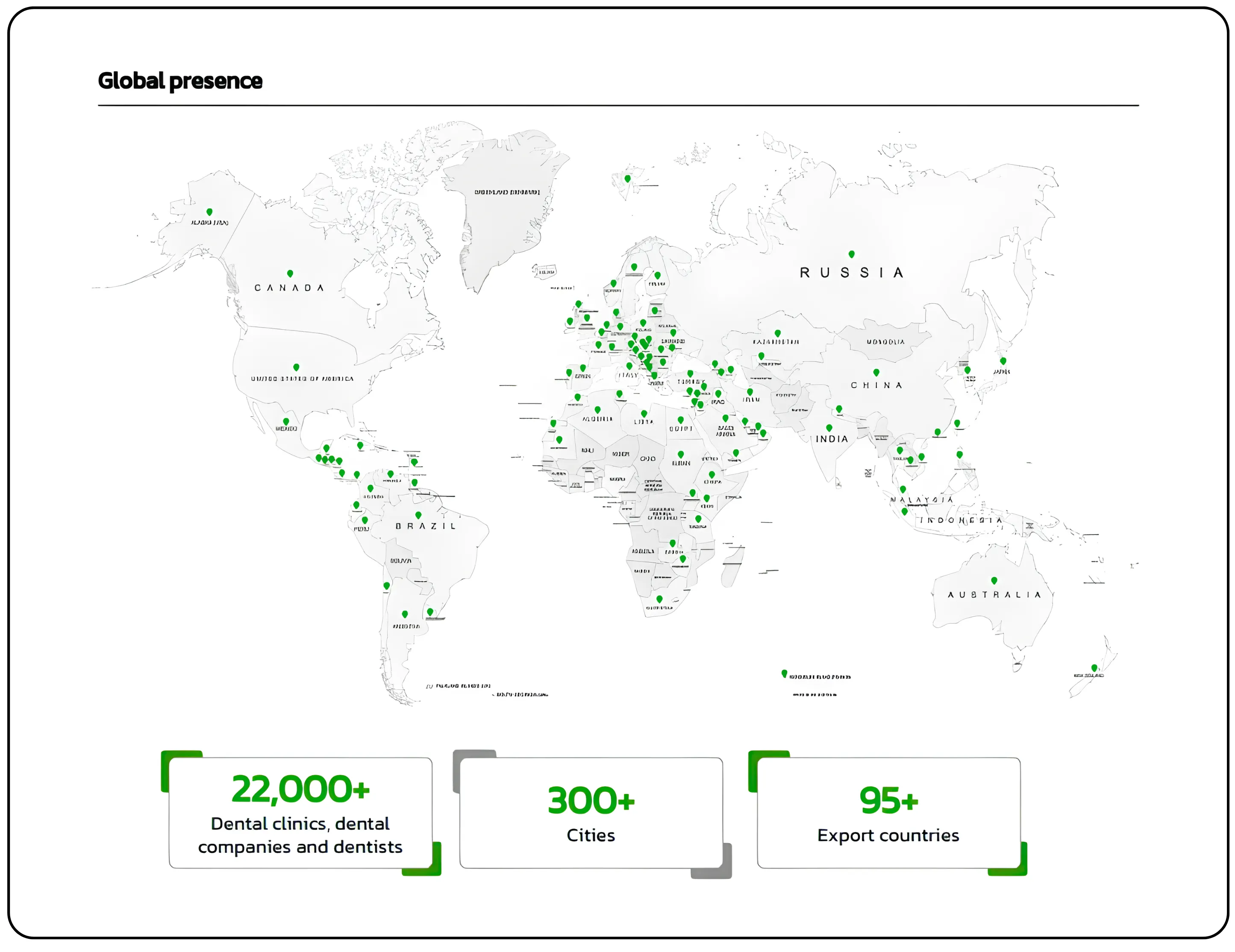

Think of Laxmi Dental as a one-stop shop for everything a dentist might need in India and around the world. Since starting in 2004, Laxmi Dental has grown from just exporting dental goods to becoming India's only full-service dental company. Today, they handle everything from manufacturing dental chairs and instruments to operating labs that specialize in the latest advancements like digital dentistry, clear aligners, pediatric care, and lab automation. Today, they serve over 22,000 dental clinics and dentists across more than 300 Indian cities and 95+ countries. Basically, if a dentist needs a product, whether it's a simple filling material or a complex piece of equipment, Laxmi Dental is likely the company they turn to. Laxmi Dental has grown from just exporting dental goods to becoming India’s only Integrated Dental Company, leading the shift toward Digital Dentistry amid strong Healthcare Growth in India

Business model and vertical integration (End-to-end integration)

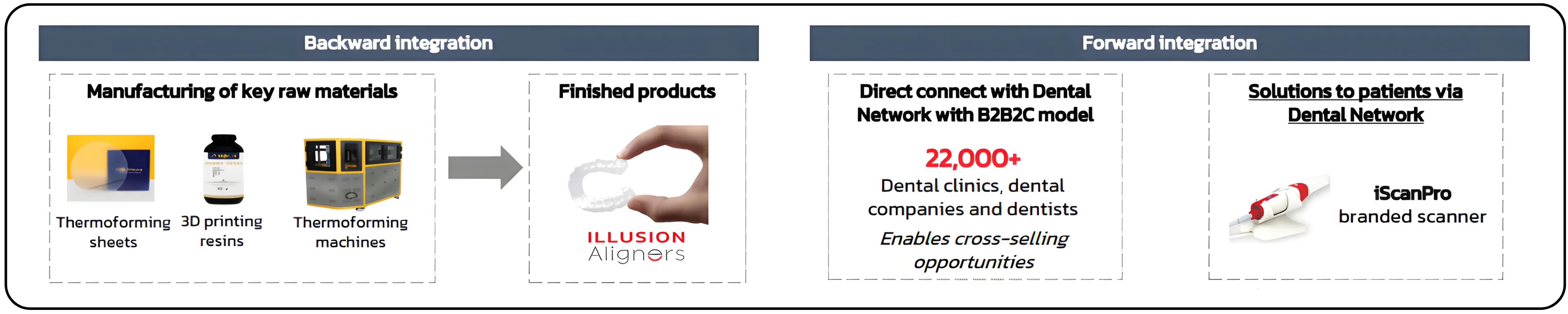

Laxmi Dental has built a one-of-a-kind vertical integration model, meaning they handle every step, from the raw material to the final, personalized solution.

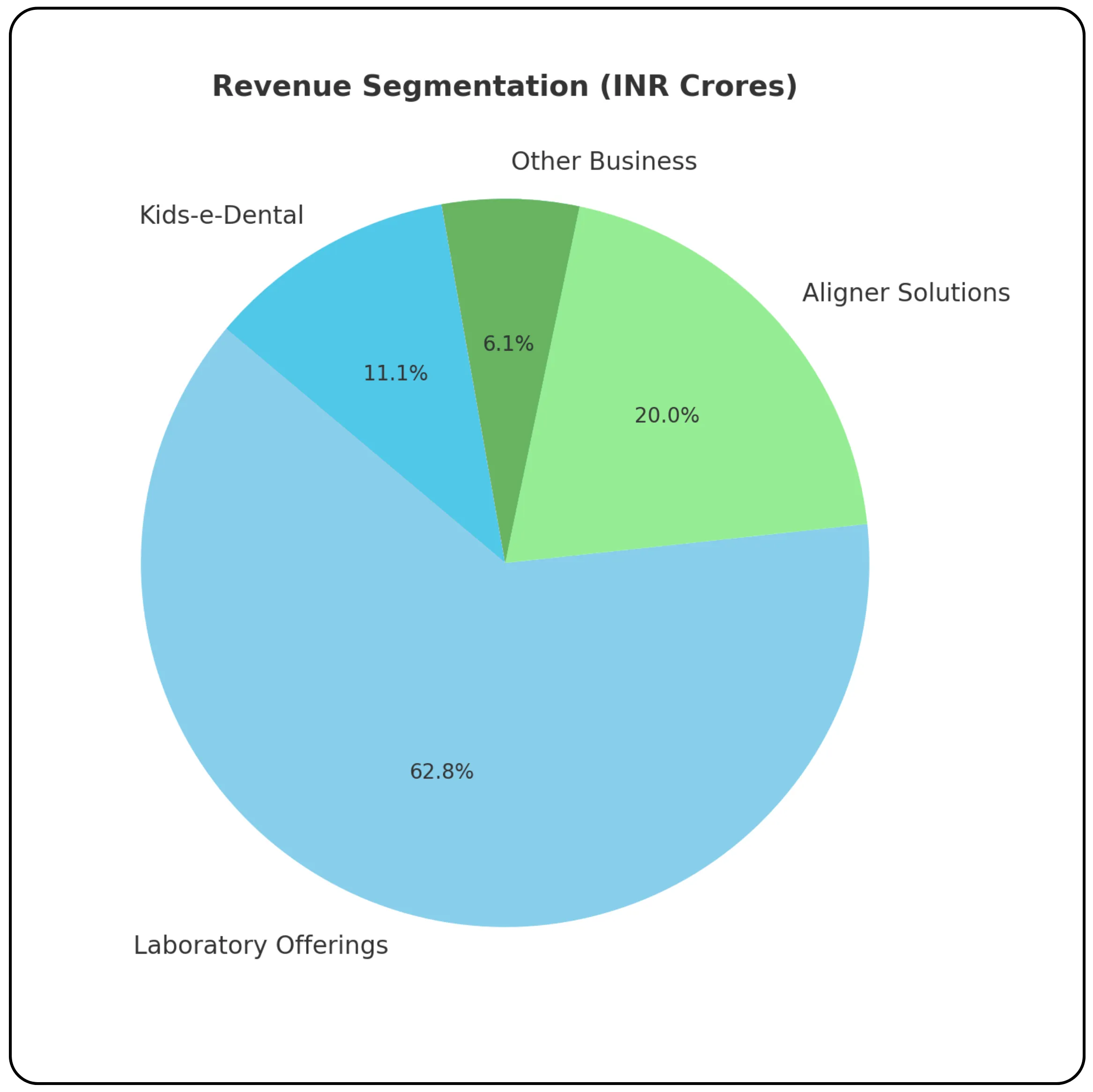

Laboratory offerings (62.8% of revenue)

Contributing ₹148.78 Cr, this segment focuses on creating fully customized dental prosthetics, including crowns, bridges, and restorative solutions. Operating through dual markets, domestic (36% of total revenue) and exports (25% of total revenue). In recent years, it has successfully shifted toward premium metal-free products. For example, zirconia-based crowns now represent 55% of domestic laboratory business, up from 48% in FY22. Branded product contribution has grown from 18% in FY22 to 40% in H1FY25, driving improved margins through the premium "Illusion Zirconia" brand.

Aligner solutions (20% of revenue) - Aligner market penetration

Generating ₹47.41 Cr, this fast-growing segment operates through "Illusion Aligners," the first Indian clear aligner with US FDA 510(k) clearance. The segment combines Bizdent Devices (responsible for final product delivery) and Vedia Solutions (focused on manufacturing and backward integration). With India's malocclusion prevalence at 75% but only 0.1% orthodontic treatment adoption versus 3% in the US, the segment projects 39% CAGR growth from FY25E-28E.

- Bizdent Devices: Focuses on the final product, delivering 100% customized, clear aligners to dentists based on patient-specific prescriptions.

- Vedia Solutions handles advanced manufacturing and backward integration, producing essential components such as thermoforming sheets, 3D printing resins, and dental-grade machinery.

Kids-e-Dental (11.1% of revenue)

Through its 60% stake in Kids-e-Dental LLP, this segment contributes ₹26.27 Cr, offering a range of pediatric dental solutions, including pre-formed pediatric crowns, Silver Diamine Fluoride, space maintainers, and fissure sealants. The global pediatric dental crowns market is expected to reach $3.5 billion by 2030 with a 23% CAGR, supported by India's young demographic profile.

Other business (6.06% of revenue)

This segment contributes ₹14.38 Cr and includes dental instruments, consumables, and emerging digital solutions, providing diversification and comprehensive customer solutions.

Financial performance

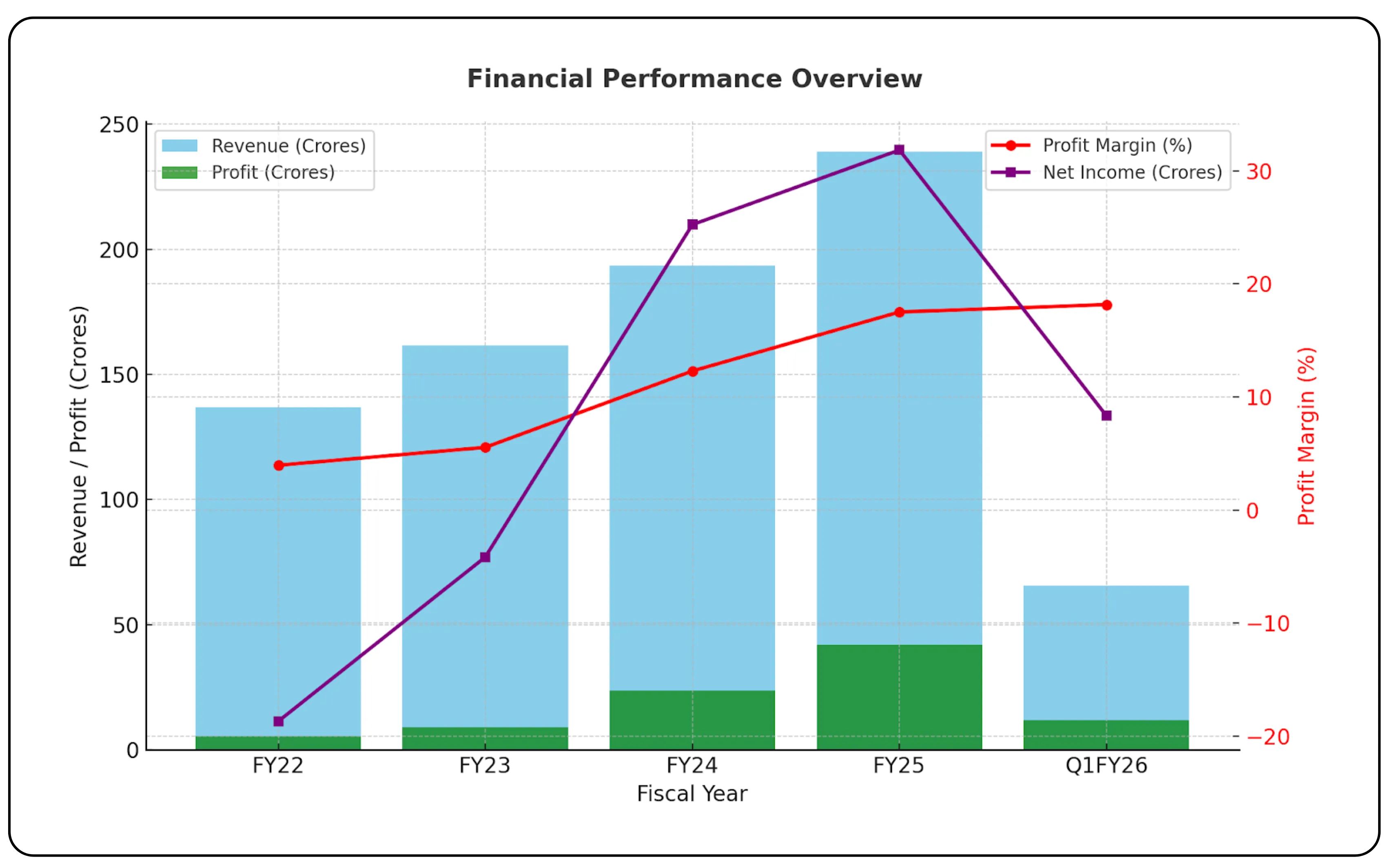

Laxmi Dental achieved a revenue CAGR of 21.6% from FY23 to FY25, with revenues growing from ₹161.63 Cr to ₹239.11 Cr. Also, EBITDA grew at 116.2% CAGR during the same period.

| Fiscal Year | Revenue (Crores) | Profit (Crores) | Profit Margin (%) | Net Income (Crores) |

|---|---|---|---|---|

| FY22 | 136.84 | 5.42 | 3.96% | -18.68 |

| FY23 | 161.63 | 8.96 | 5.54% | -4.16 |

| FY24 | 193.56 | 23.79 | 12.29% | 25.23 |

| FY25 | 239.11 | 41.87 | 17.51% | 31.83 |

| Q1FY26 | 65.6 | 11.91 | 18.16% | 8.33 |

| Segment | Revenue (INR Crores) | Percentage |

|---|---|---|

| Laboratory Offerings | 148.78 | 62.20% |

| Aligner Solutions | 47.41 | 19.80% |

| Other Business | 14.38 | 6.00% |

| Kids-e-Dental | 26.27 | 11.00% |

Profitability transformation

After recording losses of ₹18.68 Cr in FY22 and ₹4.16 Cr in FY23, Laxmi Dental achieved a profit turnaround with PAT of ₹252.3 million in FY24 and ₹318.3 million in FY25. EBITDA margins expanded significantly from 5.5% in FY23 to 17.5% in FY25, while PAT margins improved from -2.5% to 13.3%.

The company maintained strong momentum in Q1 FY26 with revenue of ₹656 million, representing 10% year-over-year growth while maintaining healthy EBITDA margins of 18.2%.

For insights into how healthcare distribution is evolving and the role of key players, explore our analysis: Entero Healthcare Solutions and the Transformation of Healthcare Distribution.

Capacity expansion

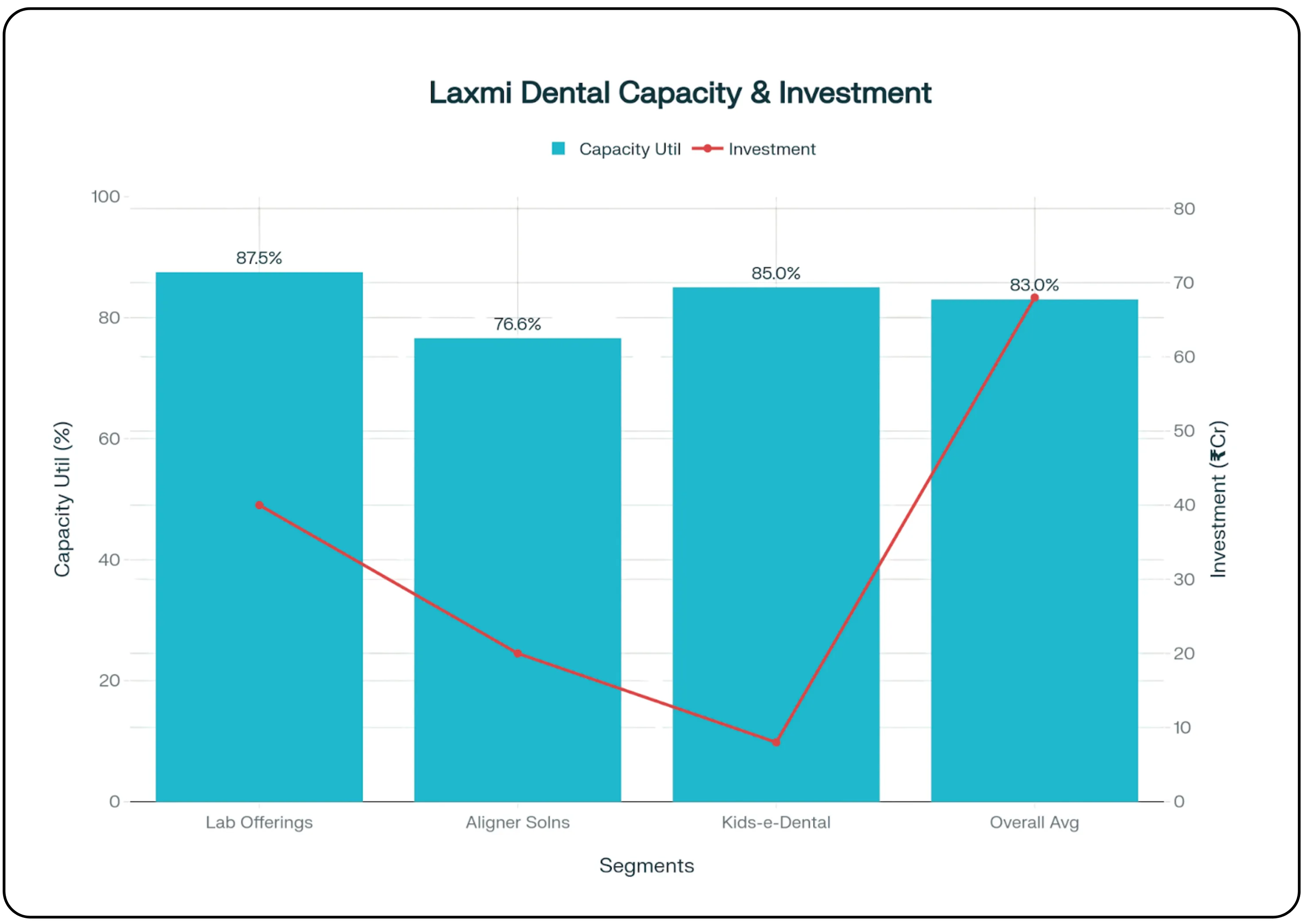

Laxmi Dental operates six manufacturing facilities spread across 147,029 square feet in Maharashtra and Kerala, plus five supporting facilities across India. The Boisar facilities adhere to US FDA quality regulations, while the Mira Road and Boisar sites are ISO 13485:2016 certified. Current capacity utilization stands at reasonable levels with plans for additional machinery investments totaling ₹68 crores funded by IPO proceeds. Within this, the Laboratory Offerings segment operates at 87.5% capacity utilization, while Aligner Solutions maintains 76.6% utilization.

Dental industry potential

Macroeconomic foundation for growth

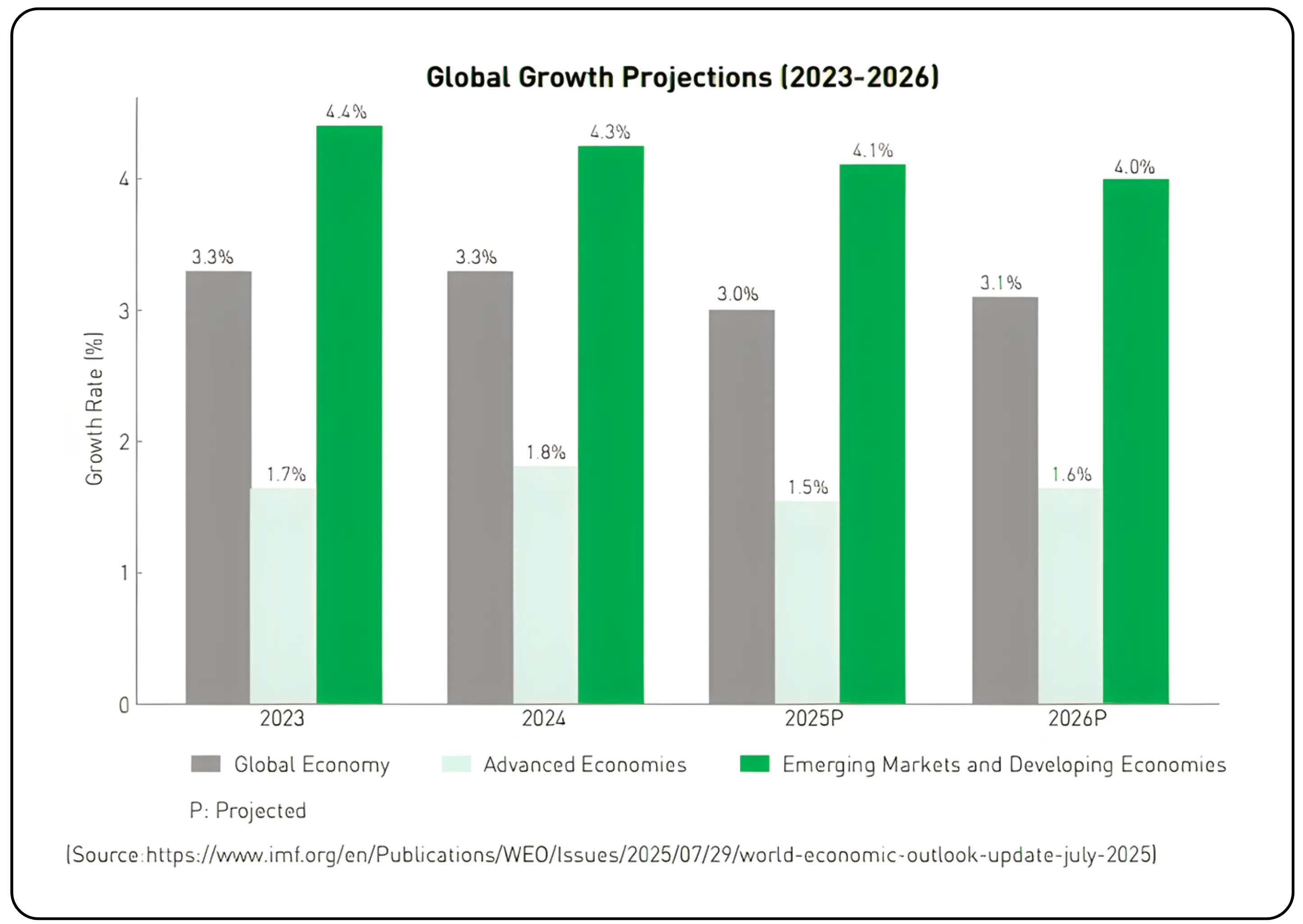

Global economic growth is expected to stay steady at 3.3% in 2024 and 3% through 2026, with emerging markets outpacing advanced economies. India leads this trend with projected GDP growth of 6.5% in 2025, driven by strong domestic demand and a rising PFCE at 7.3%. This sustained growth underpins higher healthcare and dental care spending.

Healthcare sector boom

India’s healthcare market has grown at a 22% CAGR since 2016, expanding from ₹9.13 lakh crores to a projected ₹52.79 lakh crores by 2025. This surge reflects the country’s demographic shift and rising income levels, key tailwinds for Laxmi Dental.

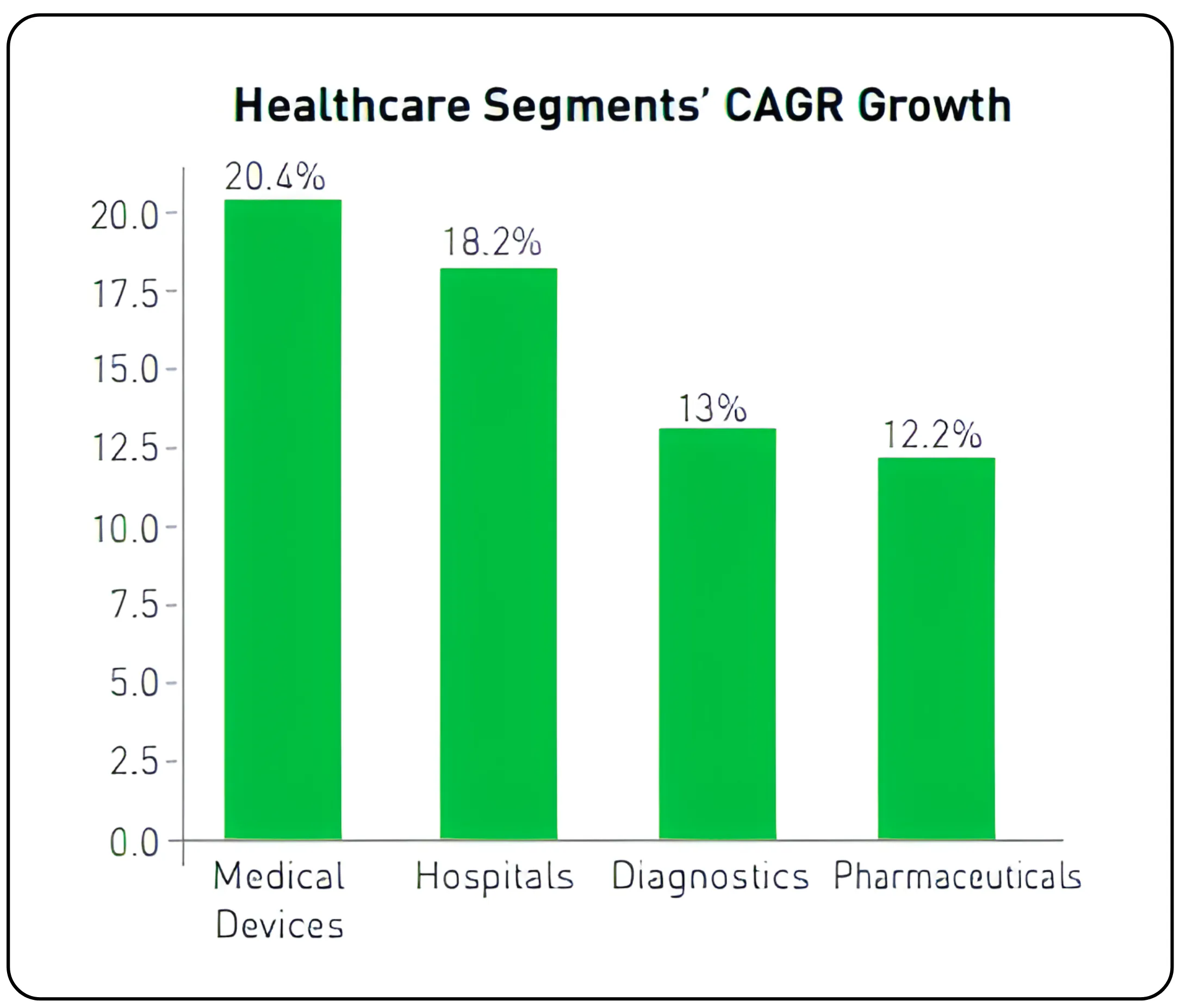

Medical devices are the fastest-growing healthcare segment, set to rise from ₹1,27,820 crores in 2022 to ₹4,15,000 crores by 2030 at a CAGR of 20.4%. Dental devices, a significant part of this segment, benefit from digital imaging, diagnostics, and government support through Make in India and PLI schemes.

Dental care market

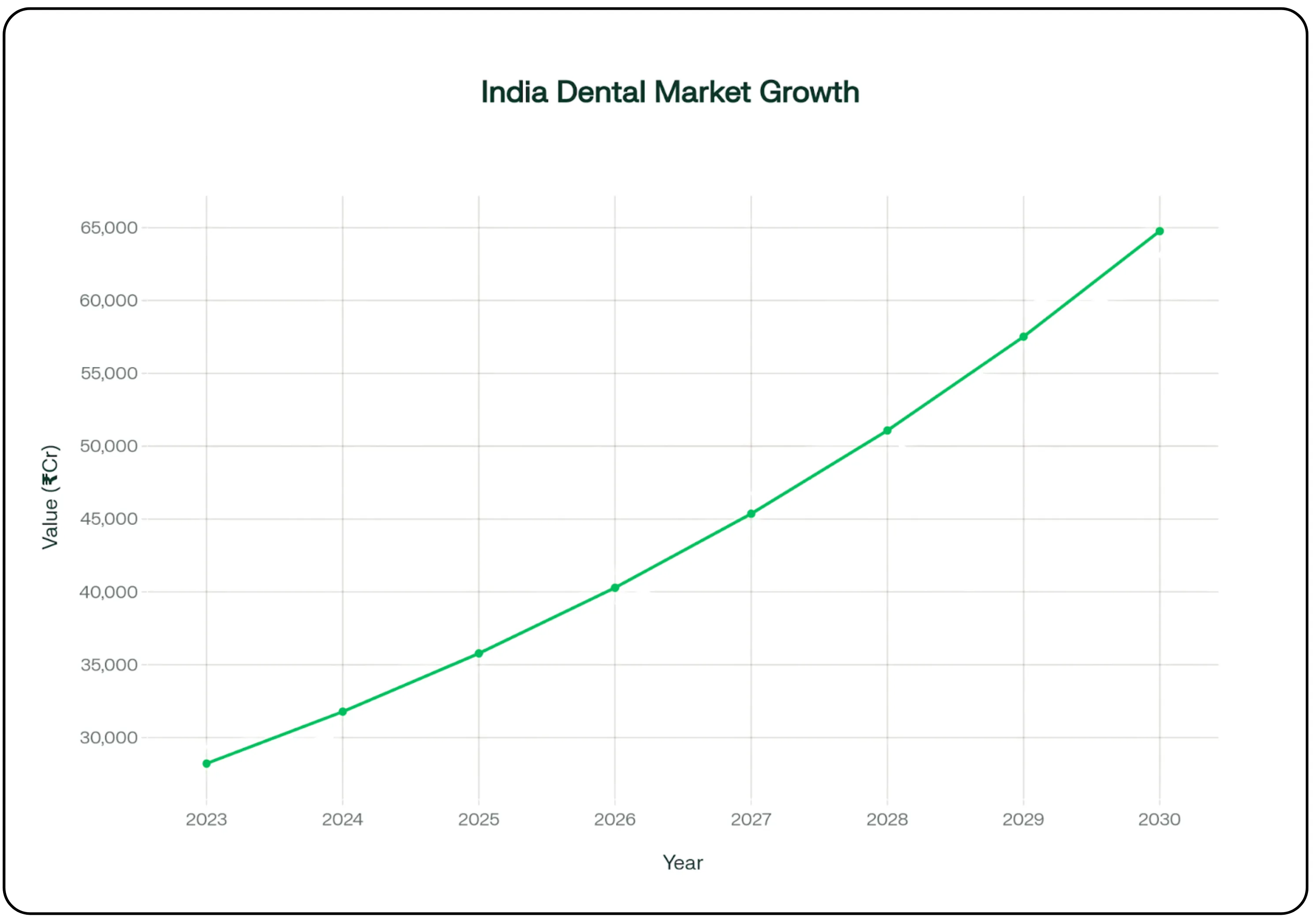

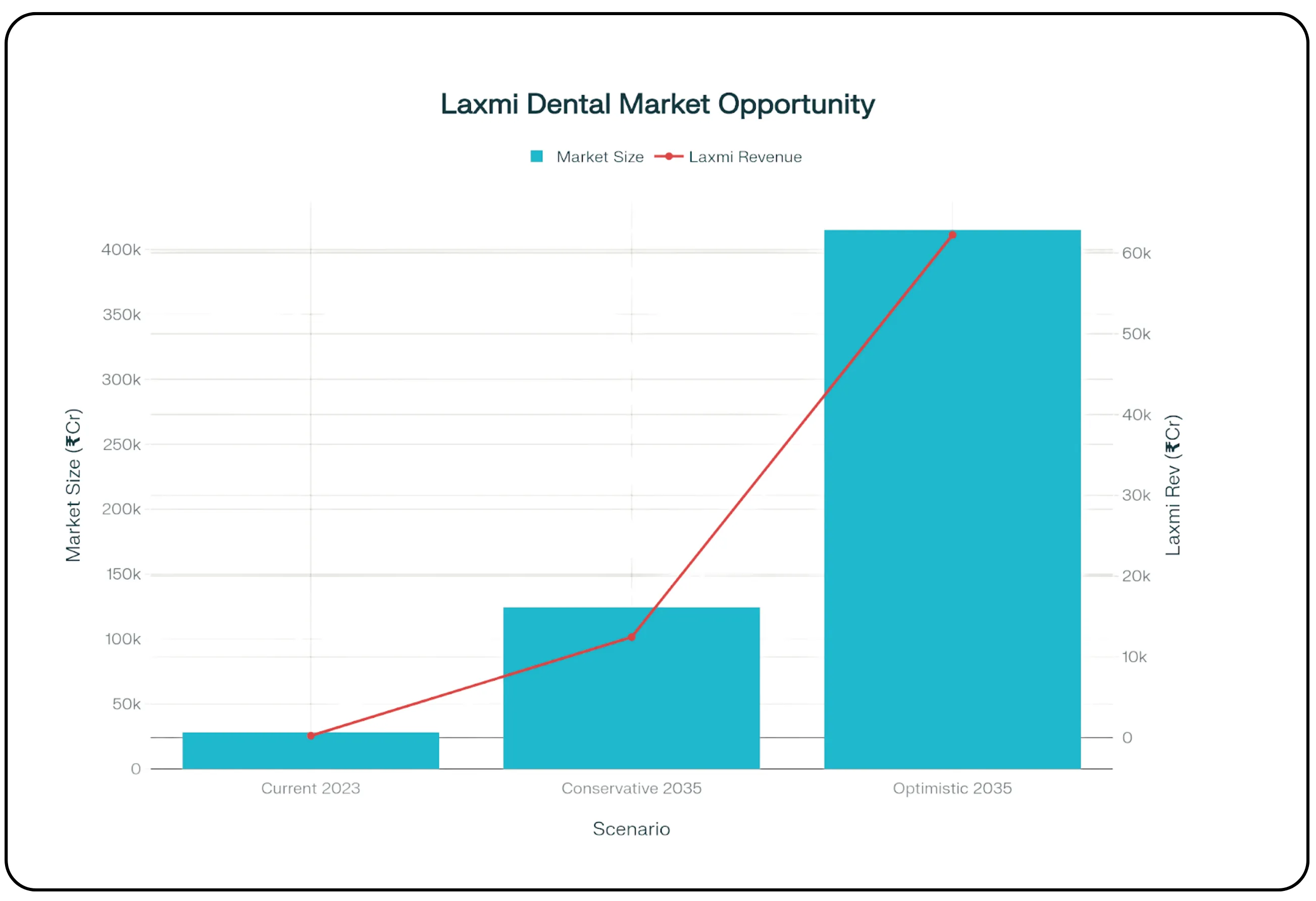

The Indian dental care market, worth ₹28,220 crores in 2023, is projected to reach ₹64,740 crores by 2030 at a 12.6% CAGR. Key growth drivers include an aging population (65+ rising to 20.8% by 2050), increasing oral disease prevalence, and heightened demand for aesthetic and restorative treatments.

Massive underpenetration

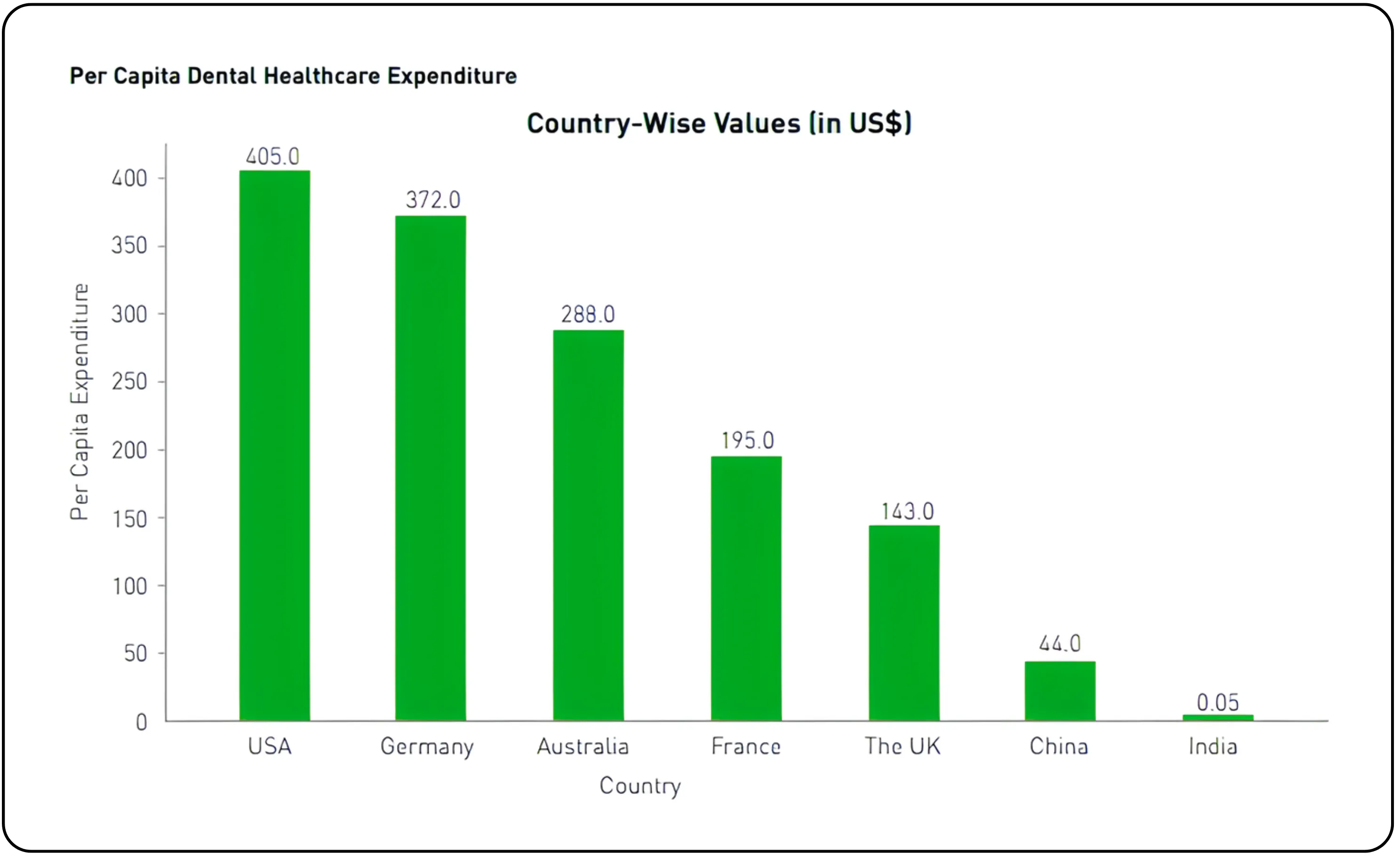

India’s per capita dental spending stands at just $0.05 versus $405 in the US and $44 in China. Bridging even part of this gap could unlock a market worth over ₹33 lakh crores as awareness and access to dental care continue to improve across the country.

For a deeper understanding of the broader healthcare landscape and growth dynamics, don’t miss our detailed analysis: A Comprehensive Industry Analysis of India’s Hospital Sector.

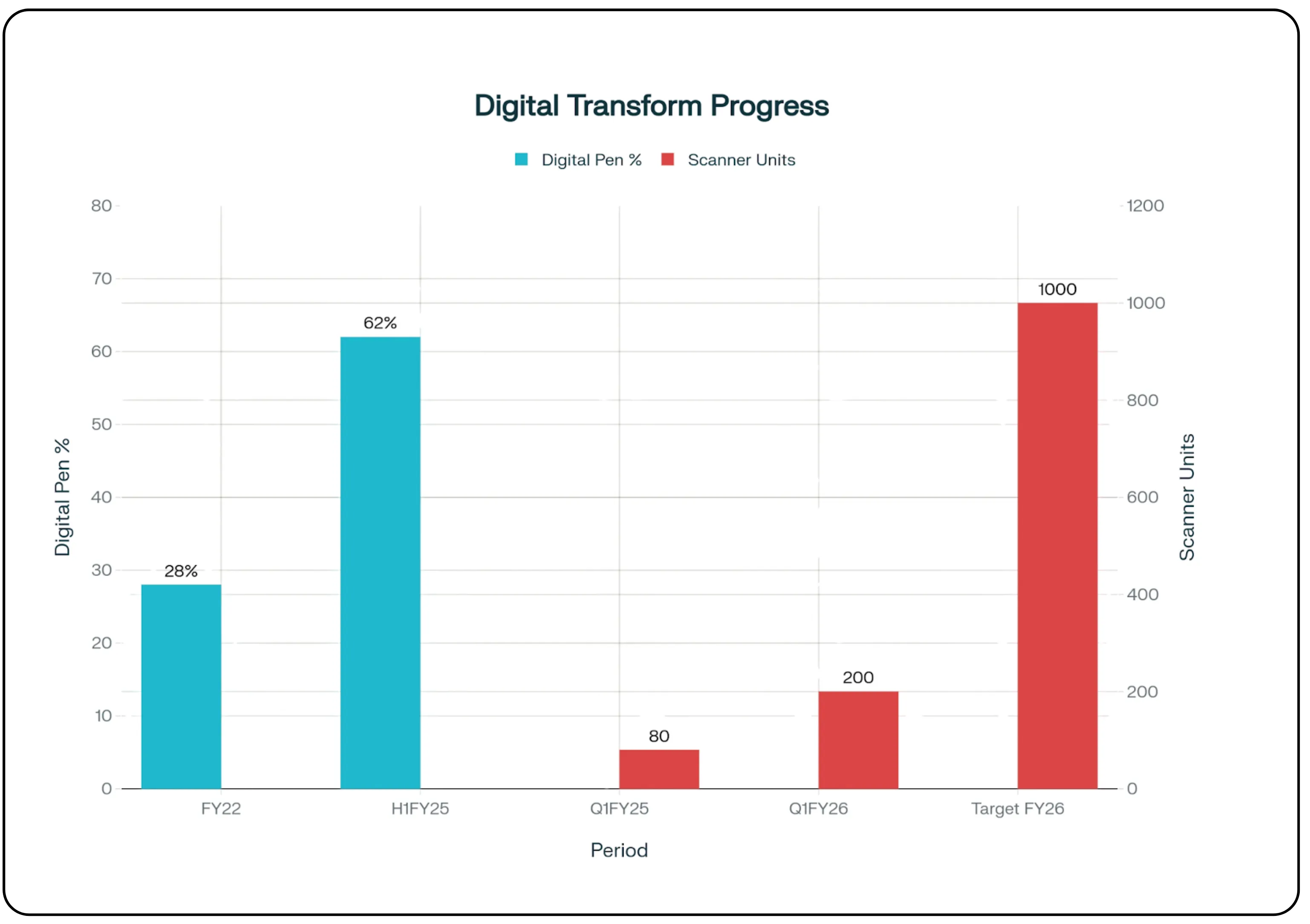

Digital transformation and export growth

The dental lab industry is undergoing rapid digital transformation, with technologies like CBCT, intraoral scanners, CAD/CAM, and 3D printing becoming mainstream. These innovations are helping labs reduce costs while improving precision and quality. At the same time, India is also emerging as a hub for outsourced dental lab services, with exports of artificial teeth and fittings growing at a 14% CAGR from 2018–2023.

Laxmi Dental’s strategic positioning

Laxmi Dental operates across 300+ Indian cities and 95+ countries, serving a network of 22,000 dental professionals. Its focus on digital workflows (targeting 90–95% efficiency with 1,000 scanners annually) and strong regulatory compliance (US FDA, ISO) strengthens both domestic leadership and export prospects.

Competitive positioning and strategic advantages

Market leadership and integration benefits

Laxmi Dental's position as India's only end-to-end integrated dental products company provides multiple competitive advantages. The company is approximately 5 times larger than the third-largest domestic player, yet maintains a modest market share, indicating significant expansion potential.

The company’s vertically integrated business model enables significant control over raw material sourcing and production processes, providing cost efficiency, quality control, and supply chain reliability that fragmented competitors cannot match.

Network effects and barriers to entry

The company's extensive network of 22,000+ dental professionals creates substantial network effects and barriers to entry. In the fragmented Indian dental laboratory market with approximately 300,000 dentists, Laxmi covers only 7% nationally (but 30% in western India), indicating significant expansion opportunities.

Risk factors and growth strategy

Market and regulatory risks

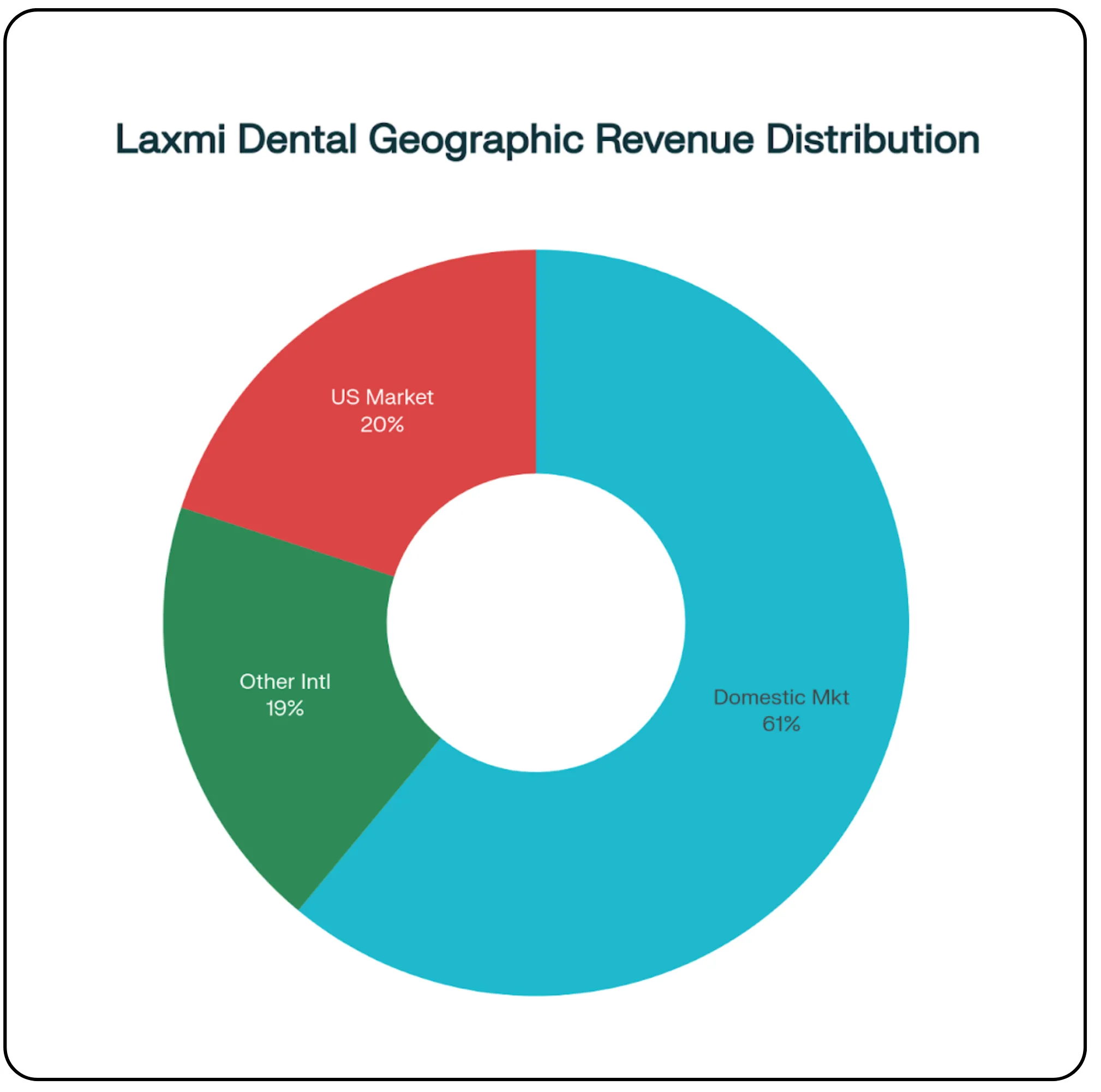

With 20% of its revenue coming from the US, Laxmi Dental faces potential risks from tariff changes. However, management expects to pass through most of these impacts by passing on cost increases to customers. Competition in the aligner segment from established players like Invisalign (68-70% market share) presents challenges, though the company's B2B2C model provides differentiation opportunities.

Strategic investment priorities

Management has guided FY26 revenue growth of 20-25% with sequential quarterly growth of 8-10%. To achieve this, the company plans to invest ₹68 crores from IPO proceeds in new machinery and capacity expansion. Geographic expansion, focusing on South India and international markets targeting Europe, APAC, and the Middle East, will reduce single-geography dependence. At the same time, brand-building initiatives, including celebrity endorsements (e.g., Kareena Kapoor for Illusion Aligners) and premium product positioning, will enhance market recognition and pricing power.

Curious how CDMO trends are fueling global growth? Check out: Senores Pharma Capitalizing on CDMO Tailwinds for Global Ascent.

Investment thesis and forward PE-based valuation

Laxmi Dental demonstrated exceptional growth characteristics with a revenue CAGR of 21.6% and an EBITDA growing at a remarkable CAGR of 116.2% from FY23-FY25. The company's transformation from losses to strong profitability (13.3% PAT margin in FY25) showcases strong execution capabilities. Return metrics remain attractive with ROE of 15.3% demonstrating efficient capital allocation.

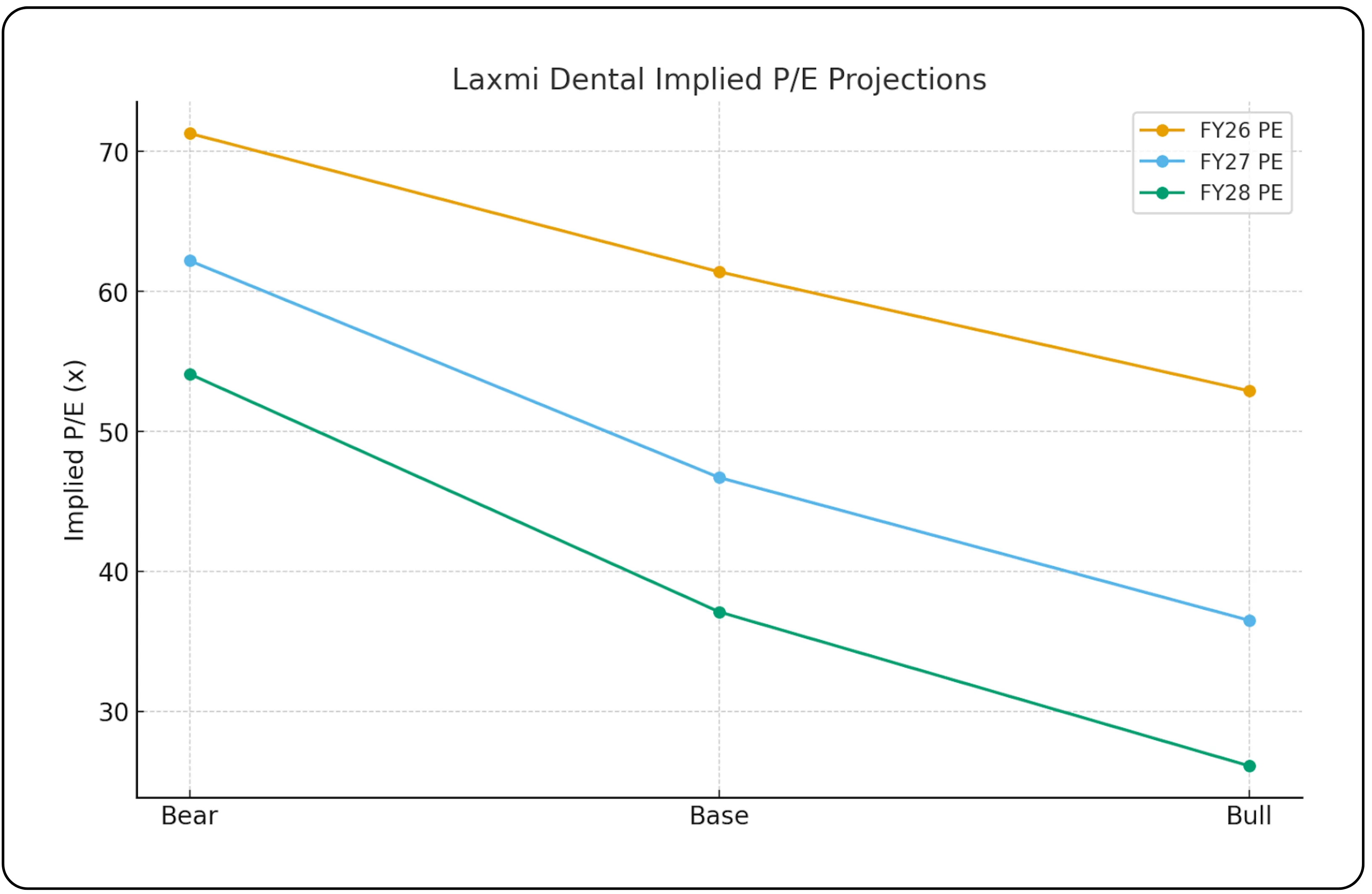

The following table presents scenario-based financial projections for Laxmi Dental, built on FY25 TTM as the base year. It illustrates how revenue, profitability, and valuations could evolve under Bear, Base, and Bull assumptions.

| Scenario | Year | Revenue (Cr) | PAT (Cr) | PAT Margin | EPS (₹) | Implied Fwd P/E |

|---|---|---|---|---|---|---|

| Bear | 2026 | 281.75 | 25.36 | 9.0% | 4.63 | 71.4 |

| Bear | 2027 | 324.01 | 29.16 | 9.0% | 5.33 | 61.9 |

| Bear | 2028 | 372.61 | 33.53 | 9.0% | 6.13 | 53.8 |

| Base | 2026 | 294.00 | 29.40 | 10.0% | 5.36 | 61.6 |

| Base | 2027 | 352.80 | 38.81 | 11.0% | 7.08 | 46.6 |

| Base | 2028 | 423.36 | 48.69 | 11.5% | 8.89 | 37.1 |

| Bull | 2026 | 306.25 | 35.22 | 11.5% | 6.42 | 51.4 |

| Bull | 2027 | 382.81 | 49.77 | 13.0% | 9.07 | 36.4 |

| Bull | 2028 | 478.52 | 69.38 | 14.5% | 12.65 | 26.1 |

Projection Methodology and Assumptions

The financial projection table for Laxmi Dental has been constructed using the company’s FY25 trailing twelve months (TTM) performance as the base year, with Revenue of ₹245 Cr, PAT of ₹23.1 Cr, and an EPS of ₹5.36.

Revenue Growth (CAGR 15–25%): Revenue has been projected under three scenarios: Bear (15%), Base (20%), and Bull (25%). These ranges are consistent with the broader medical devices and dental consumables industry, where companies typically report high-teen to mid-20% growth depending on new product launches, exports, and distribution expansion.

Profitability (PAT Margins): The company reported a PAT margin of around 9.4% in FY25 (TTM). Under the Bear scenario, margins are assumed to remain flat at 9%. In the Base scenario, gradual margin expansion to around 11.5% is considered, reflecting operating leverage. The Bull scenario factors in stronger efficiency gains, with margins improving toward 14.5% by FY28.

Valuation Multiples (Forward P/E): While the stock currently trades at a high P/E multiple of about 78× TTM, the projection uses more moderate valuation bands. The Bear scenario applies 25–30×, the Base scenario applies 30–40×, and the Bull scenario applies 40–50×. These ranges reflect potential market re-rating based on earnings visibility and sector growth.

EPS Calculation: EPS projections are derived from PAT estimates, adjusted for the 5.48 Cr share base. This allows for implied valuation ranges to be calculated under each scenario.

Interpretation

This scenario analysis is not a forecast, but rather a sensitivity framework to understand how Laxmi Dental’s financial performance could evolve under different growth and margin trajectories. It highlights the potential earnings power of the business and the valuation ranges that the market may assign, depending on execution and industry conditions.

Market opportunity and positioning

The massive underpenetration of India's dental care market, combined with Laxmi Dental's unique integrated positioning and technology leadership, creates significant long-term value creation potential. With current coverage of only 7% of the country’s 300,000 dentists indicates substantial room for domestic expansion.

Final view

Laxmi Dental Limited represents a compelling investment opportunity as India's only fully integrated dental products company positioned at the intersection of healthcare growth and digital transformation. The company's exceptional financial turnaround, technology leadership, and strategic positioning in a large, underpenetrated market with significant growth runway make it an attractive long-term investment proposition.

The integrated business model, digital transformation strategy, expanding global footprint, and strong competitive positioning provide multiple drivers for sustained growth and market share expansion. With management guidance targeting 20-25% revenue growth for FY26 and strong underlying market dynamics, Laxmi Dental offers investors exposure to India's healthcare revolution and the global shift toward digital dentistry.

The combination of strong fundamentals, market leadership in a defensive healthcare segment, technology differentiation, and significant growth potential in an underpenetrated market makes Laxmi Dental a compelling long-term investment opportunity for investors seeking exposure to India's growing healthcare and dental care markets.

Turn research into action and explore smarter investing opportunities with CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.