Varun Beverages has become India’s go-to name in soft drinks, riding the country’s growing thirst for packaged beverages even as competition heats up in a fast-growing market.

It’s the world’s second-largest PepsiCo bottler outside the US and the biggest in India. The partnership with PepsiCo goes back more than three decades and now runs through April 2039, giving Varun a deep competitive edge in a market where demand for branded drinks keeps climbing.

Business model: End-to-end integrated operations

Varun Beverages runs the entire show—from making the drinks to getting them into shops. Its network is massive: This fully integrated beverage operation allows VBL to maintain quality, improve logistics, and sustain cost leadership.

- Manufacturing: VBL operates 50 modern production facilities, including 38 plants in India and 12 overseas, strategically located to optimize production efficiency and logistics.It’s the world’s second-largest PepsiCo bottler in India, and the biggest overall across PepsiCo’s global franchise network outside the US.

- Distribution network: The company’s reach is supported by 130+ depots and a network of over 2,800 primary distributors, ensuring deep market penetration and last-mile connectivity.

- Strong retail presence: With more than 1.15 million visi-coolers installed across 4 million-plus retail outlets, VBL ensures its products remain consistently visible and readily available to consumers.

(Visi-coolers are specialized refrigerated display units placed in retail outlets to keep beverages chilled and attractively showcased, enhancing brand visibility and impulse purchases.)

- Logistics Infrastructure: VBL manages a fleet of 2,600 company-owned trucks complemented by 10,000 distributor vehicles, including over 2,000 electric vehicles, reinforcing its commitment to operational efficiency and sustainability.

- Global footprint: The company has operations spanning 10 countries with full franchise rights and holds distribution rights in 4 additional markets, underscoring its position as a key player in the global beverage industry.

This integrated setup lets VBL control quality, reach stores faster, and keep costs in check.

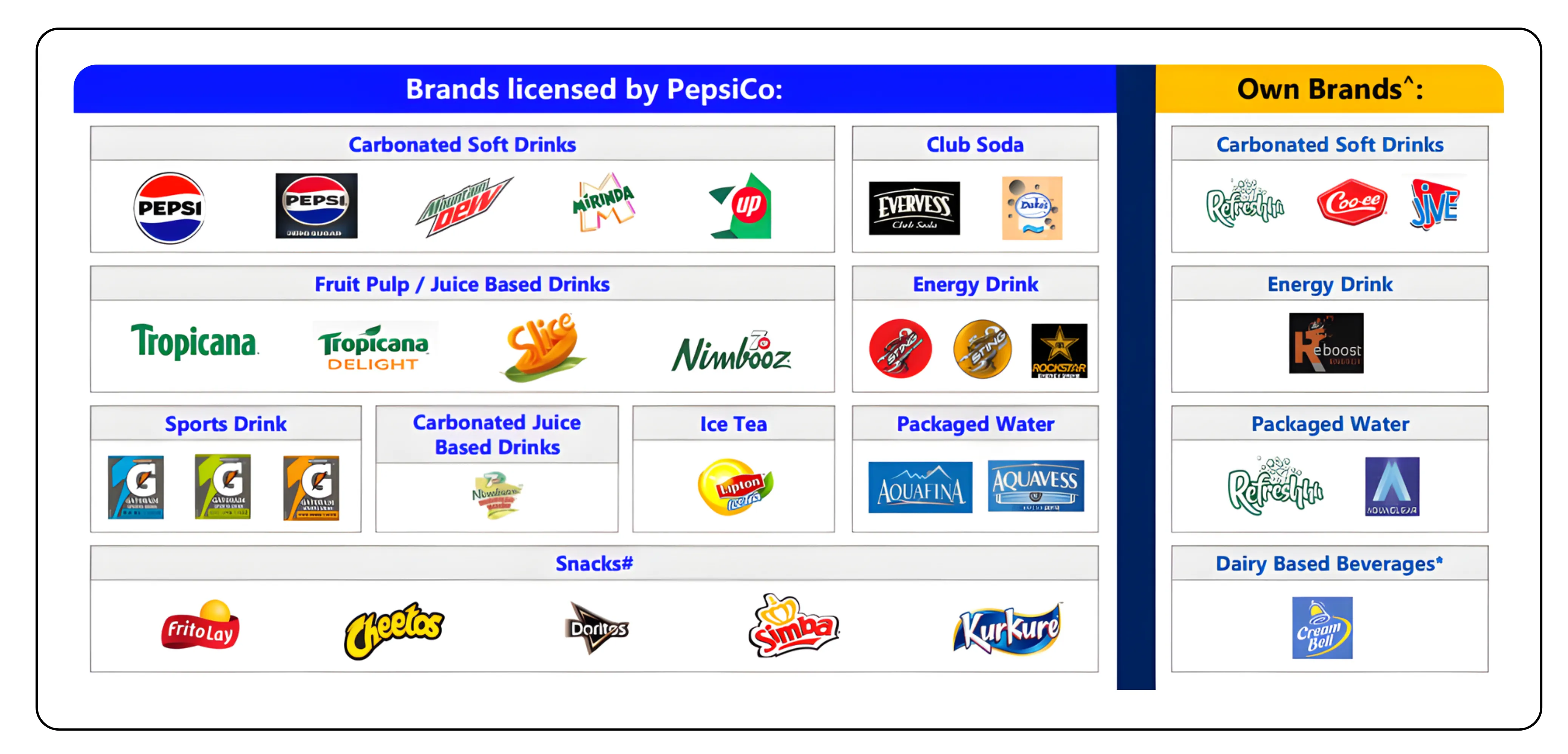

Product portfolio diversification

Varun Beverages isn’t just about fizzy drinks anymore. Its range now covers:

- PepsiCo brands: Pepsi, Mountain Dew, 7UP, Mirinda, Sting, Slice, Tropicana, Gatorade, and Aquafina

- Own brands: CreamBell dairy drinks and a few regional favourites

- New bets: Snack production like Cheetos in Morocco and Simba Munchiez in Zambia and Zimbabwe

As of Q2FY25, the mix still leans heavily toward soft drinks—Carbonated Soft Drinks make up 75% of sales, packaged water 18%, and non-carbonated drinks 7%.

Curious about another under-the-radar player? Check out Could Laxmi Dental Be the Hidden Gem in Healthcare?— our fundamental breakdown of India’s only integrated dental products maker.

Financial performance overview

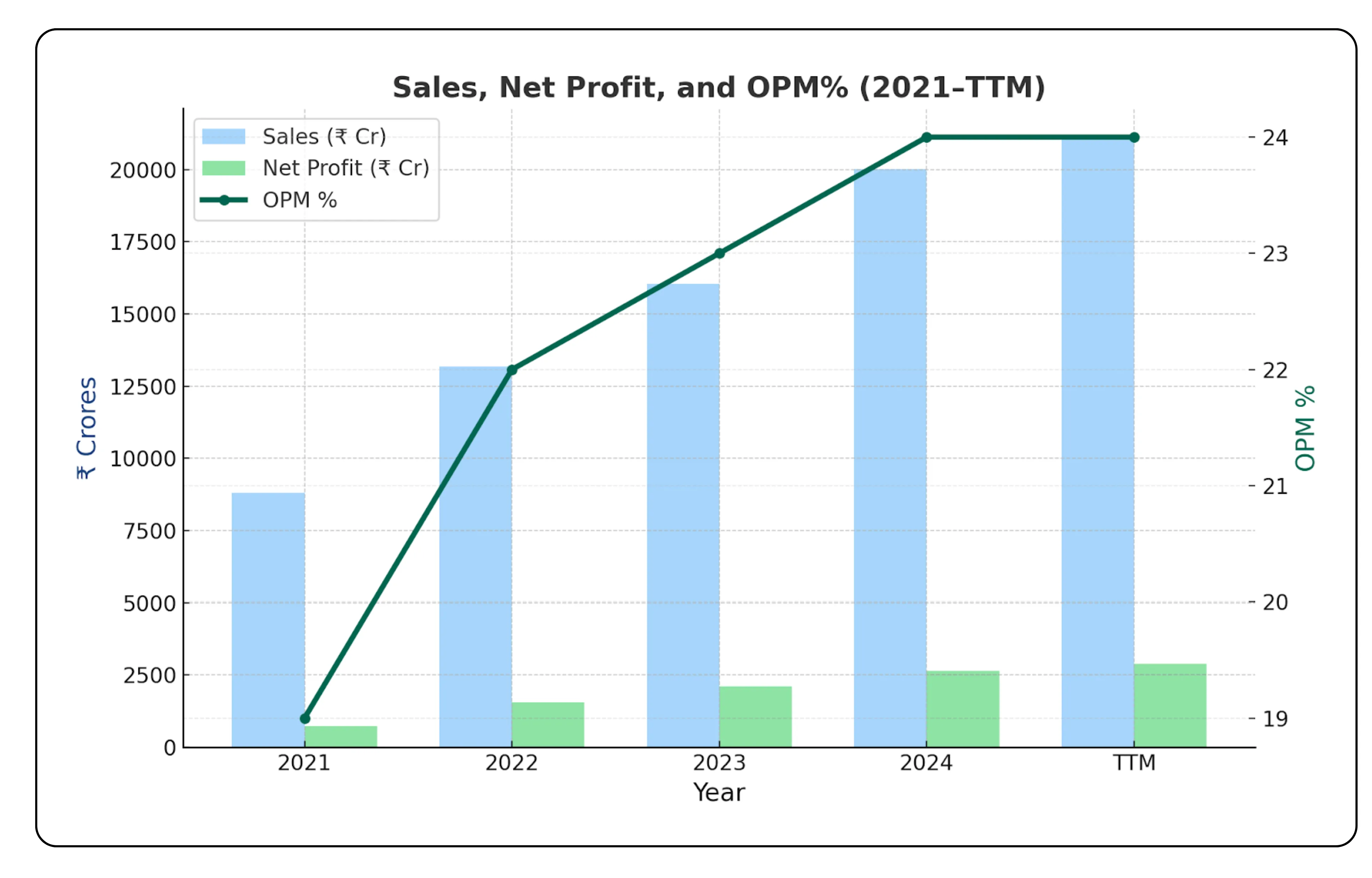

From a VBL stock analysis perspective, revenue and profit growth have been remarkably consistent:

VBL’s financial performance has shown strong and consistent growth over the past few years

| Year | Sales (₹ Cr) | Operating Profit (₹ Cr) | OPM % | Net Profit (₹ Cr) |

|---|---|---|---|---|

| 2021 | 8,823 | 1,694 | 19 % | 746 |

| 2022 | 13,173 | 2,863 | 22 % | 1,550 |

| 2023 | 16,043 | 3,717 | 23 % | 2,102 |

| 2024 | 20,008 | 4,815 | 24 % | 2,634 |

| TTM | 21,078 | 4,991 | 24 % | 2,881 |

Varun Beverages has shown strong and consistent growth over the past few years. Sales have climbed from ₹8,823 crore in 2021 to ₹21,078 crore on a trailing twelve-month (TTM) basis. Operating profits have grown in tandem, reaching nearly ₹5,000 crore in the TTM period, with operating margins steadily improving from 19% in 2021 to 24% today.

Net profit has also followed an upward trajectory, rising from ₹746 crore in 2021 to ₹2,881 crore TTM. This demonstrates not only volume growth but also operational efficiency, as the company has been able to expand margins while scaling its business.

In short, the financials highlight a combination of strong top-line growth, improving profitability, and disciplined cost management, positioning Varun Beverages for continued expansion in India and abroad.

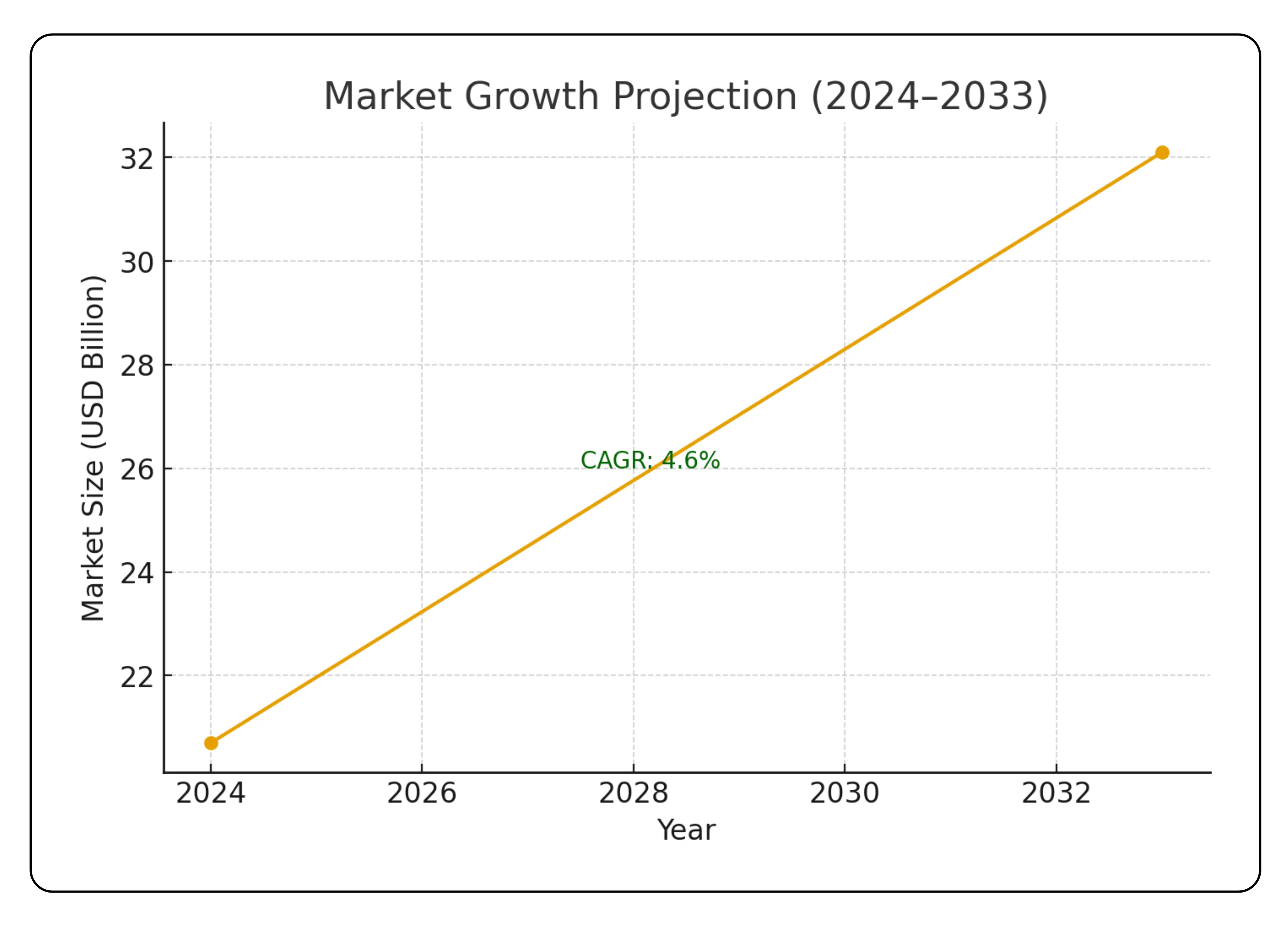

Massive market potential

India’s soft drink story is still just getting started.

The market was worth about USD 20.7 billion in 2024 and is expected to touch USD 32.1 billion by 2033 at a CAGR of 4.6%. Some other estimates peg it at USD 5.5 billion growing to USD 10.85 billion by 2034 at around 7% CAGR.

What makes it even more promising is how little Indians still consume compared to the rest of the world. Per capita soft drink intake in India is far below global averages—lower even than Bangladesh and Pakistan—leaving plenty of room for growth.

Interested in consumer stories beyond beverages? Don’t miss Sky Gold – Capturing Market Opportunities in Jewelry, a sharp analysis of how this niche player is riding India’s jewelry upcycle.

VBL growth drivers

Several tailwinds are powering Varun Beverages’ growth:

- Young population: With two-thirds of Indians under 35, there’s a natural boost in demand for ready-to-drink beverages.

- Urbanization: More people moving to cities and rising incomes mean greater appetite for packaged drinks.

- Better infrastructure: A stronger cold chain network and the rise of modern retail stores are helping drinks reach more places, faster.

- Shift to healthier choices: Low- and no-sugar options now make up 55% of sales in H1 2025, showing how VBL is keeping up with changing tastes.

Competitive landscape

India’s soft drink market share is still a two-horse race—Coca-Cola leads with about 60% share, followed by PepsiCo at 33%, where Varun Beverages bottles and distributes over 90% of PepsiCo’s India sales.

The new challenger is Reliance, which has revived Campa Cola and is pushing it hard with family packs priced 30–40% cheaper than rivals. With Reliance’s money muscle and retail reach, that’s a real threat.

Regional brands still hold roughly 50% share in some pockets, but their grip has been loosening since GST made it easier for the big players to expand.

Strategic positioning and competitive advantages

Franchise moat

Varun’s exclusive PepsiCo franchise gives it a wide moat that’s tough for rivals to cross. It gets access to PepsiCo’s global brands that customers already know and like, strong marketing muscle, a steady pipeline of new products backed by PepsiCo’s R&D, and exclusive rights to sell across 26 Indian states and 6 Union Territories.

Operational strength

The company has been steadily adding capacity, with four new plants in Prayagraj, Damtal, Buxar, and Mendipathar boosting production. Current plants run at about 70% utilization, which means VBL can handle another couple of years of growth without big new spends. Cost controls—like better freight routes, leaner staffing, and newer, more efficient lines—helped cut other expenses by 11% YoY.

International growth

Overseas markets add another layer of growth. South Africa saw 16.1% volume growth in Q2 2025, while the company is expanding snacks production with Cheetos in Morocco and a new facility coming up in Zimbabwe. Plus, the African business benefits from currency gains that lift overall profits.

Risk assessment and challenges

Competitive pressures

Reliance’s big push with Campa Cola, backed by deep pockets and aggressive pricing, could squeeze margins and chip away at market share. Local players still hold strong ground in some regions, forcing VBL to keep spending on distribution and brand visibility.

Operational risks

The business is weather-sensitive—unseasonal rains in Q2 2025 caused a 7.1% drop in India volumes. Margins also face pressure from swings in raw material and packaging costs. On top of that, future sugar taxes or health-focused regulations could dent demand for fizzy drinks.

Market risks

Shifts toward healthier lifestyles may hurt traditional soda sales, making it crucial for VBL to diversify further. And if the economy slows, discretionary spending on soft drinks is often one of the first to be cut.

Growth strategy and capital allocation

Capacity and infrastructure investment

VBL plans a moderate spend of ₹600–700 crore in India over the next year, aimed at adding capacity in key locations and improving efficiency. It’s also pushing a 15% yearly increase in visi-cooler placements, backed by in-house manufacturing through its Everest partnership.

International focus

The company is eyeing acquisitions abroad to widen its global footprint, using its healthy cash reserves. A big part of the plan is to revive growth in South Africa and tap into other promising African markets.

Product innovation

VBL is leaning into new revenue streams, especially snacks, which offer better margins. At the same time, it’s been shifting its drinks lineup—low- and no-sugar beverages now make up 55% of volumes, reflecting a solid pivot toward health-focused products.

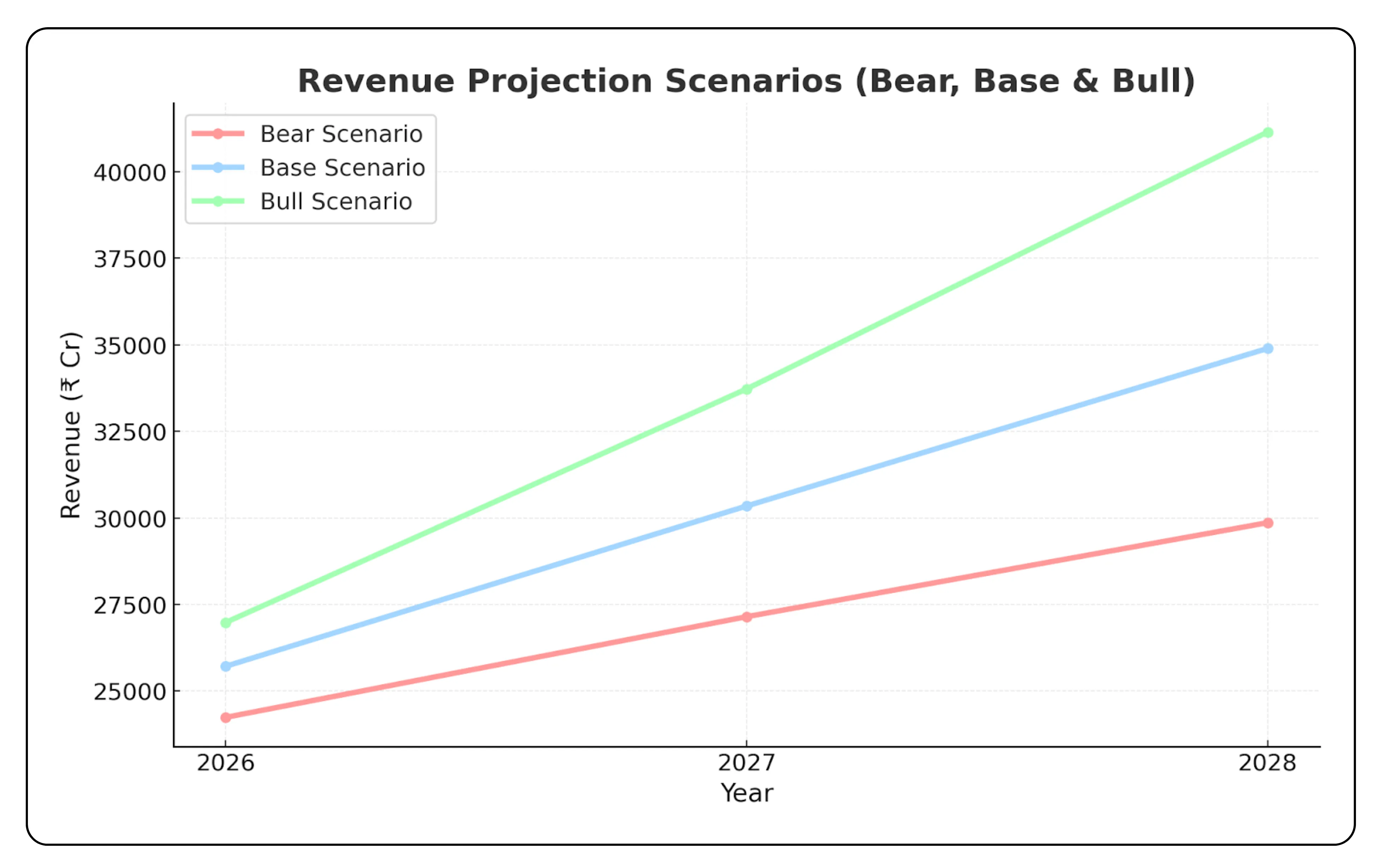

Forward P/E-based valuation scenarios for Varun Beverages Ltd

The VBL valuation under different earnings growth scenarios highlights the premium investors are willing to payBased on projected earnings, we can look at how Varun Beverages’ stock could be valued today and over the next three years under different growth scenarios.

| Scenario | Year | Revenue (₹ Cr) | PAT (₹ Cr) | PAT Margin (%) | EPS (₹) | Implied Forward P/E (x) |

|---|---|---|---|---|---|---|

| Bear | 2026 | 24,240 | 2,909 | 12.0 | 8.6 | 51.2 |

| Bear | 2027 | 27,148 | 3,122 | 11.5 | 9.2 | 47.8 |

| Bear | 2028 | 29,863 | 3,285 | 11.0 | 9.7 | 45.4 |

| Base | 2026 | 25,715 | 3,600 | 14.0 | 10.7 | 41.1 |

| Base | 2027 | 30,344 | 4,400 | 14.5 | 13.0 | 33.8 |

| Base | 2028 | 34,895 | 5,234 | 15.0 | 15.5 | 28.4 |

| Bull | 2026 | 26,980 | 4,182 | 15.5 | 12.4 | 35.5 |

| Bull | 2027 | 33,725 | 5,396 | 16.0 | 16.0 | 27.5 |

| Bull | 2028 | 41,144 | 6,789 | 16.5 | 20.1 | 21.9 |

Valuation snapshot at Current Price (₹440)

This table shows how much you’re effectively paying today for Varun Beverages based on projected earnings (EPS) under three scenarios.

- Bear scenario: Slower growth and tighter margins keep EPS lower, so the implied forward P/E is high—starting at 51x in 2026 and easing to 45x by 2028.

- Base scenario: Steady growth and improving margins gradually reduce the P/E from 41x to 28x over three years.

- Bull scenario: Strong growth and higher margins bring EPS up quickly, dropping the implied P/E from 35.5x to about 22x by 2028.

In essence, a higher implied P/E indicates paying more today relative to future profits, while a lower P/E signals better value if the company hits the projected earnings. This view helps investors see the range of potential valuations depending on how well VBL executes its growth plans.

Key Value Drivers

- Volume Growth: The company is aiming for double-digit volume growth, backed by new capacity and deeper reach into existing and new markets.

- Margin Expansion: New plants and cost-efficiency measures are expected to lift EBITDA margins over time.

- International Scaling: Growth in Africa and the snacks business adds high-margin revenue streams.

- Market Share Gains: Industry consolidation and weaker regional players could help VBL capture more market share.

Market opportunity and strategic outlook

Massive addressable market

India’s beverage market still has a lot of room to grow. VBL currently reaches around 4 million of the country’s 12 million FMCG outlets—just a 33% penetration. The company aims to expand rural coverage to 60–65% by FY27. Per capita consumption is still far below developed markets, leaving significant upside potential.

Technology and sustainability leadership

VBL is leveraging digital tools to boost efficiency, targeting 90–95% digital workflow coverage with over 1,000 scanners deployed each year. On sustainability, the company has earned CDP A- ratings for water and climate, is expanding renewable energy use, and is building circular economy initiatives. Internationally, backward integration projects are helping reduce costs and improve margins.

Final assessment

Varun Beverages Limited stands out as a long-term investment opportunity, positioned at the intersection of India’s consumption growth and global beverage industry leadership. Its strong partnership with PepsiCo, operational efficiency, and strategic market positioning create high barriers to entry while allowing the company to benefit from India’s demographic dividend.

Key investment highlights

- Market leadership: India’s largest beverage bottler with an exclusive PepsiCo franchise

- Financial strength: Consistent improvement in profitability with strong return metrics (ROE 22.5%, ROCE 24.8%)

- Growth runway: Current plant utilization at 70% leaves significant room for volume expansion, supported by low market penetration

- Defensive moat: Strong brand partnerships and an extensive distribution network provide a sustainable competitive edge

- Balance sheet: Debt-free position gives flexibility for strategic investments

Risk Considerations

- Competitive intensity: New entrants, such as Reliance’s Campa Cola, could create pricing pressure

- Weather sensitivity: Seasonal fluctuations can affect short-term volumes

- Valuation premium: The stock’s high P/E multiple requires continued execution of growth plans

- Market maturation: Slowing category growth over the long term may temper returns

If growth targets are met. With management guiding 20–25% revenue growth, expanding its international footprint, and tapping into India’s still underpenetrated beverage market, Varun Beverages is well-positioned to benefit from the structural shift toward packaged drinks and maintain its leadership in the Indian beverage sector.

Turn research into action and explore smarter investing opportunities with CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.