The Indian amusement park and theme park industry is a growing part of the entertainment sector, shaped by rising incomes and changing consumer preferences. This report examines the industry’s market fundamentals, key growth drivers, and challenges, featuring insights from leading players such as Wonderla Holidays Limited and Imagicaaworld Entertainment Limited. The sector has become an important part of India’s entertainment market, adapting steadily to shifts in demand and operating conditions.

Industry Overview and Market Size

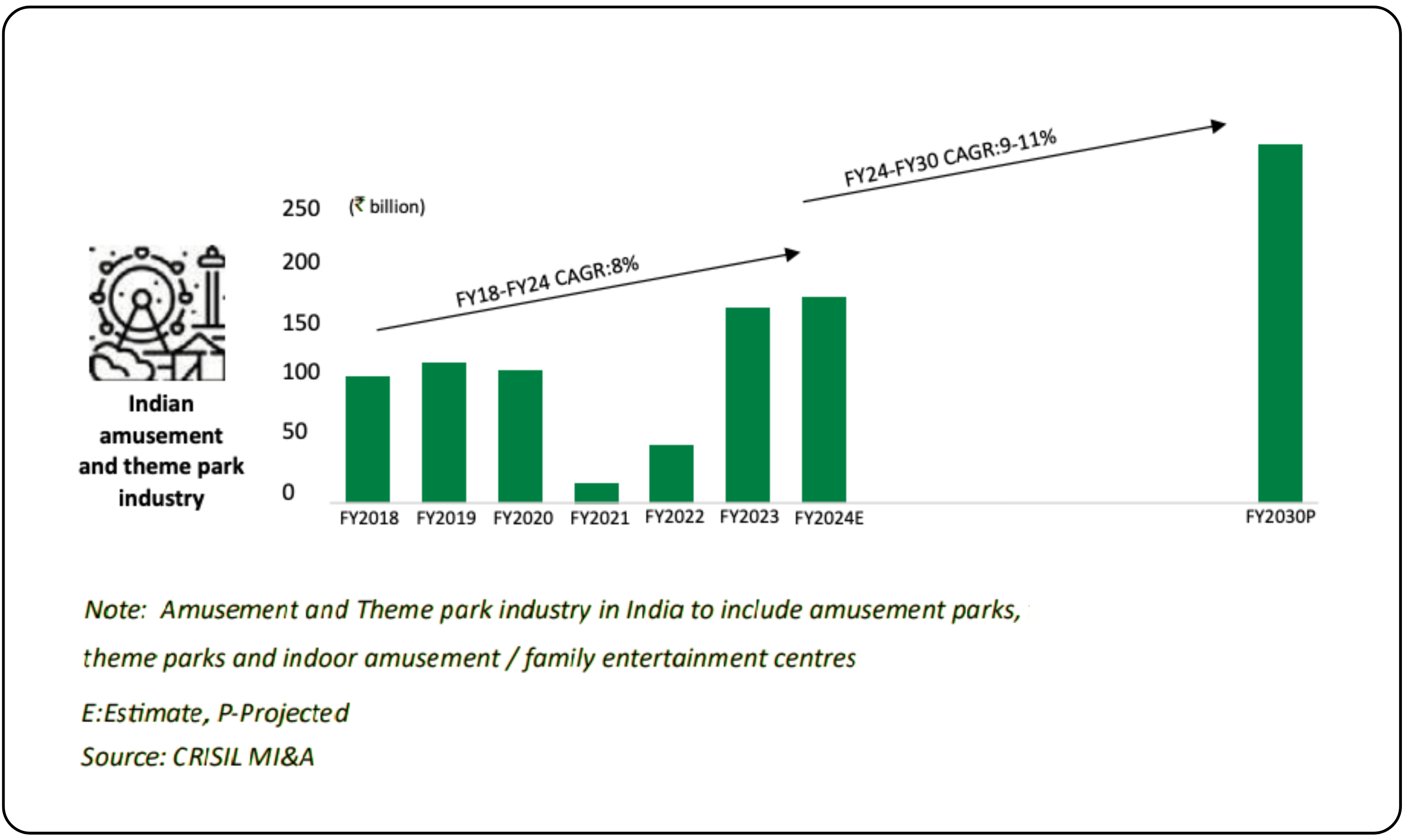

The Indian amusement and theme park industry has demonstrated remarkable resilience and growth potential across multiple economic cycles. In FY2024, the sector was valued at ₹10,800-11,400 crore and is projected to grow at a 9-11% CAGR through FY2030. This marks an acceleration from the 8% CAGR recorded between FY2018-FY2024, positioning the amusement park CAGR 2030 projections as highly attractive for investors.

The Indian amusement and theme park industry includes an estimated 240 to 250 parks and 1,800 to 2,000 indoor entertainment centers spread across India’s diverse geographic landscape. The market structure reveals a well-segmented approach with large parks comprising 14 to 16 facilities, requiring capital expenditure exceeding ₹4,000 million. Medium-sized parks encompassing 60 to 70 facilities involve investments between ₹1,000 million and ₹4,000 million. Meanwhile, small parks totaling 140 to 160 facilities, each requiring less than ₹1,000 million in capital expenditure.

The sector experienced a significant contraction during the COVID-19 pandemic, shrinking from ₹2,500 crore in 2019 to ₹400 crore in 2020. However, the recovery has been steady, with the market reaching ₹5,400 crore in 2023 and is projected to grow to ₹12,500 crore by 2030 at a 15% CAGR from 2023. This recovery highlights the sector’s resilience and strong demand for leisure experiences.

Economic Fundamentals

The industry’s performance is closely correlated with India’s macroeconomic conditions and demonstrates strong sensitivity to broader economic trends. With the Indian economy projected to grow at 6.4% to 6.5% in FY25, rising disposable incomes and favorable demographic advantages provide strong foundational support for sustained sector growth. As India continues its shift toward a consumption-driven economy, the link between economic growth and entertainment spending has become increasingly apparent.

Per capita income grew at 4.2% CAGR (FY2012-FY2023), while discretionary spending nearly doubled, rising at 7% CAGR. This sustained growth in disposable income has fundamentally altered consumer spending patterns, with entertainment and leisure activities becoming a more prominent part of household budgets.

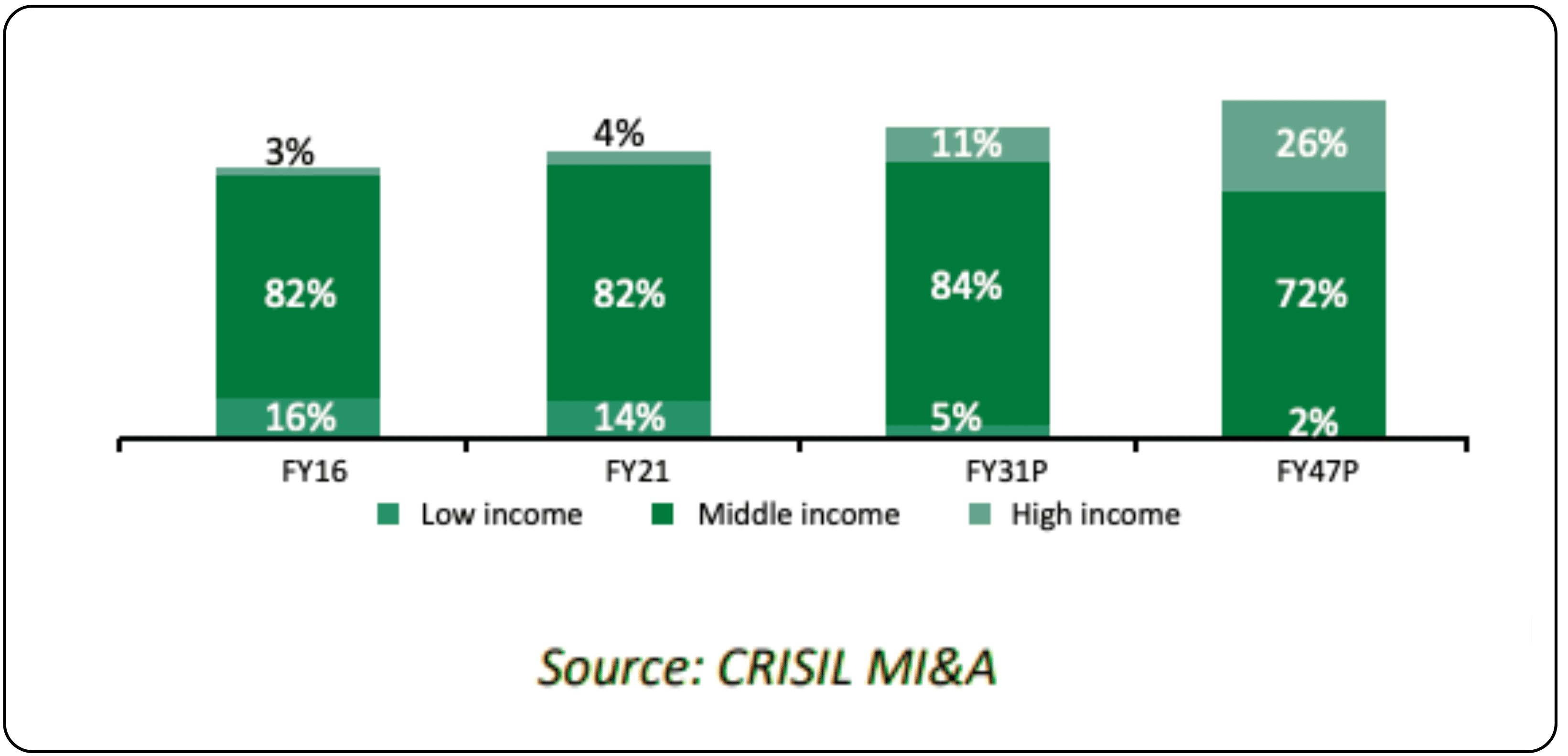

The expansion of India's middle- and high-income segments reflects the demographic drivers fueling experiential consumption, which the amusement park sector relies on. These segments are expected to grow from 86% of the population in FY2021 to 95% by FY2031. This demographic evolution is creating a large and expanding addressable market for premium entertainment experiences. Alongside this, shifting lifestyle preferences are driving a move toward experiential consumption, with consumers increasingly valuing experiences over traditional material goods.

Geographic concentration remains strategically significant with major parks positioned near economic hubs, including Mumbai, Bengaluru, Hyderabad, Delhi, Chennai, and Kolkata, where disposable incomes and urban lifestyle preferences drive consistent and reliable demand patterns throughout the year.

Demand Drivers Analysis

Primary customer demographics: The industry primarily serves families with children under 15 years of age, effectively leveraging India’s favorable demographic profile. Notably, 55% of the population falls into the economically productive 15-60 age group. With a median age of 27 years, India enjoys a demographic advantage over many other major economies worldwide, suggesting sustained demand for family-oriented entertainment options.

Key demand catalysts: Several interrelated factors are driving the growth of the amusement and theme park industry. Urbanization trends indicate a significant shift in India’s population distribution. The urban population share increased substantially from 28% in 2000 to 35% in 2020, and is projected to reach 41% by 2030. This urbanization process is accompanied by lifestyle changes that favor organized entertainment options over traditional forms of leisure.

At the same time, rising discretionary spending patterns indicate that the upper-middle household segment is expected to increase dramatically from 21% in 2018 to 44% by 2030. This segment demonstrates a higher propensity for experiential spending and is more likely to make repeat visits to entertainment destinations, making it a valuable driver of sustained demand.

Another significant growth catalyst is domestic tourism. Domestic Tourist Visits grew at 8.3% CAGR from 2012 to 2023 and are projected to continue at 8% to 10% CAGR through 2030. This tourism growth seen in India creates spillover effects that benefit amusement parks located in popular tourist destinations.

Seasonal patterns: The industry exhibits pronounced seasonality with higher attendance during school vacations, public holidays, and summer months, especially for water parks. In contrast, the monsoon periods typically see reduced footfalls. To manage these fluctuations, operators are adopting dynamic pricing strategies and seasonal programming to optimize revenue across different periods of the year.

Supply Side and Market Structure

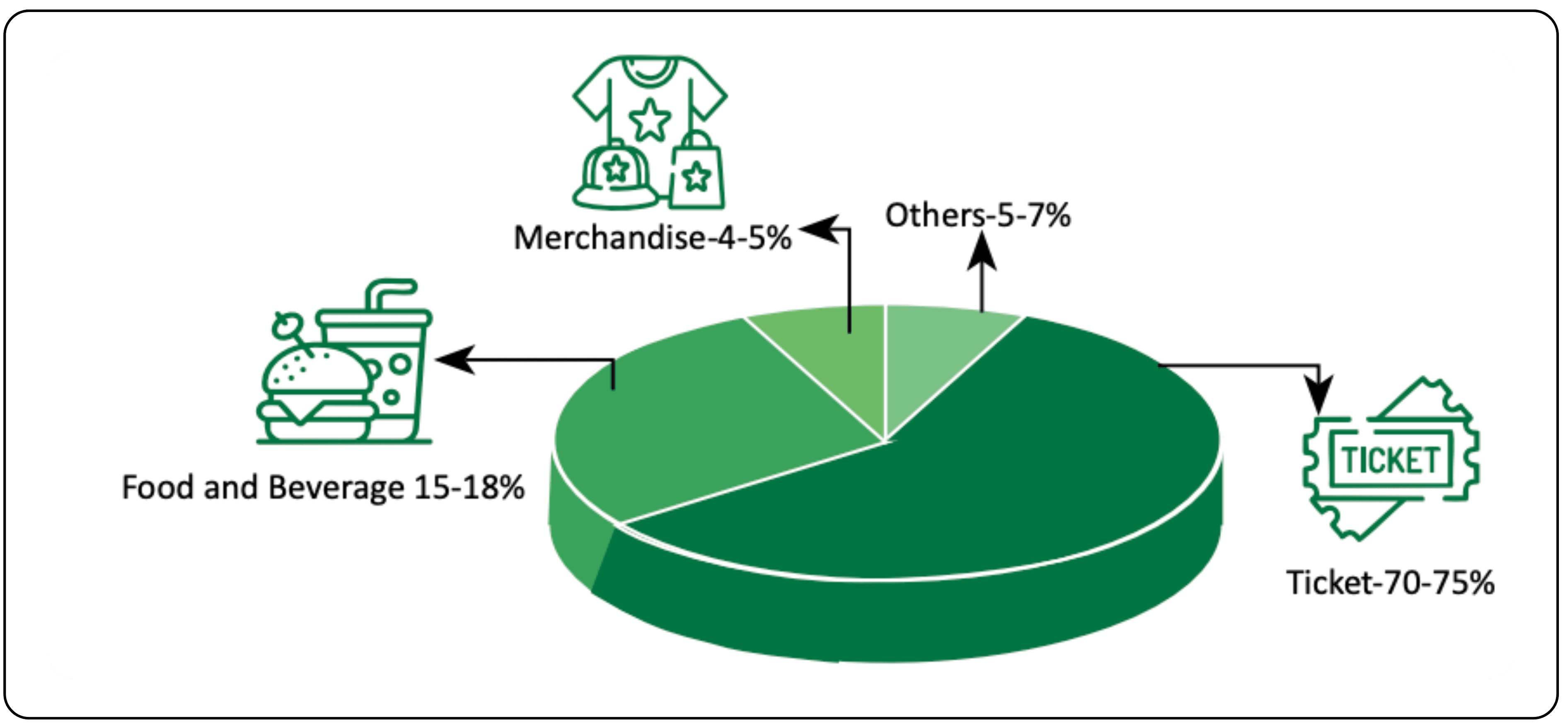

The Indian market remains moderately fragmented, with a few large organized players dominating market share and numerous small to medium-sized operators serving local and regional markets. In terms of revenue composition, the Indian market is heavily reliant on ticket sales, which account for approximately 65% to 70% of total revenue., This is in contrast to global markets, where non-ticketing revenue typically holds larger shares through merchandising, food and beverage sales, and ancillary services.

In the organized segment, Wonderla Holidays Limited stands out as a market leader, operating four strategically located parks in Kochi, Bengaluru, Hyderabad, and Bhubaneswar. The company has served over 450 lakh cumulative visitors since its inception, reflecting its strong brand presence and operational scale. Another prominent player is Imagicaaworld Entertainment Limited, which offers a multi-format destination featuring theme park, water park, snow park, and luxury hotel accommodation, having served 188 lakh visitors to date.

Infrastructure Capacity analysis reveals that large parks typically accommodate 6 to 10 lakh visitors annually with average ticket prices ranging from ₹1,000 to ₹1,400, while medium parks handle 3 to 6 lakh cumulative visitors annually with pricing between ₹700 and ₹900. Combined infrastructure across major destinations includes 187 rides of various categories, 18 restaurants offering diverse cuisine options, 5 banquet halls for events and celebrations, 6 food courts for casual dining, and 2 lounge bars for adult entertainment.

Growth Catalysts

Infrastructure development initiatives have significantly enhanced the industry’s growth prospects. Significant improvements in road connectivity through National Highway Authority of India initiatives have substantially expanded the catchment areas for existing parks. In FY24, NHAI executed 6,644 km of road projects, enhancing accessibility and reducing travel times to major park destinations, thereby expanding the effective market reach of established facilities.

Government policy support has emerged as a crucial growth enabler through various state tourism policies. The Maharashtra Tourism Policy 2016, Gujarat Tourism Policy 2021 to 2025, and Madhya Pradesh Tourism Policy 2016 provide substantial incentives for park development and operation. Government support for amusement parks in India includes substantial policy incentives like tax benefits, land allocation support, and infrastructure development assistance demographic dividend continues to be a fundamental strength, with India’s young population and growing middle class creating sustainable demand patterns. The increasing share of the working-age population, coupled with higher disposable incomes across income segments, supports consistent visitor growth and increasing per-visitor spending patterns.

Rising education levels and global exposure are driving consumers to spend more on high-quality leisure experiences, which is supporting revenue per visitor growth across all park categories.

Technology & Digital Transformation

Amusement park’s digital transformation India is reshaping guest experiences, with the sector undergoing rapid technological evolution, reshaping both guest experience and operational efficiency. Leading players have adopted mobile ticketing, RFID lockers, and virtual queuing to reduce wait times and streamline entry. These tools not only enhance the guest experience but also enable more efficient crowd flow and resource allocation. Leading operators are implementing comprehensive amusement park sustainability initiatives, with parks embracing green technologies and renewable energy adoption. For instance, over 60% of Imagicaa’s energy needs are now met through renewable sources like solar and wind power, showcasing a growing commitment to sustainability and environmental responsibility within the industry.

Advanced technologies are being deployed behind the scenes to improve safety, maintenance, and operational planning. Parks are deploying IoT sensors for predictive ride maintenance, AI for crowd management and dynamic pricing, and ERP systems for safety audits. Together, these innovations are enabling Indian amusement parks to create smarter, safer, and eco-friendly entertainment systems.

Challenges & Risk Factors

India’s amusement park sector faces multiple risks that directly affect growth, profitability, and long-term sustainability. Attendance remains highly seasonal, with summer holidays contributing over 40% of annual footfall, while monsoons reduce water park revenue significantly. Weather extremes such as heat waves and heavy rainfall create sharp volatility in visitor numbers.

Economic conditions also shape demand, as discretionary spending drives over 70% of total revenues inflation or downturns can quickly cut per-capita spending. Health risks remain critical as during the COVID-19 pandemic, the industry revenues fell nearly 90% underscoring the sector’s vulnerability to health crises and operational shutdowns. The business model itself is challenged by high fixed costs. Building a single premium amusement park requires a capital investment exceeding ₹4,000 million, making it difficult to absorb prolonged periods of low attendance or forced closures. Skill shortages in park operations, rising competition from indoor entertainment centers, environmental pressures, and increasing interest costs all contribute to higher operational expenses and weaken the financial stability of the sector.

Strategic Opportunities

India’s amusement park industry is supported by strong structural drivers. Urbanization is projected to rise from 35% in 2020 to 41% by 2030, with over 55% of the population in the 15-60 age group fueling demand. The share of Upper-middle-income households is also expected to double to 44% by 2030, boosting discretionary spending.

Domestic tourism is growing at an 8-10% CAGR, supported by better connectivity. To capture this momentum, operators are diversifying revenue beyond tickets, adopting AR/VR, RFID, and dynamic pricing, while expansion into Tier2/3 cities, sustainability initiatives, and themed IP-based attractions further create long-term growth opportunities.

Financial Performance & Investment Landscape

Market size and growth: The Indian amusement park industry was valued at ₹10,800 - 11,400 crore in FY24 and is projected to grow at a 9-11% CAGR, reaching ₹20,500 - 25000 crore by FY2030. The selector has rebounded strongly post-pandemic, expanding from ₹5,400 crore in 2020 to a projected ₹12,500 crore by 2028.

Ticket sales contribute 70-75% of industry revenues, with food & beverages (15-18%) and merchandise (4-5%) emerging as growing high-margin streams.

Revenue Stream Comparison

| Revenue Stream | Wonderla (₹ Cr) | Imagicaa (₹ Cr) |

|---|---|---|

| Ticket Sales | 320.6 – 343.5 | 287.0 – 307.5 |

| F&B | 68.7 – 82.4 | 61.5 – 73.8 |

| Merchandise | 18.3 – 22.9 | 16.4 – 20.5 |

| Others | 13.7 – 27.5 | 12.3 – 24.6 |

Company performance (FY25):

- Wonderla: ₹458 crore revenue, 30.5 lakh footfalls, EBITDA margin 37% (down due to weak demand).

- Imagicaa: ₹410 crore revenue, 27 lakh visitors, 52% YoY growth, 21.3% operating margin.

Future Outlook & Trends

The Indian amusement and theme park industry is set on a growth path with a CAGR of 9-11% through FY2030, supported by favorable demographics, rising disposable incomes, and improving infrastructure. Sustainability initiatives such as renewable energy adoption and water recycling are becoming integral to operations, aligning with global standards and consumer expectations.

At the same time, culturally relevant themed experiences, deeper integration with hospitality and retail, and a shift toward full-fledged entertainment ecosystems underline the industry’s strategic evolution. Together, these factors position the sector for long-term, sustainable growth.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.