Founded in 1939, Tata Chemicals Ltd (TCL) is one of the oldest and most globally diversified companies in India’s chemical space. Part of the Tata Group, the company manufactures and exports a range of basic and specialty chemistry products. It is not only a leading producer of soda ash and sodium bicarbonate but also a key player in agri-inputs and specialty chemicals through its subsidiary Rallis India Ltd.

TCL has evolved from a bulk commodity manufacturer to a multi-pronged chemical business with strong backward integration, global sourcing, and innovation-led product development. It operates with a dual focus: basic chemistry products like soda ash, salt, and cement, and specialty segments like nutrition, crop care, and advanced materials.

Business model and verticals

Tata Chemicals’ business model is built on integration, global reach, and category leadership. Its core verticals are:

1. Basic Chemistry

This segment contributes the lion’s share of the revenue (about 77% as of FY22). TCL is the world’s third-largest producer of soda ash and sixth-largest for sodium bicarbonate. Its production network spans across India, the US, UK, Kenya, and South Africa, with a combined soda ash capacity of over 4.3 million tonnes per annum (MTPA).

Key products include:

- Soda Ash (dense and light)

- Sodium Bicarbonate

- Salt (including pharma and industrial variants)

- Cement (byproduct from soda ash)

- Marine chemicals and halogen compounds

The company’s global subsidiaries (Tata Chemicals North America, Europe, Magadi (Kenya), and South Africa) ensure value chain integration and local market servicing.

2. Specialty Chemistry

This high-margin segment (23% of FY22 revenue) includes:

- Agro Sciences: Rallis India, a listed subsidiary, provides crop protection and agri-input solutions and reaches 80% of India’s districts.

- Nutritional Sciences: Includes prebiotics, low-GI sweeteners, and nutritional salts catering to food and wellness brands.

- Material Sciences: Advanced materials like highly dispersible silica and precipitated silica, mainly used in tyres, paints, and industrial rubber.

Geographical Split and Product Portfolio

TCL has a truly global footprint. Its regional product presence is tailored to local demand and resource availability:

- Asia (India & excluding China): Offers soda ash, sodium bicarbonate, cement, agro inputs, nutritional and specialty chemicals.

- North America: Produces dense and light soda ash via natural trona deposits; cost-efficient and environmentally superior.

- Europe: Soda ash, bicarbonate, industrial salts, energy, and de-icing salts.

- Africa (Magadi & South Africa): Specializes in high-purity soda ash, refined soda, and livestock/industrial salts.

Revenue distribution in H1FY24 was as follows:

India – 27%, US – 34%, UK – 15%, Kenya – 4%, Rallis – 20%.

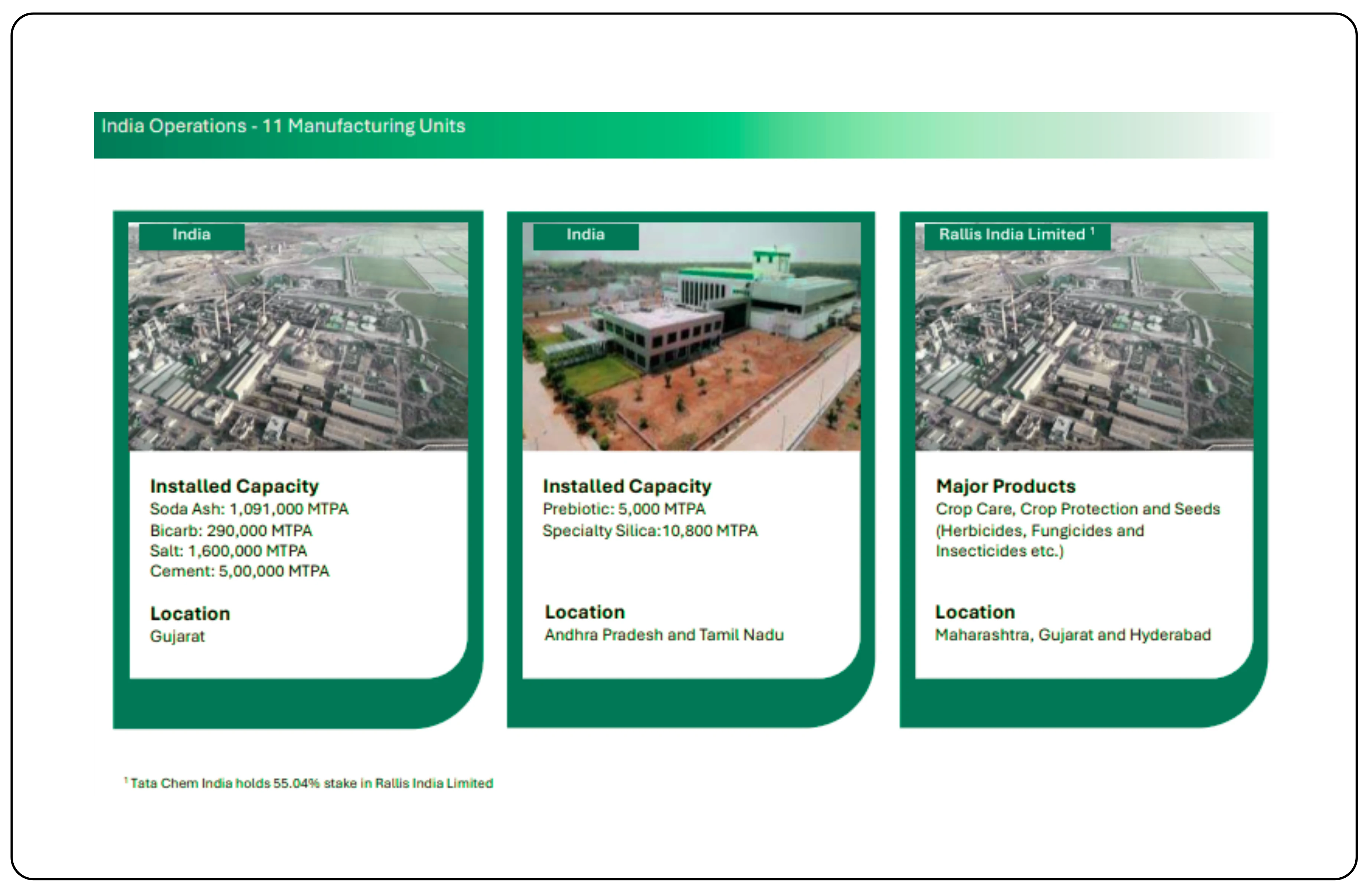

Manufacturing and R&D

Domestic Units:

- Gujarat: Soda Ash, Salt, Cement

- Andhra Pradesh, Tamil Nadu: Nutritional and Specialty products

- Maharashtra, Gujarat, Hyderabad: Rallis' agri-input manufacturing

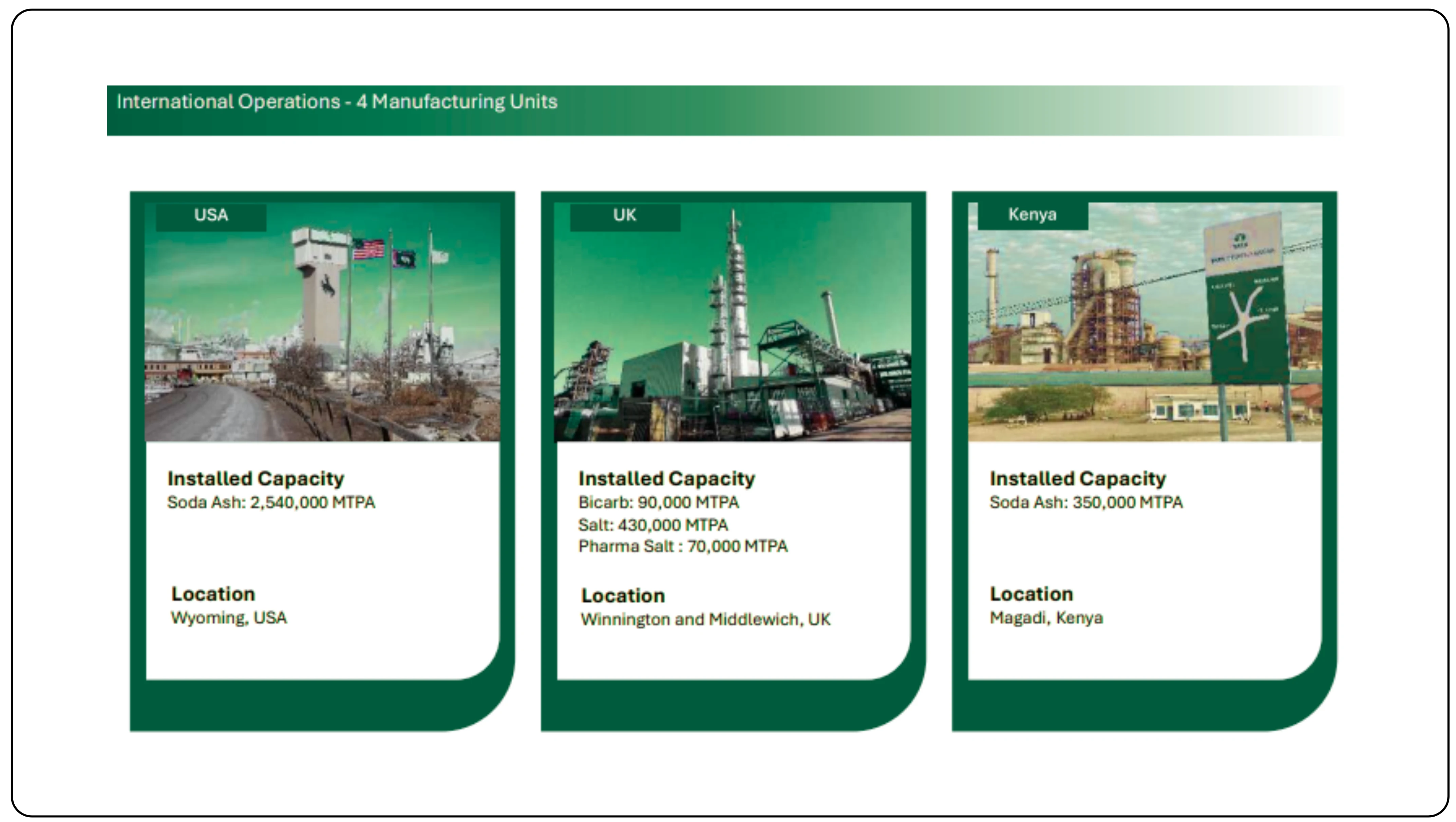

Global Units:

- USA (Wyoming): Natural soda ash

- UK (Winnington & Middlewich): Bicarb, salt, pharma-grade salt

- Kenya (Magadi): Natural soda ash

R&D:

Three advanced R&D centers and over 200 scientists have driven over 449 patents (176 granted), reflecting TCL’s pivot toward innovation and value-added chemistries.

Also read:

India’s CDMO Boom: A Rising Global Powerhouse

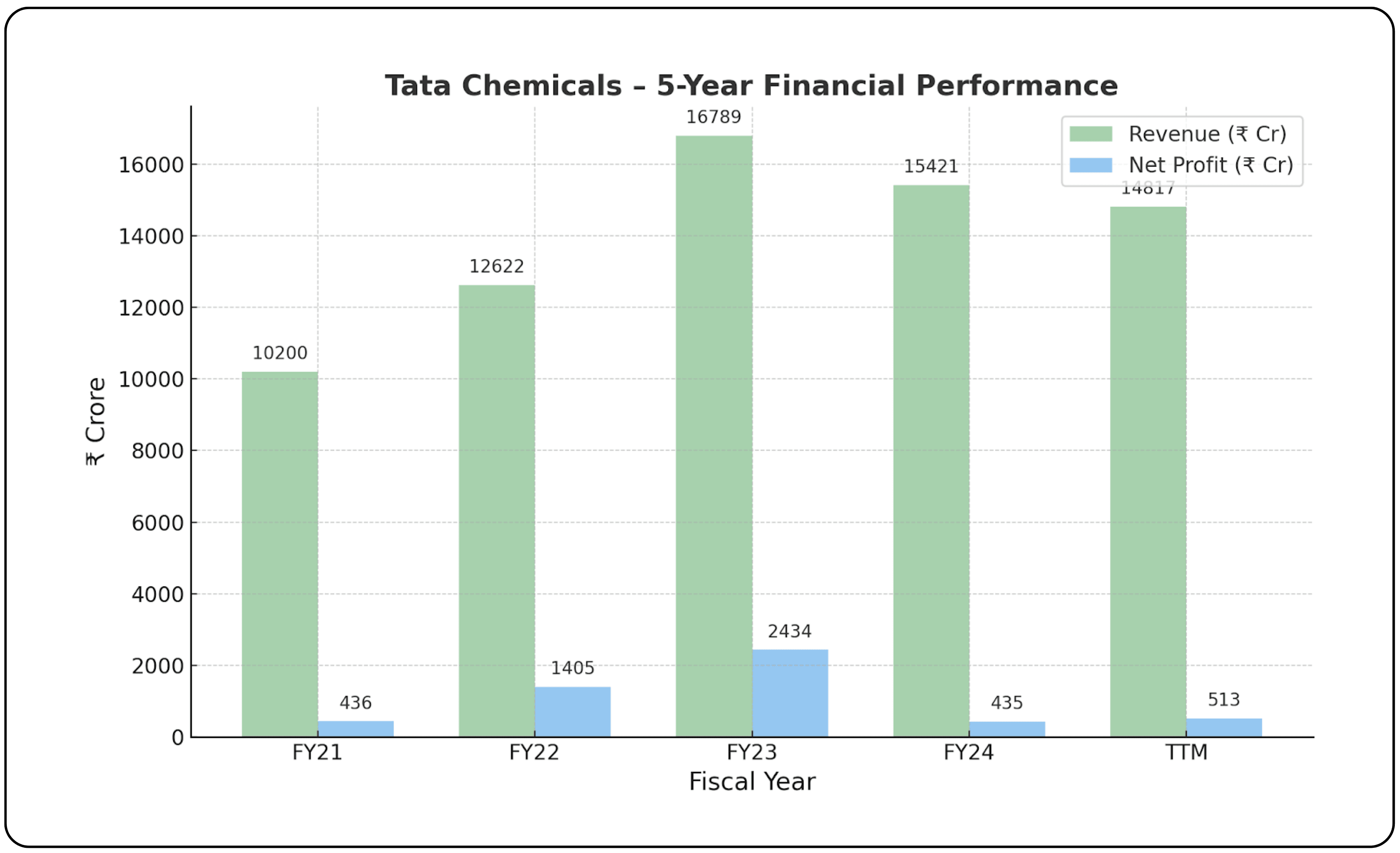

Financial Performance – 5-Year Overview (₹ Cr)

| Metric | FY21 | FY22 | FY23 | FY24 | TTM |

|---|---|---|---|---|---|

| Revenue | 10,200 | 12,622 | 16,789 | 15,421 | 14,817 |

| Operating Margin % | 15% | 18% | 23% | 18% | 14% |

| Net Profit | 436 | 1,405 | 2,434 | 435 | 513 |

After a peak in FY23 driven by strong pricing and demand, FY24 and Q1FY26 reflect a cooling cycle; global soda ash prices have softened, and volumes have been under pressure, especially in Europe and China.

Tata Chemicals’ holdings in other Tata group companies

Tata Chemicals maintains a diversified portfolio of equity investments across several Tata Group companies, aligning with its long-term value creation approach. These holdings, disclosed under fair value through Other Comprehensive Income (OCI) in the FY2024–25 annual report, include both quoted and unquoted entities. Prominent investments include Titan Company Ltd., Tata Steel Ltd., Tata Motors Ltd., and Tata Investment Corporation Ltd., alongside private holdings such as Tata Sons Pvt. Ltd., Tata Capital, Tata Projects, and Tata International. While most of these stakes are minority, they reflect the company's strategic alignment with the broader Tata ecosystem and provide additional financial strength through potential capital appreciation and dividends.

Here’s a summary of Tata Chemicals’ holdings in other Tata group companies based on the FY25 annual report:

(a) Investments in Subsidiaries and Joint Ventures (Fully paid up at cost)

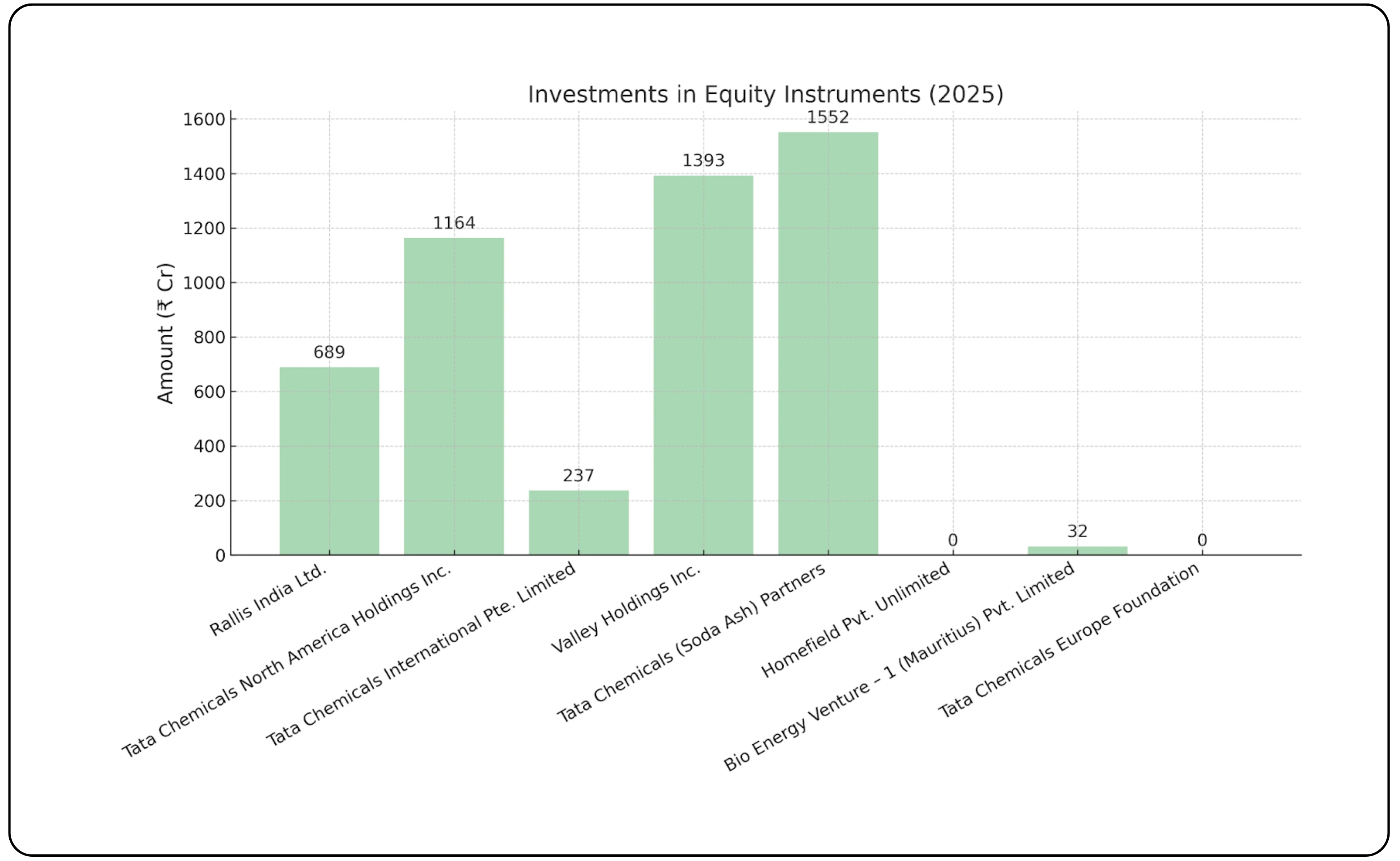

(i) Subsidiaries – Investments in Equity Instruments

This bar graph shows the amount (in ₹ Cr) invested by Tata Chemicals in its subsidiaries through equity instruments. These investments reflect the company’s strategic control and long-term interest in key operations across geographies. For instance, Rallis India contributes directly to the agri-inputs business, while Valley Holdings and Tata Chemicals (Soda Ash) Partners support the global soda ash operations. Though these holdings don’t generate direct income like dividends in all cases, they form the backbone of consolidated financial performance, influencing group-level revenue, margins, and operational leverage.

(ii) Subsidiaries – Investments in Preference Shares

This table shows the capital invested (₹ Cr) in preference shares of subsidiaries, specifically in Tata Chemicals International Pte. Limited. Preference share investments are typically structured to provide fixed returns and are prioritized over equity in case of liquidation. While they may not offer voting rights, such instruments allow the parent company to support the subsidiary’s capital needs while securing a more stable income stream compared to ordinary equity holdings.

| Name | No. of Securities | Amount (₹ Cr) |

|---|---|---|

| Tata Chemicals International Pte. Limited | 2,61,00,000 | 646 |

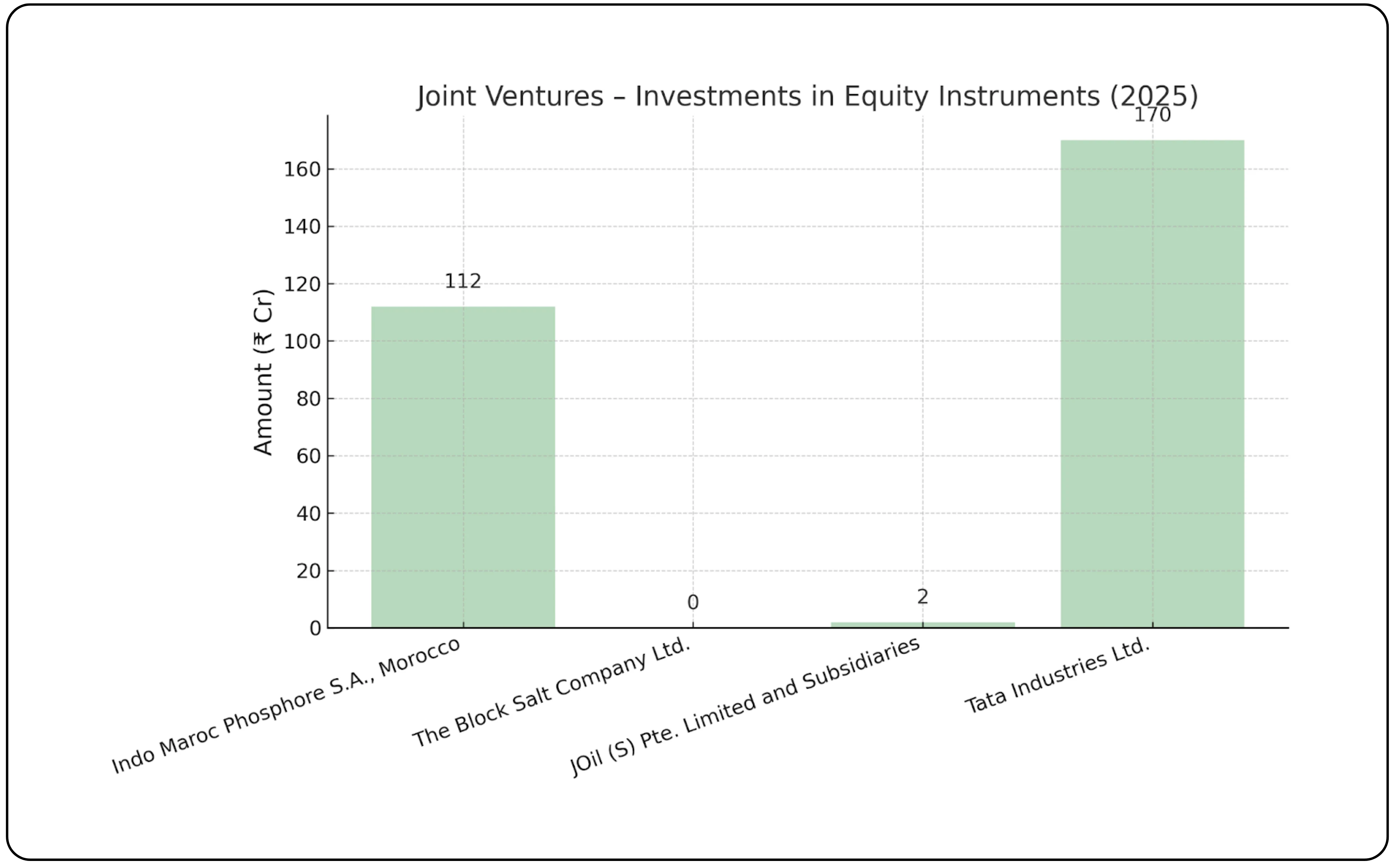

(b) Joint Ventures – Investments in Equity Instruments

This graph represents the equity investments (in ₹ Cr) made by Tata Chemicals in its joint ventures. These include strategic partnerships such as Indo Maroc Phosphore S.A., which supports backward integration for phosphoric acid, and Tata Industries Ltd., a promoter-level investment. Such joint ventures enable the company to access raw materials, expand its global footprint, and share operational risks while maintaining meaningful economic interest. Though joint ventures are not fully consolidated in financials, their performance can significantly influence Tata Chemicals’ share of profits and long-term resource security.

(c) Other Investments

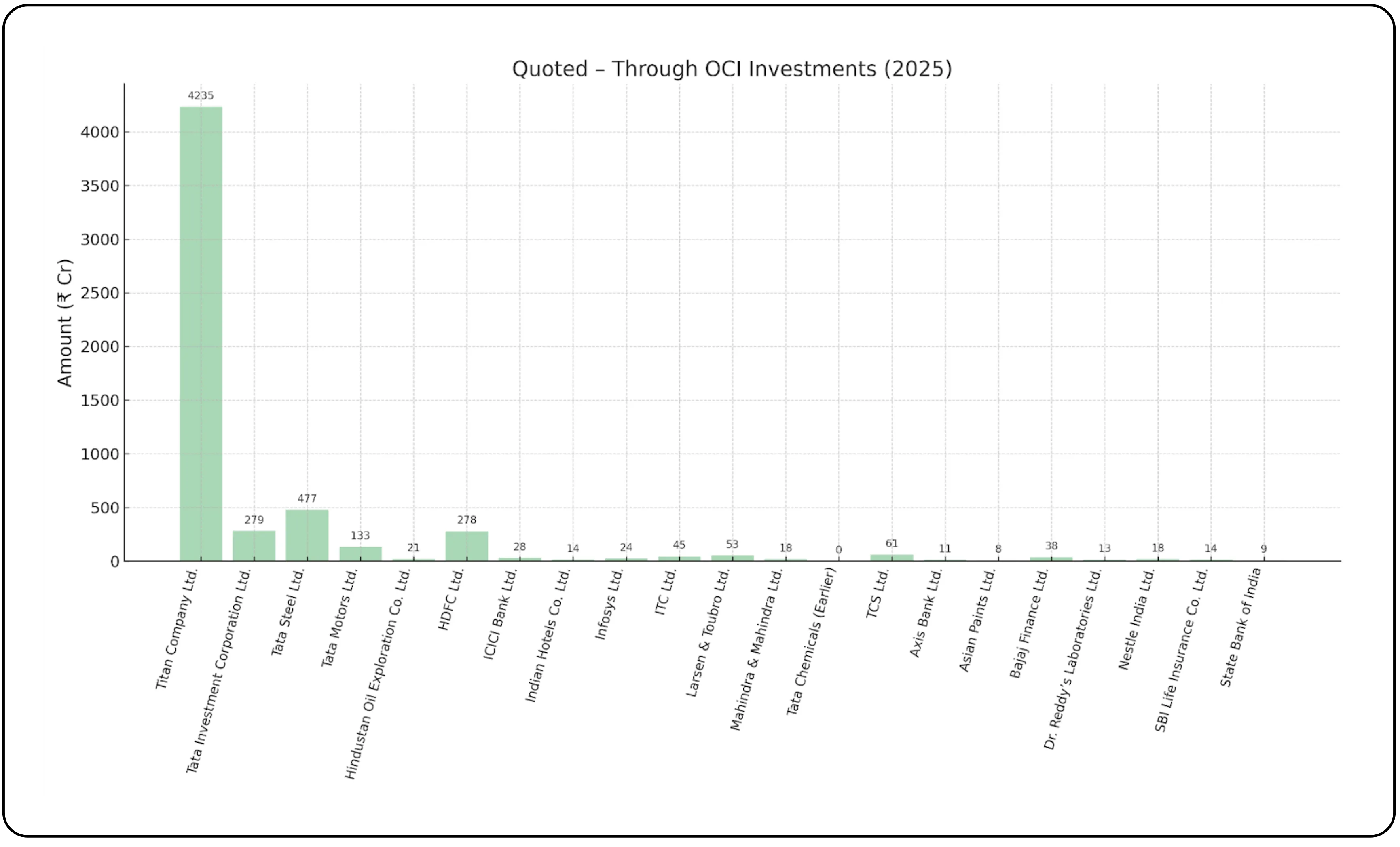

(i) Quoted – Through OCI

This bar graph displays Tata Chemicals’ investments in publicly listed (quoted) companies, categorized under Other Comprehensive Income (OCI). These are long-term, non-strategic equity holdings in entities such as Titan Company Ltd., Tata Steel Ltd., and Infosys Ltd. Since these investments are marked to market, changes in their fair value impact the company’s net worth through OCI but do not affect the profit and loss statement unless sold. This portfolio provides financial flexibility and potential capital appreciation, contributing to balance sheet strength without operational involvement.

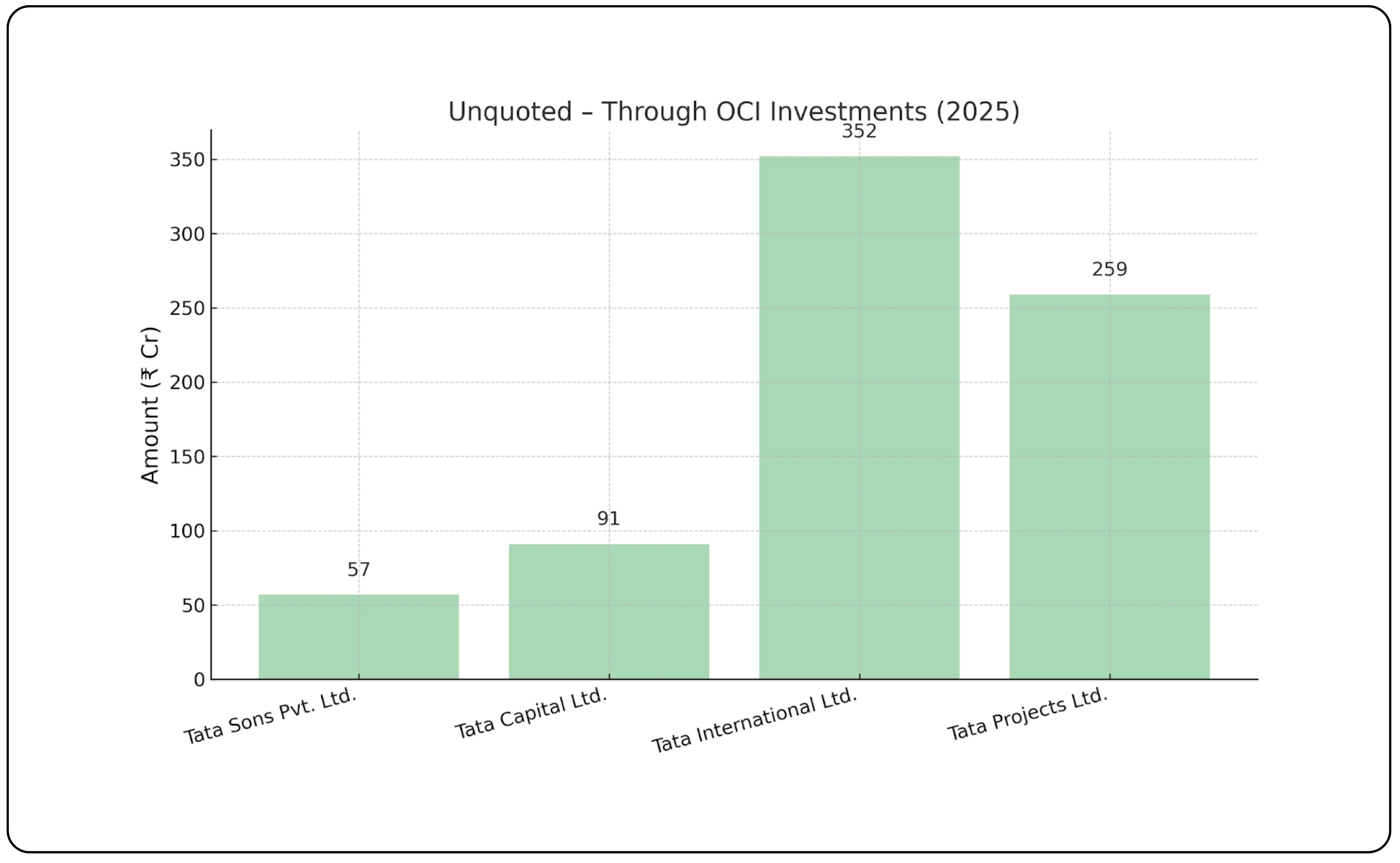

(ii) Unquoted – Through OCI

This graph represents Tata Chemicals’ investments in unquoted (privately held) companies, recorded through Other Comprehensive Income (OCI). These include entities like Tata Sons Pvt. Ltd., Tata International Ltd., and Tata Capital. While these investments do not trade on public markets, they are often strategic and reflect long-term association with core Tata Group businesses. Changes in their valuation are accounted for through OCI, impacting net worth but not the income statement. These holdings offer potential for long-term value creation, though they are generally less liquid and more conservatively valued than quoted investments.

Also read:

Why Wealthy Indians Are Buying Second Homes Abroad?

Business outlook and expansion plans

Despite the current softness in demand and pricing, the long-term demand story for Tata Chemicals remains intact. Key drivers include, the growing use of soda ash in solar photovoltaic (PV) panels and lithium-ion batteries, rising demand for prebiotics and specialty silica among health-conscious and sustainability-focused consumers, and the increasing need for agri-inputs in India.

Tata Chemicals has planned a capital expenditure of ₹2,000 crore for the period FY24–27 aimed at expanding its core capacities. The company will increase its soda ash production capacity by 30%, sodium bicarbonate by 40%, and specialty silica capacity by five times. This expansion will raise total soda ash capacity from the current 4.3 million tonnes per annum (MTPA) to 5.3 MTPA, further strengthening its position as a global leader. Notably, a significant portion of this capacity is derived from natural soda ash, ensuring lower production costs and improved competitiveness, especially during periods of global price volatility.

Valuation

Tata Chemicals currently trades at an EV/EBITDA multiple of 12.6, which is slightly below the industry average of 13.25. On the surface, this suggests modest undervaluation. However, this discount appears tied to near-term margin compression and subdued earnings in FY24 and early FY25, stemming from weak soda ash pricing and global demand softness.

Looking ahead, the picture changes. The company is in the midst of a ₹2,000 crore capex cycle aimed at significantly expanding its soda ash, bicarbonate, and silica capacities. With commissioning expected to be phased through FY26–27, the new assets are likely to unlock meaningful operating leverage. As capacity utilization improves and margins normalize, EBITDA is expected to rise faster than revenue, pulling down the EV/EBITDA multiple from current levels.

If execution stays on track and market demand stabilizes, the current valuation may prove conservative. However, any delays in commissioning or persistent pricing pressure could keep the stock trading at a discount to peers. In essence, the EV/EBITDA multiple reflects a market in wait-and-watch mode—pricing in optimism, but not fully rewarding it yet.

Closing perspective

Tata Chemicals Ltd (TCL) is in the midst of a strategic shift; from being a commodity-heavy player to becoming a specialty-driven and globally integrated chemical company. Although FY24 and early FY25 reflect margin pressure due to macroeconomic headwinds, the ongoing capex cycle and focus on innovation-led products offer strong long-term potential for the Tata chemical company.

The current valuation of Tata Chemicals appears to factor in optimism around execution and a rebound in demand. Key areas to monitor include the timely rollout of soda ash and speciality chemical capacity expansions, stabilization in the pricing environment, a recovery in Rallis India’s performance, and margin improvement heading into FY26–27.

In short, Tata Chemicals is navigating short-term challenges while building a foundation for long-term strategic strength.

Open your CubePlus account and take the first step toward smart, goal-based investing on your terms. Click here to sign up

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.