India’s hospital sector, a critical part of the Indian healthcare industry, has emerged as one of the most important pillars of the country’s healthcare system. With the Indian healthcare market valued at ₹10.7 trillion in FY 2024, the industry is projected to grow significantly, reaching between ₹15.6 trillion and ₹16.3 trillion by FY 2028.

This strong growth trajectory is being shaped by a combination of economic progress, rising healthcare awareness, demographic transitions, and technological advancements. Private hospitals and major hospital chains such as Apollo Hospitals, Fortis Healthcare, and Max Healthcare play a decisive role in this expansion. They currently account for around 64% of total healthcare spending by value, a figure that is expected to climb to 69% by 2027.

Their ability to provide advanced treatment options, better infrastructure, and shorter waiting times has made private hospitals the preferred choice for a growing section of the population.

Economic Growth and Rising Healthcare Affordability

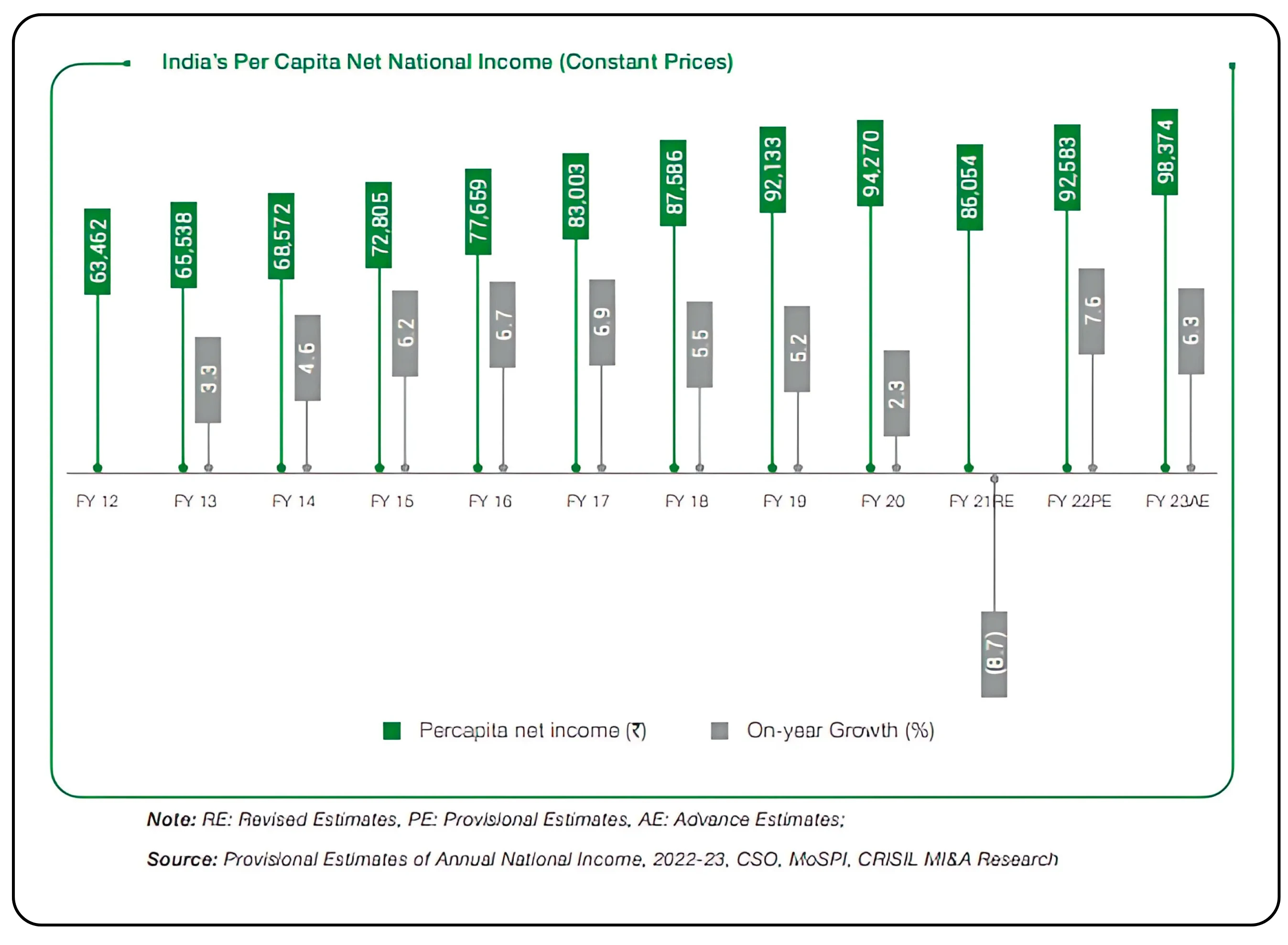

India’s macroeconomic stability provides the foundation for sustained growth in healthcare demand. The economy is expected to expand by 6.5 percent in FY 2025–26, a pace that supports rising household incomes. Per capita income has grown from ₹63,462 in FY 2012 to ₹98,374 in FY 2023, reflecting a compound annual growth rate of over 4%.

This rise in financial capacity has expanded the size of the middle class, which is increasingly prioritizing better medical care. Families that previously relied on government facilities or basic treatment now seek out private hospitals that offer specialized services and advanced technologies. As a result, healthcare spending is no longer limited to emergencies but is increasingly viewed as an essential part of quality of life.

Urbanization and the Healthcare Infrastructure Push

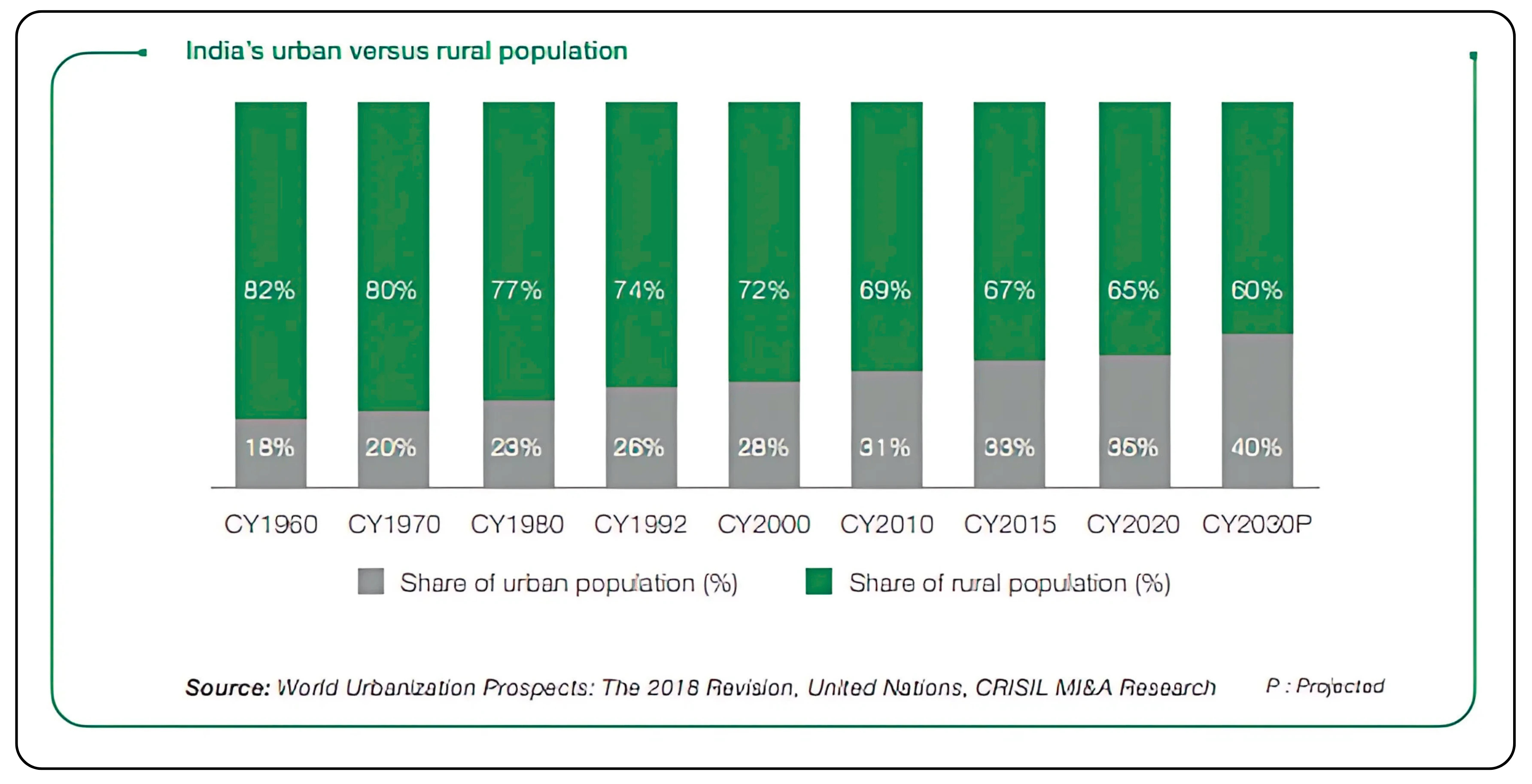

Urbanization is reshaping the geography of healthcare demand. By 2030, nearly 40% of India’s population is expected to live in urban areas. This concentration of people creates demand hubs capable of supporting large hospital networks and specialized care centers.

Metropolitan cities have already seen strong investment from major hospital chains, which benefit from economies of scale by operating multiple facilities within a single city. At the same time, Tier II and Tier III cities are becoming focal points for expansion. These cities offer a combination of sizeable populations with improving economic conditions, but often lack adequate healthcare infrastructure. The opportunity to establish hospitals in these areas is significant, as patients are often forced to travel to metros for advanced treatment.

Healthcare Spending and Infrastructure Gaps

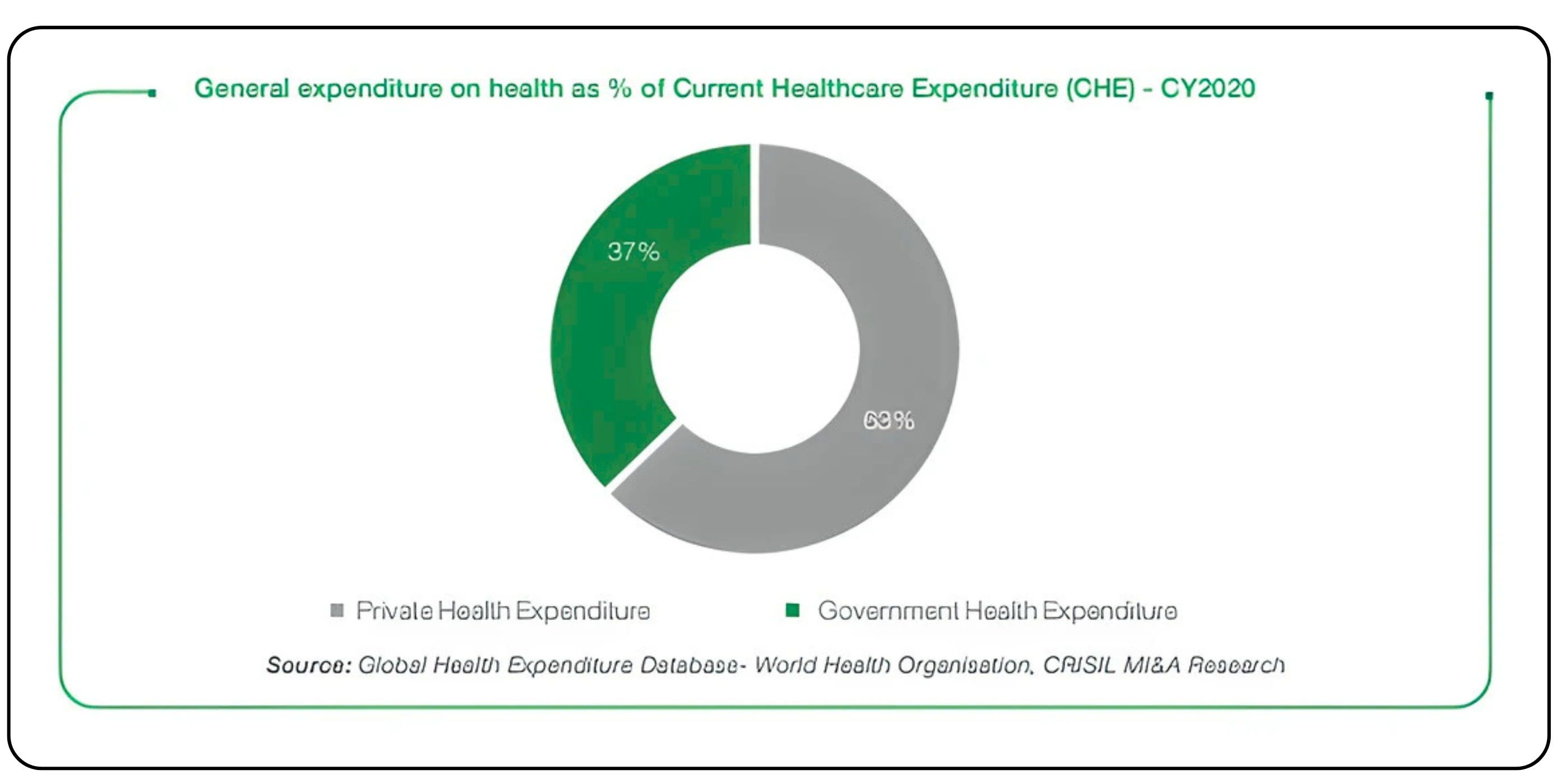

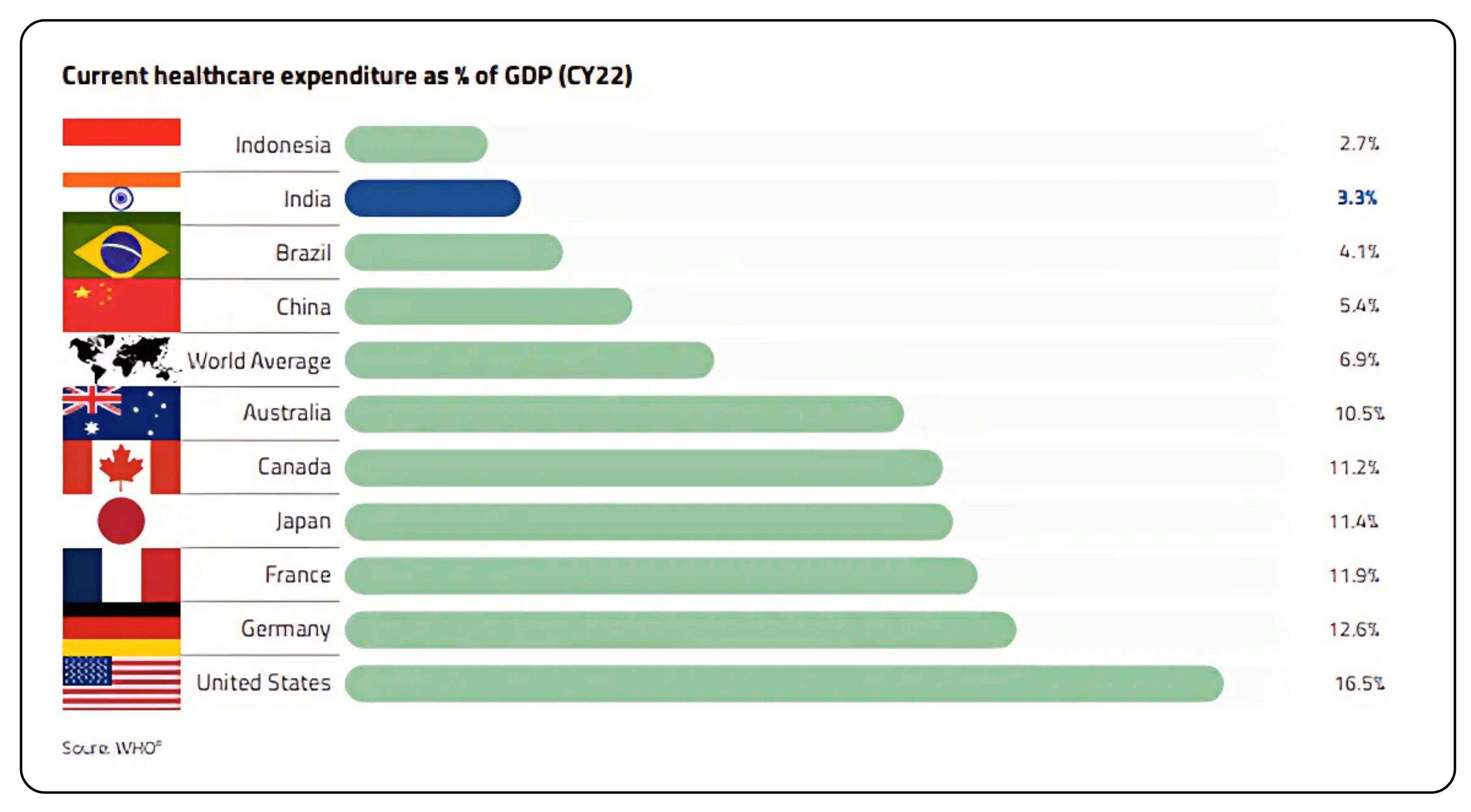

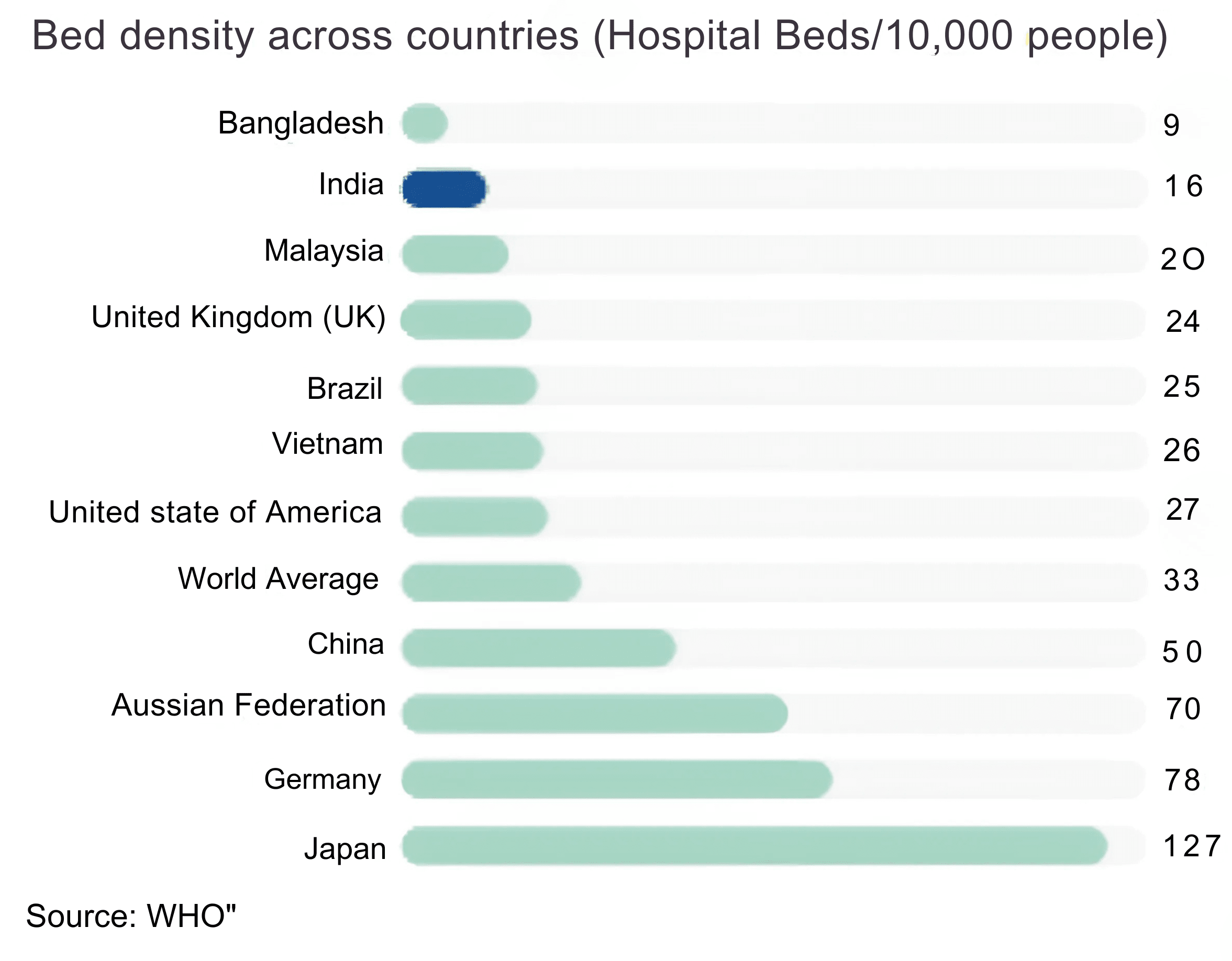

Despite these growth drivers, India’s healthcare spending remains relatively low at 3.3% of GDP, compared with over 10% in most developed economies. This underinvestment has resulted in infrastructure shortages. For instance, India has just 16 hospital beds per 10,000 people, well below the global average of 33.

Closing this gap will require both government support and private sector investment. Initiatives such as Ayushman Bharat and the National Health Policy aim to expand access to healthcare across the country. However, their success depends on collaboration with private hospital operators who have the capacity to deliver quality care at scale.

For a sharper view, explore our detailed fundamental analysis of the CDMO sector.

Private Hospitals as Engines of Innovation

Private hospitals are increasingly setting the benchmark for quality and innovation in India’s healthcare sector. Their share of treatments has risen steadily and is projected to reach nearly 69% by FY 2027. These facilities are more agile in adopting new technologies, expanding into underserved areas, and creating patient-focused care models.

Examples include the introduction of advanced platforms like the ZAP-X gyroscopic radiosurgery system for non-invasive brain tumor treatment and the use of AI-powered diagnostic tools. Investments in such technologies not only improve patient outcomes but also strengthen competitive positioning in an industry where reputation and trust are critical.

Shifting Disease Burden and New Demand Segments

Non-communicable diseases (NCDs) are medical conditions that cannot be transmitted from one person to another. They include a wide range of long-term illnesses such as cardiovascular disorders (coronary artery disease/heart attack, stroke, hypertension); chronic respiratory conditions (COPD, asthma); metabolic and endocrine conditions (type 1 and type 2 diabetes, obesity, dyslipidemia); chronic kidney disease; and chronic liver diseases (NAFLD, cirrhosis).

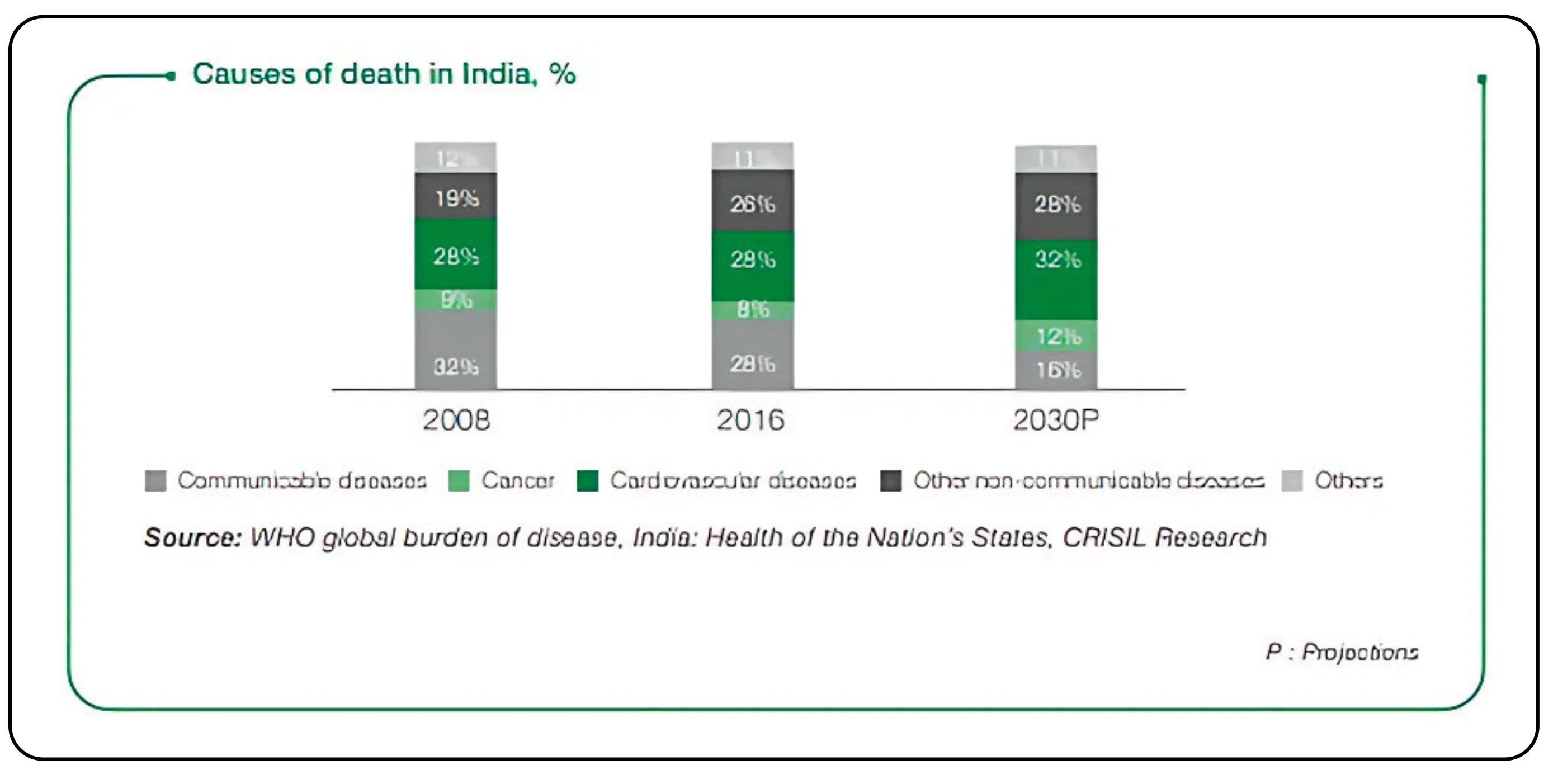

The rise of NCDs is transforming India’s healthcare demand profile. In 1990, NCDs accounted for around 30% of the disease burden. By 2016, their share had risen to 55%, and they now account for nearly 62% of all deaths. Projections indicate that by 2030, NCDs will be responsible for 84% of deaths in the country.

This trend has increased demand for specialized services in cardiology, oncology, diabetes care, and orthopedics. In response, hospitals are building Centers of Excellence, which combine advanced technology with highly trained specialists to deliver superior outcomes.

At the same time, preventive healthcare is emerging as a new growth area. Hospitals are launching health screening programs that allow early detection of chronic conditions, reducing long-term treatment costs and improving patient quality of life.

Technology and the Digital Shift

The COVID-19 pandemic significantly accelerated the adoption of digital healthcare in India. Telemedicine platforms, such as Apollo 24/7, have created entirely new channels for delivering care. By FY 2024, Apollo 24/7 had over 40 million registered users, with services ranging from online consultations to e-pharmacy delivery across 19,000 pincodes.

Digital platforms offer several advantages: they expand access to remote areas without requiring physical infrastructure, improve efficiency by reducing overhead costs, and provide patients with 24/7 convenience. Increasingly, hospitals are also integrating AI into diagnostics and treatment planning, improving accuracy and enabling more personalized care.

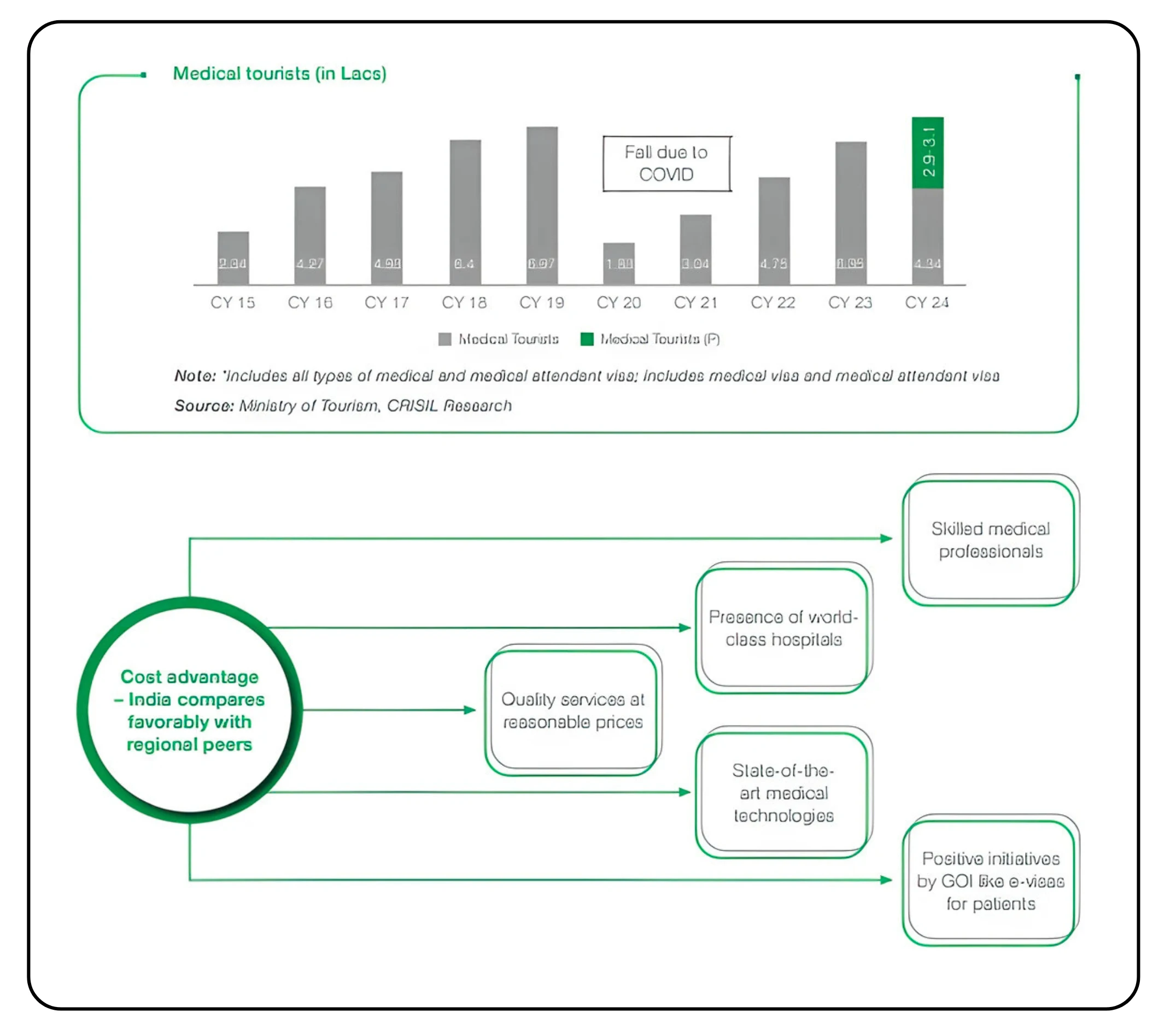

Medical Tourism: A Global Edge

Aster Medcity Kochi, Ernakulam

Aster Medcity Kochi, Ernakulam

India’s cost competitiveness has made it a preferred destination for medical tourism, with the Indian hospital sector increasingly attracting patients from abroad. Surgeries such as hip replacements, knee replacements, and cardiac bypasses are available at a fraction of the cost compared to the United States or Europe. For example, a heart bypass that might cost $144,000 in the US can be performed in India for a small fraction of that amount.

The medical tourism sector is expected to grow at around 15% annually, with nearly 7.3 lakh international patients projected to visit India in 2024. Government initiatives, including e-medical visas and the creation of the National Medical and Wellness Tourism Board, have further enhanced India’s standing as a global healthcare hub.

Also read: Our fundamental outlook on India’s port sector

Expanding Insurance Coverage

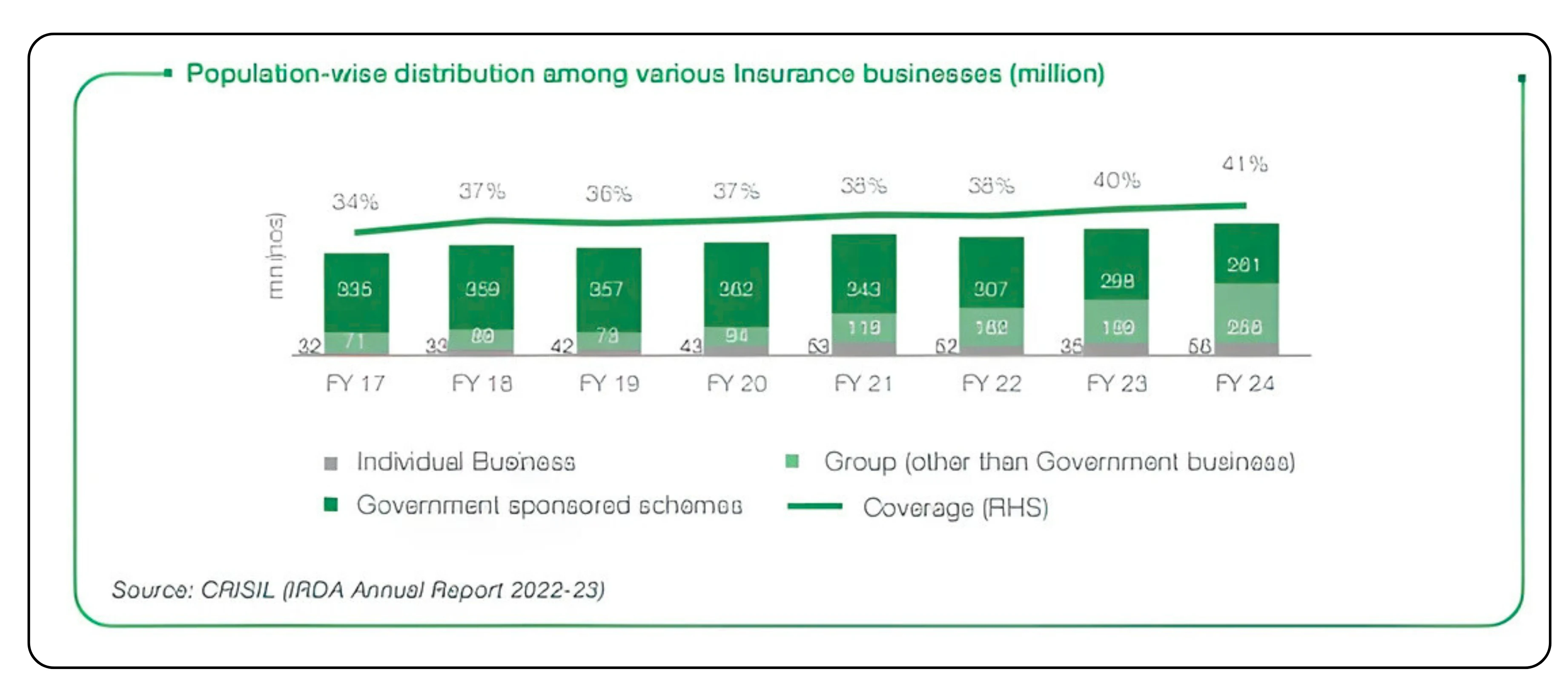

Health insurance penetration has grown significantly, with the number of insured individuals rising from 288 million in FY 2015 to 573 million in FY 2024. However, coverage still stands at just 41% of the population, leaving substantial room for further growth.

Greater health insurance coverage has multiple benefits: it makes healthcare more affordable for patients, encourages people to seek treatment earlier, and provides hospitals with greater payment security. Public schemes like Ayushman Bharat cater to low-income families, while private insurance is growing rapidly among the middle class. Both segments contribute to expanding the addressable market for hospitals and supporting the overall growth of the healthcare ecosystem.

New Growth Segments

Beyond traditional hospital care, new segments are creating additional growth avenues. Diagnostics is a rapidly expanding market, projected to reach up to ₹1,375 billion by FY 2028, supported by rising preventive testing and advanced diagnostic technologies.

Day-care and ambulatory services are also gaining importance, as patients increasingly prefer treatments that do not require overnight stays. For hospitals, this model improves asset utilization and allows more patients to be treated with the same infrastructure.

Key Challenges

While the healthcare sector’s growth potential is substantial, it also faces significant challenges.

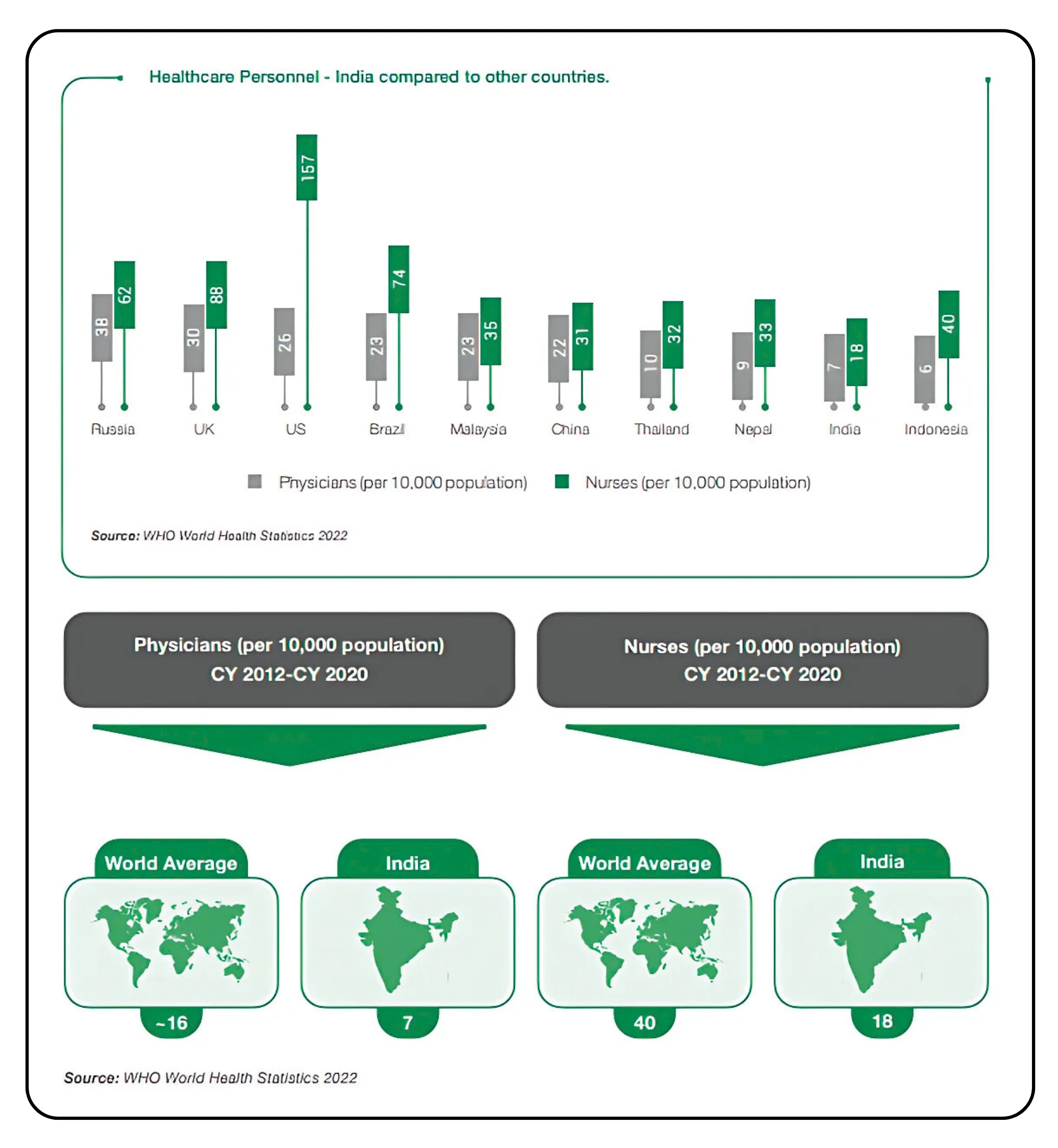

- Workforce shortages remain one of the most critical issues. India has only 20 healthcare professionals per 10,000 people, well below global standards. This shortage is particularly acute in rural areas.

- Regulatory complexity adds another layer of risk. Price caps on certain procedures, exclusion from GST credits, and heavy compliance requirements all affect margins.

- Competition pressures in urban markets require continuous upgrades in technology and service quality.

Hospitals must therefore invest in training, education, and retention programs to ensure they can meet rising demand.

Strategic Opportunities

Despite these challenges, the sector continues to offer opportunities:

- Expansion into Tier II and Tier III cities: Lower capital costs and less competitive environments create favorable conditions for growth.

- Omnichannel healthcare ecosystems: Integrating hospitals, diagnostic centers, pharmacies, and digital platforms enhances patient experiences and loyalty.

- Public-private partnerships (PPP): Collaboration with government agencies helps reach underserved populations while leveraging public funding.

Financial Performance and Investor Interest

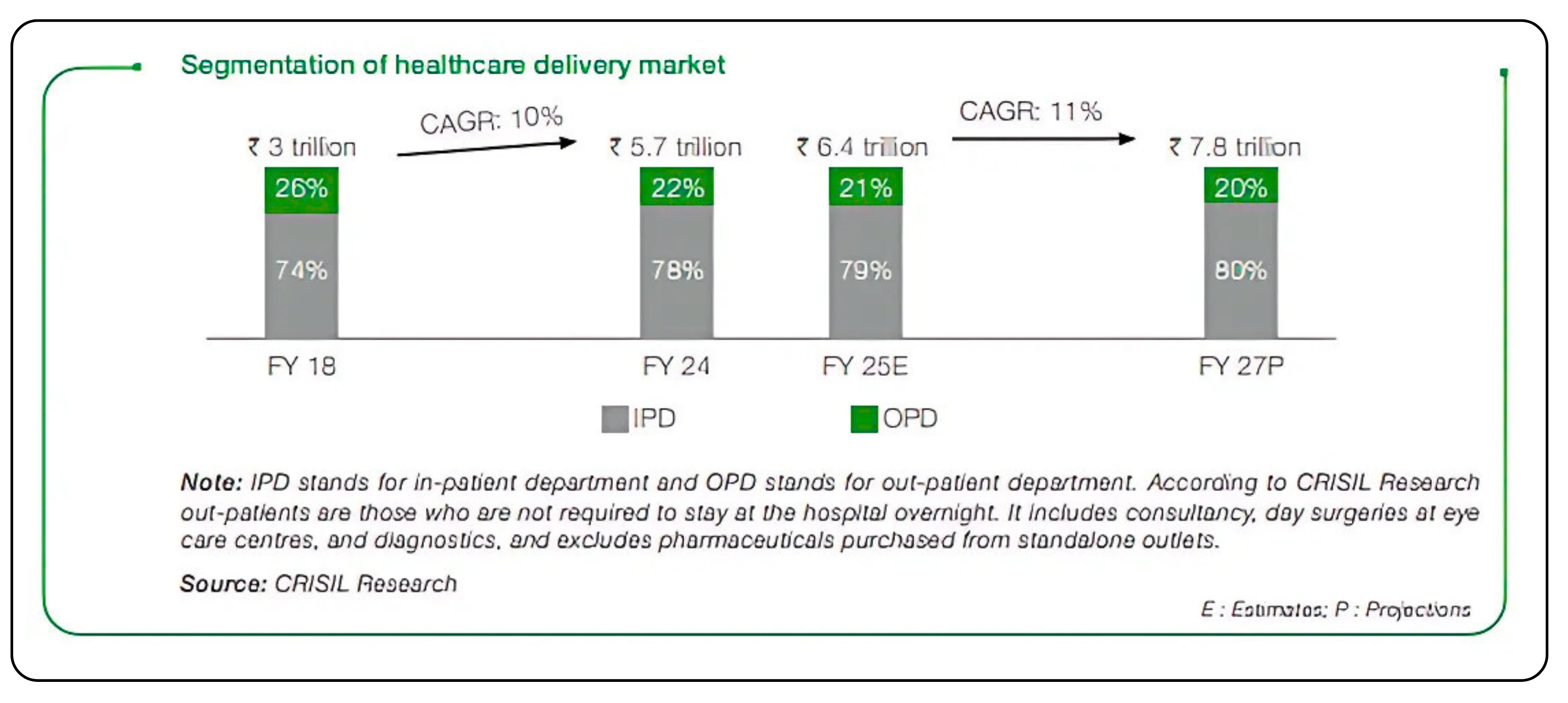

The healthcare delivery market is projected to grow at a CAGR of 9–11%, reaching around ₹7.8 trillion by FY 2027. Hospital operators with strong brands and efficient operations are expected to capture a significant share of this growth.

Investor confidence remains high, with private equity firms actively pursuing opportunities. Recent deals involving global funds such as GIC, KKR, and EQT underscore the sector’s long-term potential. Consolidation is also likely to accelerate, creating larger players with stronger financial and operational capabilities.

Outlook

India’s hospital sector stands at the intersection of economic growth, demographic change, and technological advancement. The rising burden of non-communicable diseases, increasing insurance coverage, and rapid digital adoption are reshaping demand in ways that create both challenges and opportunities.

For hospitals, long-term success will depend on their ability to maintain clinical excellence, expand strategically into new geographies, integrate digital solutions, and address workforce shortages. For investors, the sector offers the potential for strong financial returns alongside meaningful social impact, improving access to healthcare in the world’s most populous country.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.