Exide Industries is repositioning as the energy storage market transitions from lead-acid to lithium-ion technologies. After decades in lead-acid batteries, the company is investing in lithium-ion cell manufacturing to address rising domestic demand for electrification.

India is in the midst of a rapid global shift in energy storage practices. Government measures such as Production Linked Incentives (PLI) provide financial support and operational incentives to scale domestic battery manufacturing.

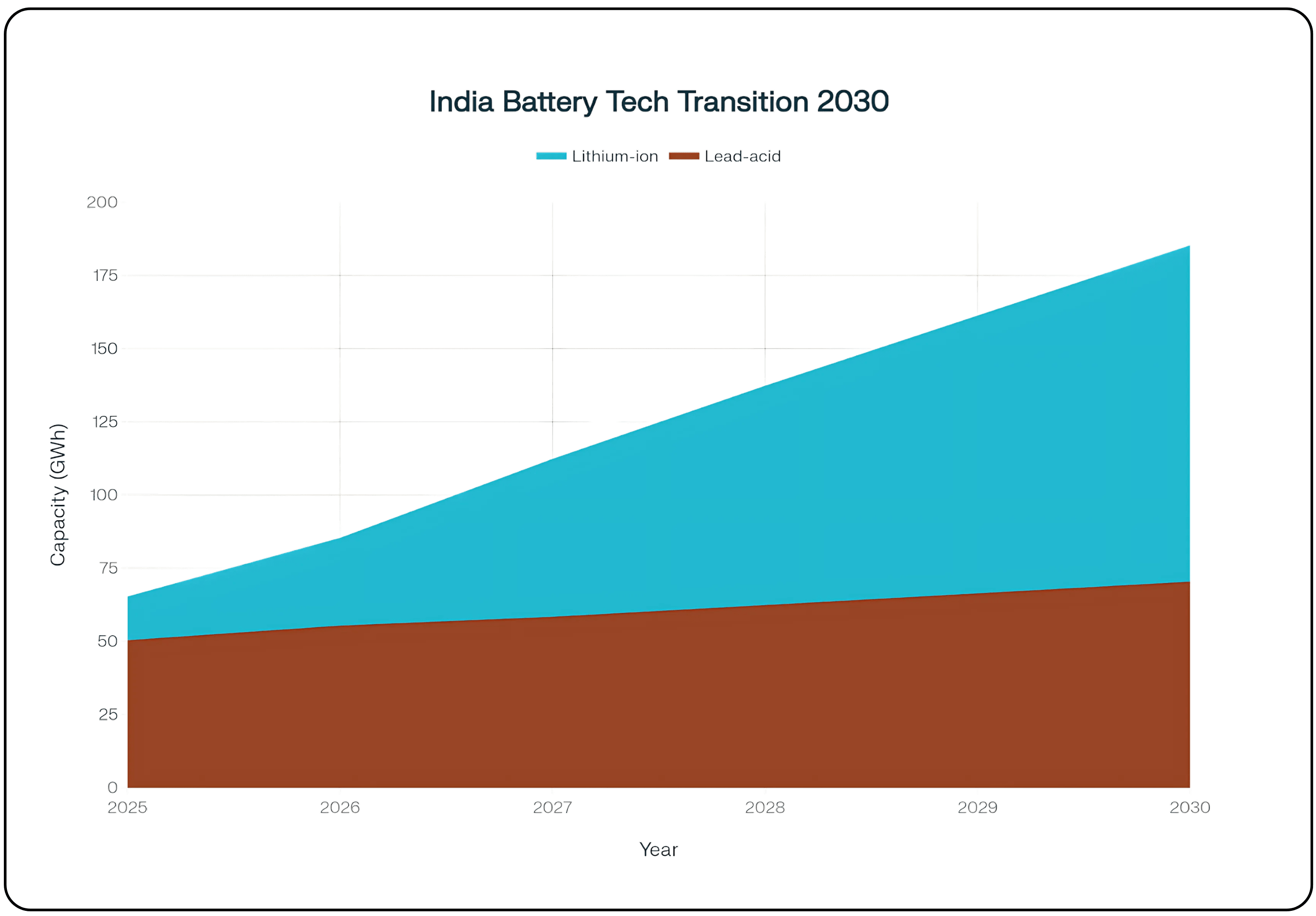

Analysts estimate India will require roughly 120–130 GWh of lithium-ion capacity by 2030 to meet projected EV and energy storage demand. Government initiatives like Production Linked Incentive (PLI) schemes for battery manufacturing and ambitious renewable energy targets are acting as powerful catalysts. Concurrently, the data center market is expanding at a CAGR of approximately 20%, requiring reliable power backup solutions. The legacy lead-acid market remains sizable, creating a strategic dynamic between lead-acid and lithium-ion segments; the relevant industrial and automotive applications are forecasted to grow at ~7% CAGR through 2031. This dual-market reality forms the backdrop for understanding Exide’s future prospects and why investors are closely watching the execution.

Also read: Ajax Engineering A Strong Play on India’s Infrastructure Mechanisation

Business Snapshot and Evolution

With more than seven decades of operations, Exide is a long-established participant in India’s battery manufacturing sector. Historically a leader in the lead-acid battery world, the company is now in the middle of a significant evolution. Recognizing the potential of new energy technologies, Exide is pivoting to a future where it leads not just in its core segment but also in the new and ever-evolving green energy ecosystem in the form of Li-ion batteries.

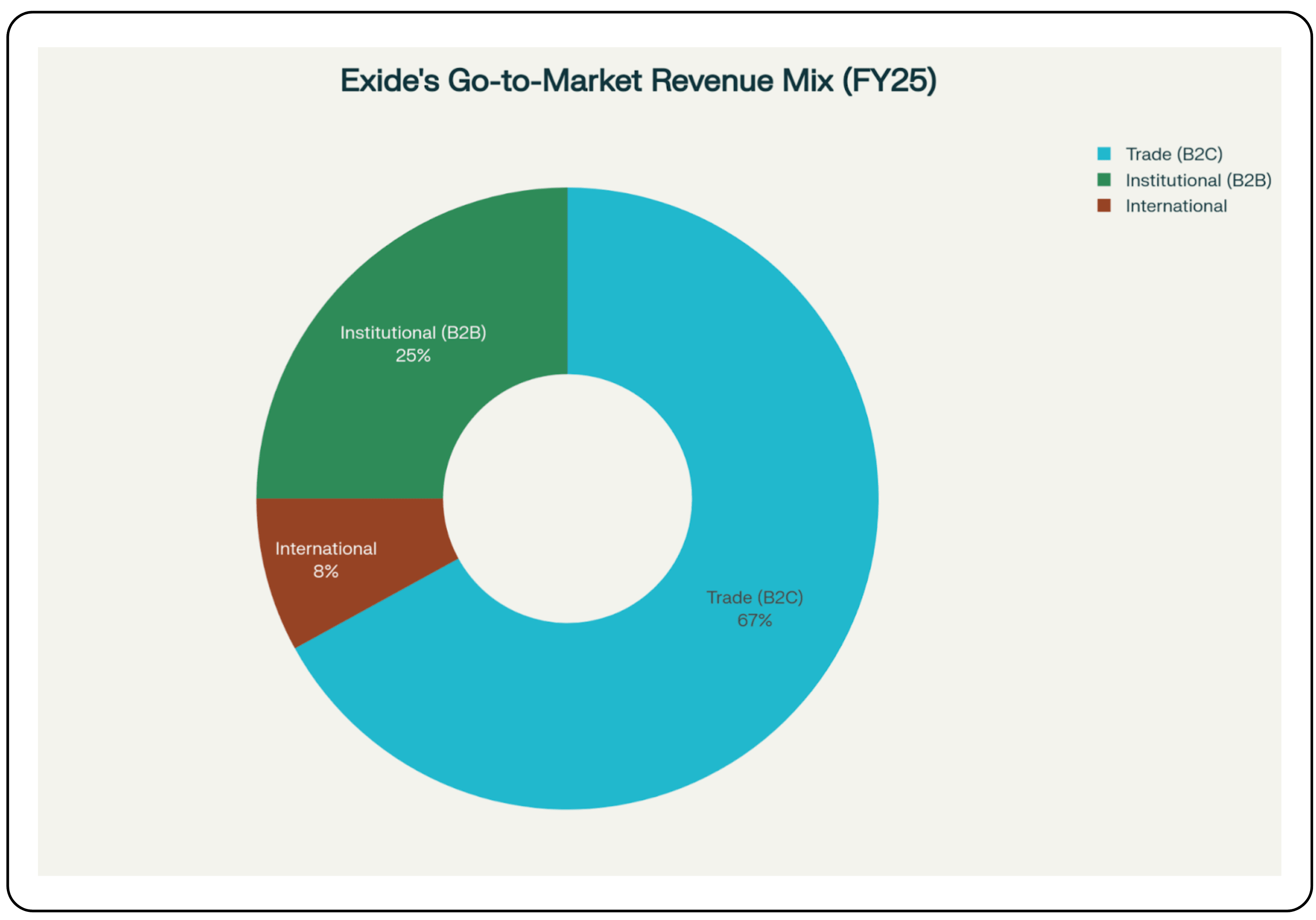

The company recently reorganized how it works. Instead of having separate entities for different products, they now have three main vertices focused on different types of customers. The company has restructured from an SBU-led model to a functional organization to improve agility and commercial focus. The new structure comprises three verticals - Trade (B2C), Institutional (B2B) and International - intended to sharpen go-to-market execution and customer focus across legacy and new technology segments.

Financial Performance Overview

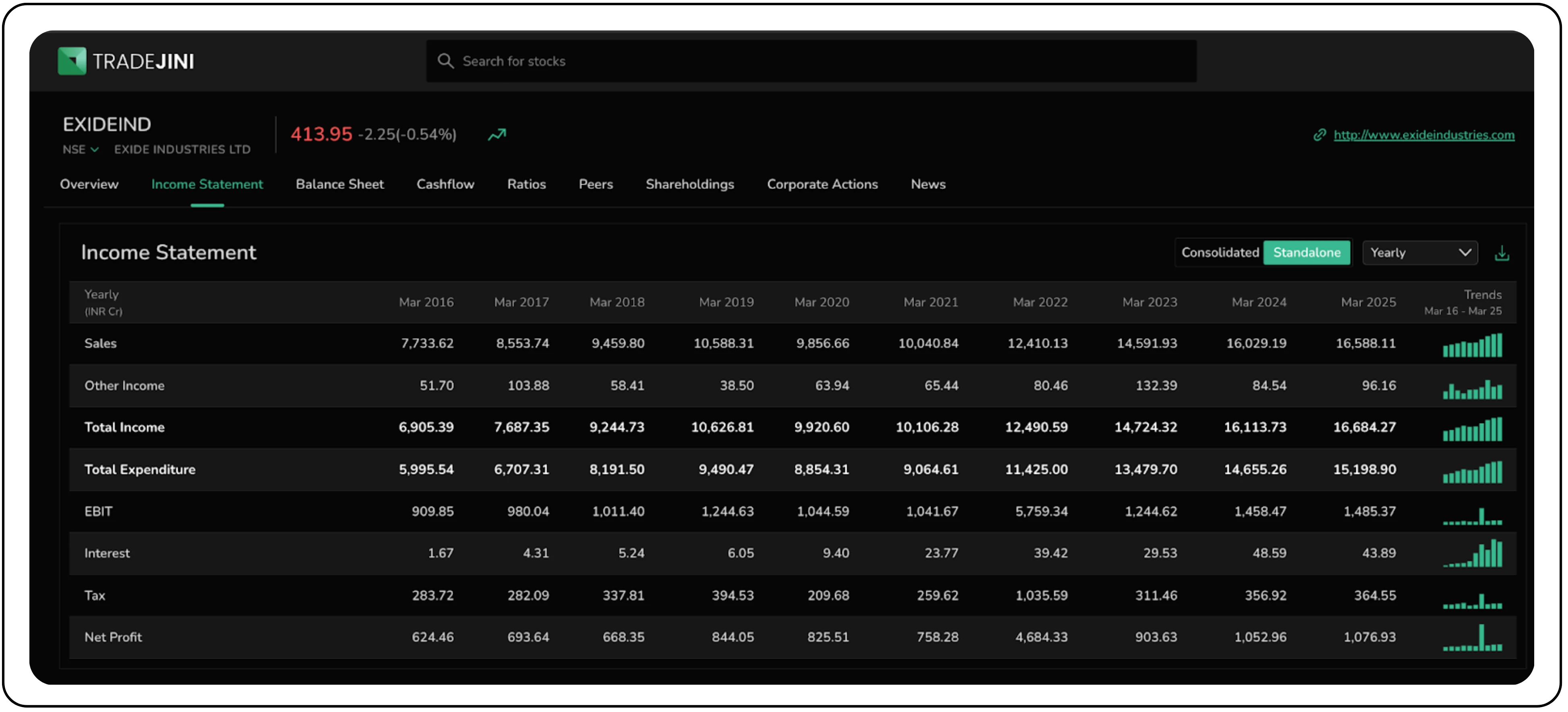

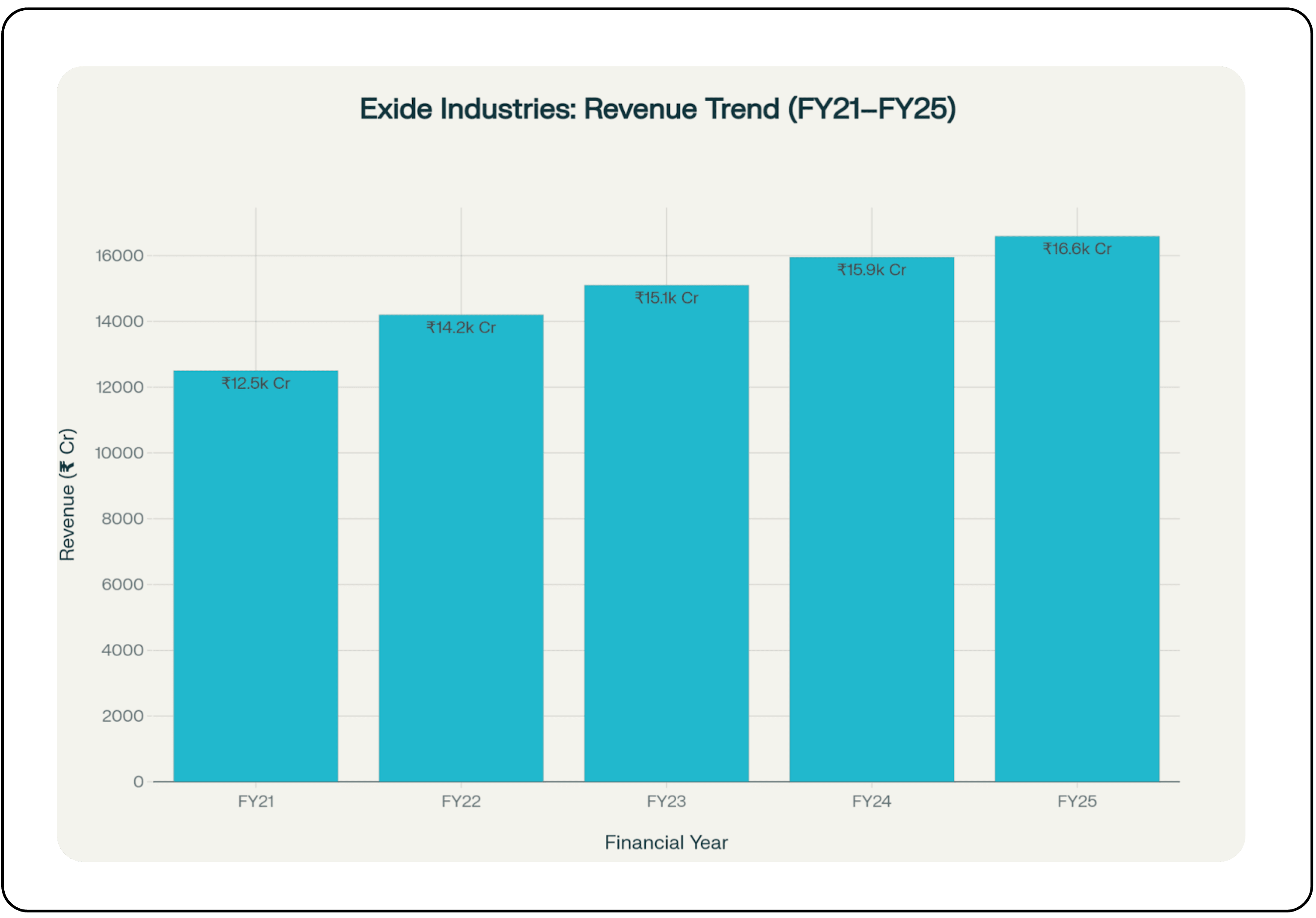

Exide’s recent financials show a stable core business that is being used to fund investments in lithium-ion capacity. For FY25, revenue rose 4% year-on-year to ₹16,588 crore. EBITDA was ₹1,893 crore (+1% YoY) and PAT was ₹1,077 crore (+2.3% YoY), reflecting modest margin expansion on a high prior-year base.

Profitability and operating cash flow diverged in the period. Operating cash flow declined 35% year-on-year, primarily due to higher working capital requirements. Excluding the working capital build, operating cash flow was broadly in line with the prior year.

Exide has maintained a net-debt-free balance sheet since 2012. The company has retained financial flexibility and maintained strong credit metrics. New projects, including the capital-intensive Li-ion venture, are funded primarily through internal accruals, showcasing robust operational cash generation over the long term and allowing it to pursue transformative growth without compromising its financial stability.

Business Segments Breakdown

Operations are organized around two pillars: the established lead-acid business and the emerging lithium-ion venture.

The Lead-Acid Profitable Core

This segment is characterized by continuous innovation and market dominance across three verticals:

- Trade Business (B2C)

This vertical is Exide’s direct artery to the end consumer, commanding a vast and diverse market. Its largest component is the Mobility aftermarket, where Exide is a dominant force, supplying replacement batteries for the entire spectrum of Indian vehicles, from two-wheelers to heavy commercial trucks. It extends into the rapidly growing Home Energy Storage space, offering inverter batteries and UPS systems under the well-regarded “Exide Home” sub-brand. Capitalizing on the renewable energy push, the vertical also offers end-to-end rooftop solar solutions through its “Exide Sunday” brand. And finally, it addresses sustainable urban mobility through its E-Rickshaw batteries and vehicles, marketed under the “Exide Neo” brand, cementing its presence in last-mile connectivity.

- Institutional Business (B2B)

This vertical underscores Exide’s role as a critical partner to India’s industrial and mobility infrastructure, a business characterized by deep relationships and high entry barriers. It serves as a key supplier to Vehicular OEMs, providing advanced batteries for new vehicles and, crucially, supplying essential lead-acid auxiliary batteries to four-wheeler EV manufacturers. In the Industrial UPS (I-UPS) space, Exide provides indispensable power backup for mission-critical sectors like IT data centres, with its specialized Front Terminal Planished Grid (FTPG) range as well as financial services and hospitals.

The Infrastructure arm has a long-standing presence in core sectors like railways, telecom, and power. Its portfolio also includes traction batteries for material handling equipment in logistics and warehousing, and high-performance Submarine batteries for the Indian Navy, showcasing its advanced engineering capabilities.

- International Business

The International business provides geographic diversification, contributing roughly 8% of standalone turnover through exports to over 60 countries.

Lithium-ion (EESL): Future Growth Engine

The lithium-ion initiative is executed via Exide Energy Solutions Limited (EESL), a wholly-owned subsidiary tasked with establishing domestic cell manufacturing. It is a decisive pivot designed to establish leadership in the next era of energy storage.

- A planned 12 GWh greenfield facility in Bengaluru is central to the company’s cell-manufacturing strategy

- The stated objective is end-to-end capability - “molecule to megawatt” to address automotive and stationary storage applications

- The plant is being designed for multiple chemistries (NMC, LFP) and form factors (cylindrical, prismatic) to retain commercial flexibility.

- This multi-pronged approach future-proofs the business against rapid technological shifts and positions Exide to be a one-stop solutions provider in India’s growing EV and renewable energy markets.

Strategic Moats and Differentiators

Exide’s competitive position is supported by brand reach, an integrated value chain and technology collaborations.

Brand and Reach: Exide’s primary moat is its unparalleled market presence, built over decades of trust and an expansive physical network. The Exide brand itself possesses immense equity and recall, making it the default choice for millions of consumers across India. This is also amplified by dominant market positions in key, profitable segments; for instance, the company commands more than half of the organized 4-wheeler aftermarket. This leadership is strengthened by an unmatched distribution network of over 120,000+ channel partners across India. The extensive distribution network supports product availability and service reach; replicating this scale would require significant investment for competitors.

Integrated Value Chain: Exide’s operational moat is derived from its scale and its deep integration across the value chain. The company operates 11 manufacturing plants and three lead-recycling facilities, supporting production continuity and material sourcing. Unlike many companies, Exide controls most of their supply chain. They have 11 factories and 3 recycling plants. They recycle 75% of the lead they use, which saves money and protects them when raw material prices go up.

Technological Leadership: Exide differentiates itself through a dual-pronged technology strategy, enhancing its current portfolio while proactively building for the future. In its core business, a strong R&D focus has led to a continuous stream of advanced products such as FTPG batteries for data centres, and the adoption of Punched Grid and CONCAST technologies to improve battery performance and manufacturing efficiency. This internal innovation is accelerated through five global strategic technical collaborations with partners like SVOLT and East Penn Manufacturing.

Growth Drivers and Expansion Plans

Exide Industries is executing a clear, multi-pronged strategy to fuel its next phase of growth. The strategy aims to leverage the stable lead-acid business to fund investments in lithium-ion capacity and related technologies.

Deepening Domestic Dominance: The core of Exide’s strategy is the continued expansion of its dominant position in the domestic lead-acid market. The company is actively capitalizing on robust, double-digit growth in the automotive aftermarket and the solar solutions space. This market penetration is being fueled by a continuous pipeline of new products, including enhanced battery ranges for commercial vehicles and e-rickshaws, and the “Exide Sunday” end-to-end rooftop solar offerings. In the B2B space, the focus is on capturing high-value opportunities in growing sectors like data centres by deploying specialized products like the FTPG battery range. This ensures that the profitable core business continues to grow and generate the capital required for future investments.

The Lithium-Ion Gambit: As of June 2025, Exide has invested ₹3,602 crore of equity toward the 12 GWh Bengaluru facility, which is targeted for commercial production in FY26. The explicit goal is to capture a significant share of India’s projected 120 GWh Li-ion battery demand by 2030. By building capabilities for multiple chemistries and form factors, Exide is positioning itself to supply the entire spectrum of the market, from two-wheelers to grid-scale storage systems. This ambition is already gaining traction, evidenced by the formation of binding agreements and advanced discussions with major automotive OEMs.

Risks and Industry Headwinds

Exide faces several material risks related to commodity volatility, technological transition and execution of large capital projects. These challenges range from broad macroeconomic shifts to specific operational and technological pressures that require constant vigilance and agile management.

Operational and Commodity Price Volatility: Battery making needs metals like lead and antimony. When these prices go up suddenly, Exide loses money. In Q4 FY25, a sharp antimony price spike reduced profitability by roughly ₹50 crore, illustrating commodity sensitivity. The price of lead, its primary input, is also notoriously volatile. While these costs are passed on, there is often a time lag that can squeeze margins in the short term. In periods of muted top-line growth, the company faces the challenge of lower absorption of its fixed overheads, which can impact operating profitability. The business is only exposed to global supply chain disruptions and logistical costs, which it actively mitigates by diversifying its logistics partnerships.

A structural headwind is the transition to lithium-ion technologies, which could reduce demand for lead-acid solutions in certain applications. This shift poses a direct threat to Exide’s legacy lead-acid business in several key sectors. The telecom, railway, and traction segments are rapidly transitioning to Li-ion solutions, driven by their declining prices and superior performance characteristics. While Exide is proactively addressing this with its own Li-ion venture, it must manage the decline in its traditional markets. Furthermore, the business faces heightened competitive intensity, from established players in the lead-acid space and international cell manufacturers who could exert pricing pressure as the Li-ion market matures.

Market View and Valuation

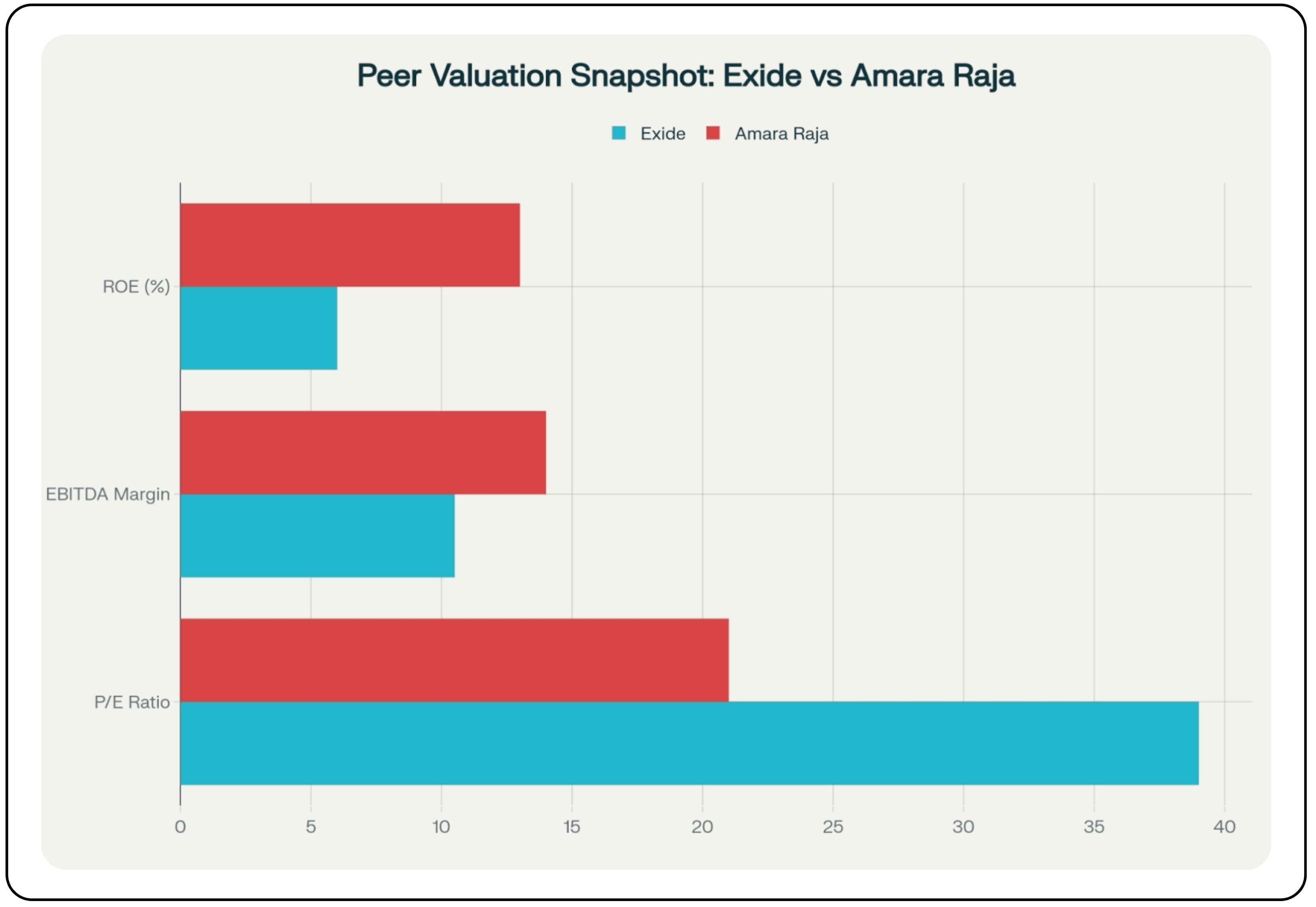

Exide trades at a trailing P/E of ~40x, compared with ~21x for peer Amara Raja Energy & Mobility, implying a material valuation premium.

The valuation premium appears to reflect market expectations of value capture from the company’s lithium-ion investments. Investors are seemingly pricing in the long-term value of its large-scale, vertically integrated factory, anticipating that a first-mover advantage will allow Exide to capture significant value from India’s energy transition. This valuation reflects a bet on a successful transformation, where the strategic potential of becoming a leader in next-generation energy storage justifies paying a premium today.

However, this outlook is balanced by current operational metrics, where the company lags some peers on profitability and efficiency. The market is therefore weighing two narratives: the ambitious, forward-looking growth story against the reality of modest current earnings. The prevailing premium implies that the stock is overvalued and can only sustain its current P/E if the lithium-ion venture delivers as planned.

Bottom Line

Exide Industries represents a classic case of expansion into related ventures from an established market leadership position. The company’s strategy hinges on using the cash flows from its mature and profitable lead-acid business to finance a large-scale entry into the high-growth, but capital-intensive, lithium-ion market.

The success of this strategy depends on several things: Building the factory on time and within budget, learning how to make lithium-ion batteries efficiently, and competing with international companies that might have cheaper products. This path presents considerable execution risks, including adhering to project timelines, managing a steep technological learning curve with inherent initial yield losses, and navigating a competitive market with potential pricing pressures from international players.

If the lithium-ion strategy succeeds, Exide could evolve into a broader energy-storage supplier, which may justify multiple expansions; failure would likely limit upside. Exide’s future valuation will depend on execution - delivering the project on time, controlling costs, and managing the decline of legacy markets while scaling new revenues.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.