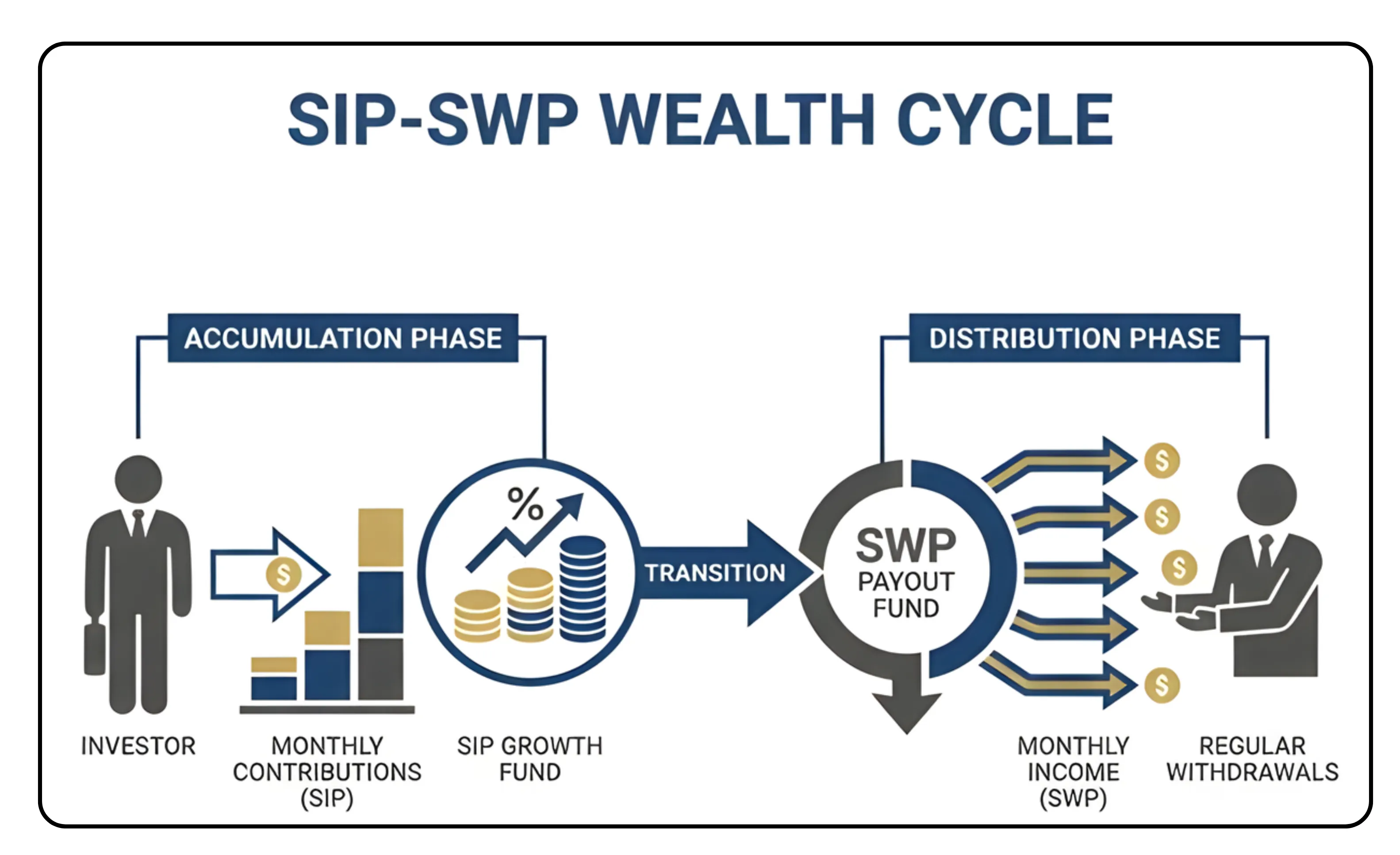

A Systematic Investment Plan (SIP) is a disciplined way to build wealth over time. However, wealth creation is only one phase of the financial journey. At some point, investors need a structured method to convert their accumulated corpus into regular income, without compromising long-term financial stability. This is where a Systematic Withdrawal Plan (SWP) becomes essential.

An SWP allows investors to withdraw a fixed amount at regular intervals while the remaining balance continues to stay invested. By maintaining market participation, the portfolio retains its growth potential even as it generates steady cash flow to meet real-world financial needs.

“A Systematic Withdrawal Plan allows an investor to withdraw a fixed amount at predetermined intervals from mutual fund investments.”

“Withdrawals can be monthly, quarterly, or annually, though monthly withdrawals are most common.”

“SWP credits money directly to the investor’s bank account.”

From wealth creation to income generation

During the accumulation phase, SIPs steadily build a corpus. As financial goals approach or retirement begins, priorities shift from growth to dependable income.

An SWP enables periodic withdrawals while the remaining corpus continues to grow. This balance helps prevent premature depletion of savings while providing a steady cash flow.

Investors can choose the withdrawal amount, frequency, and duration based on their financial needs.

Why SWP becomes essential after retirement

SWP is widely used during retirement, when a regular income stream becomes critical. It can support monthly living expenses, healthcare costs, education commitments, or ongoing financial obligations.

In a country where traditional pension coverage remains limited, SWP offers a structured way to generate income while preserving long-term savings.

“SWP is particularly suited for retirees or anyone needing regular supplemental income.”

“The need for SWP varies based on individual financial goals.”

Want a portfolio aligned with your financial goals? Read How to Build a Mutual Fund Portfolio That Serves Your Goals.

A solution beyond retirement

SWP is equally relevant for individuals with unpredictable income patterns. Consultants, freelancers, and business owners often experience uneven cash flows. A structured withdrawal plan can provide predictable monthly income while surplus funds remain invested.

It can also support lifestyle needs such as travel, celebrations, or planned large expenses without requiring full liquidation of investments.

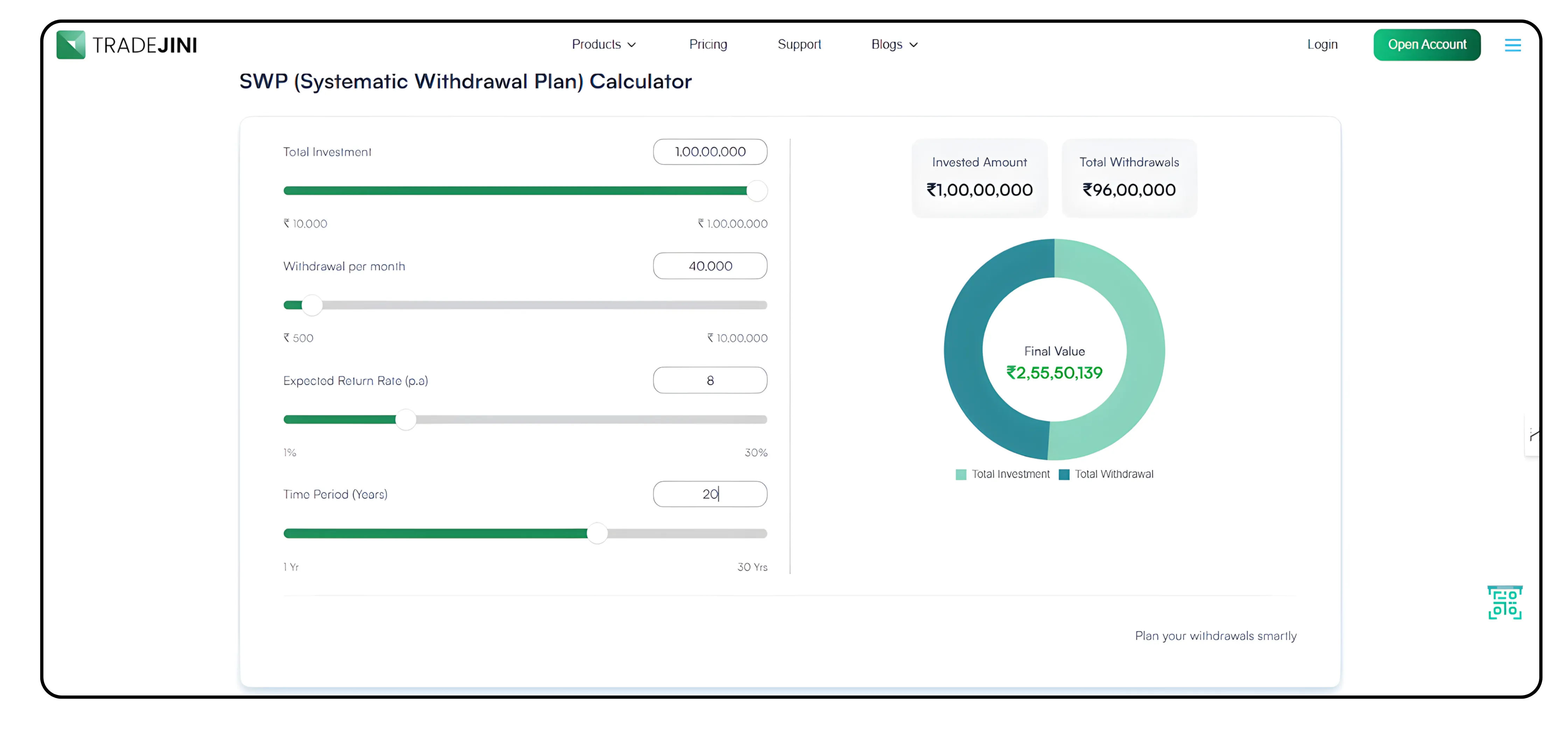

For instance an investor with a retirement corpus of ₹1,00,00,000 starts a SWP of ₹40,000 per month for 20 years. Assuming an average annual return of 8%, the total withdrawal over 20 years amounts to ₹96,00,000. Despite these regular withdrawals, the remaining corpus continues to grow due to compounding. At the end of 20 years, the investor is left with approximately ₹2.55 crore. This example demonstrates how an SWP can provide steady income while still allowing the investment to grow over the long term, provided the return rate is higher than the withdrawal rate.

Check our Tradejini’s SWP calculator

Planning the transition from SIP to SWP

The shift from accumulation to withdrawal should be deliberate. Ideally, SIP contributions are paused a few years before withdrawals begin. This allows the corpus to grow without fresh inflows and reduces the risk of withdrawing during a market downturn.

A well-planned transition improves withdrawal stability and reduces timing risk.

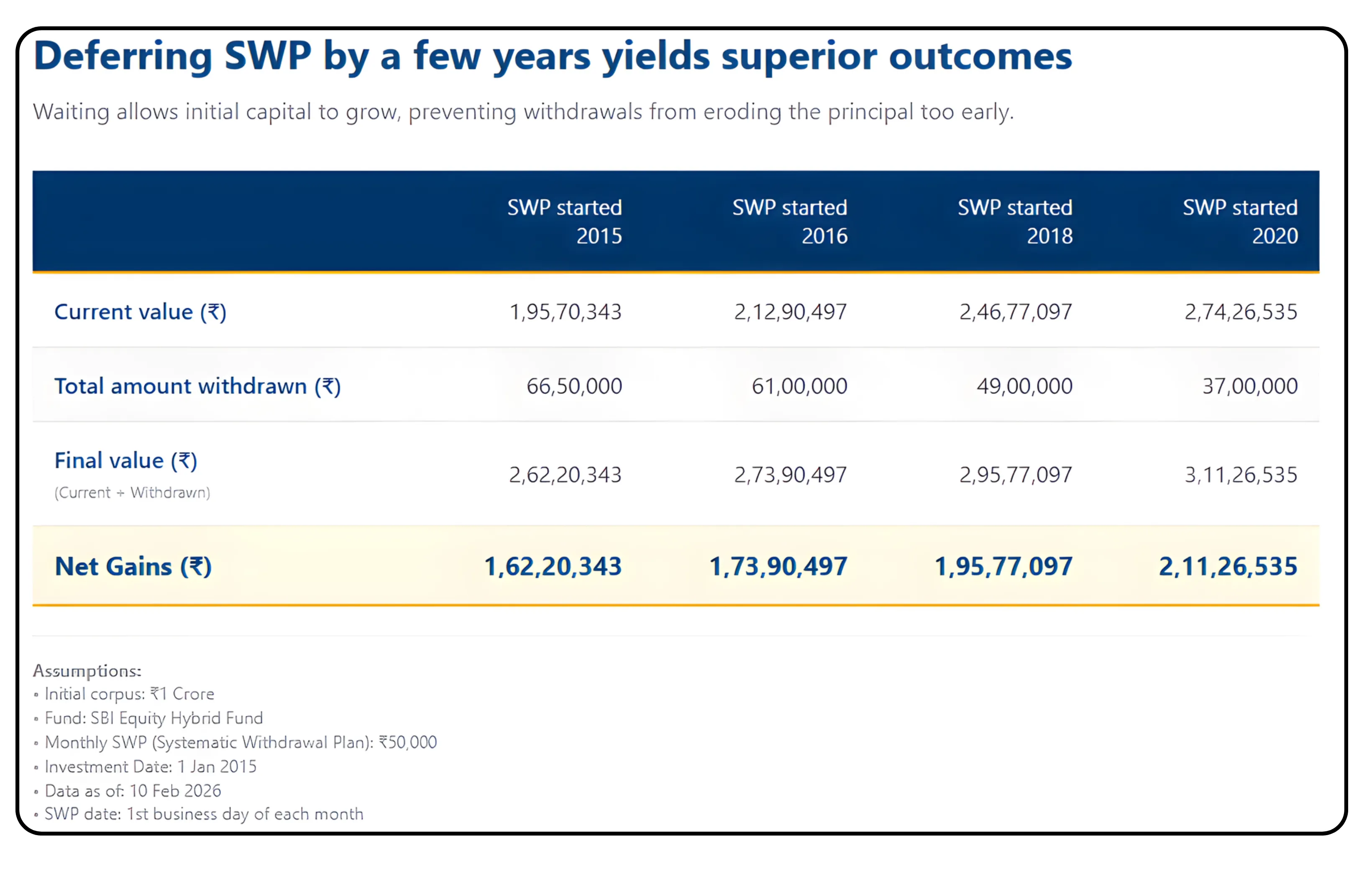

The advantage of waiting

Allowing investments more time to compound before starting withdrawals strengthens the portfolio’s ability to sustain long-term income. A longer growth period increases resilience and improves sustainability.

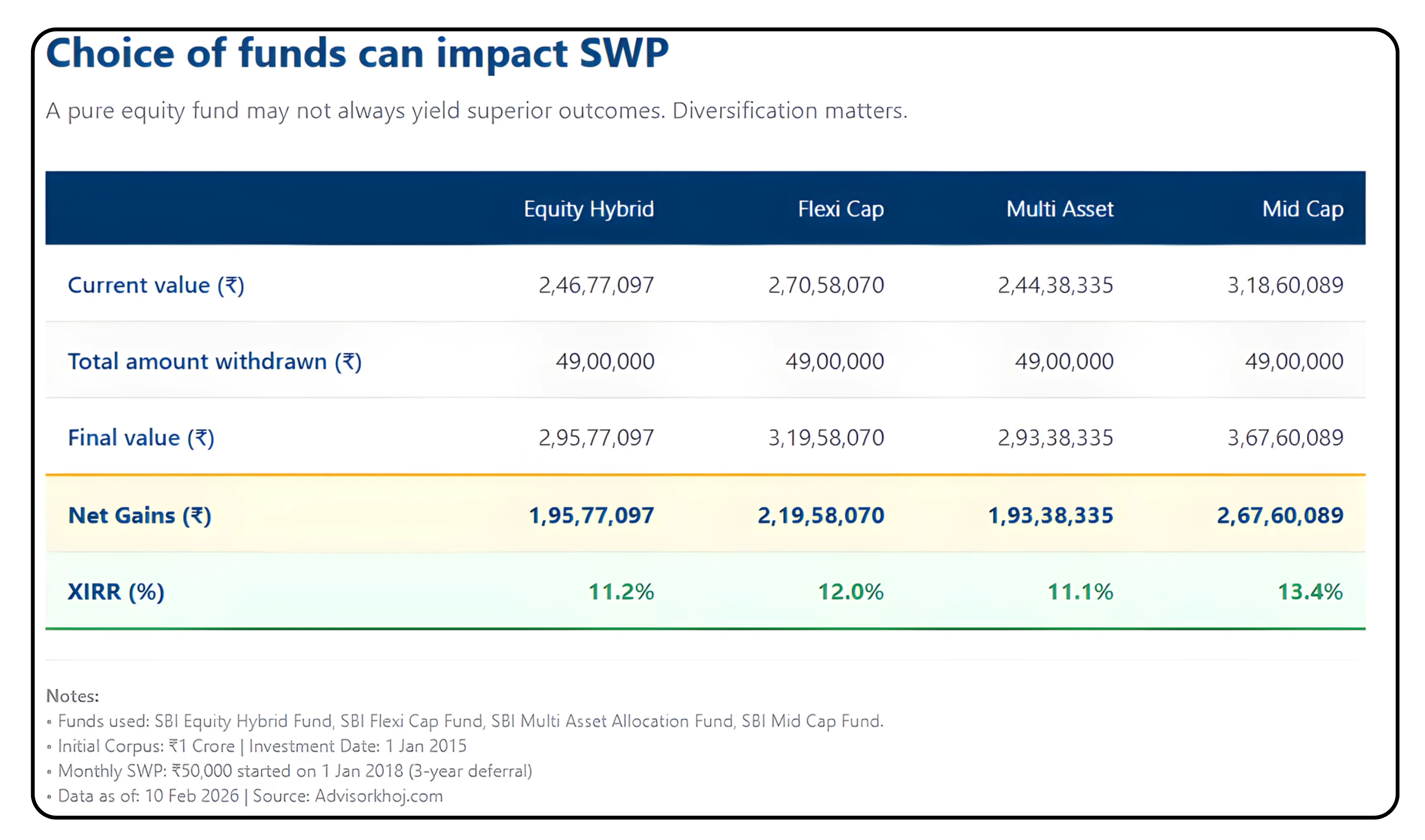

Choosing the right fund mix

The type of funds used for withdrawals plays an important role in long-term outcomes. A balanced allocation that blends growth potential with relative stability can support income needs while managing volatility.

Thoughtful fund selection helps maintain both sustainability and peace of mind.

“Hybrid and balanced advantage funds dynamically adjust equity and debt exposure to manage volatility.”

“Debt funds can offer stability, while hybrid funds balance growth with moderate risk.”

“Balanced advantage funds are often preferred to reduce drawdowns during market corrections.”

Want more stability in your income strategy? Explore Multi-Asset Allocation Funds.

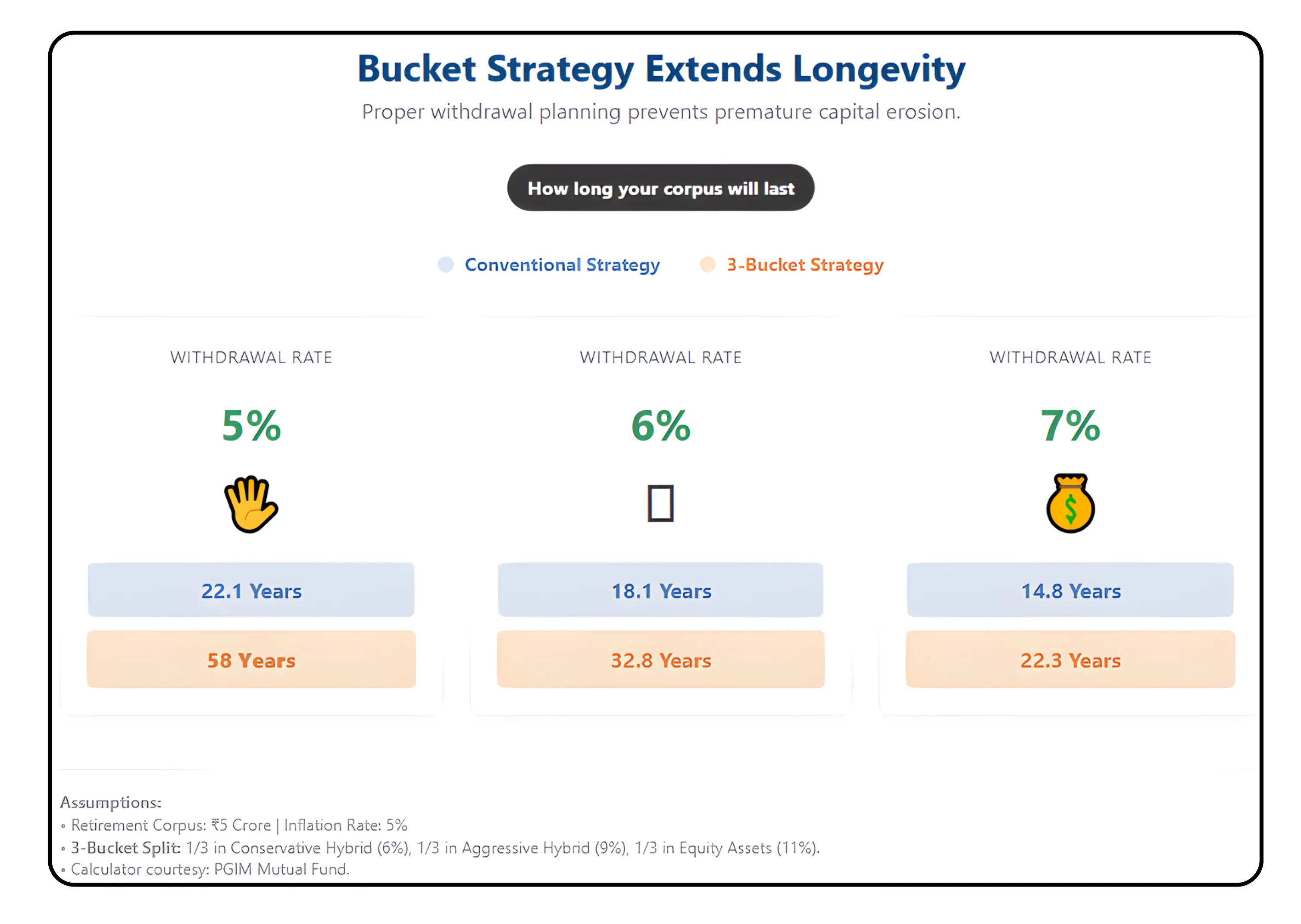

Using a bucket strategy for stability

A bucket approach divides retirement savings based on time horizon and purpose.

A short-term bucket covers immediate expenses.

A medium-term bucket supports needs over the next several years.

A long-term bucket remains invested for growth and inflation protection.

This structure helps manage market fluctuations while ensuring uninterrupted income.

Setting a sustainable withdrawal level

Withdrawal amounts should be aligned with long-term sustainability. Excessive withdrawals can erode capital, especially during market declines.

Factors such as inflation, life expectancy, expected returns, and lifestyle needs should guide withdrawal decisions.

“A withdrawal rate of about 4–5% annually is often considered sustainable for long-term income.”

Tax efficiency and flexibility

In equity mutual funds, long-term capital gains above the exemption limit are taxed at applicable rates, while debt funds follow capital gains taxation based on holding period.

Lifecycle approach to financial independence

Used together, SIP and SWP create a disciplined financial journey:

Accumulate wealth through systematic investing

Allow investments to grow over time

Generate steady income through structured withdrawals

This approach supports financial independence while preserving long-term wealth.

“An SWP calculator can help estimate how long your corpus will last based on withdrawal rate and expected returns.”

“It requires inputs such as investment amount, withdrawal amount, tenure, and expected return.”

“Investors should review expense ratios, exit loads, and tax implications before choosing an SWP fund.”

“Funds can be switched if performance declines, but exit load and tax impact should be evaluated.”

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.