DATA PATTERNS

The Indian aerospace and defence sector is undergoing a structural transformation, as it is getting a big boost from government policies. The central theme of this shift is ‘Atmanirbhar Bharat”, a national mission aimed at making India self-reliant in defence production by reducing imports and encouraging local manufacturing of weapons, electronics, and aerospace systems. This initiative has created significant tailwinds for indigenous companies, fundamentally altering the market landscape from one of global competition to a protected, high-growth domestic ecosystem.

The scale of the opportunity is substantial. The Indian aerospace and defence market was valued at approximately USD 26-27 billion in 2023 and is projected to nearly double to USD 48-54 billion by 2032, registering a compound annual growth rate (CAGR) of around 6.8-7.0%. This growth is fueled by India’s position as the world’s fourth-largest defence spender, with a budget of INR 6.21 lakh crores (approximately USD 75.7 billion) for the year 2024-25.

More critically for domestic players, government policy has moved beyond mere rhetoric to concrete action. A significant portion - three-quarters - of the capital procurement budget for modernization is now reserved for domestic sourcing, creating a captive market. This is enforced through the issuance of “positive indigenisation lists,” which effectively act as import-ban lists for hundreds of strategic components, sub-systems, and entire platforms, guaranteeing demand for capable Indian manufacturers. These policies are showing positive results: domestic defence production surged to a record INR1.27 lakh crore in FY 2023-24, and exports grew by 32.5% to INR 21,083 crores., Additionally, the government targets ₹50,000 crore in exports by 2028–29. This policy framework ensures that agile, technologically advanced private sector firms are no longer just peripheral suppliers but are being nurtured as strategic partners in India’s quest for strategic autonomy.

Read also: Engineering Defense Growth with CFF Fluid Control Ltd.

Business Snapshot and Evolution of Data Patterns:

Established in 1998, Data Patterns India Limited has evolved into a premier defence provider that controls everything from design to manufacturing for its products, all in-house: from initial design and R&D to prototyping, qualification, manufacturing, and long-term support. This end-to-end control is a foundational element of its strategy, enabling it to serve the entire Indian defence ecosystem, including the Ministry of Defence (MOD), the Defence Research and Development Organisation (DRDO), and major Defence Public Sector Undertakings (DPSUs) like Hindustan Aeronautics Ltd. (HAL) and Bharat Electronics Ltd. (BEL).

The company’s core expertise lies in critical, high-technology domains such as Radars, Electronic Warfare (EW), satellite systems, avionics, and advanced communication systems. Historically, like many private players, its role was often confined to supplying components or sub-systems for larger platforms. However, the company has embarked on a deliberate and transformative strategic evolution to move up the value chain. This involves transitioning from a sub-system supplier to a prime provider of complete, integrated systems. This strategic pivot is not merely an operational shift but a calculated move to significantly expand its Total Addressable Market (TAM) from an estimated range of INR 10,000-15,000 crores to a much larger pool of INR 20,000-30,000 crores, allowing it to bid for system-level defence projects. This goal to capture more value from each project drives the company’s growth and profit plans.

Financial Performance Overview

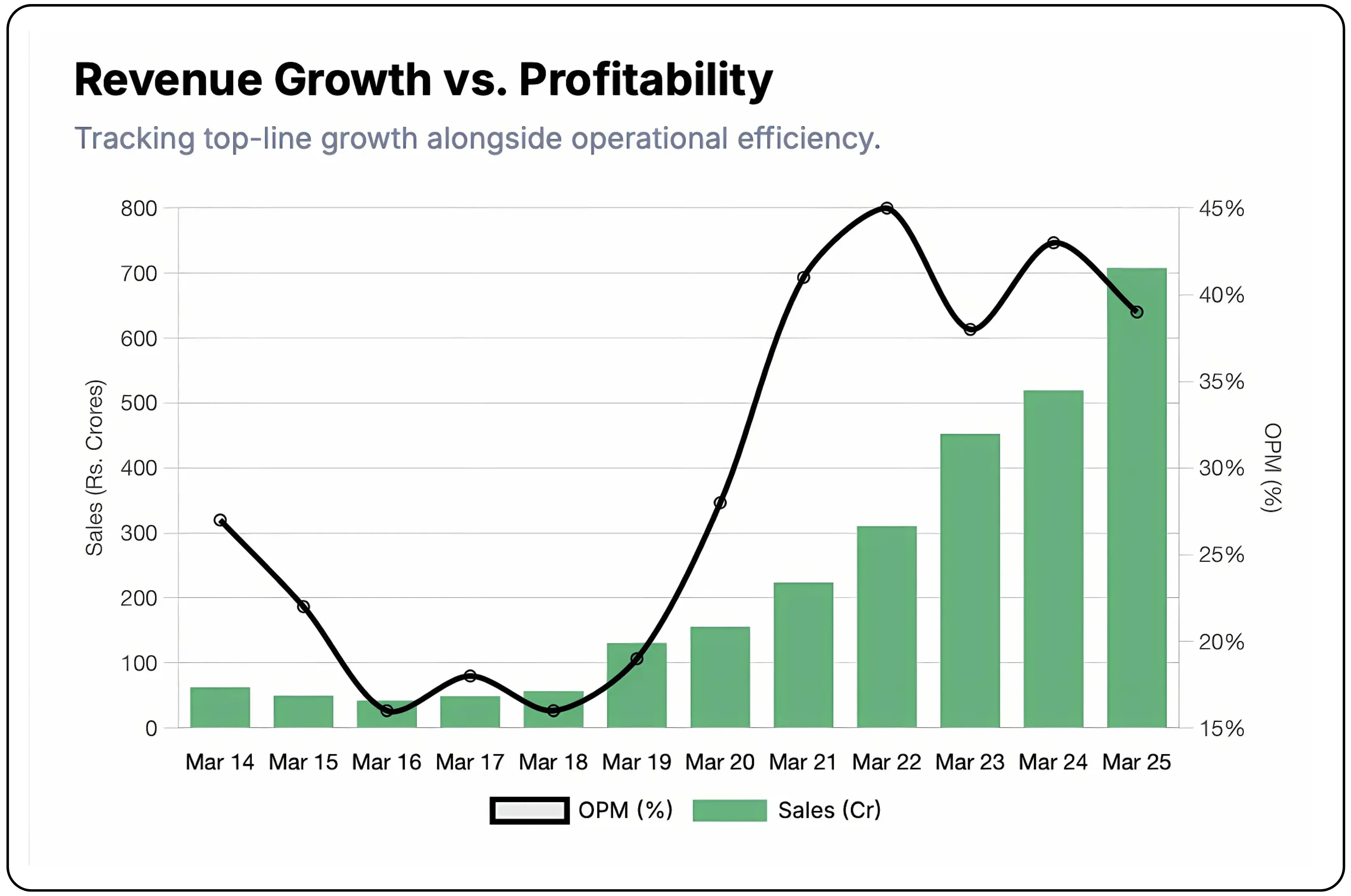

Data Patterns is growing exceptionally fast and is very good at making money. Over the last five years, its sales have grown at an average of 33% per year, while profits have grown even faster at around 41% per year. The company is also highly profitable with a range of 39% operating profit margin.

The company is in a very safe financial position. It is completely debt-free. On top of that, it has a huge cash pile of over ₹424 crores. This cash cushion allows it to handle any payment delays from clients and fund new projects without needing to borrow money. All these things have contributed to the Data Patterns stock looking interesting among its peers.

The company has a clear view of its future business. It already has ₹814 crores of confirmed orders to work on. Furthermore, it expects to secure potential new orders worth between ₹2,000 to ₹3,000 crores in the next couple of years, ensuring its growth continues.

Business segments breakdown

Data Patterns has cultivated deep domain expertise across a diversified portfolio of critical defence electronics segments. This technological breadth not only allows it to address a wide array of platform requirements but also mitigates program-specific risks, providing a more stable foundation for growth. The company’s capabilities are not just theoretical but validated by successful deliveries and landmark technological achievements.

Radars and Electronic Warfare (EW)

The Radar vertical is a cornerstone of the company’s business, accounting for roughly 90% of the company’s turnover, with a product range that includes sophisticated Fire Control Radars, X-Band Radars for various applications, and compact radars designed for Unmanned Aerial Vehicles (UAVs). A significant operational milestone in this segment has been the successful delivery and installation of nine Precision Approach Radars for the Indian Army and Navy, demonstrating its ability to execute on critical infrastructure projects. Similarly, its Electronic Warfare (EW) suite is comprehensive, covering intelligence-gathering systems like COMINT (Communications Intelligence) and ELINT (Electronic Intelligence), as well as countermeasures such as airborne jammerpods and radar warner receivers. With India’s EW market projected to grow steadily, this segment represents a key area of focus and opportunity.

A showcase of Data Patterns’ versatile mobile tactical systems and the high-performance Precision Approach Radar (PAR)

Missile Systems and Avionics

One of the strongest proofs of Data Patterns’ advanced technology is its success in missile systems. The company recently announced the successful flight test of its indigenously designed and developed seeker for the BrahMos supersonic cruise missile, a premier strategic weapon system. The seeker, which is the missile’s “eye,” is one of its most complex components. Achieving “excellent performance” in live trials has led to a major production contract, a key milestone for the company. This builds upon its existing role in the BrahMos program as a supplier of launchers and test equipment. In avionics, the company is developing critical systems such as advanced Glass Cockpit Displays and mission computers for key indigenous platforms like the Light Combat Aircraft (LCA) and various helicopters, placing it at the heart of India’s aviation modernization efforts.

Strategic Moats

Data Patterns has constructed a formidable competitive moat that protects its business and sustains its high-margin profile. This advantage comes from the powerful combination of its integrated business model and expanding proprietary Intellectual Property (IP).

End-to-End Control and In-House Intellectual Property (IP)

The primary moat for Data Patterns is its fully integrated business model, which gives it control over the entire product lifecycle - from initial design and R&D to manufacturing and testing. Its products are built with in-house systems and IP, meaning they are independent of foreign technology transfers, a point the management consistently highlights.This in-house control is a significant advantage in the defence sector for several reasons:

- Speed and Agility- Enables faster development and quicker response to customer needs.

- Quality and Security- It ensures stringent quality control over every component and protects sensitive, proprietary defence technology from external exposure.

- Cost Efficiency- Greater control over the production process allows for better cost management, resulting in the company’s industry-leading profit margins.

- Strategic Independence- Reduces risks by avoiding reliance on foreign technology and geopolitical disruptions, positioning Data Patterns as a truly indigenous partner for India’s defence establishments.The Reusable Building Blocks Flywheel

A flywheel, in business terms, is a self-reinforcing cycle where each success makes the next success easier and faster. Just like a physical flywheel stores energy and spins more smoothly over time, a business flywheel gains momentum as its processes, knowledge, and assets build upon each other. This concept lies at the heart of Data Patterns’ R&D strategy. The company has made substantial investments of over INR 145 crores in product development in the last 1.5 years alone to create a modular library of proven hardware and software components, creating a strong, self-reinforcing cycle of innovation.

- When a new system is required, engineers don’t start from scratch. They use ready-made, tested components from their existing library.

- This dramatically reduces development risk and accelerates the time-to-market for new products.

- With each new project, the IP library of these building blocks expands and is further validated, making the next development cycle even more efficient.

Long-Term Support and Customer Stickiness

Data Patterns has built a moat based on trust and reliability by committing to maintain and support its products for 20 years. This directly addresses a major challenge for defence clients, who often struggle with equipment obsolescence and high maintenance costs, particularly with foreign-produced systems. This long-term commitment achieves two critical goals:

- Builds Deep trust by fostering customer stickiness, by positioning Data Patterns as a long-term strategic partner, not just a supplier.

- Creates Recurring revenue as it ensures a steady and predictable stream of high-margin revenue from service, maintenance, and upgrade contracts, further solidifying the company’s financial foundation.

At the core of Data Patterns’ strategy is a focus on "reusable building blocks”. Over the past 1.5 years, the company has invested around ₹140 crore to develop a modular library of proven hardware and software components. When developing a new system, instead of starting from scratch, its engineers can assemble a significant portion of the solution using these pre-existing, qualified blocks. This approach creates a powerful flywheel effect: development becomes faster and less risky, and with each new project, the IP library expands, making the next project even more efficient. This self-reinforcing cycle of innovation is incredibly difficult for competitors to replicate.

Furthermore, the company has built a moat based on trust and longevity. It commits to providing service and support for its products for 20 years, directly addressing a major pain point for defence clients who often face obsolescence issues and high maintenance costs with foreign equipment. This commitment fosters deep customer stickiness and ensures a long tail of high-margin service and upgrade revenue, solidifying its position as a long-term strategic partner rather than a mere transactional supplier.

Growth drivers and expansion plans

Data Patterns is actively deploying capital and resources to fuel its next phase of growth, preparing to capitalize on the enormous opportunities in the Indian defense market and beyond. The company’s growth strategy is multi-pronged, focusing on capacity building, securing large-scale orders, and expanding its geographic footprint.

A key sign of management’s confidence in future growth is its aggressive capital expenditure plan, with ₹150 crore allocated over the next two years. This investment focuses on strategic capacity enhancement. It includes the construction of large systems integration hangars and specialized facilities for complete radar and Electronic Warfare (EW) vehicle integration. Such infrastructure is essential for executing the large, full-system orders that are central to its value-ascension strategy, signaling the company’s readiness for significant business growth.

This investment is backed by a strong and visible order pipeline. Management has guided for INR 2,000 - 3,000 crores in new orders over the next 18-24 months and expects new order intake for FY26 to be in the range of INR 1,000 - 2,000 crores. A large share of these are repeat orders for proven products, which generally offer higher margins and lower execution risk. Beyond the domestic market, Data Patterns is actively expanding into exports, competing with global Original Equipment Manufacturers (OEMs) in markets across Europe and East Asia. To support this, the company plans to set up a dedicated marketing organization. Its international order book already stands at a robust level of approximately INR 100 crore, and success in the export market will provide valuable revenue diversification and de-risk its dependence on the Indian procurement cycle.

Risks and industry headwinds

While the long-term outlook for Data Patterns is compelling, the business is exposed to inherent risks and operational challenges, primarily stemming from its deep dependence on the government-led defence procurement ecosystem. These risks primarily impact the timing of revenue recognition and put pressure on working capital.

The most frequently cited headwind is customer-side delays. The company has experienced repeated instances of “delivery deferments,” where manufactured products are ready but revenue cannot be booked due to delays in customer inspections, clearances, or final acceptance. This issue, which impacted approximately INR 70 crore of products in one quarter of FY25, creates significant quarter-to-quarter volatility in financial performance. Similarly, new order inflow is uneven and unpredictable, as it depends on government decisions and tender timelines, which are outside the company’s control.

These delays have a direct and material impact on the company’s working capital, which stands out as its primary operational challenge. The long gestation periods of large, development-intensive projects require substantial upfront investment in materials and engineering. This has led to a noticeable increase in inventory days, which rose from 155 to 161 days in FY25, stretching the overall cash conversion cycle. The financial statements reflect this pressure with cash flow from operations turning negative in FY25. While the company’s strong, debt-free balance sheet provides a crucial buffer to absorb this strain, sustained delays across multiple large projects could test its liquidity and represent the most significant risk to its operational rhythm.

Market View

Data Patterns commands a premium valuation in the Indian defence sector, trading at a significantly higher multiples than some of its larger, state-owned peers. This premium reflects strong investor confidence in the company’s superior growth and profitability profile, positioning it more as a high-growth, intellectual property (IP)-led technology company than a traditional industrial manufacturer

| FY | Sales (₹ Cr) | Expenses (₹ Cr) | Operating Profit (₹ Cr) | Other Income + (₹ Cr) | Interest (₹ Cr) | Profit After Tax (₹ Cr) |

|---|---|---|---|---|---|---|

| Mar-25 | 708 | 433 | 275 | 46 | 12 | 222 |

| Mar-24 | 520 | 298 | 222 | 46 | 9 | 182 |

| Mar-23 | 453 | 282 | 172 | 9 | 8 | 124 |

| Mar-22 | 311 | 170 | 141 | 4 | 11 | 94 |

| Mar-21 | 224 | 132 | 92 | 3 | 14 | 56 |

| Mar-20 | 156 | 113 | 43 | 4 | 13 | 21 |

| Mar-19 | 131 | 106 | 26 | 1 | 11 | 8 |

| Mar-18 | 57 | 48 | 9 | 0 | 5 | 1 |

As of the latest filings and market data (August 2025), Data Patterns trades at a trailing twelve-month (TTM) Price-to-Earnings (P/E) ratio of approximately 65.4x and an Enterprise value to EBITDA (EV/EBITDA) multiple around 44.2x. In comparison, major state-owned peers trade at lower multiples:

| Company | YoY Profit Growth (%) | P/E Ratio | EV/EBITDA |

|---|---|---|---|

| Data Patterns | 22 | 65.4 | 44.23 |

| Hindustan Aeronautics Ltd (HAL) | 9.75 | 36.48 | 21.16 |

| Bharat Electronics Ltd (BEL) | 34.1 | 51.61 | 35.08 |

| Bharat Dynamics Ltd (BDL) | -10.3 | 104.17 | 64.86 |

Data patterns exhibit strong YoY profit growth of 22%, significantly higher than HAL and BDL and slightly below BEL’s 34.1%. Its valuation multiples, like the P/E and EV/EBITDA, are also above HAL and BEL, indicating a premium for its growth and profitability, though below the very high multiples of BDL, which has more volatility. The company’s trailing twelve months PAT margin also exceeds 31% and the 5-year revenue CAGR is above 35%, far outpacing larger players with slower growth.

The market’s premium valuation on Data Patterns is justified by its strategic positioning as an R&D-driven firm with proprietary IP and its ability to sustain high growth and margins while being a reliable vendor to even some of its peers mentioned above.

Bottom Line (Decoder’s Take)

Data Patterns stands out as a high-quality, high-growth compounder, uniquely positioned to capitalize on India's multi-decade defense modernization and indigenization imperative. Its strategic moat, built on deep in-house R&D and proprietary IP, enables an industry-leading margin profile and a strong competitive position. While the business faces inherent risks from lumpy government order cycles and working capital intensity, its pristine balance sheet provides a substantial cushion. The stock's premium valuation is a clear reflection of its superior growth prospects and profitability.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.