On Nxtoption, traders quickly realize that Delta isn’t a fixed number, it moves as the market moves. The Greek that explains this behaviour is Gamma. Gamma tracks how much Delta changes when the underlying price shifts. If Delta is your speedometer, Gamma is your acceleration gauge. A higher Gamma means Delta responds faster to price moves, making positions more sensitive and often riskier to manage. A lower Gamma means changes happen more gradually, giving you more breathing room. Understanding Gamma on Nxtoption can help you adjust your positions more effectively as the market unfolds.

Also read: A practical guide for new traders learning Delta

| Concept | Details |

|---|---|

| Gamma (Γ) | Change in Delta for a ₹1 change in the underlying asset |

| Units | Change in Delta per ₹1 move |

| High Gamma | Delta changes quickly → greater directional sensitivity |

| Low Gamma | Delta changes slowly → more stable position |

| Sign | Always positive for long options, negative for short options |

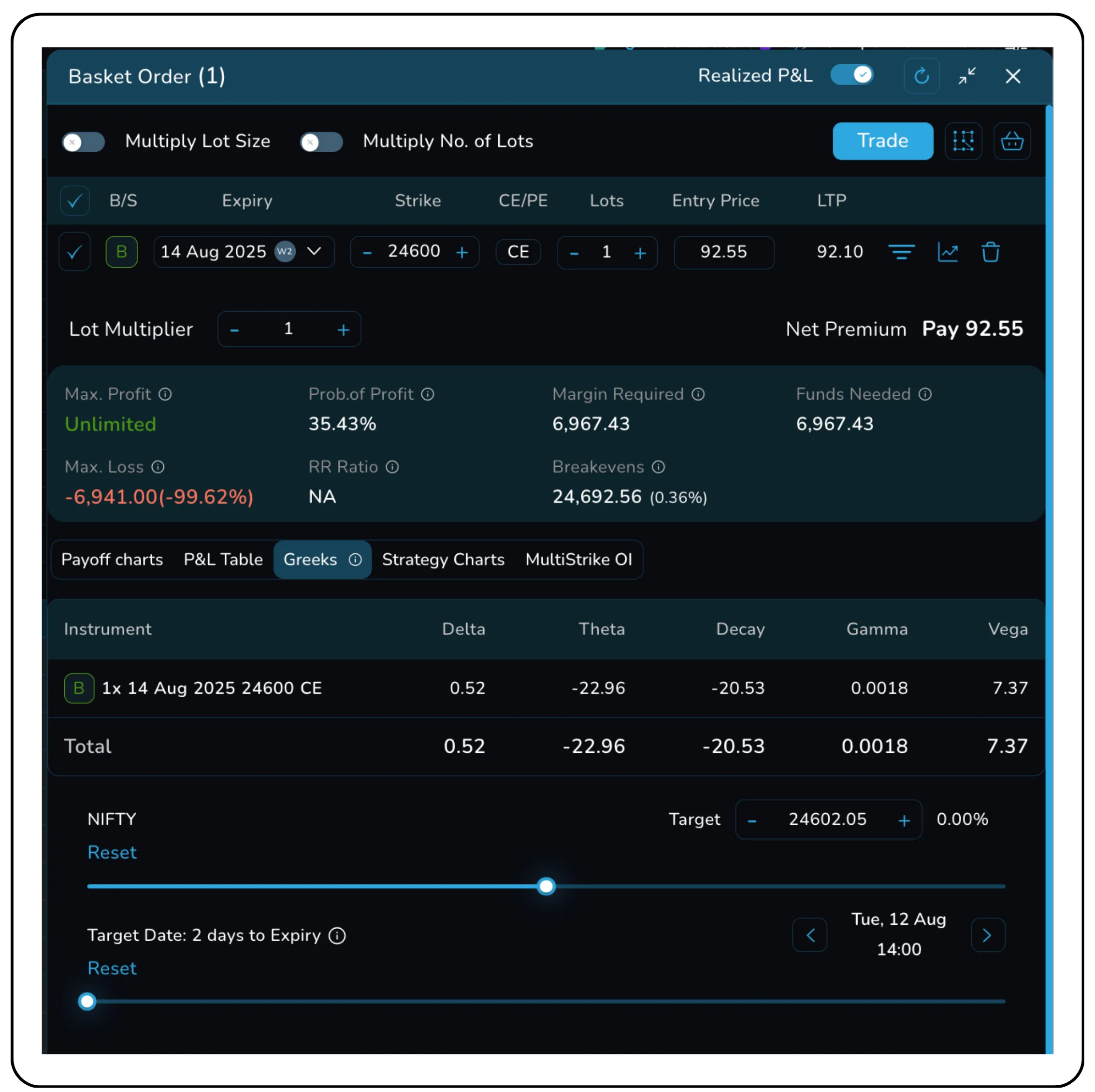

Example Setup-

Consider a position involving buying 1 lot of Nifty 24,600 CE options expiring on 14 August 2025 (weekly expiry) for the spot being ₹24,602.05

- Strike Price: 24,600 CE

- Premium Paid: ₹92.55

- Delta: 0.52 (positive because it’s a long call option)

- Gamma: 0.0018

If the Nifty index increases by ₹10:

Change in Delta = Γ × Price Move = 0.0018 × 10 = 0.018

New Delta = 0.52 + 0.018 = 0.538

This indicates that following a ₹10 increase, the option becomes slightly more sensitive to further price gains, thereby strengthening its directional exposure as the price moves favorably.

Based solely on the Delta component, the estimated change would be:

Change in Premium ≈ Δ × Price Move = 0.52 × ₹10 = ₹5.20

New Theoretical Premium ≈ ₹92.55 + ₹5.20 = ₹97.75

However, because Gamma increases Delta for subsequent price movements, additional rises would yield larger gains than the initial ₹10 move. This is the “acceleration” effect that makes long Gamma positions favorable in trending markets.

Gamma Behavior

Gamma is influenced by the same factors that affect other Greeks, but with its own patterns:

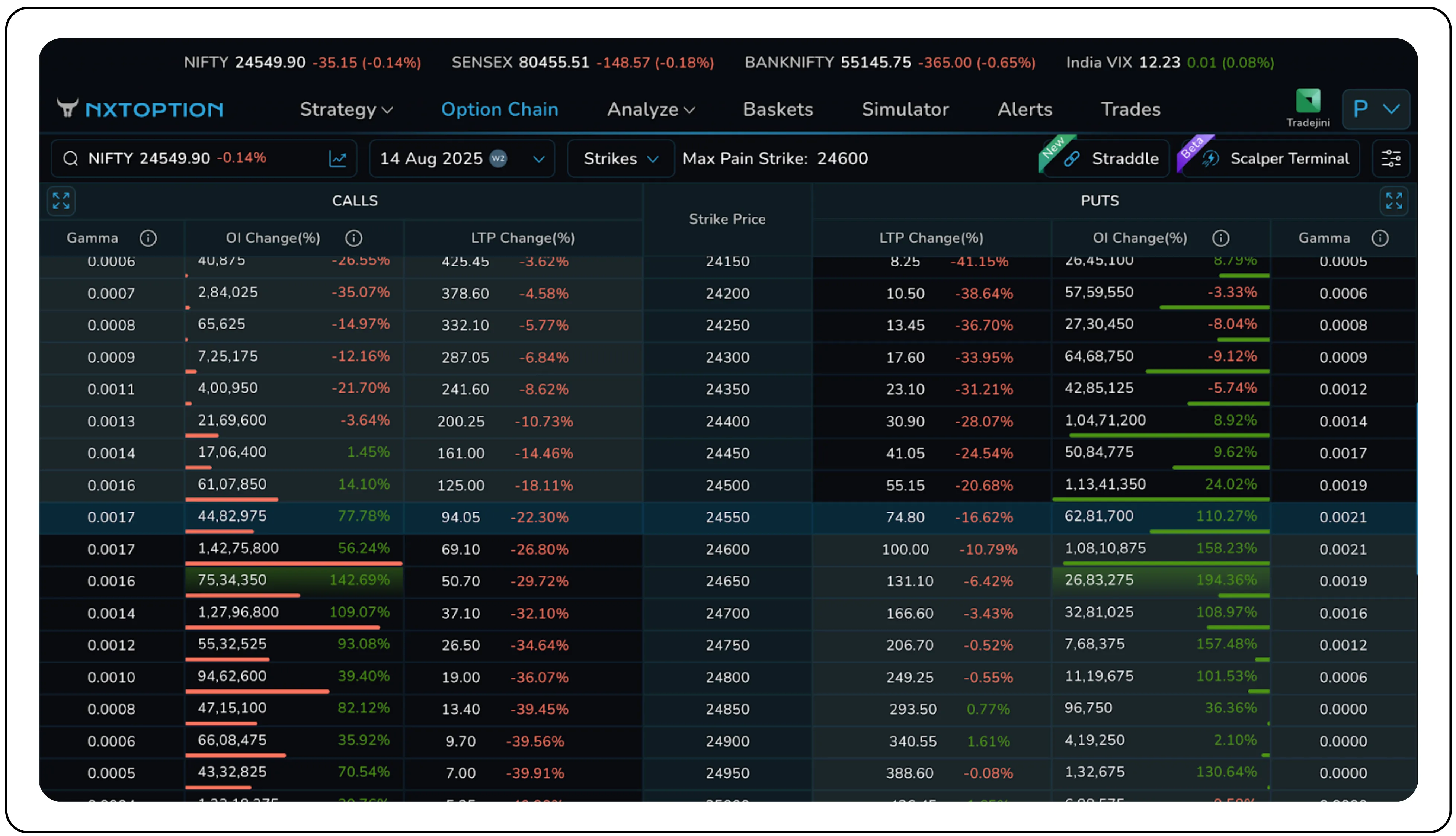

Moneyness

ATM options have the highest Gamma as small moves can flip them from OTM to ITM instantly. Whereas, deep ITM and far OTM options have low Gamma, as Delta is already near ±1 or 0 and cannot change much further. This can further be seen in the following.

With NIFTY at ₹24,549.90:

Calls are in-the-money (ITM) if the strike is below spot (e.g., 24,150 CE).

Visit ExamplePuts are ITM if the strike is above spot (e.g., 24,900 PE).

At-the-money (ATM) options have strikes near spot, here around 24,550, and show the highest Gamma.

Out-of-the-money (OTM) calls have strikes above spot, while OTM puts have strikes below spot.

ATM strikes are most sensitive to price changes, making them crucial in Gamma-based strategies.

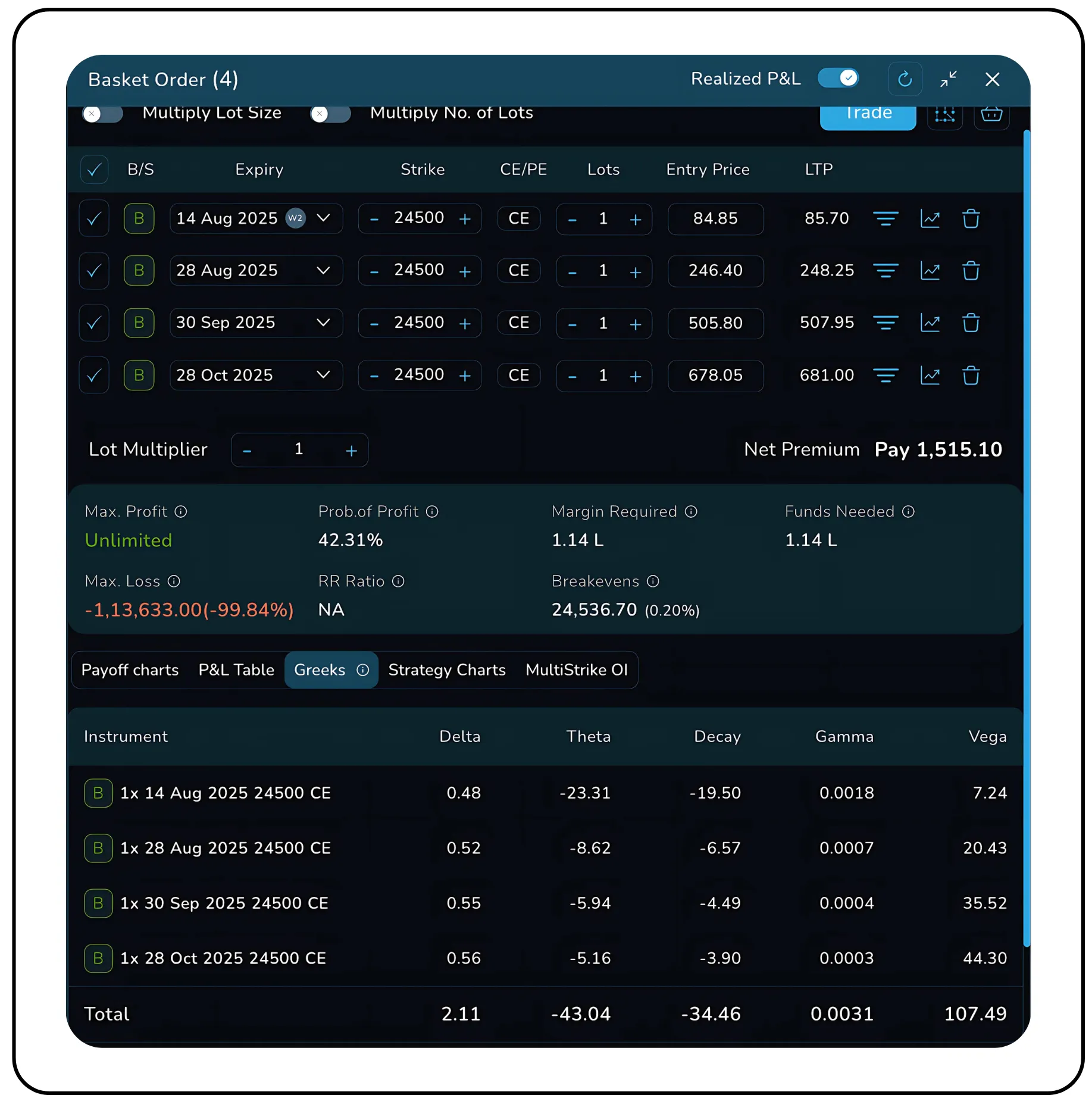

Time to Expiry

Gamma spikes for ATM options during near dated expiries. This is because probability shifts are more binary (either ITM or worthless). Whereas ATM options for far dated expiries have low Gamma which is distributed across the strikes.

Above, we can see all calls have the same strike but different expiries. Short-dated options, like the 14 Aug contract, have higher Gamma (0.0018) as compared to longer-dated ones like 28 Oct (0.003). Higher gamma means delta shifts more rapidly with price movements, making expiry options more sensitive and volatile. This can benefit traders seeking quick directional gains but also increases the risk if the market moves unfavourably.

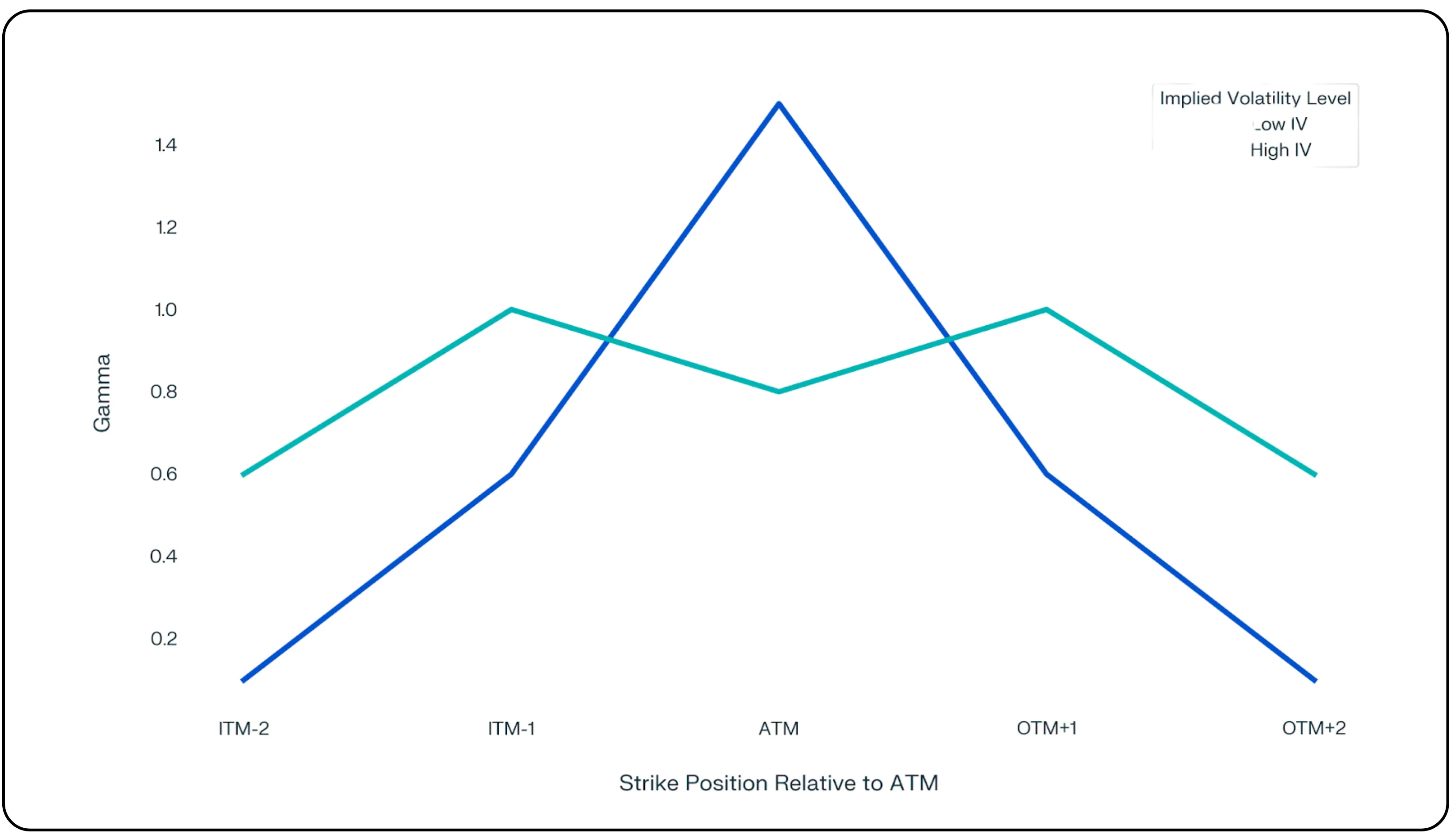

Implied Volatility (IV)

When IV is high, the probability of larger price moves increases, which spreads the Gamma curve wider. This results in a lower gamma value at the at-the-money (ATM) strike, but relatively higher Gamma for strikes slightly in-the-money (ITM) or out-of-the-money (OTM)

Conversely, when IV is low, the expected price range is smaller, concentrating Gamma sharply at the ATM strike. In such conditions, ATM options become more sensitive to small price movements, while strikes away from the ATM see much lower Gamma. This relationship affects risk and reward dynamics for option traders. This behaviour of gamma in high and low IV environments is showcased in the following graph.

Gamma in the trade’s context

In our example-

You buy 1 lot of Nifty 24600 CE expiring on 14th Aug 2025 (weekly expiry)

Spot Price: ₹24,602.05

Strike Price: 24,600 CE

Premium Paid: ₹92.55

Delta: 0.52 (positive because it’s a long call option)

Gamma: 0.0018

What this means is, for every ₹1 move in Nifty, the delta changes by 0.0018. In a high-gamma environment (usually near expiry with low IV), Delta adjusts rapidly, making intraday P&L highly sensitive to small price swings, ideal for quick scalps but riskier if direction reverses. In a low-Gamma environment (often with high IV), Delta changes slowly, giving smoother exposure but reducing short-term trading edge. Gamma thus shapes how "responsive" your position is to the market.

Understanding Gamma is not just an academic exercise. It directly influences position management and risk control. Traders holding long Gamma (for example, through buying options) will see their Delta move in their favour as the market trends, but they also need to manage the cost of holding these positions due to Theta decay. On the other hand, short Gamma positions (example, through selling options) gain from time decay but face accelerated losses if the underlying moves sharply.

High Gamma positions require frequent hedging, as Delta can swing rapidly. This is especially true for short-dated ATM options, where a small move can dramatically change exposure.

Low Gamma positions allow more relaxed adjustments, making them more suitable for passive traders or range-bound expectations.

Gamma scalping

Active traders often use a strategy called Gamma scalping, where they exploit high Gamma positions by repeatedly hedging Delta during market swings. The aim is to lock in small gains from the underlying’s volatility while offsetting Theta losses. This works best in volatile markets where the realized volatility exceeds the implied volatility priced into options.

Risk management with gamma

Ignoring gamma can be dangerous, especially for short option sellers. An option that appears stable due to low Delta can quickly become highly directional if Gamma spikes, such as during expiry or a sudden volatility event. A short ATM option on expiry day, for instance, can flip from being profitable to deep in-the-money within minutes due to sharp Delta changes.

While Delta offers a snapshot, Gamma offers a forecast. It tells traders how quickly their directional exposure will change. High Gamma means high responsiveness, which means even small underlying moves can drastically shift Delta. Whereas, Low Gamma means stability, which means positions retain their Delta exposure for longer without needing adjustment.

Gamma is particularly critical near expiry and around at-the-money (ATM) strikes, because both conditions cause Delta to move sharply with small price changes.

Ready to move from theory to practice? Track your position's Gamma in real-time to manage risk and make smarter, more informed trades with Nxtoption.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.