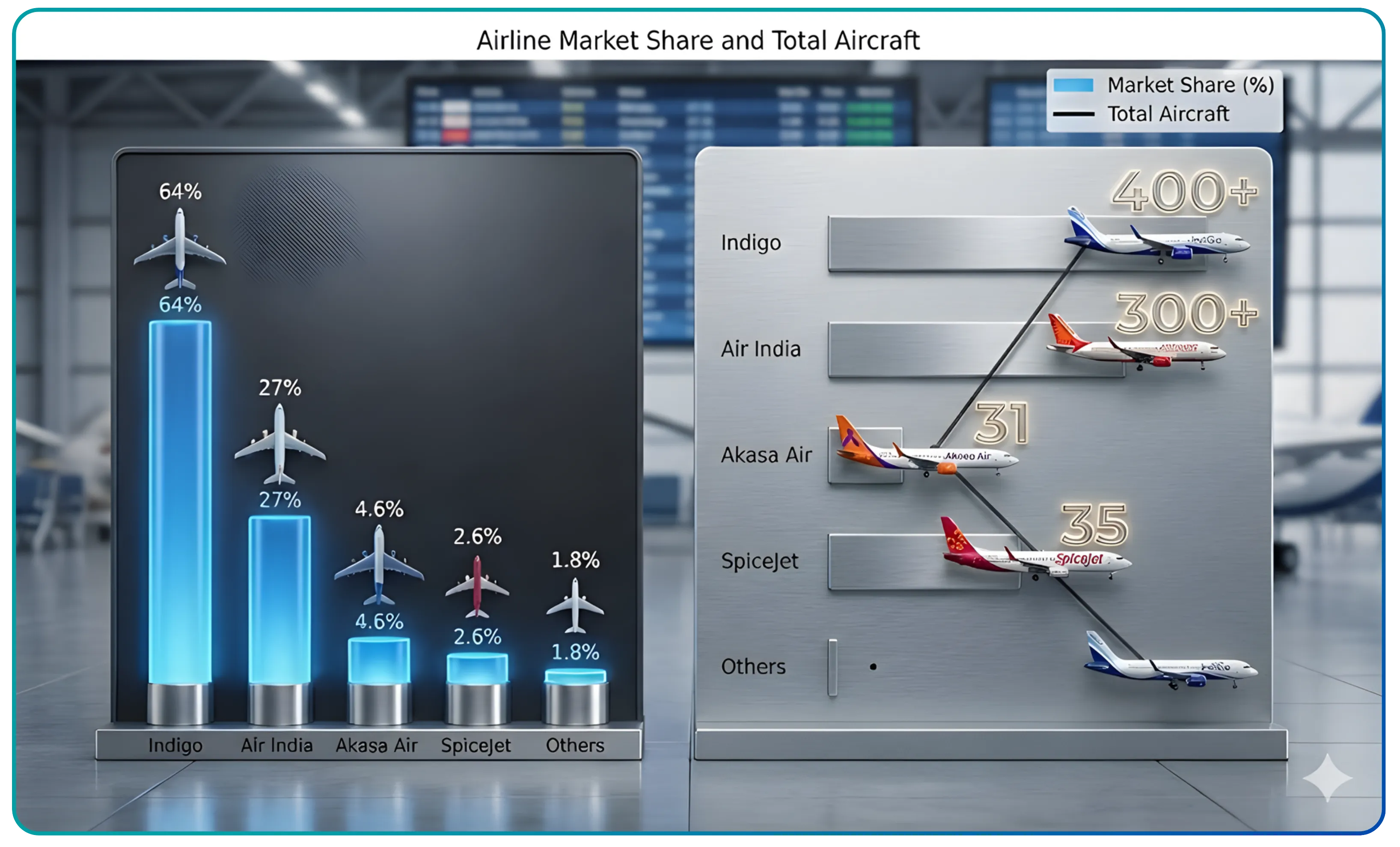

| IndiGo | 64% | 419 |

| Air India (Combined: Air India Express & Vistara) | 27% | 300 |

| Akasa Air | 4.6% | 31 |

| SpiceJet | 2.6% | 35 |

| Others | 1.8% | — |

Current Domestic Market Share: Key Airlines in India

Market share data is based on domestic passengers carried within India in 2024 and early 2025, using Directorate General of Civil Aviation (DGCA) statistics and industry estimates. The concentration level in india’s aviation sector reveals a highly consolidated market structure dominated by a few major players.

IndiGo maintains its position as the largest airline in India with approximately 60% domestic market share in Q1 2025. The carrier’s dominance stems from its extensive route network covering over 80 domestic destinations, superior on-time performance consistently above 85%, and high aircraft utilization rates that enable competitive pricing while maintaining profitability.

Air India Group: Commanding a combined domestic market share of 28–31%, the unified group integrates the full-service strengths of Air India and Vistara with the low-cost efficiency of Air India Express (including AIX Connect). Backed by Tata Group's fleet renewal and investment, the entity now serves a diverse spectrum of travelers—from premium business and long-haul international passengers to price-sensitive leisure segments- while leveraging regional routes to feed its expansive global network.

Akasa Air has rapidly grown to 5-6% domestic market share as a new entrant since 2022, demonstrating that market disruption remains possible despite high concentration. The airline’s modern fleet, competitive pricing, and focus on operational reliability have enabled quick market penetration.

SpiceJet holds 4-5% domestic market share but faces financial stress and network shrinkage that limits its competitive position. The carrier’s reduced operational scale constrains its ability to compete effectively on major routes against better-capitalized rivals.

Smaller regional airlines including Alliance Air, Star Air, and flybig collectively hold less than 2-3% of domestic traffic but serve crucial roles in connecting tier-2 and tier-3 cities under the UDAN (Regional Connectivity Scheme).

| Airline Type | Market Share | Key Characteristics |

|---|---|---|

| Low-Cost Carriers | ~75% | Price-focused, high density seating |

| Full-Service Carriers | ~22% | Premium service, multiple cabin classes |

| Regional Carriers | ~3% | UDAN routes, government support |

The dominance of low-cost carriers over full-service carriers in the domestic market reflects Indian consumers’ high price sensitivity and preference for basic air transport services over premium amenities.

Growth Drivers

Demand tailwinds: Rising incomes, business travel beyond metros, and leisure flyers choosing planes over long train journeys.

Policy push: Airport expansion and MRO incentives, plus regional connectivity schemes that bring first-time flyers into the market.

Supply build-out: Big fleet orders, better maintenance ecosystems, and improved airport capacity support steady growth in seats and routes.

Interesting facts….Many of the fastest-growing routes are not between metros; they connect smaller cities directly, cutting travel times dramatically.

Value takeoff:

The aviation market is on track for 12% CAGR from 2025 to 2030 – steady growth after a sharp post - pandemic rebound

The aviation market is on track for 12% CAGR from 2025 to 2030 – steady growth after a sharp post - pandemic rebound

International Market Share: Indian vs Foreign Airlines

International market share is measured by passengers carried to and from India in 2023-2024, encompassing both Indian and foreign carriers operating on international routes. The competitive dynamics differ significantly from the domestic market due to bilateral agreements, hub strategies, and varying cost structures.

Air India leads among Indian carriers on international routes with approximately 23-25% share of international traffic carried by Indian airlines in 2024. The carrier focuses on North America, Europe, and Middle East destinations, leveraging its wide-body fleet and Delhi hub for long-haul operations. Recent fleet additions and route expansions have strengthened its position on premium international corridors.

IndiGo ranks as the second-largest Indian airline by international passengers, with rapidly growing share on short-haul routes to Gulf countries, southeast asia, and neighboring SAARC nations. The carrier’s narrow-body fleet and point-to-point model excel in high-frequency, price-sensitive international markets within six hours flying time from India.

Foreign airlines collectively carry the majority of international passengers to and from India, particularly through their hub operations. Emirates maintains among the strongest positions of foreign carriers, with significant presence in major airports including Mumbai, Delhi, and Bengaluru. Qatar Airways, Singapore Airlines, and Etihad also command substantial market shares through their respective hub strategies.

Gulf carriers dominate leisure and VFR (visiting friends and relatives) traffic, connecting Indian cities to destinations worldwide through Dubai, Doha, and Abu Dhabi hubs. Their extensive networks and competitive pricing appeal to price-conscious travelers, while their connecting flights serve markets that Indian carriers cannot reach directly.

| Market Segment | Indian Carriers | Foreign Carriers |

|---|---|---|

| Total International Traffic | ~35–40% | ~60–65% |

| Gulf Routes | ~25% | ~75% |

| Europe/US Routes | ~45% | ~55% |

| Southeast Asia | ~50% | ~50% |

Bilateral agreements between India and foreign countries, hub-and-spoke strategies of Gulf carriers, and slot constraints at European hubs like London, Heathrow, and Frankfurt significantly influence market share distribution. Indian airlines face challenges competing with foreign carriers’ established route networks and lower operational costs at their home bases.

AlsoRead:https://www.tradejini.com/blogs/how-varun-beverages-is-responding-to-campa-colas-comeback

Historical Evolution of Aviation Market Share in India

The transformation of India's aviation market from a protected, state-dominated industry to today’s competitive landscape reflects decades of policy evolution and market forces. Understanding this historical context explains current market share patterns and competitive positioning.

Pre-liberalization era (1953-1991) saw state-run Indian Airlines and Air India enjoying protected monopolies under the Air Corporations Act of 1953, which nationalized civil aviation and restricted private operators. During this period, market share was administratively determined rather than competitively earned, with limited passenger volumes and high fares constraining market development.

Early liberalization (1991-2003) introduced private carriers like East-West Airlines, ModiLuft, and later Jet Airways, gradually opening competition in domestic markets. Jet Airways emerged as the leading private carrier, eventually capturing approximately 35% market share at its peak in the mid-2000s, challenging state-run airlines through superior service and modern aircraft.

Low-cost carrier revolution (2003-2015) fundamentally reshaped market dynamics as Air Deccan, IndiGo (launched 2006), SpiceJet, and GoAir introduced no-frills models that dramatically reduced fares and expanded market access. LCCs gradually captured majority domestic market share by offering reliable, affordable air travel to price-sensitive passengers previously dependent on rail transportation.

Consolidation phase (2012-2025) witnessed the collapse or grounding of several major carriers, redistributing market share among surviving airlines. Kingfisher Airlines ceased operations in 2012, Jet Airways suspended operations in 2019 after financial difficulties, and Go First was grounded in 2023, each event concentrating more traffic among remaining carriers, particularly IndiGo and the Air India Group.

Market structure evolution from the fragmented 2010s to today’s consolidated landscape reflects both natural market forces and specific events. By 2024-2025, the market is dominated by 3-4 major groups controlling nearly all domestic traffic, representing a significant shift from the more diverse competitive environment of the previous decade.

| Period | Key Event | Market Impact |

|---|---|---|

| 1991 | Liberalization begins | Private carriers enter market |

| 2003 | Air Deccan launches LCC model | Fare democratization accelerates |

| 2012 | Kingfisher collapse | Market share redistributed |

| 2019 | Jet Airways suspension | IndiGo dominance strengthens |

| 2023 | Go First grounding | Further consolidation |

| 2024–2025 | Tata consolidation | Air India Group strengthens |

This evolutionary pattern demonstrates how regulatory changes, business model innovations, and financial sustainability determine market share distribution in india’s aviation sector.

Drivers Shaping Market Share: Policy, Pricing, and Connectivity

Market share in India is fundamentally influenced by government policy frameworks, cost structures, regional connectivity objectives, and consumers’ extreme price sensitivity. Understanding these drivers explains why certain carriers succeed while others struggle in this competitive environment.

Policy Framework and Regulatory Environment General of civil aviation

The National Civil Aviation Policy 2016 (NCAP 2016) and subsequent updates have encouraged regional connectivity while supporting the growth of low-cost models through flexible regulations. The policy’s 5/20 rule modifications allowed domestic carriers to start international operations with smaller domestic networks, enabling rapid expansion by efficient operators like IndiGo.

UDAN (Ude Desh ka Aam Naagrik) has created opportunities for smaller and mid-sized carriers to gain market share on tier-2 and tier-3 routes through subsidized operations. Alliance Air, Star Air, and Flybig have utilized these schemes to establish presence in underserved markets, though their combined market share remains limited due to route economics and operational challenges.

Cost Structure and Pricing Power

The importance of low fares, ancillary revenue optimization, and high aircraft utilization cannot be overstated in determining competitive success. IndiGo and Akasa Air have captured large market shares by maintaining superior operational efficiency that enables sustainable low-fare strategies while preserving profitability margins.

Airlines with higher cost structures, including legacy full-service carriers, face pressure to match LCC pricing on overlapping routes, often resulting in yield compression that impacts their financial sustainability and ability to invest in market share growth.

Infrastructure Constraints and Slot Allocation

Airport infrastructure limitations at congested metro airports like Delhi and Mumbai create barriers to rapid market share expansion, as slot availability constrains airlines’ ability to add frequency on high-demand routes. Incumbent carriers with established slot portfolios maintain competitive advantages that new entrants find difficult to overcome.

The development of new airports including navi mumbai international airport and expansion of existing major airports will eventually provide more opportunities for market share redistribution, though slot allocation policies and pricing will determine which carriers benefit most from increased capacity.

Digital innovations including DigiYatra, online travel agency platforms, and sophisticated revenue management systems have democratized access to demand forecasting and dynamic pricing, enabling smaller carriers to compete more effectively against established players in yield optimization and market responsiveness.

Also Read: https://www.tradejini.com/blogs/the-next-tata-generation

Conclusion: India's Consolidated and Growing Aviation Market

India's aviation market is defined by a powerful post-pandemic rebound and a highly consolidated structure, with the domestic segment dominated by low-cost carriers (LCCs). IndiGo remains the overwhelming leader, capitalizing on superior efficiency and high price sensitivity among domestic passengers. The major transformative force is the Air India Group (including Vistara and Air India Express), which is leveraging massive fleet orders to mount a serious challenge, especially in the long-haul international sector. With passenger traffic projected to hit 350-400 million by FY30 and sustained growth fueled by policy, connectivity (UDAN), and rising incomes, the industry's future will be shaped by the intensifying competition between these two giants, while new entrants like Akasa Air drive efficiency and disruption.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.